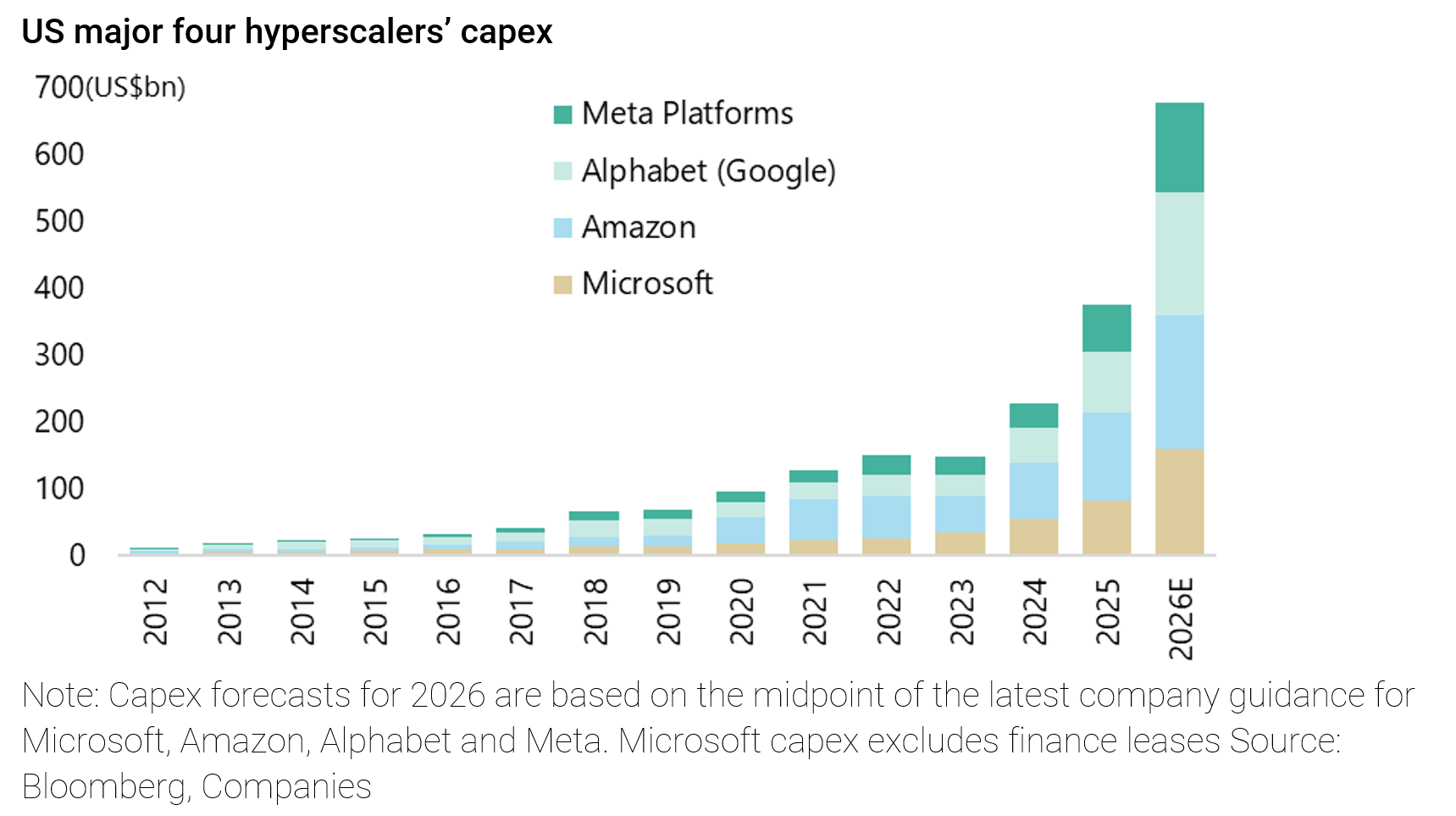

The key medium-term issue for the US stock market at the start of 2026 remains whether the hyperscalers will be able to monetise their AI capex, which this year is now forecast to reach a staggering US$680bn for the major four US hyperscalers following the latest earnings guidance.

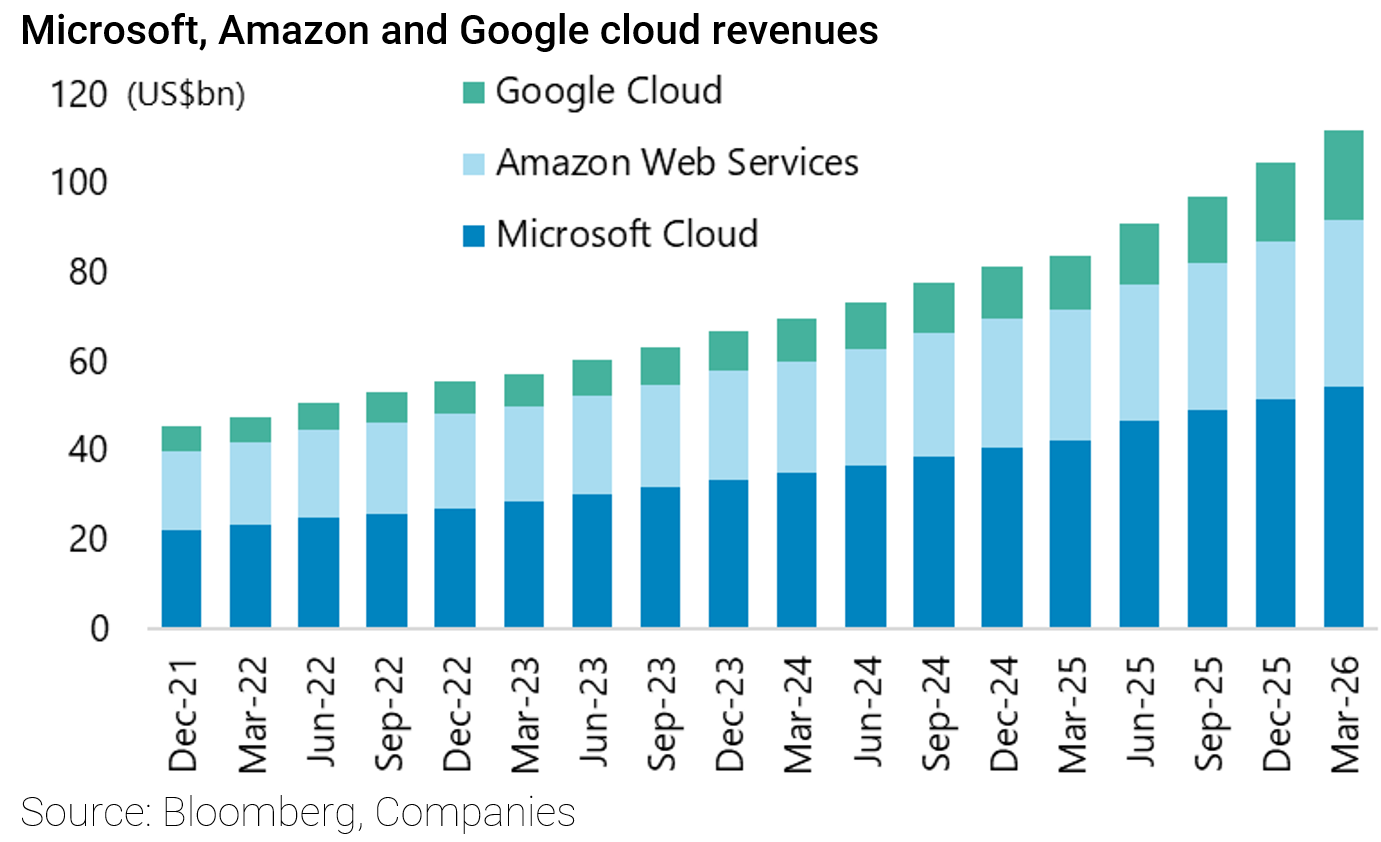

The market has viewed the increased capex for Alphabet, Microsoft and Amazon as positive because it has seen growing revenues in their cloud businesses.

Google Cloud’s revenues rose by 63% YoY last quarter, while Amazon Web Services (AWS) and Microsoft Cloud increased revenues by 28% and 29% YoY respectively.

Still there is an element of circularity here since cloud is benefitting from the pickup in demand from the likes of OpenAI and Anthropic.

The real winner from the AI capex thematic in stock market terms remains the picks-and-shovels trade with the huge gains in the three global suppliers of DRAMs, two of which are quoted in the Korean market.

This has been the main driver of very positive earnings revisions in both the US and Asian equity universes.

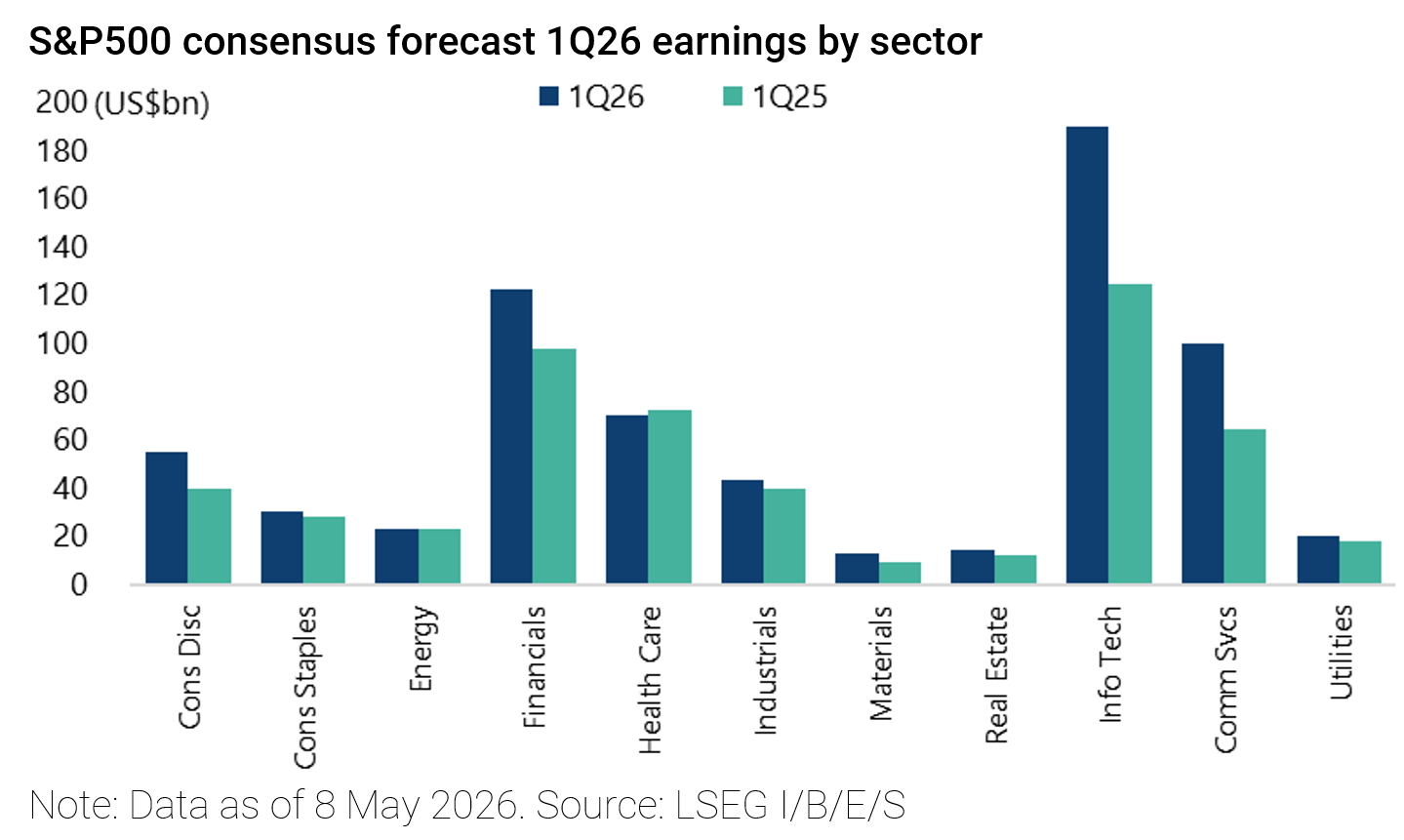

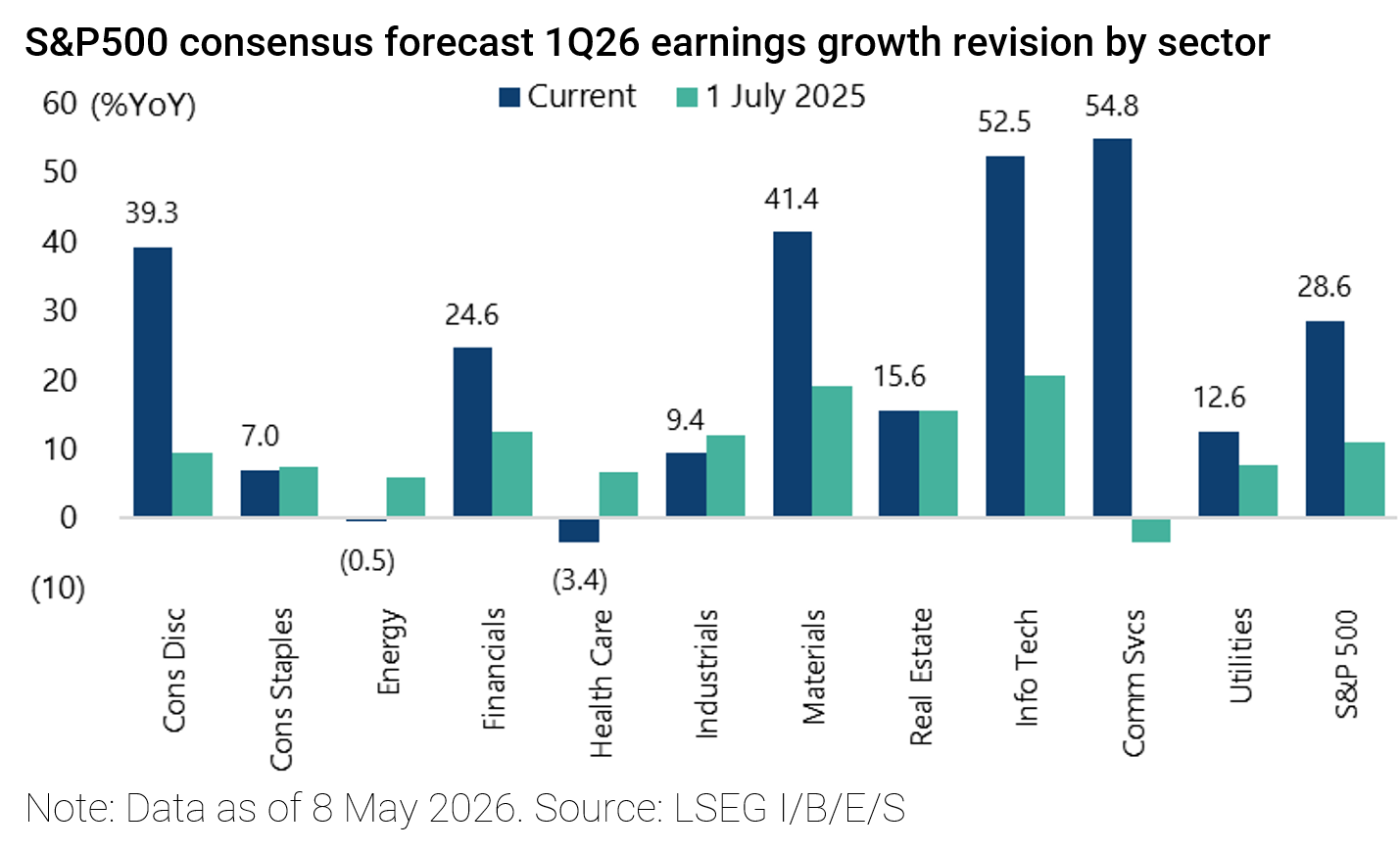

The LSEG I/B/E/S consensus data as of 8 May shows that S&P500 1Q26 earnings are expected to rise by 28.6% YoY, up from 10.9% growth expected last July.

The IT sector now has the second-highest forecast 1Q26 earnings growth of 52.5%, up from 20.7% last July.

Thus, the IT sector is expected to earn US$190.1bn in 1Q26, up from US$124.6bn in 1Q25, with all 12 sub-industries in the sector having higher earnings than a year ago.

Earnings for the IT sector account for 27.9% of the I/B/E/S forecast 1Q26 earnings for the S&P500, up from 23.5% in 1Q25. Unsurprisingly, the semiconductors and electronic components sub-industries have the highest earning growth (110.2% and 54.7%, respectively).

If these two sub-industries are excluded, the forecast growth rate for the IT sector declines to 27.1%.

Meanwhile, the Communication Services sector, which includes Alphabet and Meta, has the highest forecast 1Q26 earnings growth rate of 54.8%.

As for Asian equities, consensus 2026 earnings growth for the MSCI Asia Pacific ex-Japan universe is now 37%, but “only” 13% if Korea and Taiwan are excluded.

Consensus 2026 forecast EPS for the MSCI Asia ex-Japan universe has been revised up by 17% over the past three months, with the IT sector earnings being revised up by a massive 54%.

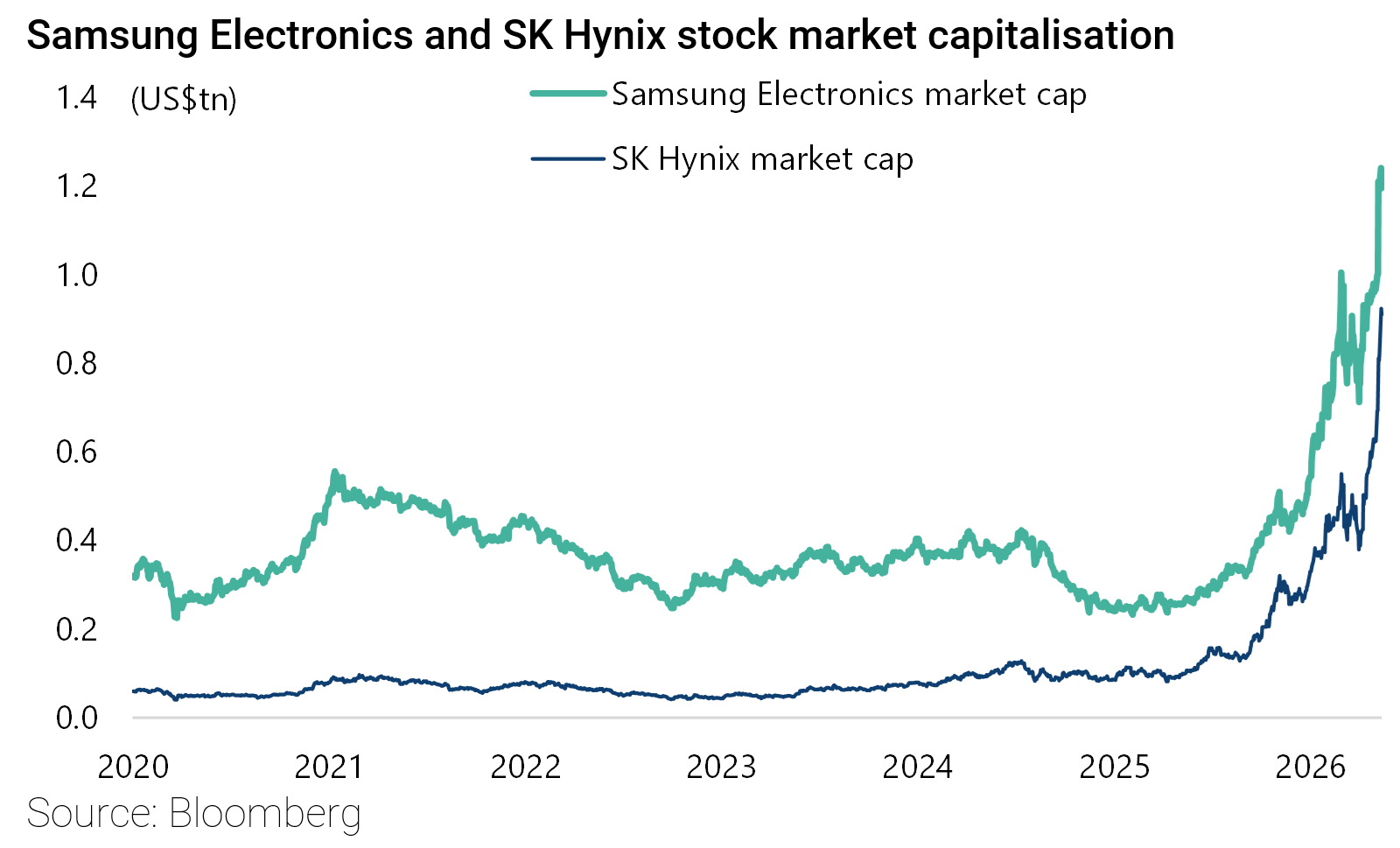

The result has been a dramatic rise in the stock market capitalisation of the likes of Samsung and Hynix.

Their profits this year are now forecast, for example, to be more than three times the total forecast profits of the benchmark Nifty 50 Index in India.

Samsung and Hynix are forecast by consensus to earn profits totalling W452tn (US$307bn) this year, compared with the total forecast profits of US$102bn for India’s Nifty 50 universe.

Still, it should be noted that the DRAM makers book their revenues up front, highlighting the front-end loading of profits.

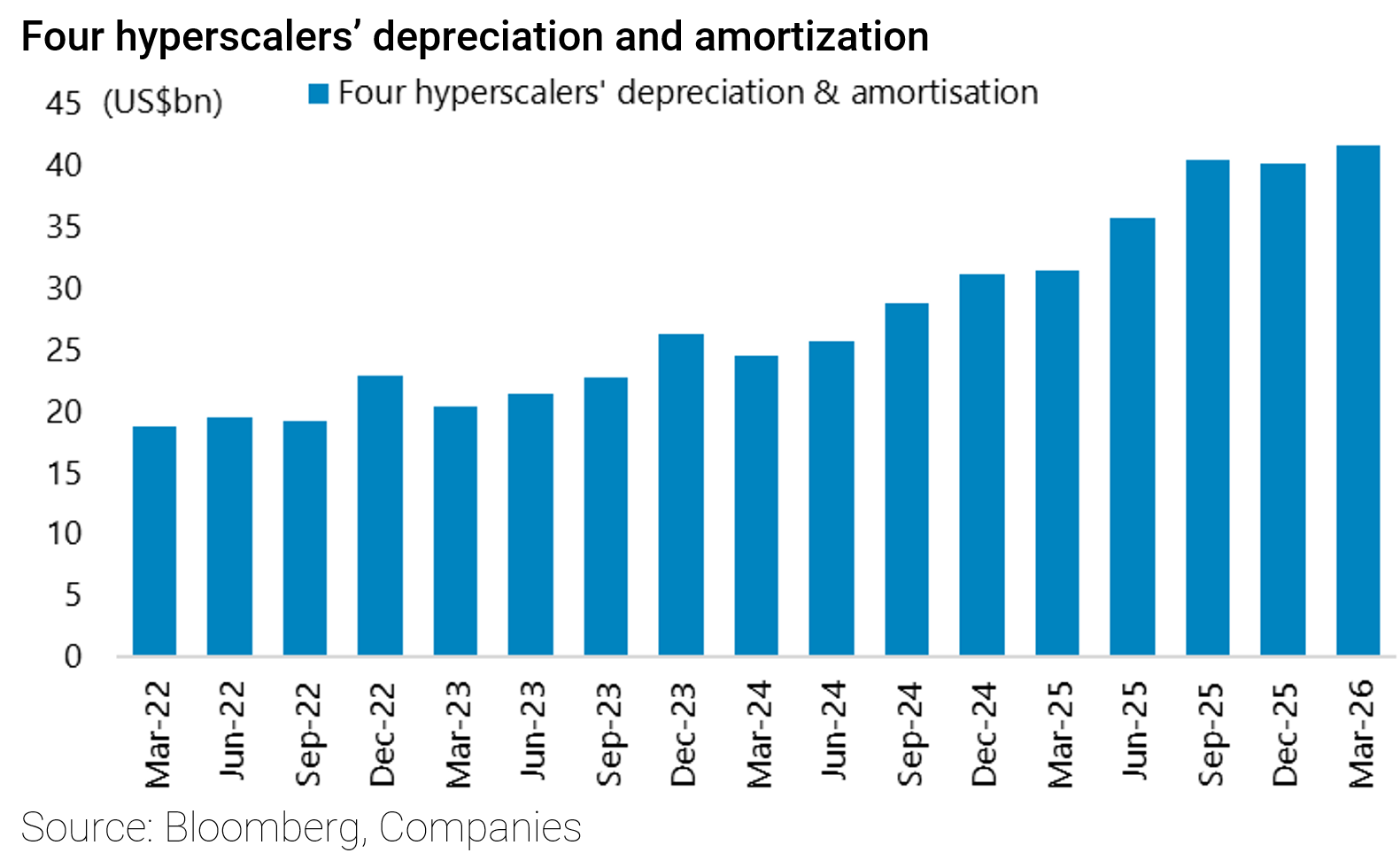

By contrast, the hyperscalers are delaying the payment of the AI capex via extended depreciation schedules.

Still, the deprecation bill is rising.

The four major hyperscalers collectively spent US$130bn on capex in 1Q26, but their depreciation expenses were only US$41.6bn, though up 33% YoY (see following chart and WSJ article: “The Clock Is Ticking for Big Tech to Make AI Pay”, 30 April 2026).

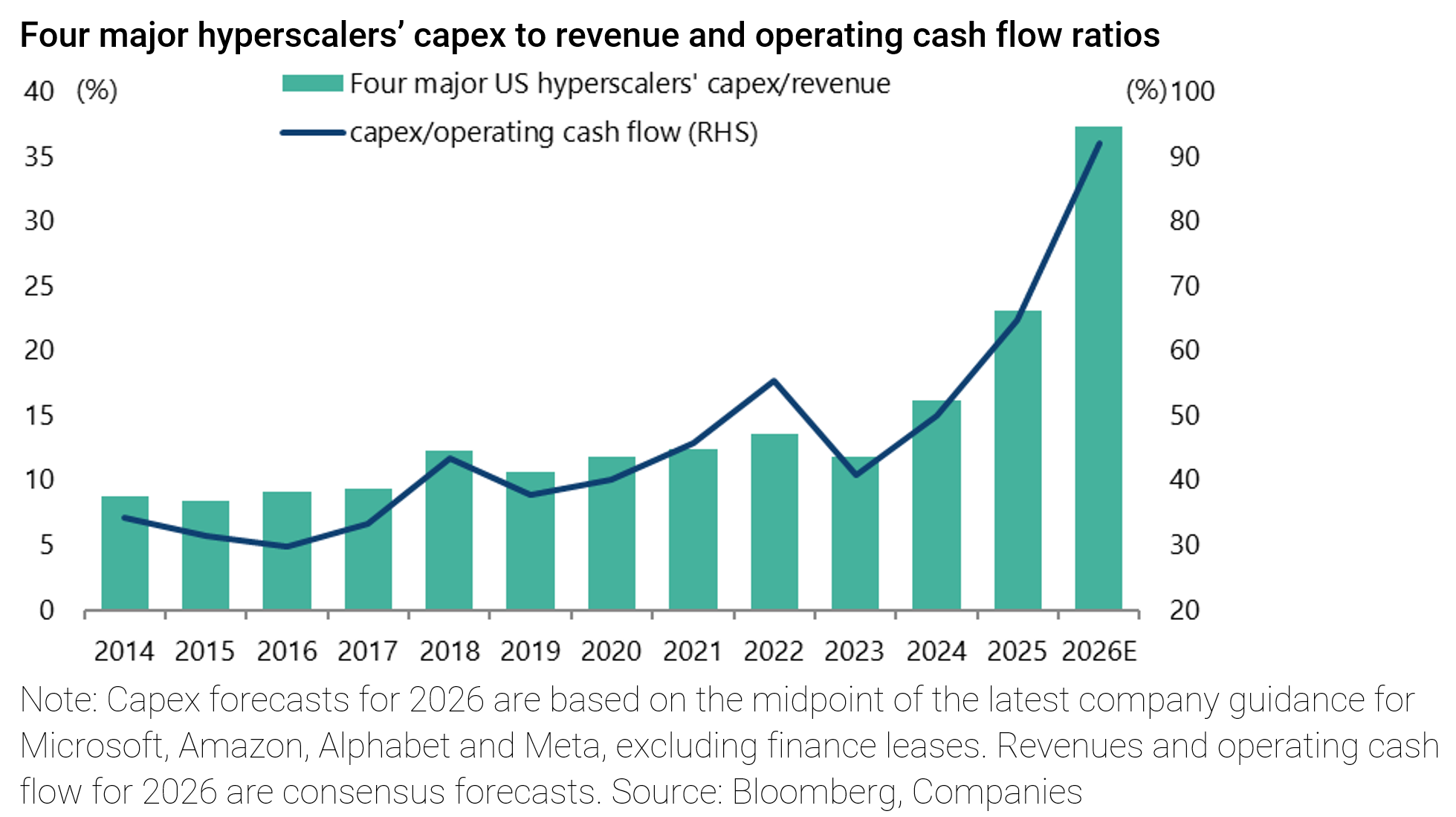

Still, the impact on their free cash flow is already dramatic.

The four hyperscalers’ capex to operating cash flow ratio has risen from 41% in 2023 to an estimated 92% this year, based on consensus operating cash flow forecasts.

In the case of Meta, this is already being construed as a negative because Meta does not have a cloud business.

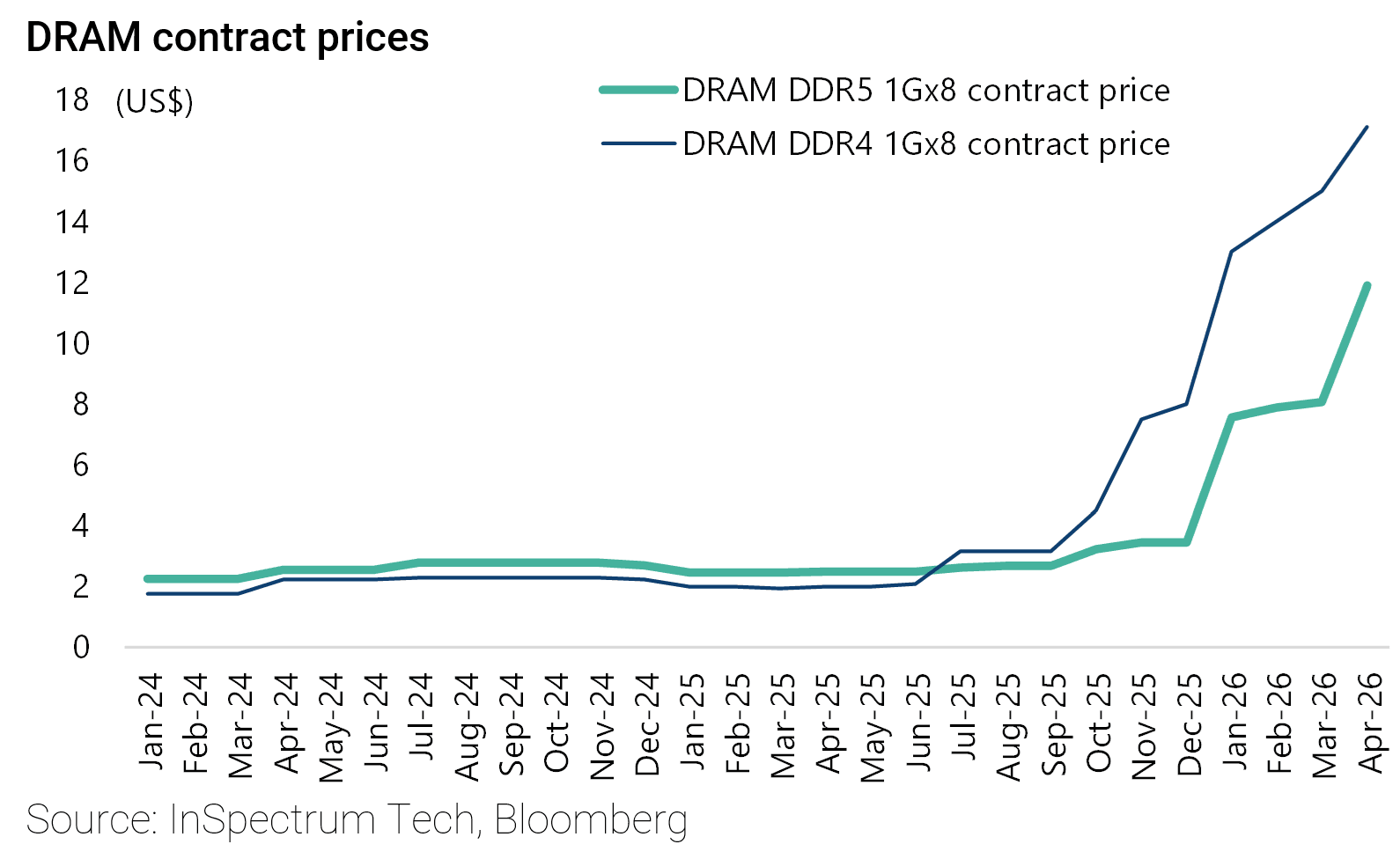

The surging cost of compute, as reflected in DRAM prices—which have risen by 340-440% since the beginning of 4Q25 — means that the cost of using AI will surely have to increase.

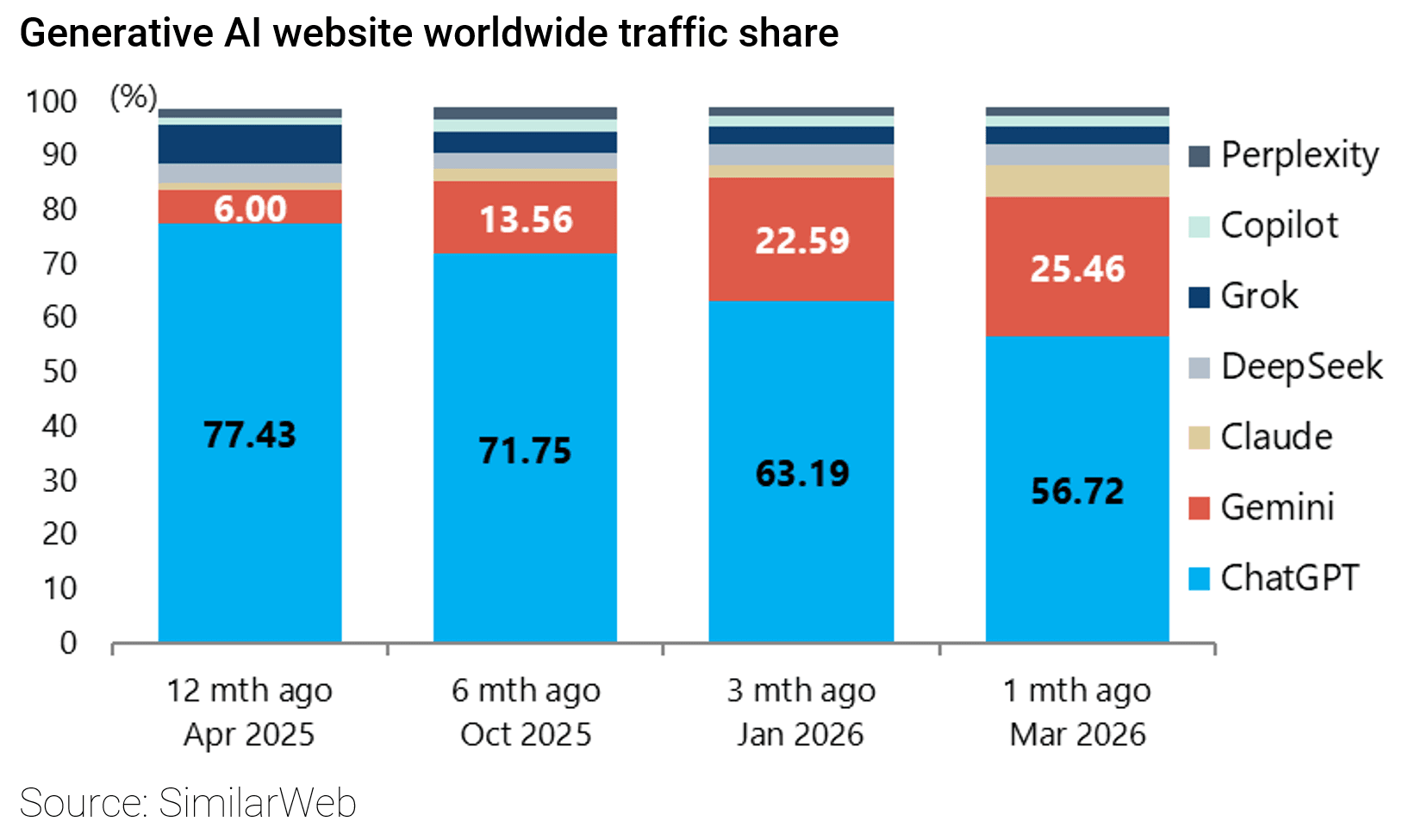

ChatGPTs Declining Market Share

So far, the case for monetization is far more proven in the corporate market with the success of Anthropic than is the case in the consumer market.

Meanwhile, in the latter, OpenAI continues to lose market share to Alphabet’s Gemini.

Gemini’s web traffic in the Generative AI market has increased from 6.0% to 25.5% over the past 12 months to March, while ChatGPT’s market share has declined from 77.4% to 56.7% over the same period, according to SimilarWeb.

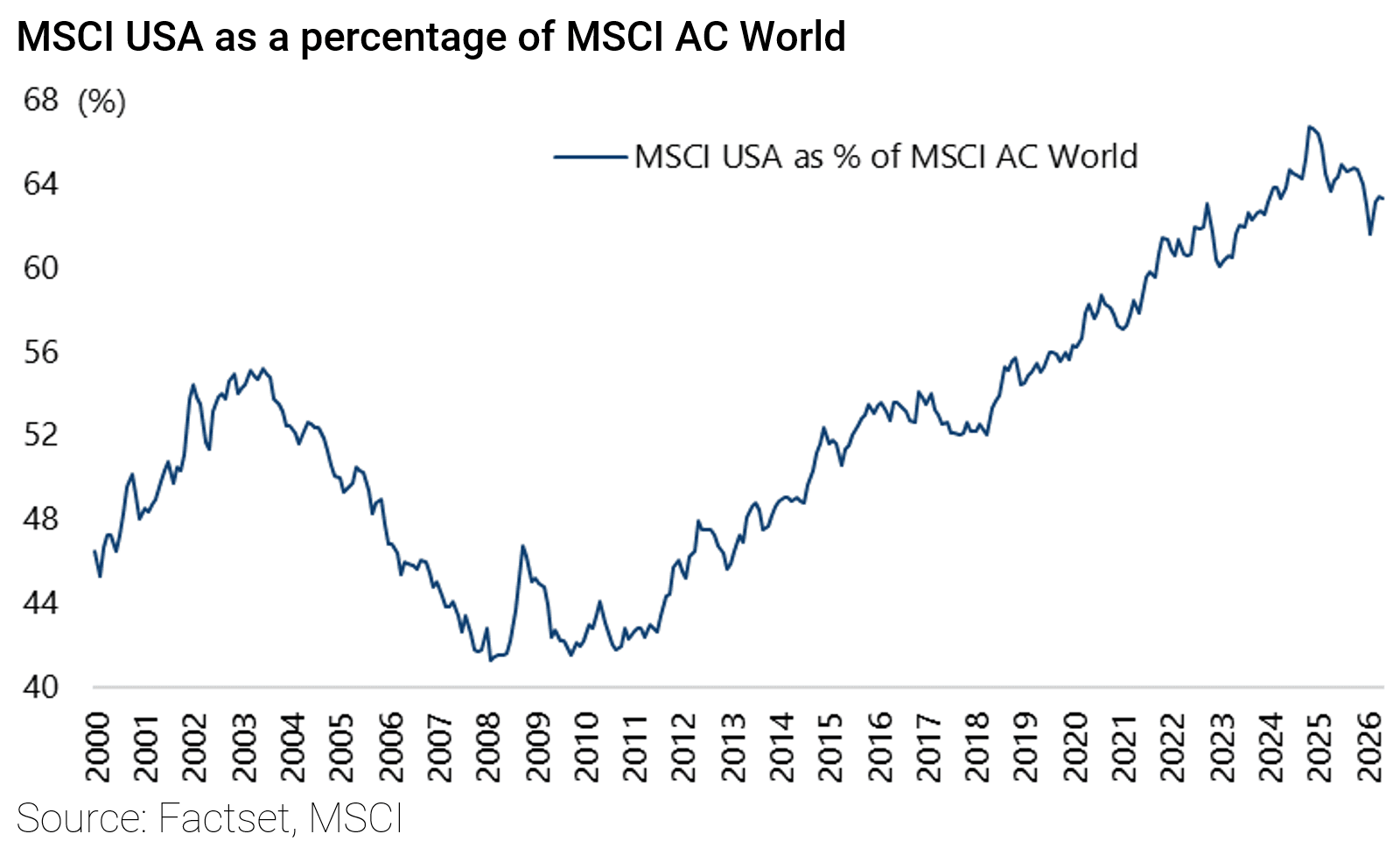

The US Stock Market Share of Global Value has Peaked in Our View

Meanwhile, the base case remains that the US made an all-time peak as a percentage of the MSCI All Country World Index of 67.2% on 24 December 2024.

It ended last year accounting for 64.0% and is now 63.3%.

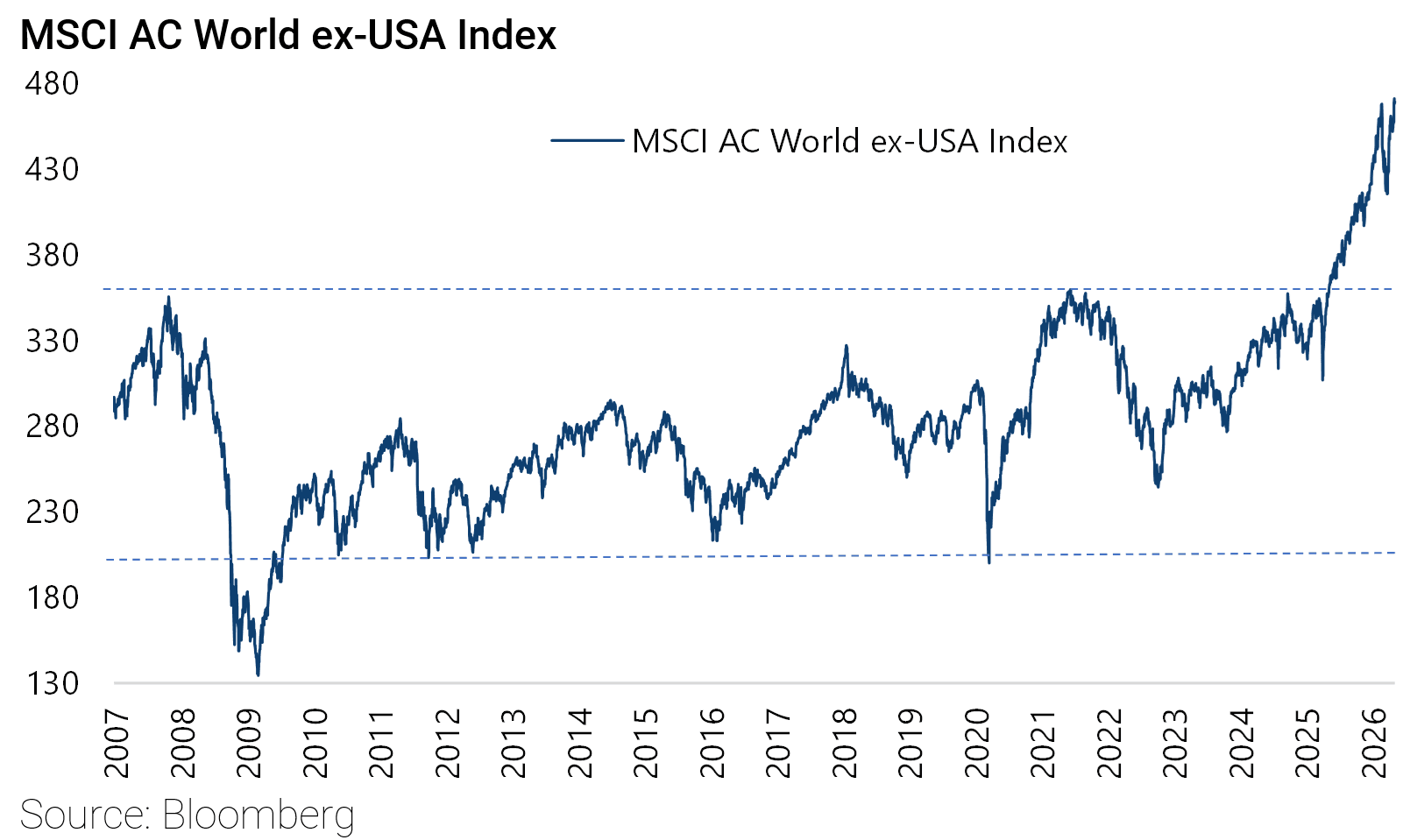

The MSCI AC World ex-US Index broke positively out of an 18-year trading range last year supporting such a view.

Still, the Iran war, so long as it continues, is a positive for America relative to Europe and Asia, since the US is clearly less dependent on imported energy.

The risk to the above view of the US having made an all-time peak remains that the hyperscalers successfully monetise their AI capex.

US Economic Growth Continues to Rely on AI Spending

The other bull story for US equities at the start of this year was a projected broadening out of capex beyond the AI area as a result of some of the provisions in the Trump administration’s One Big Beautiful Bill Act (OBBBA), most particularly the temporary window for bonus depreciation.

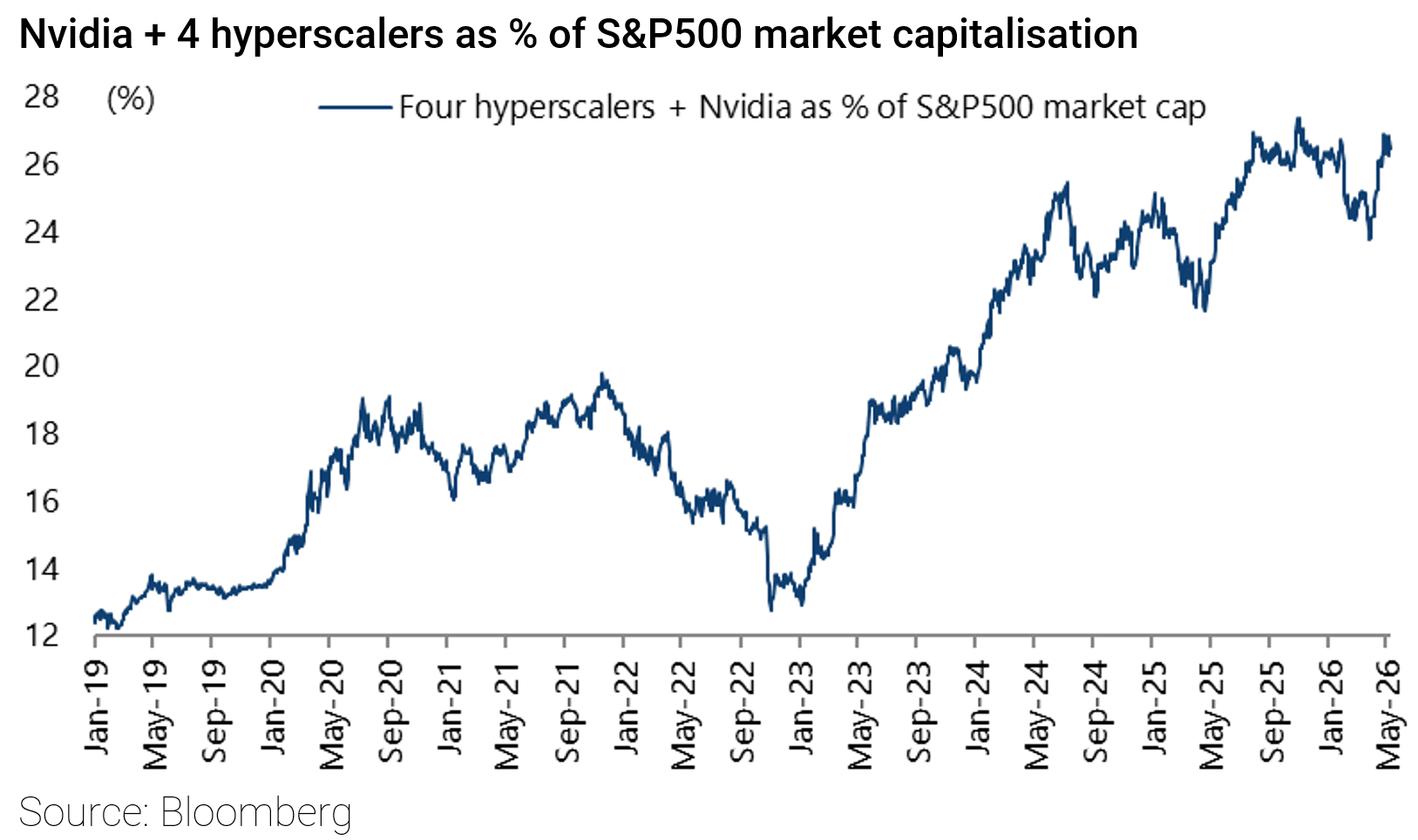

If this is a potential positive, and would certainly suggest a broadening out of the stock market, the reality is that the AI theme has been driving the American stock market for the past three years and continues to do so.

The four major US hyperscalers plus Nvidia accounted for a record 27.4% of S&P500 market capitalisation on 3 November 2025 and are now 26.5%, up from 12.9% in early January 2023.

They also account for an estimated 43% of the gains in the S&P500 since the beginning of 2023.

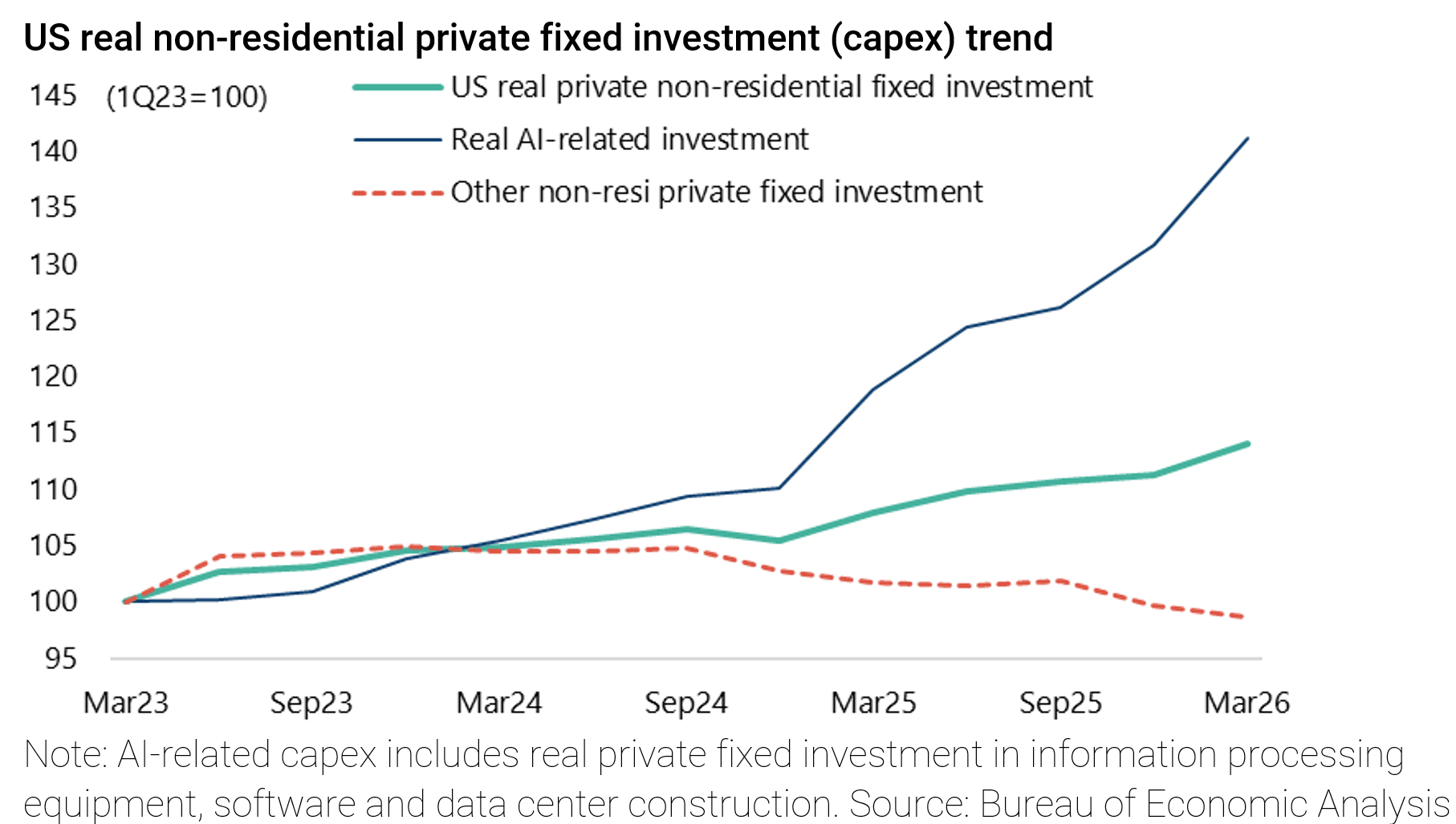

The other reality is that the first-quarter US GDP data has again confirmed the continuing huge gearing of the US economy to AI capex and the lack of any evidence thus far of a pickup in capex outside AI.

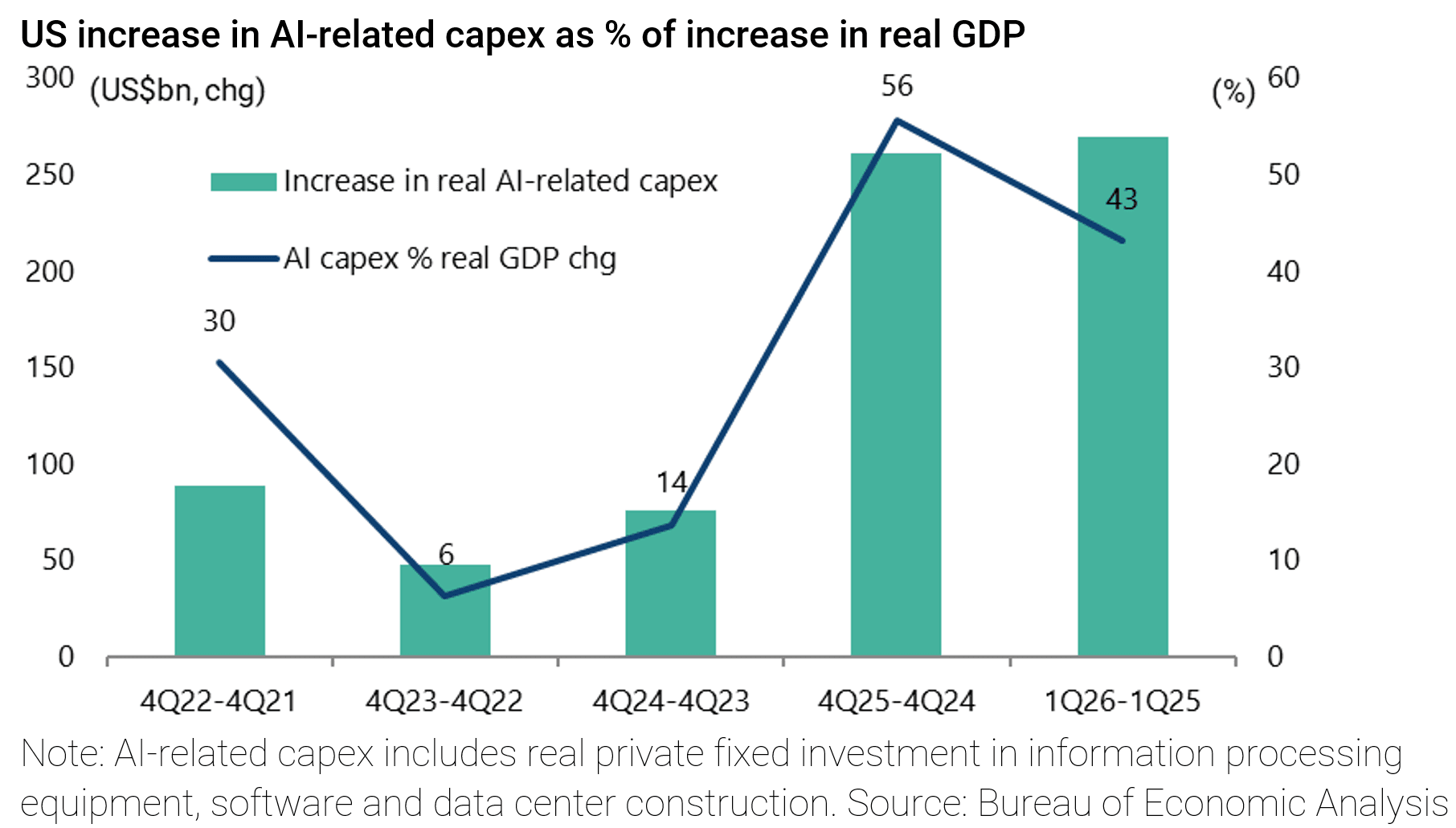

US real AI-related capex, measured as nonresidential private fixed investment in information processing equipment, software and data center construction, contributed 1.15ppts or 43% to US real GDP growth of 2.7% YoY in 1Q26.

AI-related capex rose by an annualised 32% QoQ in 1Q26 and was up 18.8% YoY, while non-AI capex declined by an annualised 4.0% QoQ in 1Q26 and was down 2.9% YoY.

This followed the same pattern observed last year.

AI capex was the main driver of US economic growth last year after personal consumption, based on national accounts data.

Thus, US real GDP rose by US$469bn or 2.0% YoY in the four quarters to 4Q25.

Meanwhile, real personal consumption and real AI-related fixed investment increased by US$344bn and US$261bn respectively over the same period, or 2.1% and 19.6% YoY.

As a result, real AI-related investment contributed 56% of the increase in real GDP in the four quarters to 4Q25, compared with 73% from real personal consumption.

Is the AI Model Business Really Just the Latest Commodity Business?

The base case remains that the AI capex arms race will culminate in massive over-investment in data centers and the like, as US Big Tech has felt compelled to participate for fear of being disrupted in what might be described as FOMO (i.e. fear of missing out).

In this respect, the motivation to spend has been as much a negative than a positive.

As a result, the hyperscalers have exited their moats and shed their asset-light business models.

Yet, these are the two features which made them such attractive equity investments over the past many years.

Meanwhile, it remains far from clear who, if anyone, is going to be the winner in the US in terms of the race to build large language models and monetise them in the personal market.

Indeed, there is a view that AI could turn out to be much more like the capex-intensive airline industry than the winner-takes-all network effect of the Internet economy from which US Big Tech so benefited.

Certainly, so far as this writer can tell, no killer app has yet been developed for the masses in terms of the practical application of AI.

Rather, this is an area which looks increasingly commoditised with a lack of product differentiation between different providers.

True, AI agents are coming and doubtless will have significant commercial implications.

But it is also the case that fortunes have already been invested.

Still, the upside of the seemingly inevitable over-investment bust when it happens, in terms of the amount being spent on compute and AI data centers, is that the costs of so-called “inference” should collapse and demand should surge.

This is, of course, what happened in the Dotcom bust in the early 2000s, when fiber-optic excess capacity caused a big decline in the cost of broadband, leading to the resulting explosion in e-commerce demand.

The difference this time remains that the AI chips have a much shorter shelf life (apparently 3-4 years) than fiber-optic cables (around 25 years).

Still, that practical reality has in part been disguised by America’s generous depreciation rules, which have become more generous thanks to OBBBA, in terms of spreading out the cost of purchasing chips and related equipment over several years.

In other words, US Big Tech is in no hurry to pay for the AI capex in terms of accounting for it as already discussed.

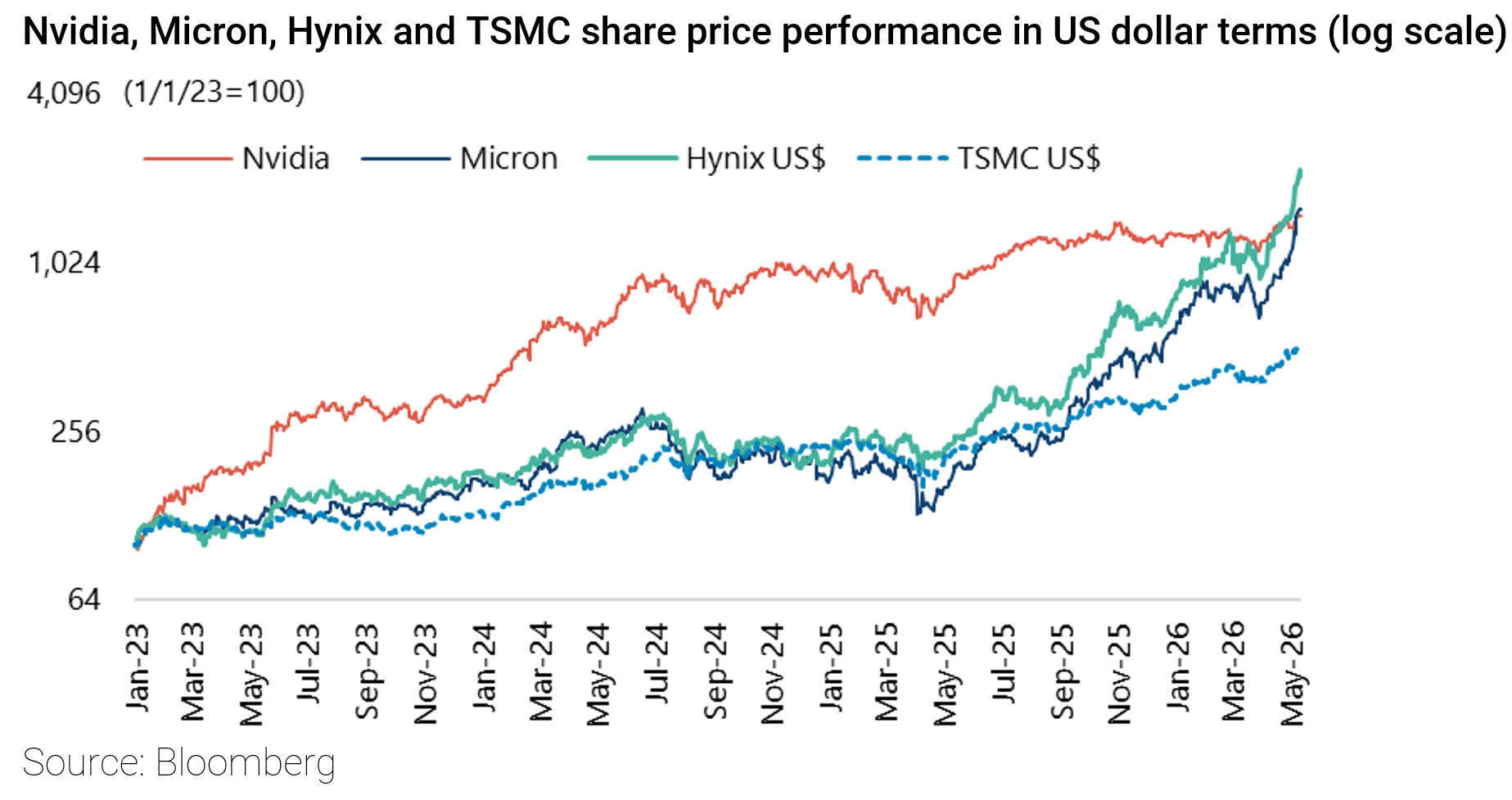

All this is why the easy money has been made in the “picks and shovels” trade since the AI theme entered markets at the start of 2023 benefitting the likes of Nvidia, Hynix, Micron and TSMC.

Their share prices are up 1,402%, 1,985%, 1,491% and 391% respectively in US dollar terms since the beginning of 2023.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.