This column has tended to focus primarily on monetary policy as it relates to the trend in financial markets.

But another longer term issue is the sheer scale of the government debt taken on in the G7 world last year in response to the pandemic.

This is worth spelling out in some detail.

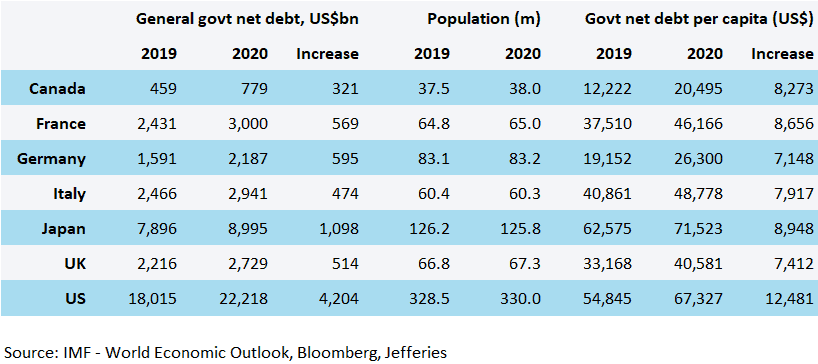

The leader both in terms of amount of new debt borrowed, and the increase in government debt per capita, was America.

The new government debt burden in 2020 amounted to US$4.2tn in America which was equivalent to a US$12,481 increase in debt per capita, according to the IMF’s net government debt estimates.

Other G7 countries saw large increases, though not quite as dramatic on a per capita basis.

In the case of long fiscally profligate Japan, the increase was US$1.1tn or US$8,948 per capita.

It should also be noted that these estimates do not take into account the latest stimulus measures announced in Japan and America in December, never mind the bigger US$1.9tn now being proposed by the Biden administration.

Increase in G7 Government Debt and Government Debt per Capita

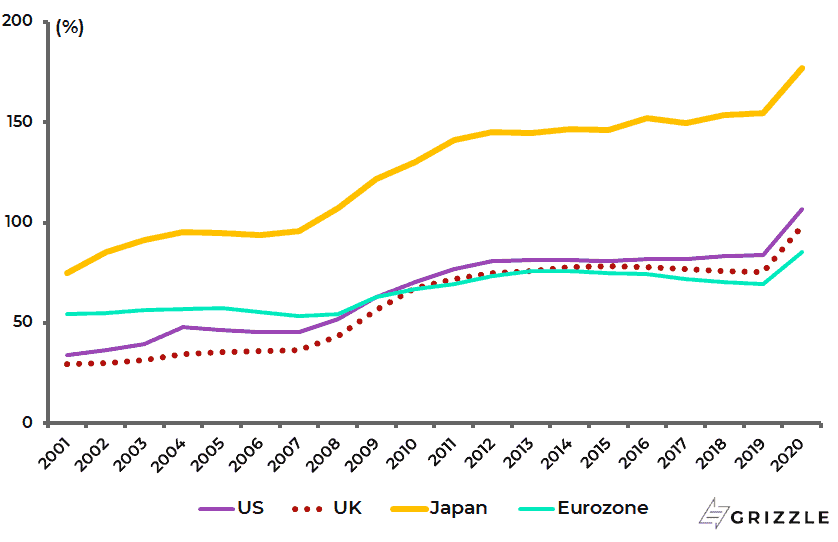

As a result, net government debt as a percentage of GDP is now running at 107%, 177% and 85% respectively in America, Japan and the Eurozone (see following chart). These are levels where the sheer burden of debt is a constraint on long-term growth rather than a positive or, in other words, the law of diminishing returns sets in.

US, UK, Japan and Eurozone general government net debt to GDP

Debt Case Study – Japan

In this respect, it has long been understood that Japan has reached a level of indebtedness in its government sector which has made higher interest rates not an option; though the passive nature of Japanese investors has allowed seemingly unimaginable excesses to have been reached in terms of government debt to GDP ratios.

To be fair, the Japanese numbers look more manageable on a net rather than a gross basis. Japan’s gross general government debt to GDP rose to 238% of GDP at the end of 2019 and is projected by the IMF to have reached 266% by the end of last year, while general government net debt to GDP was 155% of GDP in 2019 and is projected to have reached 177% in 2020.

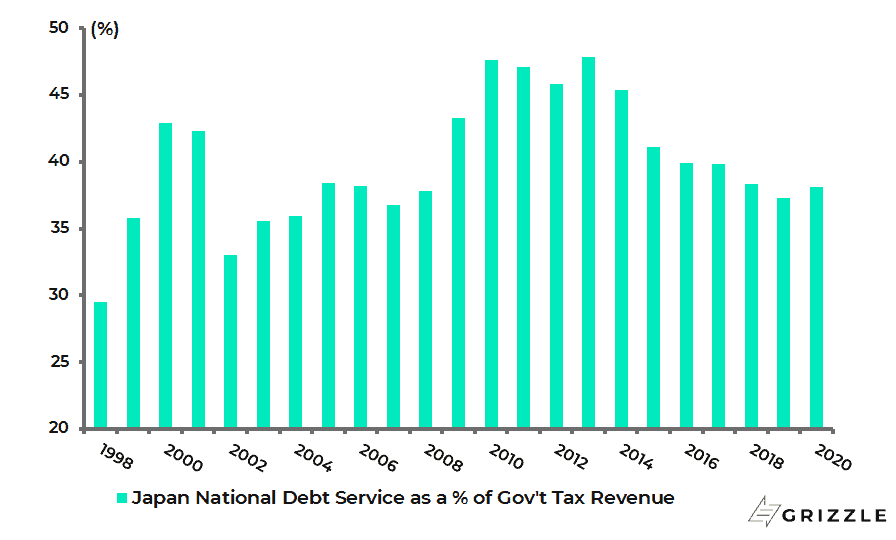

Meanwhile, the debt servicing ratio of the Japanese government has actually fallen in recent years courtesy of ultra-low bond yields.

Japan’s national debt service, as a percentage of government tax revenues, has declined from 47.8% in FY12 ended 31 March 2013 to 38.1% in FY19, though it is budgeted to rise to 43.6% this fiscal year ending 31 March due to a projected decline in tax revenue.

Japan National Debt Services as % of Government Tax Revenue

Still, the Japanese have long been flirting with levels of monetization which, based on historical experience, raises the risk of a flip-out of deflation into inflation caused by a trend change in velocity. In this respect, the great hyperinflationary episodes in the past century have all been triggered by central banks’ direct financing of governments.

On this point, it is a useful exercise to look at where Japan stands in relation to certain thresholds which were identified by economic historian Peter Bernholz in his book chronicling inflationary episodes in the twentieth century (“Monetary Regimes and Inflation: History, Economic and Political Relationships” by Peter Bernholz, Edward Elgar Publishing, 2003).

Bernholz argued in his book that hyperinflations have all been caused by the financing of huge public sector deficit through money creation.

These perceived thresholds concentrate on two key variables.

- The first is central bank monetization as a percentage of government expenditure.

- The second is the budget deficit as a percentage of government expenditure.

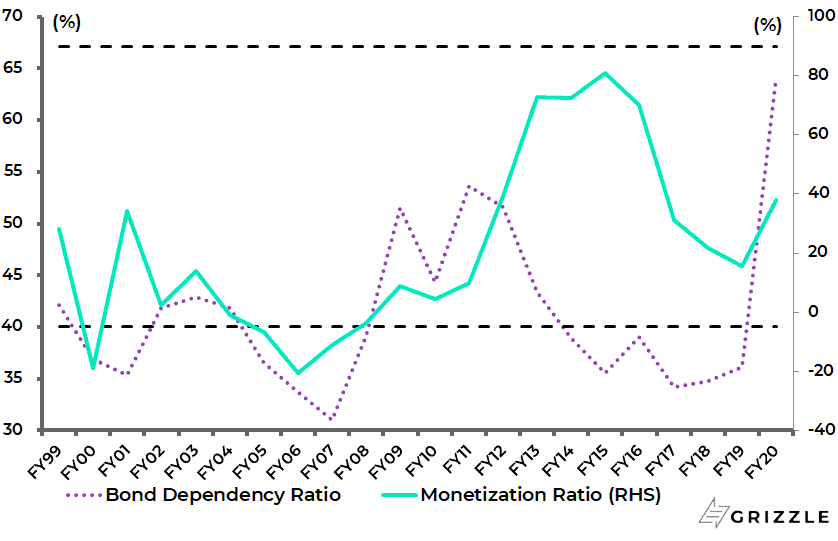

In the case of Japan the budget deficit ratio, measured as net government bond issuance as a percentage of government expenditure (or the so-called bond dependency ratio) rose to 51.5% in FY09 ended 31 March 2010 and 53.7% in FY11, well above the identified Bernholz threshold of 40%.

But at that time the monetization ratio, defined as the Bank of Japan’s net purchases of Japanese government securities as a percentage of government expenditure, was relatively low at only 8.7% in FY09 and 9.9% in FY11.

Japan Bond Dependency Ratio and Monetisation Ratio (with projection for FY20)

Since then the monetisation ratio rose sharply in the early years of Kuroda’s tenure as Bank of Japan Governor to a peak of 81% in FY15, close to the 90% level.

But at that time the budget deficit ratio was declining, falling to a low of 34% in FY17.

Still, that dynamic has now changed.

With the renewed Japanese fiscal stimulus in response to the pandemic, the budget deficit ratio is projected to rise to 64% this fiscal year if the third supplementary budget announced in December is taken into account (which projects a record Y112.6tn of bond issuance).

Meanwhile, monetisation has also picked up again as the Bank of Japan, which already owned 48% of outstanding JGBs at the end of 3Q20, has had to increase its JGB buying again in response to the Covid triggered stimulus.

The monetisation ratio is projected to rise to 38% this fiscal year based on annualised BoJ net purchases of government securities.

The BoJ has bought a net Y50tn of government securities in the period between 1 April and 30 December, or an annualised Y66tn.

America is Now Following Japan’s Lead on Debt Issuance

As for America, both trends are now going in the wrong direction, in terms of the budget deficit ratio and the monetisation ratio, though certainly not yet at Japanese levels.

And they are very likely to deteriorate further in a Democrat controlled Washington.

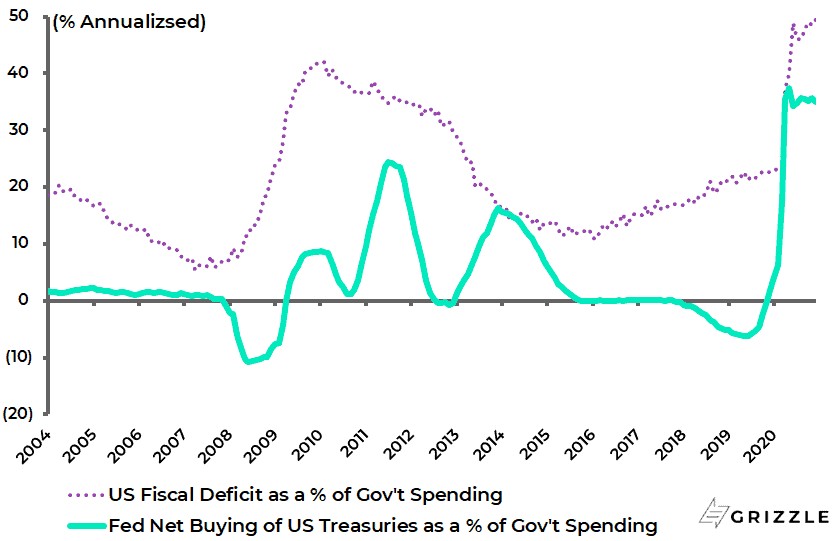

The budget deficit ratio, defined as the annualised fiscal deficit as a percentage of government expenditure, soared as a result of the pandemic-triggered surge in the fiscal deficit.

The budget deficit ratio rose from 22.6% in March 2020 to 49.5% in December.

As for the monetisation ratio, defined as the Fed’s annualised net purchases of Treasury securities as a percentage of government expenditure, it fell from a high of 24.4% in mid-2011 to a negative 6.2% in mid-2019 and was 35% in December.

US Fiscal Deficit and Fed net Buying of Treasuries as % of Government Expenditure

Still, if America’s situation is not yet as extreme as Japan’s, it has to be wondered whether American bond investors will remain as passive as Japanese investors have been all these years.

It also should be noted that the Japanese own 92.7% of their own bond market, whereas 30% of outstanding US Treasury securities are owned by foreigners.

This is, clearly, yet another incentive for the Federal Reserve to implement yield curve control in the US before the bond market takes fright.

Modern Monetary Theory is Taking Hold in America

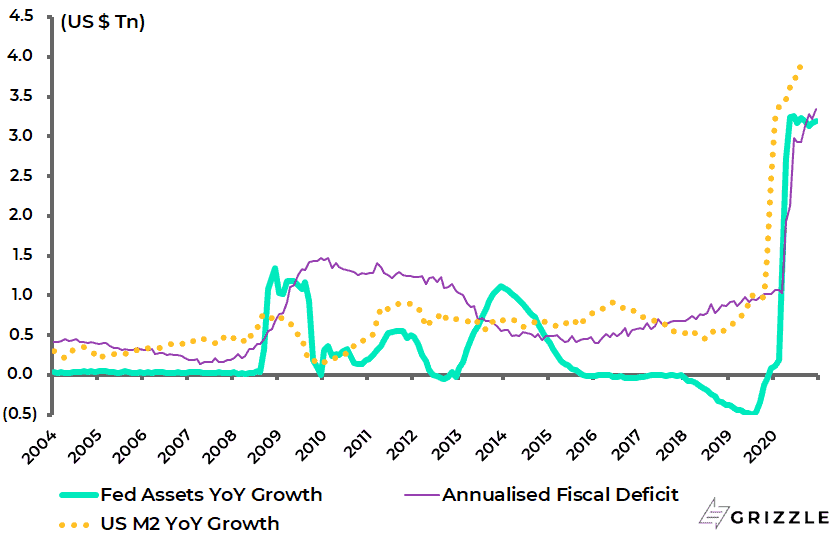

Meanwhile, the growing convergence of monetary policy with fiscal policy in America continues to be highlighted dramatically by the chart below showing the trend in Fed balance sheet expansion, the annualised US fiscal deficit and US M2 growth.

US Annualised Fiscal Deficit and YoY Increase in Fed assets and US M2

That growing convergence is also symbolized by the appointment of former Fed chair Janet Yellen as Treasury Secretary in the Biden administration.

The above is not to say that America has entered into a formal regime of direct monetisation, as advocated by the believers in Modern Monetary Theory (MMT).

So far the policy response has remained on a “needs must” basis in response to the perceived emergency circumstances created by the pandemic.

It is also the case that so far the Fed has been primarily lending to the fiscal entity and not directly funding government expenditure.

In this respect, the monetisation is implicit rather than explicit.

Still it should be understood that advocates of MMT, who are represented on the progressive wing of the Democratic Party in America, will want to make such a policy explicit.

This is where the political pressures will undoubtedly grow on the Fed if it tries to turn orthodox in terms of policy.

All of the above highlights why the system in the G7 world cannot withstand higher interest rates, without considerable economic pain, and why there will be massive political pressure on G7 central banks not to tighten in the coming cyclical upturn.

That is also why the base case should be yield curve control in America and financial repression even in the face of evidence of cyclical recovery, with all the negative implications for the value of the US dollar which such an outcome entails.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.