Online Mattress Brand Casper (NYSE: CSPR) reported earnings that largely met expectations but commentary about the impact from the Coronavirus was not taken well by the market.

Management admitted they are seeing an impact to their business which includes store closings and the closing of some suppliers which may end up impacting sourcing of materials.

Management also said they are slowing the rollout of stores this year which will negatively impact growth.

Revenue of $113 million beat the consensus estimate of $110 million by 3%.

However, the earnings loss of -$1.20/sh was worse than the analyst estimate of an -$0.85/sh loss.

The EBITDA loss of $29 million met expectations.

[su_panel] Casper has 9 months of cash left at the current $35 million a quarter burn rate which is low. it is also growing at half the rate of Purple, its largest competitor. Management may come under pressure to issue more shares or borrow debt if they don’t start generating cashflow by the end of the year. Investors should own Purple (NASDAQ: PRPL) instead due to Casper’s inferior growth and liquidity risk. [/su_panel]

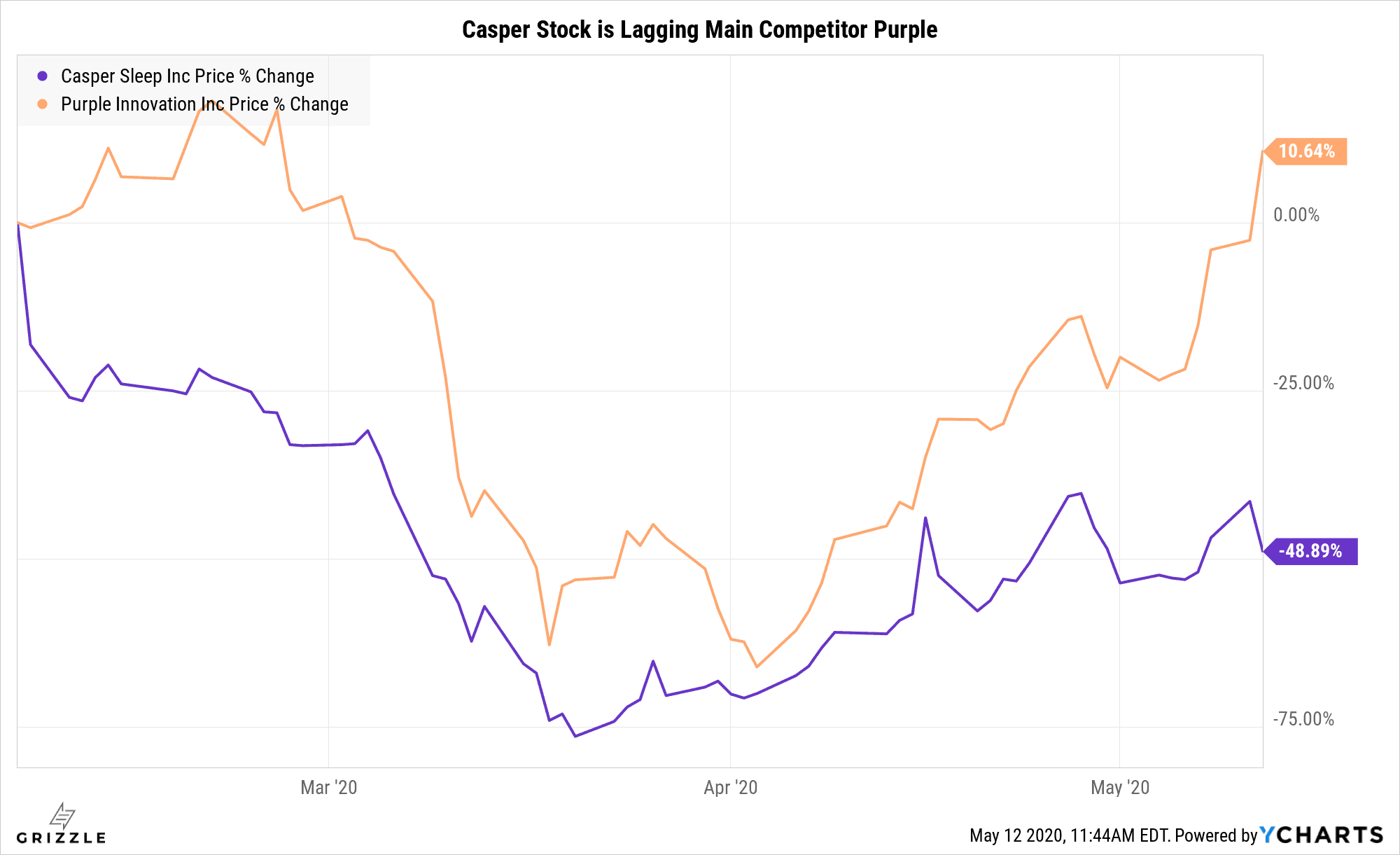

Casper has been a dog since its IPO, severely lagging its main competitor Purple Innovation.

The stock remains 50% below its IPO price which was already lowered 40% from where the company originally thought they could sell shares ($20/sh).

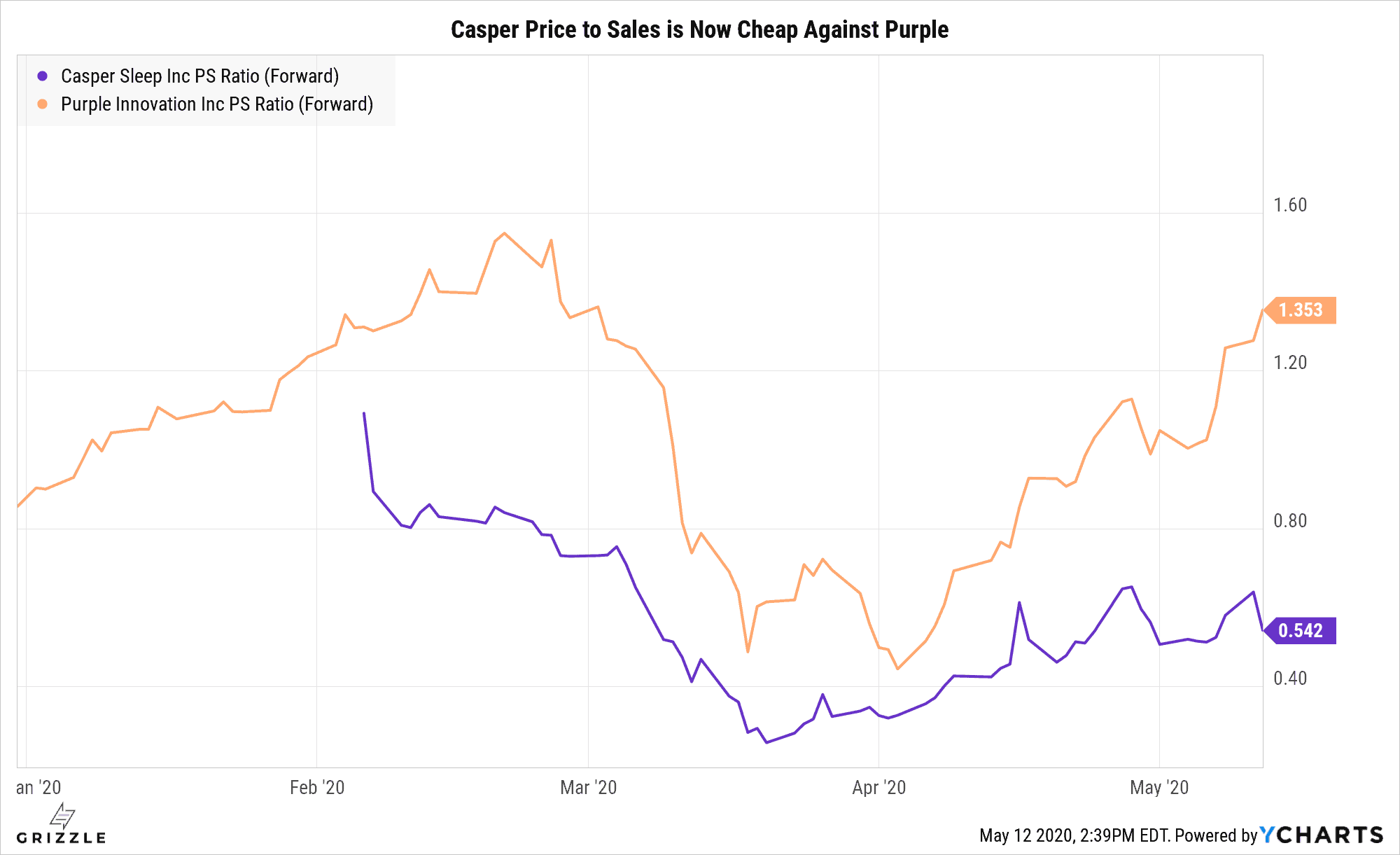

Casper’s price to sales multiple is now downright cheap compared to competitor Purple Innovations.

This is likely due to the superior growth profile and profitability of Purple coupled with the problems management is facing from empty retail stores, the low cash level and sourcing issues.

Casper Price to Sales Multiple Closer to Where it Should Be

Stock is Worth No More than $9.50 per Share

We dug deep into this stock for our IPO Guide to see what the true value of this company likely way and we came back with $8.00/sh.

However as interest rates have fallen since then, the valuation is now up to $9.50/sh.

Looking at Grizzle’s stock price tool you can see it has been very helpful so far at picking bottoms and tops in this stock.

Stocks often trade for more and for less than they are truly worth and Casper has been no exception.

The stock got close to our fair value this week before the dramatic drop today on earnings.

At $6.70/sh Casper is now looking like a bit of a bargain, though the stock could come under pressure if management can’t generate positive EBITDA in the next six months.

Casper has $15 million of debt due this year and $50 million due in five years against $116 million of cash.

Casper has a little under 9 months to generate cashflow or they will have to issue more stock which could put pressure on the stock price.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.