Etsy (NASDAQ: ETSY) the global online marketplace for creative goods delivered strong Q1 2020 results.

Revenue came in at $228.0 million, which beat analyst estimates of $219.3 million (+4% vs consensus).

EBITDA came in at $55.1 million, beating analyst estimates of $51.7 million (+6% vs consensus).

EPS came in at $0.11 missing analyst estimates of $0.25 (-56% vs consensus).

The coronavirus pandemic has created a strong tailwind for delivered goods, Etsy has been uniquely positioned to capitalized on this captive market. The purchase of homemade masks are one example of local communities showing support for local craftspeople.

The company provided guidance for Q2 2020: Revenue of $310-340M +70-90% y/y (street estimates are at $208M) & Adjusted EBITDA of $75-90M +23-27% y/y (street estimates are at $29M).

Grizzle has been bullish Etsy since 2018, we viewed it then as we do now as a baby Amazon for goods produced by real people for real people – it’s a website that was built for a world post-globalization.

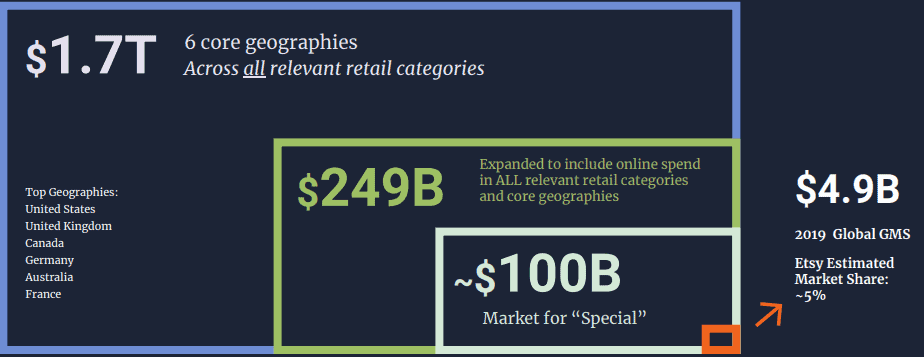

There is a large total addressable market for Etsy to grow market share, the creative and special marketplace globally is worth $100B.

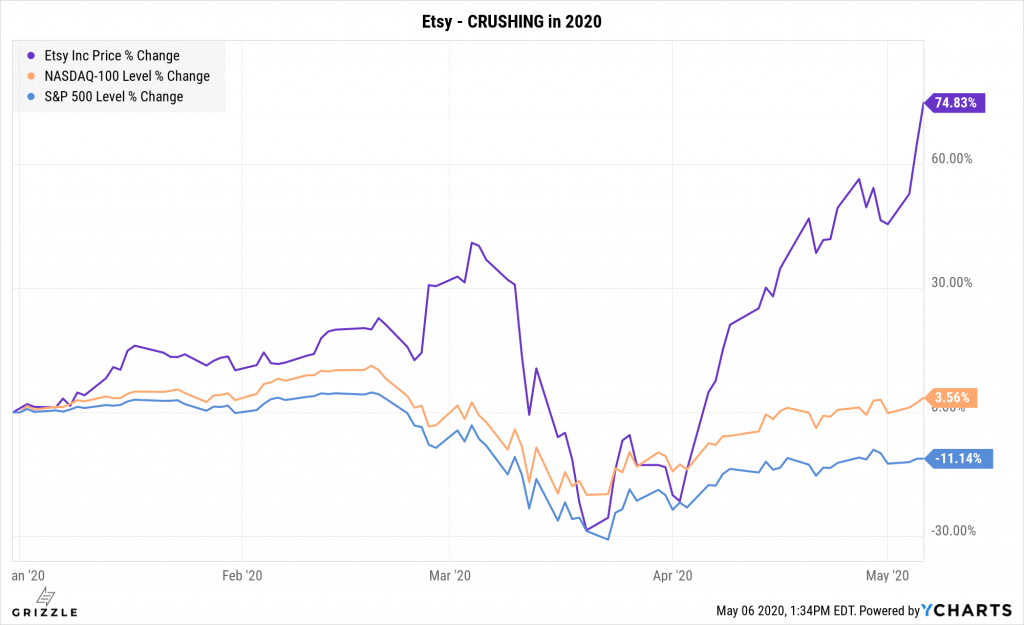

Etsy has significantly outperformed the Nasdaq and S&P 500 in 2020.

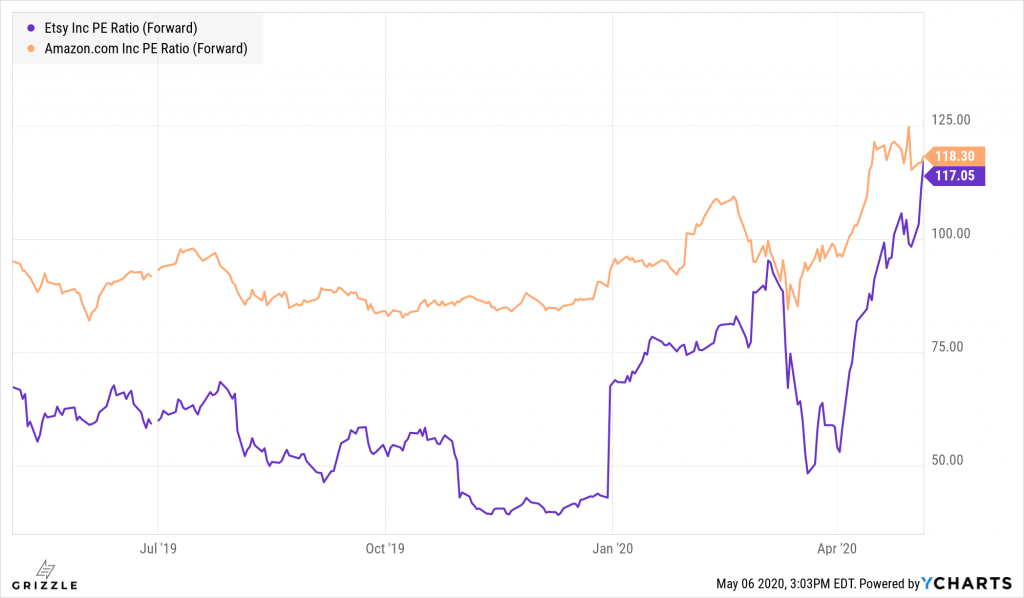

In early April we identified the significant valuation disconnect between Amazon and Etsy, we pounded the table – identifying it as a Grizzle conviction call. Now that valuation gap has closed, both Amazon and Etsy trade at compare forward Price/Earnings ratios.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.