Aside from the human death toll inflicted by Covid-19, the big story about Covid-19 has always been where it came from.

It was, frankly, a little pathetic how little the mainstream media in the Western world has focused on this issue over the past year and more.

This was even more the case when it became known that there was a well-known laboratory conducting experiments on coronaviruses, namely the Wuhan Institute of Virology.

It is also the case that the fact that China was so quick to shut down its economy in the first quarter of last year suggested that the central government was extremely concerned.

Otherwise Beijing would not have taken the extreme step of sacrificing growth.

For if the virus was man made, having leaked accidentally from the lab, then it could no longer be assumed that it would run its course naturally, thereby raising doubts about whether such otherwise sensible theories as herd immunity and Farr’s Law would prove to be applicable.

That the virus is here to stay looks increasingly likely to be the case, which is why a key issue is whether the new messenger RNA technology can deal with the new variants via booster vaccines.

This also for now seems to be the case.

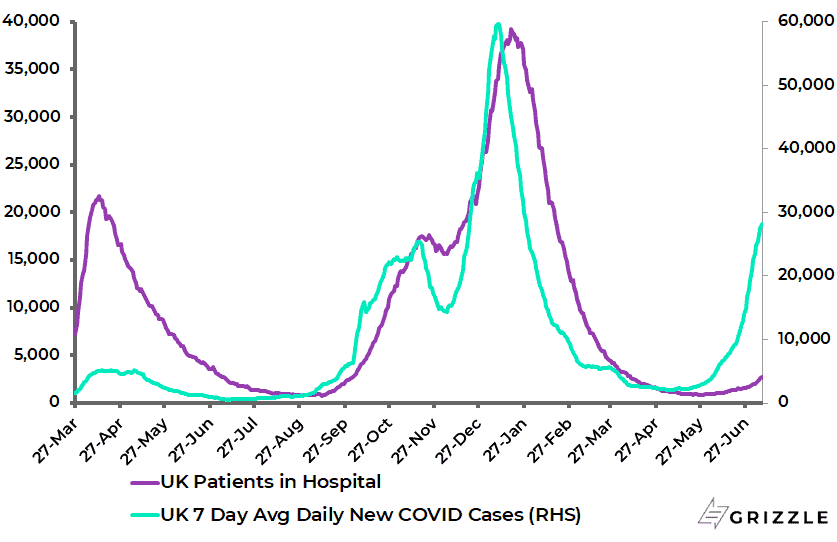

The empirical evidence also supports this assumption for now in the case of the ongoing vaccine rollouts in countries like the United Kingdom, where the Delta variant is soaring but hospitalization rates are not rising commensurately.

UK 7-day Average Daily new Covid Cases and Total Covid Patients in Hospital

Origins of the Virus Will Further Strain US China Relations

The first mainstream media coverage of the lab-leak theory this writer read was in Britain’s Mail on Sunday in April last year (“Did coronavirus leak from a research lab in Wuhan? Startling new theory is ‘no longer being discounted’ amid claims staff ‘got infected after being sprayed with blood’”, 5 April 2020).

But the story was not taken up by the mainstream media at large, primarily because it was associated with alleged right-wing conspiracy theories in the context of the then ongoing US presidential election campaign.

Certainly, blaming Covid on China became a major theme of the Trump campaign.

Facebook even went so far as to take down posts claiming the virus was man made as part of its campaign against right-wing conspiracy theories.

Still all that has now changed with Joe Biden’s statement on 26 May ordering the US intelligence agencies to do further analysis and report back to him on the lab-leak theory within 90 days.

The American president has openly conceded that at present there is no hard conclusion on this issue.

Still for anyone interested in looking further into the topic this writer recommends reading again the attached lengthy article written by a former New York Times science writer (see Bulletin of the Atomic Scientists article: “The origin of COVID: Did people or nature open Pandora’s box at Wuhan?” by Nicholas Wade, 5 May 2021).

Clearly, the renewed focus on the source of the virus has the potential, at least, to trigger a further serious deterioration in US-China relations, and indeed China’s relations with the West in general, in terms of the potential to trigger accusations of cover ups.

Comparisons are already being made to Chernobyl and Three Mile Island.

Whereas until the recent renewed focus on the origins of the pandemic, the narrative which has prevailed as regards the pandemic is that China has managed it much better than the West, which has indeed been the case.

Still, ultimately, it is going to be hard to prove this issue definitively unless Beijing cooperates.

And that from a domestic Chinese political standpoint implies an unacceptable interference with China’s domestic affairs and an unacceptable loss of face.

There is also the complicating factor that the US National Institute of Allergy and Infectious Diseases (NIAID) funded in part the research done at the Wuhan Institute, as detailed in the abovementioned article.

Still investors should prepare themselves for a lot of noise on the above in coming weeks and months.

China Wants to Become Rich Before It Gets Old

Pandemic related issues aside, this writer remains constructive on the renminbi in the context of the still assumed base case, namely that the world has entered a weak dollar era.

It certainly remains the case that Beijing favours a strong currency, fundamentally, since China is a domestic demand-driven economy and a stronger renminbi increases Chinese people’s purchasing power in US dollar terms.

In this respect, the goal remains for China to become rich before it gets old.

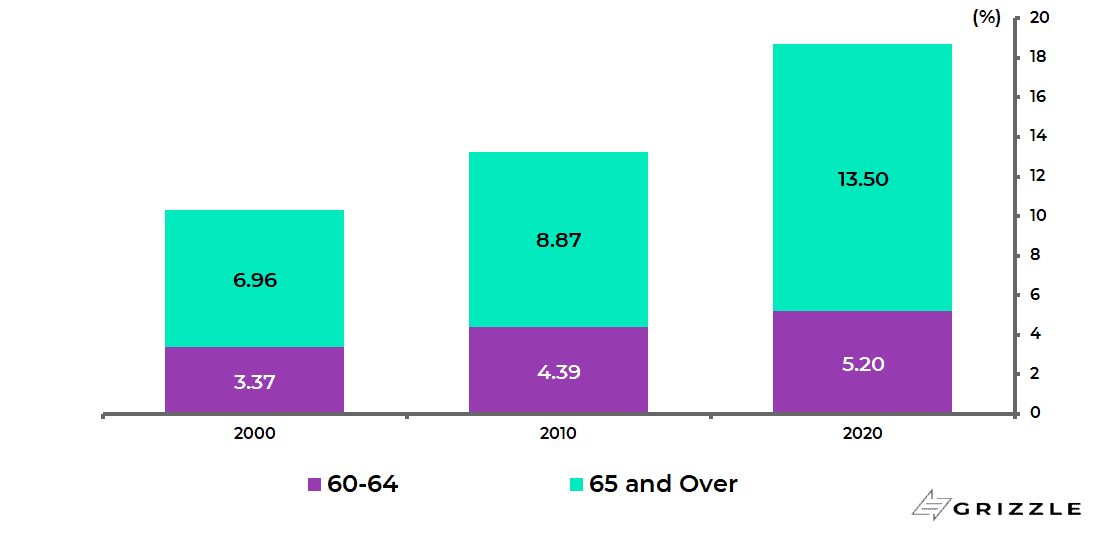

On this latter point, the latest census data has indicated that China is ageing more quickly than previously thought.

The mainland population aged 60 and above rose to 264m or 18.7% of the total population in 2020, up from 177.6m or 13.26% in 2010.

While those aged 65 and above increased to 190.6m or 13.5% of the total in 2020, up from 118.8m or 8.87% in 2010.

This compares with UN estimates of 12% of the population aged 65 and above and 17.4% aged 60 and above.

China National Population Census: Share of population aged 60 and above

The demographic issue also is the context to view the announcement on 31 May that China will now allow its citizens to have three children. It is increasingly evident that the One-Child policy, in place from 1979 to 2015, was a massive error.

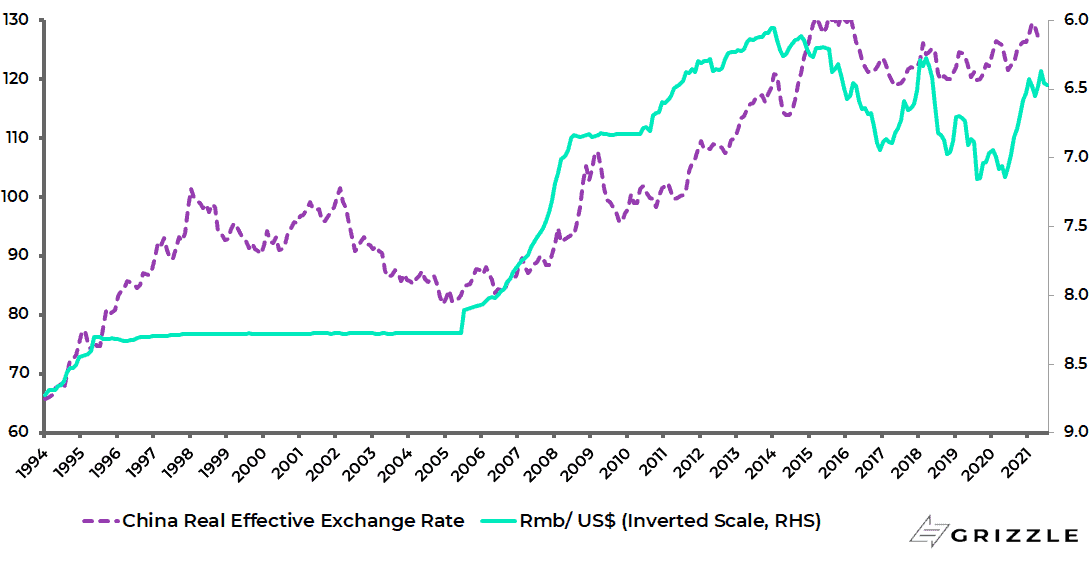

Beijing’s preference for a strong currency is why longstanding concerns in the US and Europe that China will want to devalue to boost its exports have long since been out of date; though such concerns have lingered despite the renminbi having appreciated by 28% against the US dollar since 2005 in nominal terms.

While its real effective exchange rate has appreciated by 55% over the same period.

China real effective exchange rate and renminbi/US$ (inverted scale)

But none of the above means that China wants uncontrolled appreciation.

Nor does it mean that China’s ambition to build a greater international role for the renminbi will lead it to liberalise fully its capital account.

For that would lead to an unacceptable loss of control for the Chinese Communist Party, which is also why Beijing has cracked down on crypto assets as discussed here last week (“Will China’s Crypto Crackdown Push Bitcoin Into the Arms of the West?” 5 July 2021).

This stance has been maintained for the past seven years since Chinese authorities barred financial institutions from handling Bitcoin transactions in December 2013, though the campaign has been stepped up of late.

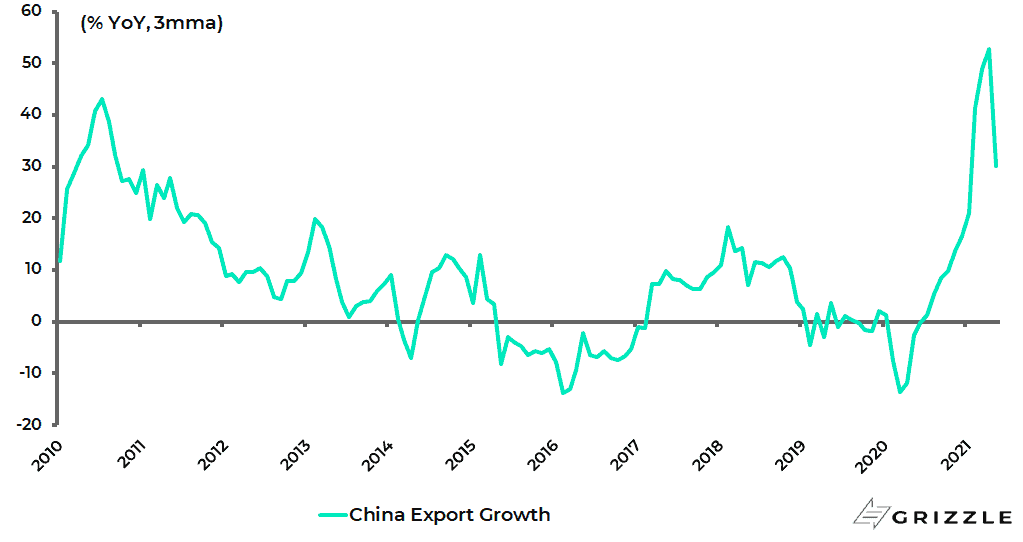

China Still an Export Juggernaut

Meanwhile, there is as yet no sign from Chinese export data that the renminbi is posing a competitiveness problem for Chinese exporters.

Exports rose by 28% YoY in May and were up 40% YoY in the first five months of this year.

China Export Growth

Still, export growth should slow as factories re-open globally in coming months.

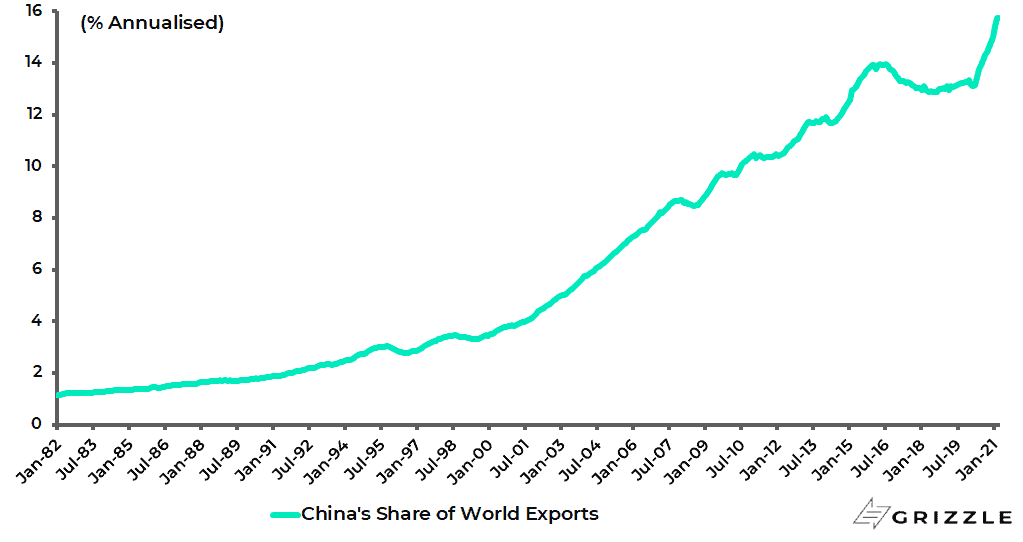

In this respect, one of the consequences of the pandemic has been to cause China to increase further its share of world exports.

China’s share of annualised world exports rose from 13.3% in February 2020 to a new record 15.7% in March 2021.

This is despite all the talk of production moving out of China because of tariffs imposed by the Trump administration.

China’s Share of Annualised World Exports

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.