China’s 14th Five-Year Plan

While world markets have been focused on the US presidential election, an important event also took place in Beijing in late October. That was the annual plenum of the Chinese Community Party where decisions taken will lay the groundwork for the drawing up of the 14th Five-Year Plan from 2021 to 2025, though targets were also prepared for 2035.

The meetings contained more actual inputs for local government officials than was conveyed in the formal communiqué. This is because Beijing has learned from the furore generated by the national security lobby in Washington over the “Made in 2025 Programme” that it makes no sense to go into too much detail in public.

Still, Beijing would seem to have three main goals. The first is to be the global market leader in 5G-derivative technologies. The second is to lead in green technologies globally, which should trigger massive opportunities commercially as the world pursues its decarbonisation targets.

Hence Xi Jinping’s recent pragmatic pledge, made to the United Nations General Assembly in September, for China to be carbon-neutral by 2060 and for CO2 emissions to peak by 2030. The third goal is to attract foreign talent to help achieve the desired technological upgrade.

In this respect, China seems to have decided to follow the policy pursued by Singapore founder Lee Kuan Yew, who consciously sought the employment of foreign talent, via tax breaks and related incentives, to help serve as a catalyst to upgrade the city state’s economy.

Attracting students from abroad, and particularly from elsewhere in Asia, to do post-graduate studies in the specialist areas related to 5G or green technologies, could certainly play a role in this regard. It is also worth noting that, according to the Global Times, the Chinese character for “innovation” appeared nearly 20 times in the communiqué, and the character for “technology” 13 times (see Global Times article: “China sets ‘pragmatic’ targets through 2035”, 29 October 2020).

China’s Renewed Focus on Domestic Demand Growth

All of the above is in the context of the renewed emphasis on domestic demand growth since the Chinese leadership is now preparing for the worst, in terms of a potential continuing deterioration in US-China relations as well as the potential for a further hit to the global economy because of, from a Beijing perspective, the continuing mismanagement of the pandemic in the West.

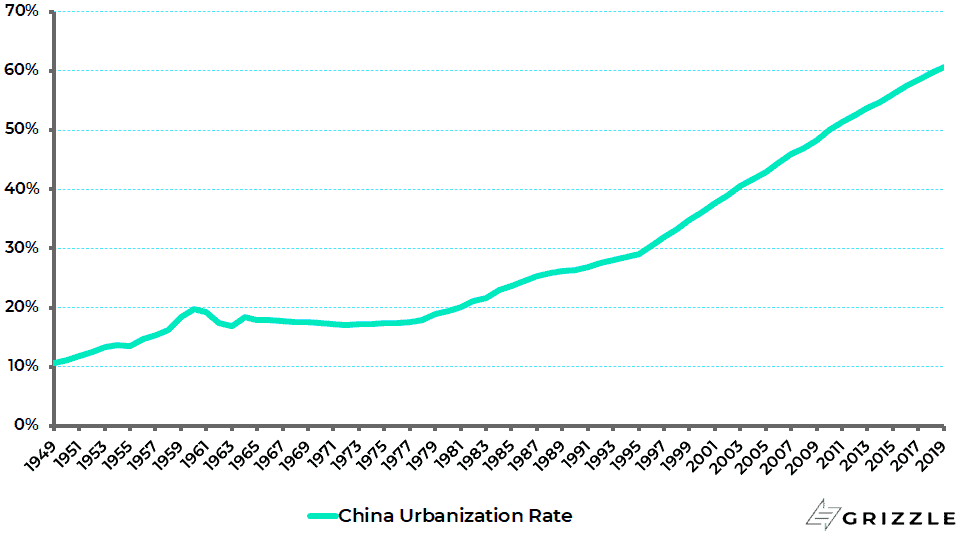

The key driver of growth is not just Xi’s previous focus on the elimination of poverty but also boosting development in the lower-tier cities. China’s current urbanisation rate is 61% (see following chart).

Until recently, the focus was on continuing migration from the smaller cities to the big cities. That has now changed to bringing the growth to the smaller cities themselves, a process in which it is hoped that the likes of 5G applications will serve as a catalyst. There are an estimated 500-600m people living in these low-tier cities who have the potential to become middle class over the targeted 15-year period to 2035.

Overweight China and Emerging Markets

Meanwhile all of the above is in the content of Xi’s new slogan of “dual circulation”, and the now national agenda to reduce dependence on US technologies as quickly as possible given the painful lessons learned as regards semiconductors during the Trump administration.

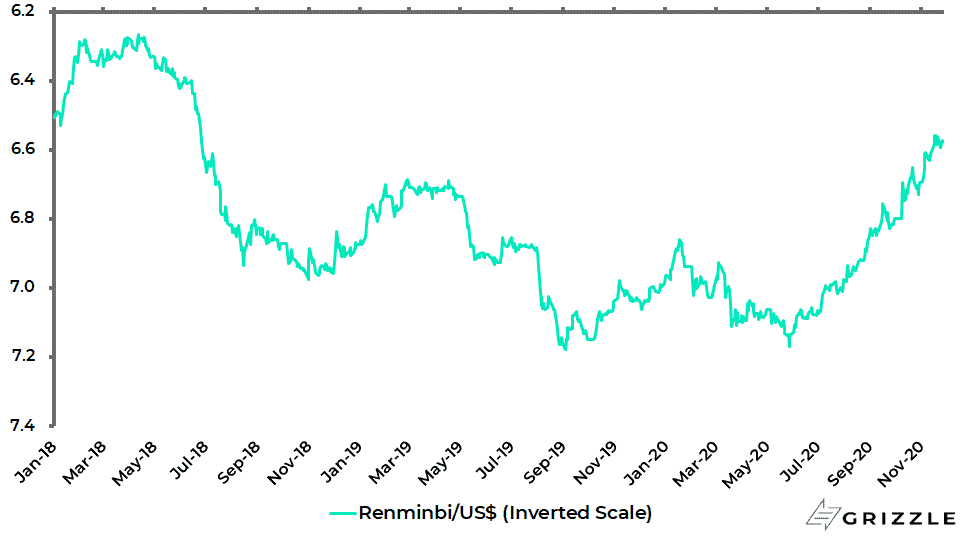

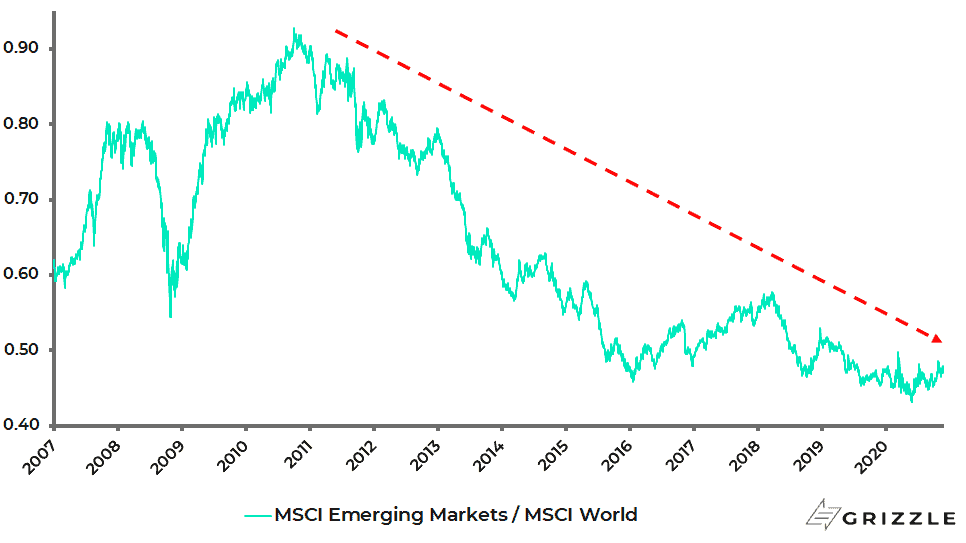

This writer has every confidence that China will achieve these goals; and also remains positive on the Chinese renminbi, which has appreciated by 6% against the US dollar year to date (see previous chart). This is another reason to overweight Chinese equities and indeed emerging market equities since China accounts for 41% of the MSCI Emerging Markets benchmark. The long-term potential for emerging markets to outperform is shown in the chart below (see following chart).

Ant Group – The Regulator is Boss

Meanwhile, interesting regulatory developments have occurred in Beijing in early November. Regulators from four government bodies, including the PBOC and the CBIRC, held a supervisory meeting with Ant Group’s controlling shareholder Jack Ma and two other senior executives in early November.

This coincided with the publication by the CBIRC and PBOC of new draft rules for online micro-lending businesses on the same day, which would force the fintech company Ant and other operators of online lending platforms in China to fund a greater share of the loans they offer together with banks.

The next day the Ant Group’s giant US$35bn dual IPO was postponed only two days before the company was meant to list because Ant had not complied with certain regulatory requirements.

The signal has, therefore, been sent that the regulator is the boss. As for the draft measures themselves, they seem sensibly prudential. The rules cap the size of loans at Rmb300,000 for individuals, or one third of average annual income earned in the past three years, while lending to corporate entities should be less than Rmb1m.

Online micro-lending platforms are also required to contribute at least 30% of loans funded jointly with banks, up from the current only 1-20%. National online micro-lending companies that conduct cross-provincial business will, going forward, be supervised by central regulators, including the PBOC and the CBIRC, instead of local financial bureaus.

As for Ant Group itself, it changed its name from Ant Financial ahead of the announcement of the IPO in August, with the current full name Ant Technology Group. This was to emphasis that it views itself as a technology company, not a financial company.

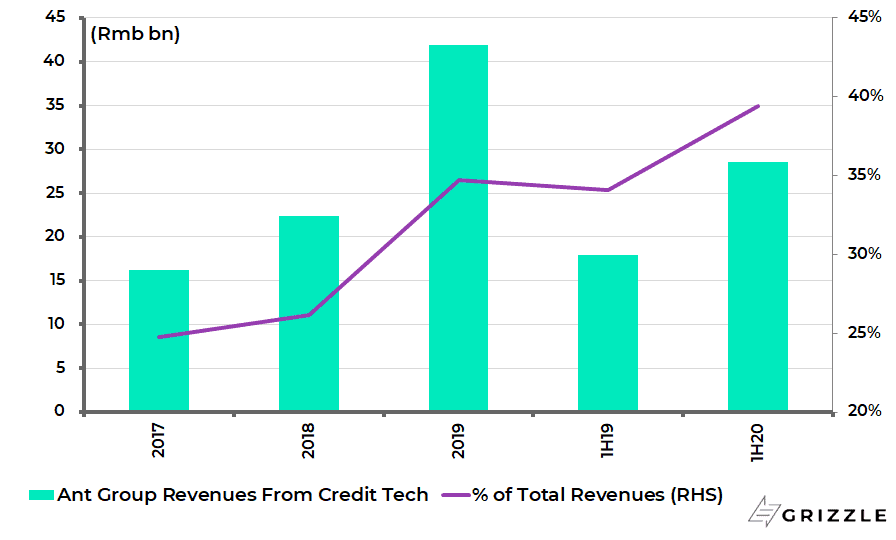

Still, the reality is that its business model is heavily geared to consumer lending. The micro-loan technology platform, named CreditTech, generated Rmb28.6bn in revenue for Ant Group in the first half of 2020, accounting for 39.4% of its total revenues (see following chart). The annualized interest rate of Ant’s consumer loans is about 15%, which compares with the 15.4% interest rate ceiling for consumer lenders imposed by a recent Supreme Court ruling.

Meanwhile, Ant’s prospectus shows that only a tiny 2% of Ant Group’s Rmb2.15tn of credit extended is funded with its own money, with the rest funded by banks or asset-backed securities. This will now change since the Chinese regulators, sensibly, want Ant to have some skin in the game. Remember it was the lack of “skin in the game” by the Wall Street peddlers of securitisation that triggered the US subprime mortgage crisis back in 2008.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.