Datadog (Nasdaq: DDOG) the cloud monitoring and analytics platform reported solid Q1 2020 that were ahead of analyst estimates. The stock is up 3% in after hours trading.

Revenue came in at $131.2 million, which beat analyst estimates of $117.8 million (+11% vs consensus). Revenue growth was +87% year-over-year.

EPS came in at -$0.02/share, topping analyst estimates of -$0.02/share.

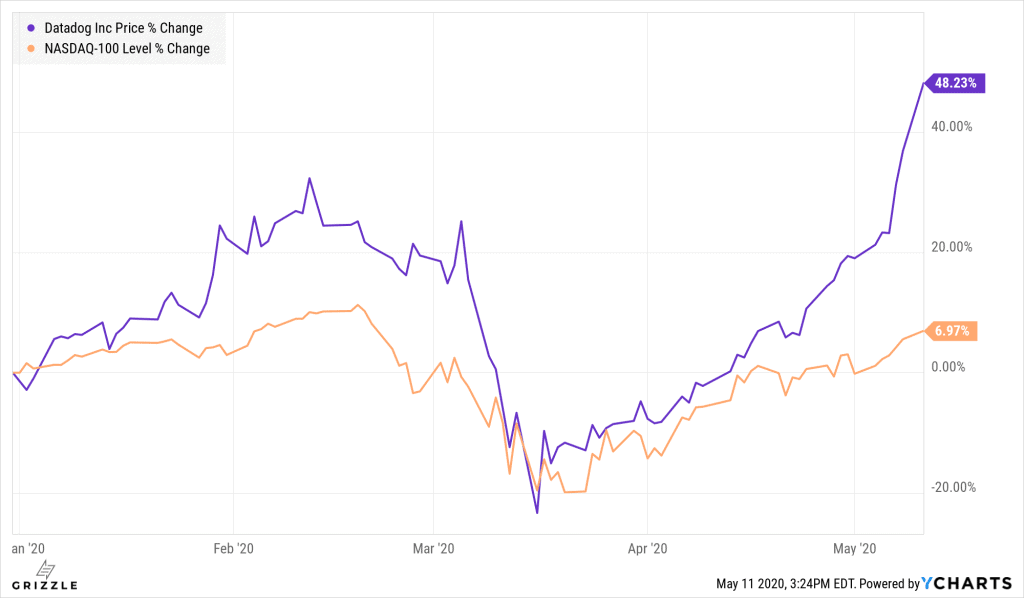

This marks the 3rd consecutive quarterly top line revenue beat for Datadog. The stock has had a tremendous run year-to-date, up +48% versus the Nasdaq 100 up +7%.

Year-to-Date Performance

The software as a service (SaaS) group of technology stocks have been very resilient in the face of COVID-19. In the March 25th edition of Grizzle’s Coronavirsus SOS series we highlighted this group of stocks as ones to own on the rebound.

For Datadog the tailwind would be more companies transitioning their on-premise infrastructure to the cloud, resulting in market share gains versus legacy non-cloud infrastructure monitoring peers.

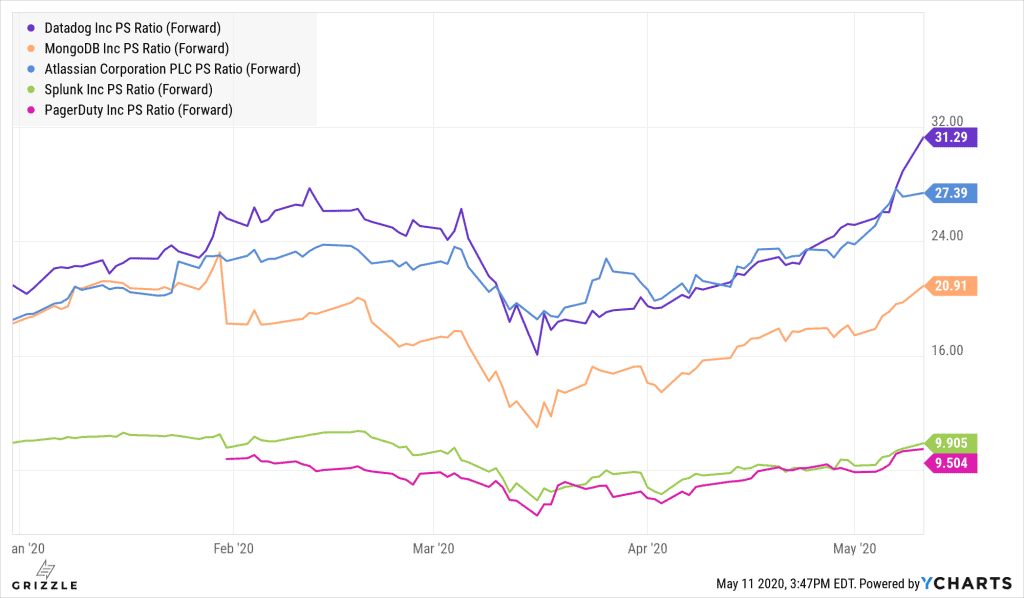

Valuation remains the main hurdle for growth investors with a value bias, Datadog trades at 31x P/S, the highest among its platform infrastructure peers.

Forward Price-t0-Sales

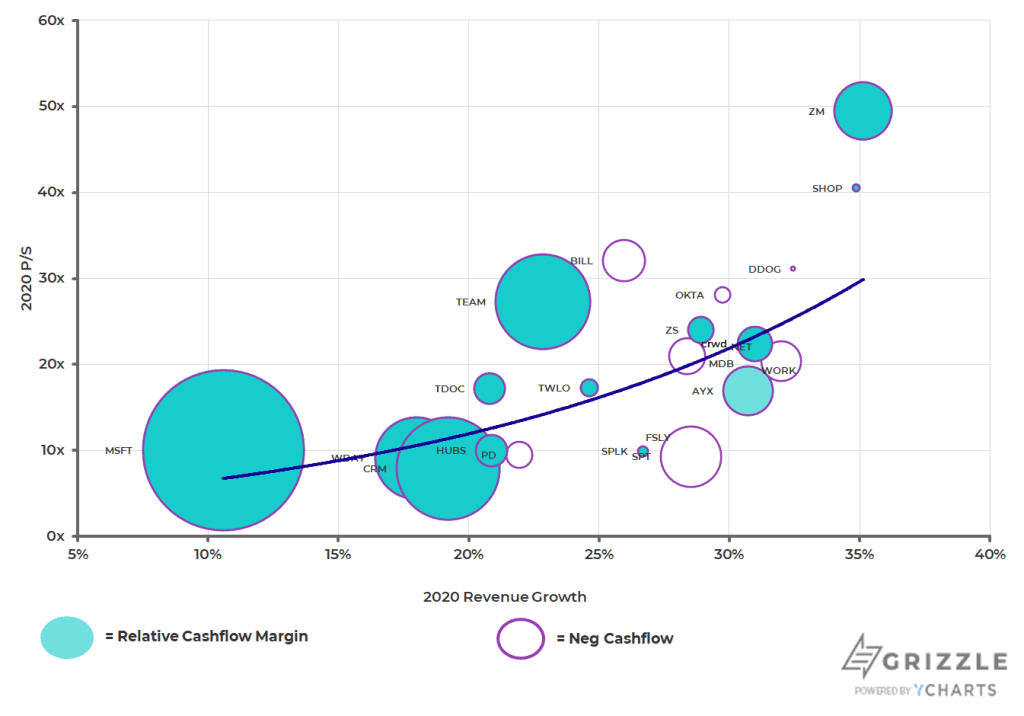

Looking at Datadog’s valuation dynamically, we see that they are expensive when comparing 2020 Price-to-Sales ratio relative to 2020 Revenue Growth, additionally their relative cashflow margin is lower than many of its high growth peers.

2020 P/S vs. 2020 Revenue Growth

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.