The Federal Reserve has duly delivered on the expected softening of the inflation target in the latest FOMC meeting in mid-September.

The key point is that the Fed has now given itself formally the room to overshoot the 2% inflation target, though by what magnitude remains unspecified.

That will presumably hinge on what is being signaled by inflation expectations.

In that sense, the Fed’s obsession with inflation targets and inflation expectations remains.

But what was perhaps less expected is that Pivot also effectively signaled that the Fed no longer believes in the Phillips Curve, or at least will not feel bound to raise rates just because the labour market is tightening.

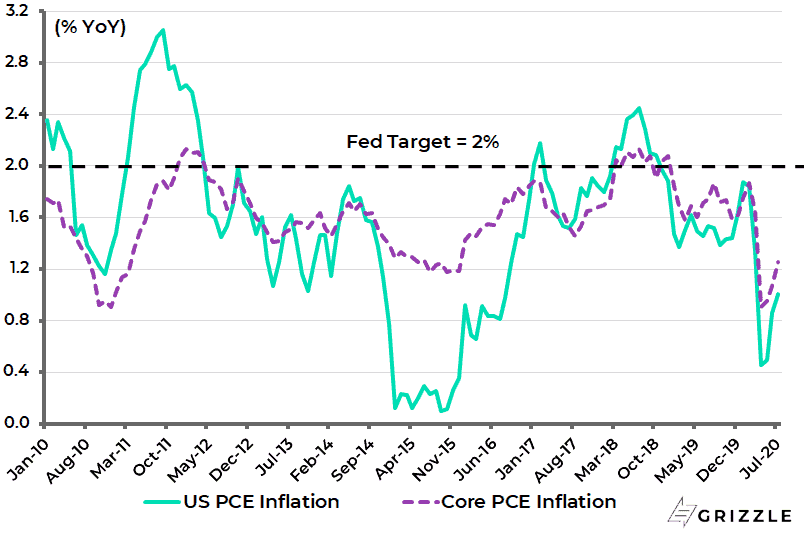

For those who want to monitor the extent to which the Fed has in recent years undershot its inflation target on its favoured core PCE measure of inflation, the chart below makes clear the potential latitude to overshoot.

Core PCE has been under 2% for 11 of the past 12 years.

US PCE inflation

Meanwhile, the new Fed policy, is, as far as this writer is concerned, another long-term reason to sell US dollars and buy gold or indeed bitcoin.

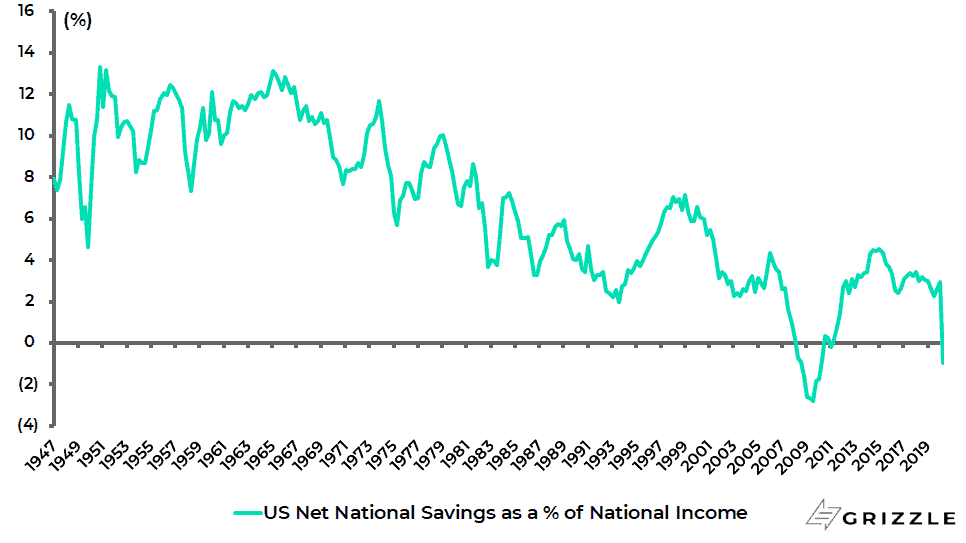

On the point of a weaker US dollar, the latest revisions to the US GDP data have triggered another deterioration in America’s national savings trend.

US net national savings; measured as the sum of savings by businesses, households and the government sector, adjusted for depreciation, declined from 2.9% of national income in 1Q20 to a negative 1.0% in 2Q20.

This is primarily due to an increase in government dissaving (i.e. a rising fiscal deficit).

US National Savings as % of Gross National Income

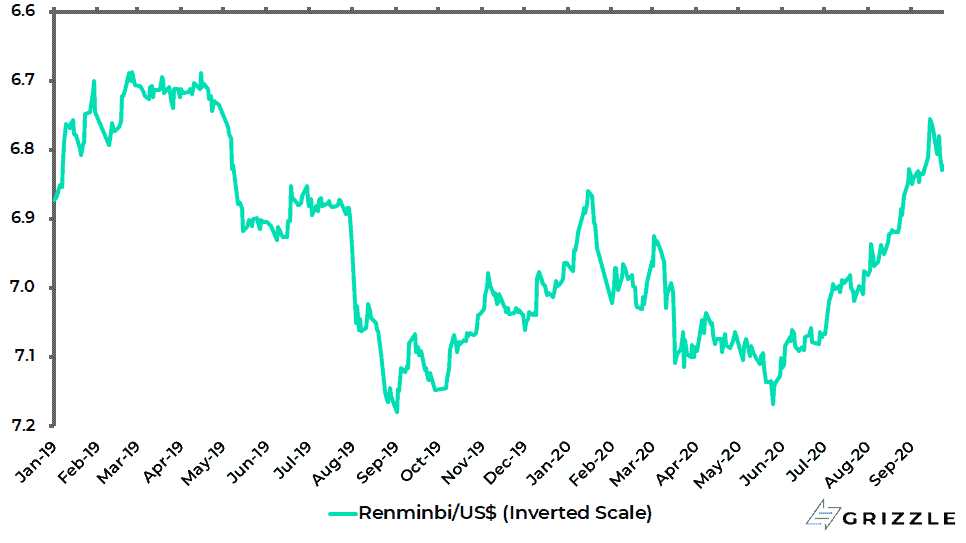

Still, there is another trade suggested by the new Fed licence to overshoot.

That is to sell the dollar and buy the renminbi since the PBOC is the last remaining bastion of orthodoxy in the world of central banking.

Renminbi/US$ (inverted scale)

The 10-year Chinese government bond currently yields 3.13%.

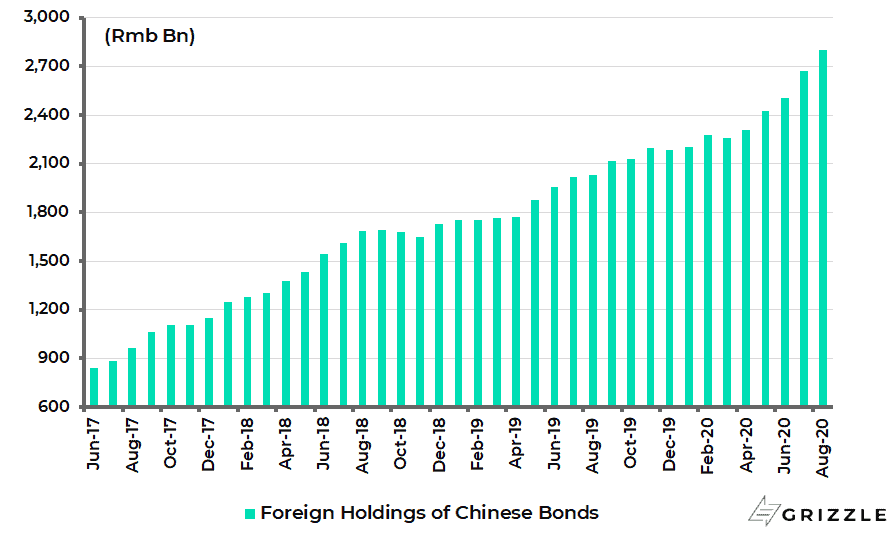

It is also why foreign investors continue to pour money into the Chinese bond market, a trend again confirmed with the latest data for August.

Foreign holdings of Chinese bonds increased by another Rmb130bn in August and by Rmb615bn or 28% in the first eight months of 2020 to Rmb2.80tn.

Foreign Holdings of Chinese Bonds

The commitment to orthodoxy also has positive implications for the Chinese currency, the renminbi.

The Chinese policy response to the pandemic has been remarkably constrained compared with the Gadarene swine-style panic witnessed in the G7 world.

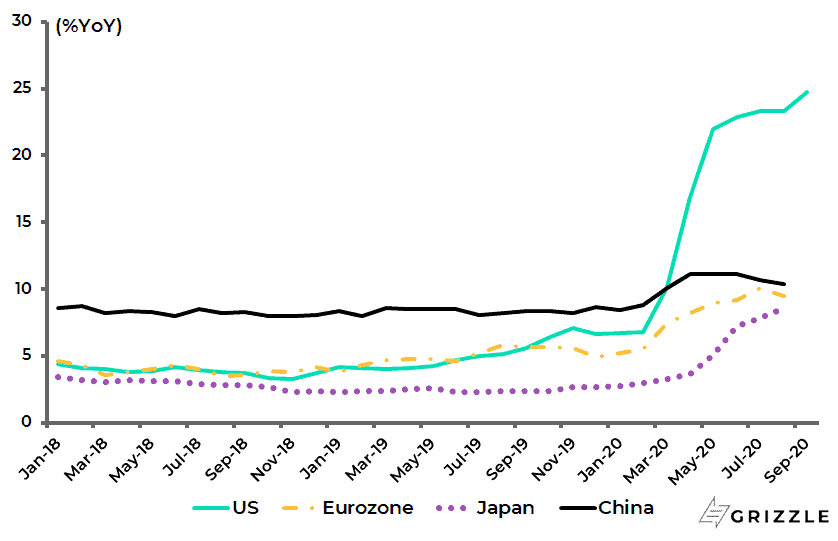

This is illustrated by the stark contrast between the modest increase in broad money growth in China compared with the surge in America, Eurozone and even Japan.

US M2 growth has risen from 6.7% YoY in December to 24.7% in mid-September, while Japan M2 growth and Eurozone M3 growth were up from 2.7% and 4.9% in December to 8.6% and 9.5% in August.

By contrast, China M2 growth has risen from 8.7% YoY in December to 10.4% YoY in August.

US, Japan, Eurozone and China Broad Money Growth

This more cautious approach was articulated in a speech in June by Guo Shuqing, chairman of the China Banking and Insurance Regulatory Commission (CBIRC) and the senior party official in the People’s Bank of China.

Commenting that many countries had rolled out fiscal policies and financial incentives of “unprecedented scale and intensity” in response to the pandemic, Guo stated:

This quote is directly from the English translation of the speech published by the BIS (see Guo’s speech: “Accelerate the normalization of economic activity and further reform and open up the financial system” at the 12th Lujiazui Forum in Shanghai, 18 June 2020).

Such a stance is clearly renminbi-positive.

In this respect, this writer continues to hear predictions of a market-driven collapse in the renminbi or a devaluation engineered by Beijing to restore its export competitiveness.

These predictions have proved very wrong in the past and will likely continue to be proven wrong.

China is a domestic-demand-driven economy, which is why the last thing Beijing wants is a major devaluation, which would reduce the purchasing power of Chinese consumers in US dollar terms.

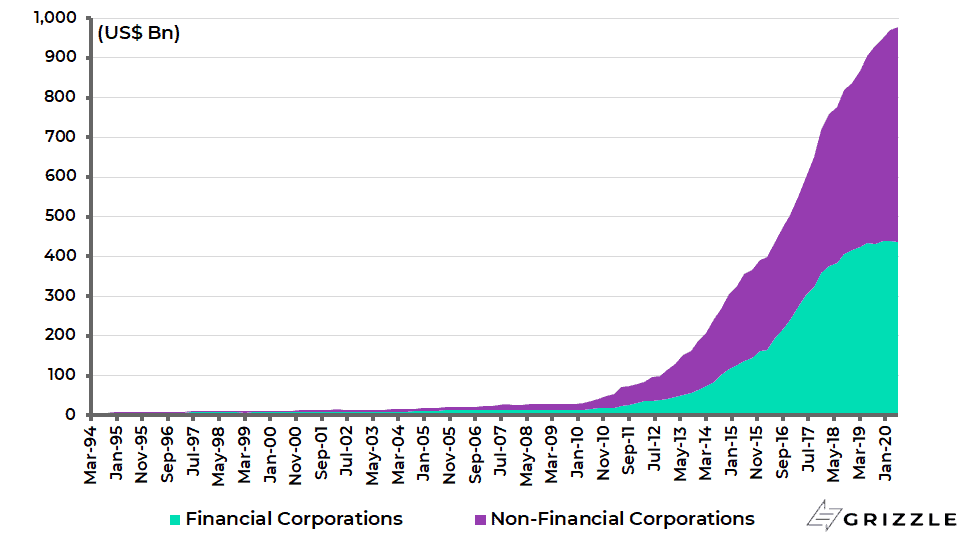

It is also the case that a stronger renminbi will make it easier for Chinese corporates to service and repay offshore US dollar borrowings.

Chinese corporations’ US dollar- denominated international debt securities outstanding have increased from US$49bn at the end of 2010 to US$977bn at the end of 2Q20, according to the BIS.

Chinese Corporations’ US Dollar-Denominated International Debt Securities

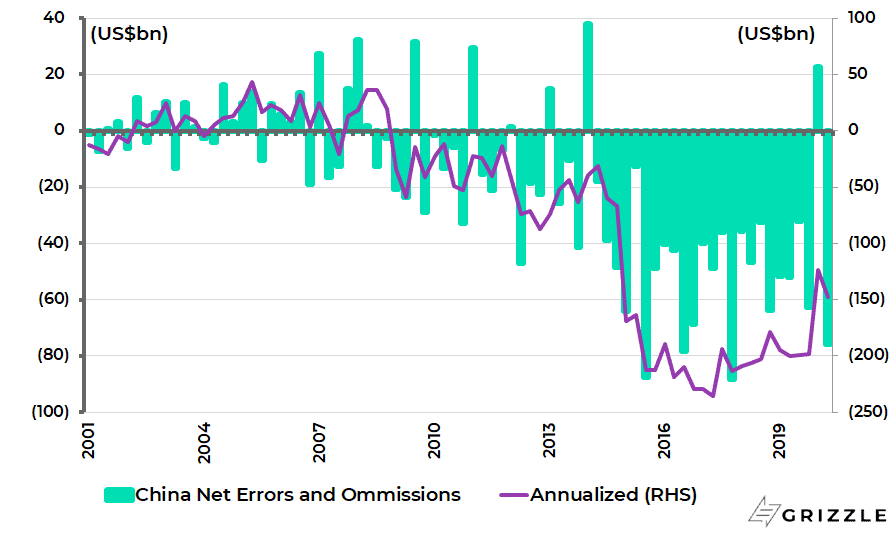

Meanwhile, the fact that the first quarter of this year was the first in six years not to show capital outflow pressure on the net errors and omissions item in the balance of payments shows that China’s relatively orthodox policy is beginning to attract capital inflow.

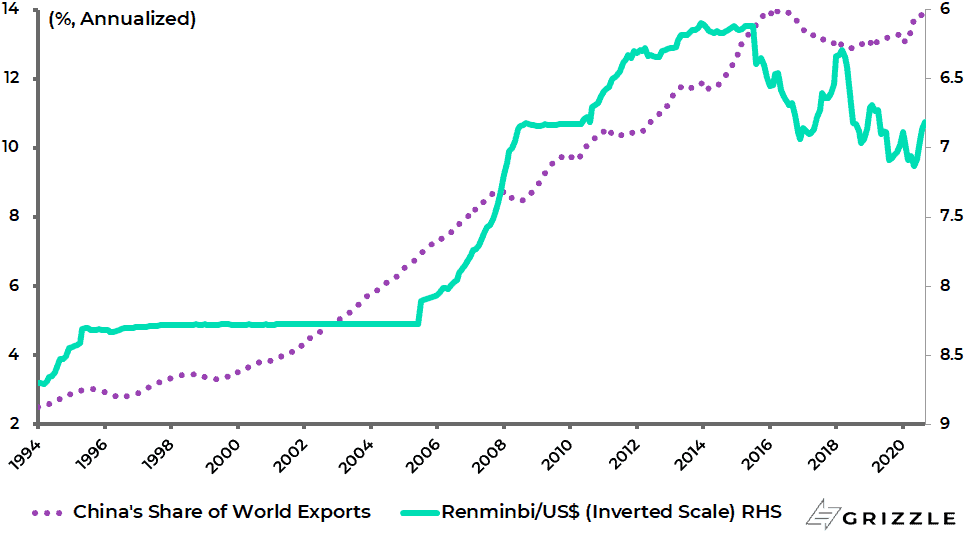

It should also be remembered that, for all the continuing talk of China needing to devalue its way out of trouble, the track record suggests that China has done a remarkable job of maintaining its share of world exports despite the significant appreciation of the renminbi since 2005.

China Balance of Payments: Net Errors and Omissions

China’s share of annualized world exports rose from 7% in 2005 to a then peak of 14% in 2015 and was 13.9% in June, despite a 21% appreciation of the renminbi against the US dollar since 2005.

China’s Share of World Exports and Renminbi/US$ (inverted scale)

This should have risen to a new peak by now with China’s exports rising by 9.5% YoY in US dollar terms in August.

Clearly, part of that rise is China taking market share as its factories reopened in 2Q20 while factories elsewhere remained closed.

Remember that China is one quarter ahead of the rest of the world in the pandemic cycle.

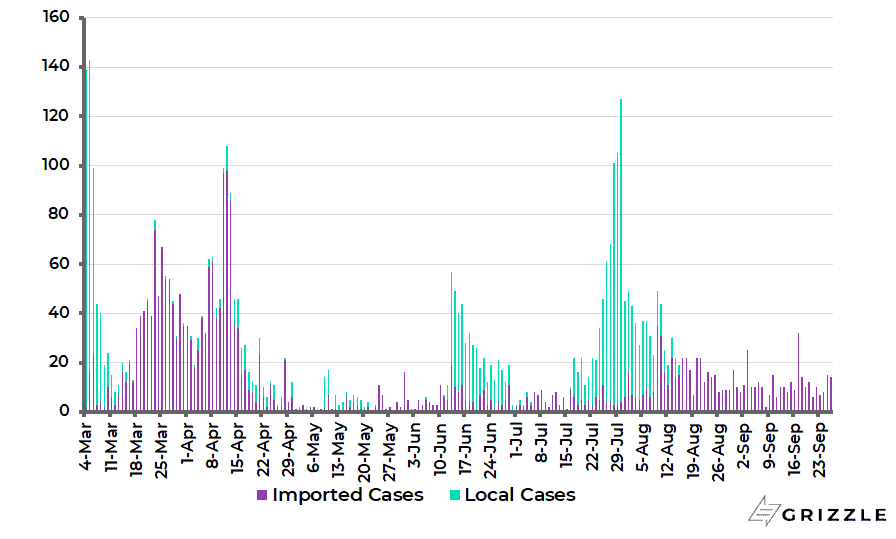

COVID-19 also remains remarkably under control in China.

There have been only 11 new cases per day, on average, in September, with no new locally transmitted cases since mid-August and no new deaths since mid-April.

China Daily New COVID-19 Cases

The investment conclusion from all of the above is that investors are recommended to own both the renminbi and Chinese equities.

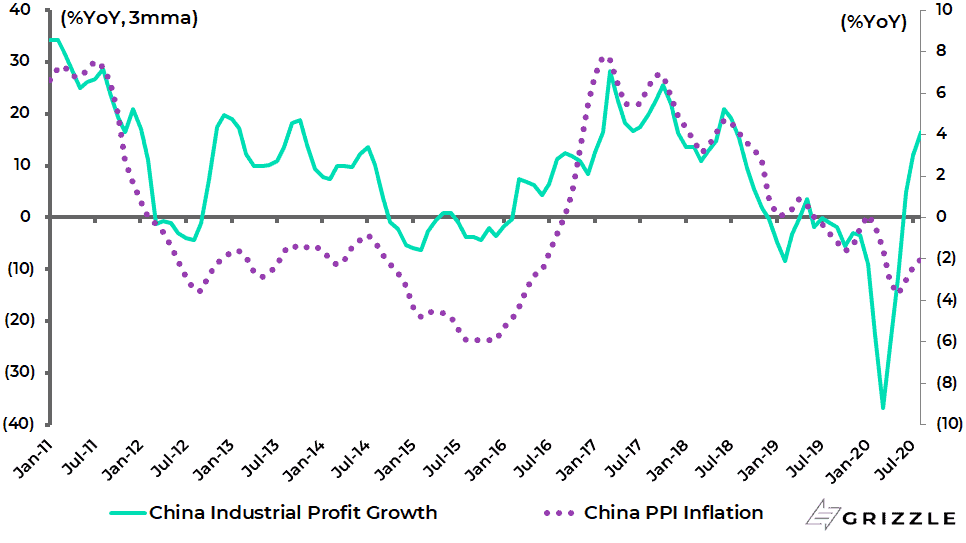

The continuing cyclical recovery was signaled by the latest data for industrial profits which, as usual, have turned up along with PPI.

China industrial profits rose by 19.6% YoY in July and 19.1% YoY in August, up from 11.5% YoY in June and from a 38.3% YoY decline in January-February.

While PPI has improved from -3.7% YoY in May to -2.0% YoY in August.

China Industrial Profit Growth and PPI Inflation

Still, if China remains promising, it is the case that China increasingly dominates the global emerging market asset class, accounting for 42% of the MSCI emerging markets benchmark index.

And this is not taking into account the increasing weighting of China domestic A shares in the future.

For such reasons, it is increasingly easy to imagine future growth in “China only” investment mandates combined, maybe, with global emerging market ex-China mandates.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.