Earlier this month, Grizzle identified Etsy Inc. (ETSY) as one of the best platform tech stocks for the long haul. That view has not changed despite a slightly disappointing first-quarter earnings call on Wednesday.

Q1 2019 Summary

- Earnings: $0.24 per share (adjusted)

- Revenue: $169.3 million

- Gross Merchandise Sales: $1 billion

Strong Revenue Growth Still Misses the Mark

Unlike Etsy’s blowout fourth-quarter earnings report, the company undershot expectations in the March quarter — at least, as far as revenues are concerned. The online platform for handmade goods generated $169.3 million in sales between January and March, gaining 40% over year-ago levels. That was still shy of expectations, which called for $170 million.

Despite the revenue miss, gross merchandise sales jumped 19% to $1 billion. This allowed the company to raise its outlook for the category to a range of $4.6 billion to $4.8 billion for the current fiscal year. Its overall revenue guidance was bumped up to $785 million to $797 million.

On the earnings side, Etsy generated an adjusted $0.24 per share, which was 10 cents higher than forecast.

Stock Plunges

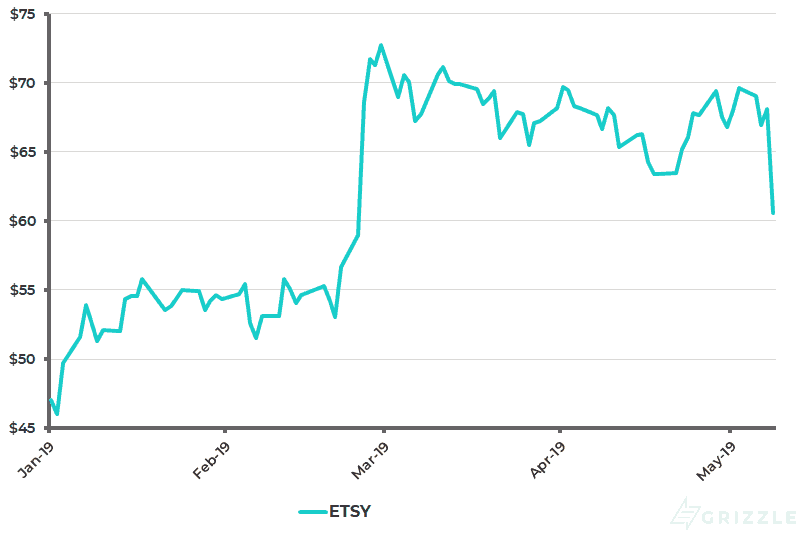

For Etsy’s investors, any sign of slowing growth is perceived to be a threat for a company that has far exceeded its projections in recent years. This rapid growth is reflected in the ETSY share price, which appreciated some 450% in the last two years to set multiple record highs.

But as revenues missed the mark, the stock plunged double-digits on Thursday to its lowest level since late February. At its lowest point during the day, ETSY stock was down 12.5%.

Prior to the selloff on Thursday, Etsy’s share price had appreciated more than 43% year-to-date

When we wrote about Etsy last week, the company had a total market capitalization of $8.1 billion. On Thursday, the market cap had fallen to around $7.4 billion.

Etsy Still a Keeper

The disappointing revenue figure and subsequent collapse in ETSY shouldn’t deter long-term investors from snatching up the stock at a bargain price.

For starters, Etsy has maintained a streak of double-digit revenue growth for more than four years. The fact that it is considered to be a “mini Amazon” with no direct competition leaves plenty of runway for significant growth. If Amazon has a high P/E multiple because of its business model, then the same logic can and will apply to Etsy.

Etsy’s numbers are extremely impressive for a company that burst onto the scene virtually out of nowhere. As of January, the company had more than two million sellers and over 35 million buyers.

Conclusion

Given its size, business model and growth rate, it would be foolish to bet against Etsy at this stage in the game. The company has yet to hit full stride, as evidenced by the monstrous revenue growth figures seen in recent years.

Disclaimer: Author holds no investment position in Etsy at the time of writing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.