The Politics of COVID-19

The politics of the Coronavirus have become ever clearer. Domestically it is evident that Donald Trump wants to return to normal as soon as possible.

It is also clear that the Democrat opposition is much more inclined to take the line of safety first.

There is room for legitimate disagreement over how to handle a public health crisis. But the state of the economy in the run up to the November presidential election is, obviously, also a motivating factor here.

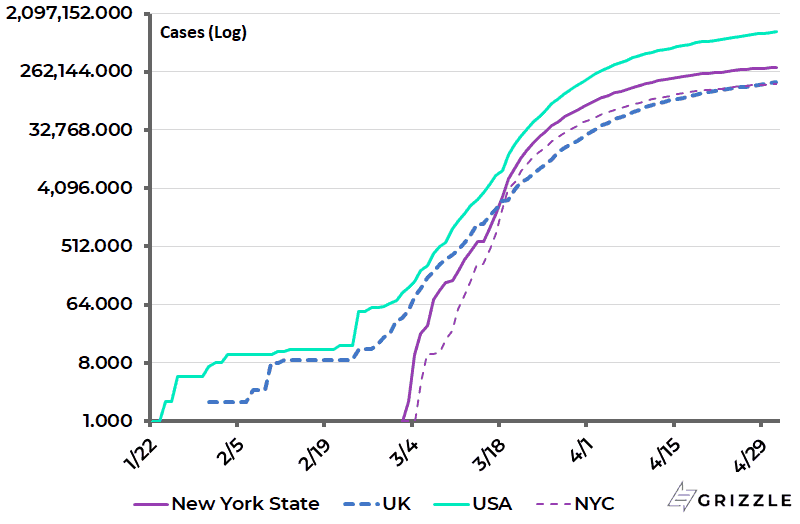

With the spread of Covid-19 in America still less than the worst fears in mid-March (see following chart), it remains inconceivable that President Trump is going to lock down the American economy into a Great Depression and, seemingly, certain electoral defeat.

Coronavirus Cases in America and Britain (log scale)

This suggests an American economy returning to normal next quarter – with a lot of activity resuming in June – just as the Chinese economy is now attempting to return to normal. Still a complicating factor is America’s constitution and which political party controls which state.

China is Coronavirus Economic Base Case

The above is critical for stock markets since the Chinese experience suggests the stock market can look through one quarter of appalling data if there is light at the end of the tunnel.

This is why the biggest risk right now for all world stock markets remains a renewed outbreak of the virus in the mainland economy.

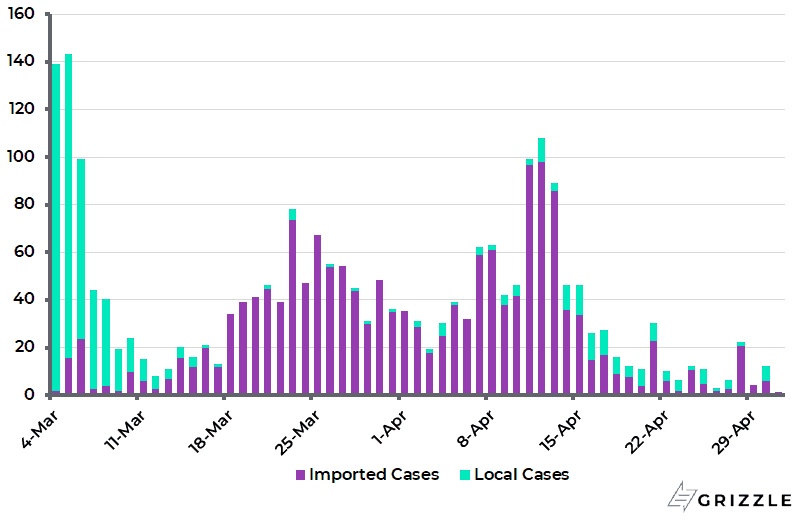

So far that is not happening with the main cluster in Heilongjiang on the Russian border in Northeast China where the problem has been imported infections. There have been 996 new confirmed cases in China since the beginning of April, including 865 imported cases (see following chart), while new confirmed cases totaled 460 in Heilongjiang over the same period.

China Daily New Coronavirus Cases

If it is assumed that China can continue to manage the health issue it will set an encouraging precedent. The other point is the question of how quickly economies can bounce back once controls are lifted.

Here the duration of the virus cycle remains critical. There can be a surprisingly quick bounce back if the virus proves to be a three to four-month cycle. This is, after all, an economic downturn which has been mandated by governments with the service sector hit hardest.

In sectors such as restaurants people can be hired back as quickly as they have been fired. This is why the present downturn is entirely different from previous recessions.

Longer Lockdowns Increase the Risk of a Debt Deflation Cycle

Still if the lockdowns continue for longer than this base case, either because of a renewed outbreak of cases or because governments stick to mistaken lockdown policies for longer than necessary, then the risk of a debt deflation cycle grows dramatically given the prevailing high debt levels.

Such a debt deflation cycle will then trigger even more dramatic government intervention, including ever greater Federal Reserve involvement in the credit markets and even potentially in the stock market.

Still none of this needs to happen if the lockdowns are reversed sooner rather than later. If there was a case for lockdowns, or circuit breakers, to slow the virus to allow hospital systems to cope, that has already been achieved in this writer’s view.

This is why there is a real risk that a continuing lockdown is worse than the virus itself, it terms of the impact on jobs and incomes, most particularly as regards the impact on the young and the poor.

COVID-19 – Baby Boomers Shafting Millennials

In this respect, Covid-19 and the subsequent fiscal spending orgy adopted by panicking governments is, unfortunately, yet another example of baby boomers shafting millennials in terms of the extra government debt burden taken on.

It is not as if the millennials are at great risk of dying from Covid-19. Still assuming, in line with the base case, that the lockdowns end during this quarter, how quickly will economies bounce back?

The End of Lockdown Will Trigger Massive Pent-Up Demand

In this respect, there is a lot of trendy talk at present that the current forced suspension of activity will lead to a change in lifestyle once the virus disappears with a greater appreciation for stay-at-home lifestyles and work-at-home lifestyles. This kind of talk is mostly nonsense, though it should probably be conceded there are some negative implications for commercial real estate.

The view here is quite simple. This is that the end of the lockdowns will trigger massive pent up demand, most particularly in the Western world where many people have continued to be paid a big percentage of their normal wages on furlough schemes.

While in America average weekly unemployment benefits have increased from US$385 a week to US$985 a week, which is more than many people would make in a regular job! This is because under the fiscal stimulus programme, all unemployment insurance claimants will receive an additional US$600 per week through to 31 July.

This is why, by the way, lockdowns in countries such as India and Indonesia are even more disastrous for human welfare and economies since there is no help for small businesses being handed out, nor are there unemployment benefits.

The Spike in Demand Will Trigger an Inflationary “Impulse”

Pent-up demand pressures also raise the potential for an inflation “impulse” resulting from the current crisis. That is despite the fact that the near-term impact will undoubtedly be dramatically deflationary.

This means that inflation may well turn negative in the immediate months ahead, or in other words there will be the dreaded “deflation”!

Still the more the pent-up demand for goods and services is not met because of the inevitable supply-side disruptions caused by the lockdown and the anticipated return to normal, the bigger the potential for such price spikes.

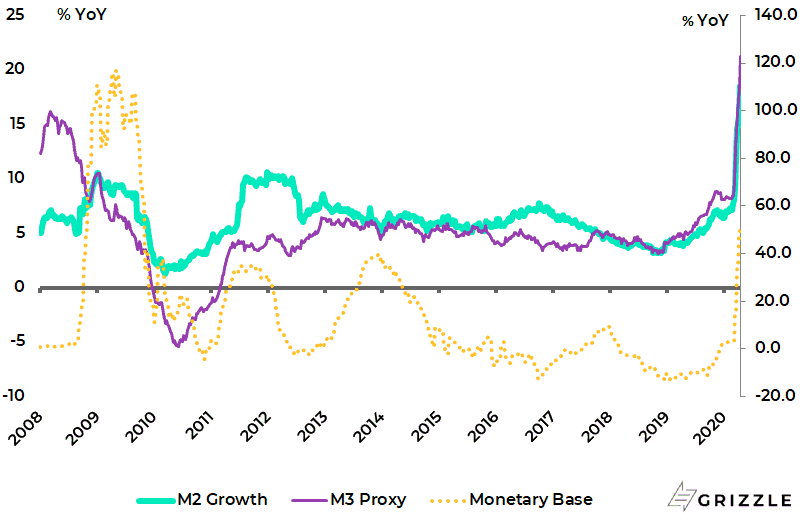

There is certainly the monetary means to accommodate them. In this respect, it is not only narrow money supply which is surging as a result of recent Fed policies.

US monetary base and M2 soared by 49.3% YoY and 18.5% YoY respectively in the week ended 20 April. While a proxy for M3, measured as M2 plus institutional money funds and commercial banks’ large time deposits, rose by 21.3% YoY (see following chart).

US Narrow and Broad Money Supply Growth

This is a different pattern from what happened coming out of the 2008 financial crisis when only narrow money supply surged courtesy of quanto easing. Such an inflation spike would then put pressure on the long end of the government bond market.

It is at that point, if not well before, that the Federal Reserve is expected to adopt its own version of the Bank of Japan’s yield curve control by fixing government bond yields up the yield curve, with similar policies quite likely to be adopted by other copycat G7 central banks.

The introduction of price controls in the US government bond market will mark the introduction of a formal regime of financial repression and a fundamental retreat from the deregulation polices unleashed by Ronald Reagan in the early 1980s.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.