The extended dog’s dinner over the re-appointment of Jerome Powell as Federal Reserve chairman on 22 November hardly amounts to a ringing endorsement.

That it took so long was because the Biden administration was seeking to determine whether there were the votes in the Senate for the Democratic Party’s candidate Lael Brainard to be nominated.

In this regard, the moderate West Virginia Democrat Senator Joe Manchin appears to have played a key role, and it is quite possible that a behind the scenes deal has been done with moderate Democrat Senators such as himself where a more relaxed view on the so-called “Build Back Better” bill is taken as a quid pro quo for the Powell appointment.

Meanwhile, the decision to replace Fed Vice Chairman Richard Clarida with Brainard when he steps down at the end of January means that she will remain highly influential in the formation of monetary policy, just as Clarida has been.

The reality is that Powell is a lawyer by training and so much less technically qualified for the job than academic economists like Brainard or, for that matter, Clarida.

In this respect, his track record shows he always defers to the experts.

It is also the case that the differences between Brainard and Powell should not be exaggerated, a point well made in a to-the-point editorial published in the Wall Street Journal last month (“Tweedledum and Tweedledee at the Fed”, 17 November 2021).

The through-the-looking-glass nature of Fed policy remains rather extraordinary and future economic historians will no doubt be astonished at the amount of attention paid by financial markets and the media to the comments emanating from individual central bankers in the current era.

Still for now the pantomime continues and Clarida definitely got the markets’ attention when he commented on 19 November that it may be appropriate to accelerate the pace of tapering.

Thus, he said at a virtual event hosted by the San Francisco Fed:

This message was confirmed 11 days later when the reappointed Powell himself formally dropped the word ‘transitory’ when referring to inflation in testimony before Congress on 30 November. Ironically, this comment came just at the time when the cyclical trade had been hit by the renewed surge in Covid cases in America and Europe.

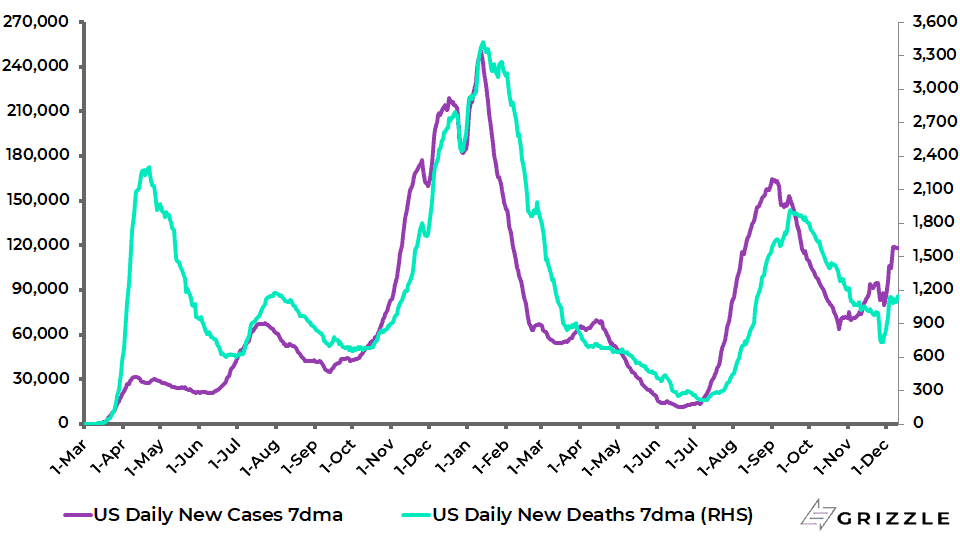

US 7-day average daily new Covid cases and deaths

The 7-day average daily new Covid case count in America has risen from 64,151 in late October to 118,575, while, more worryingly, the 7-day average daily new case count in Europe ex-UK has surged from the recent low of 30,366 in early October to 203,698.

Europe ex-UK 7-day average daily Covid cases and deaths

With the depth of winter now here in the northern hemisphere, this renewed Covid outbreak is clearly the biggest risk to the cyclical trade, most particularly with the appearance of the new Omicron variant.

But for now, the base case is that Omicron, while more infectious than previous Covid variants, is also less lethal most particularly for those vaccinated.

This conclusion is based on the initial evidence from South Africa where the Omicron variant was first identified. The 7-day average daily new Covid case count in South Africa has surged from 258 in early November to 15,580, while the 7-day average daily death count has only increased from 11 in mid-November to 22.

It is also the case that the number of Covid patients in ICU in the country has risen from 230 on 26 November to “only” 406, compared with 526 at the beginning of November.

South Africa 7-day average daily new Covid cases and deaths

Demand is Driving Inflation not the Supply Chain

Meanwhile, this writer’s preference remains with the cyclical trade because of the continuing likely resilience of the American economy as a result of the strength of household balance sheets despite the negative impact on real incomes of higher prices.

On this point, it is worth highlighting that retail sales were 23% above the pre-pandemic level as of October.

US retail sales

This is in large part a consequence of the stimulus to demand provided by transfer payments.

In this respect, it remains hard to exaggerate the extent to which American households have been net financial beneficiaries of the pandemic.

The above is why supply-chain bottlenecks are not the key drivers of the inflationary pressures which have surprised the Fed this year.

Remember the Fed at the start of 2021 forecast only 1.8% PCE inflation in 2021.

Rather the inflationary pressures are primarily demand-driven, in significant part by transfer payments financed indirectly by the Fed in a policy.

The Freightos global container freight index has declined by 15% from the peak reached in mid-September but is still up 200% year-to-date.

But such will be the narrative driving markets at that time.

Freightos Global Container Freight Index

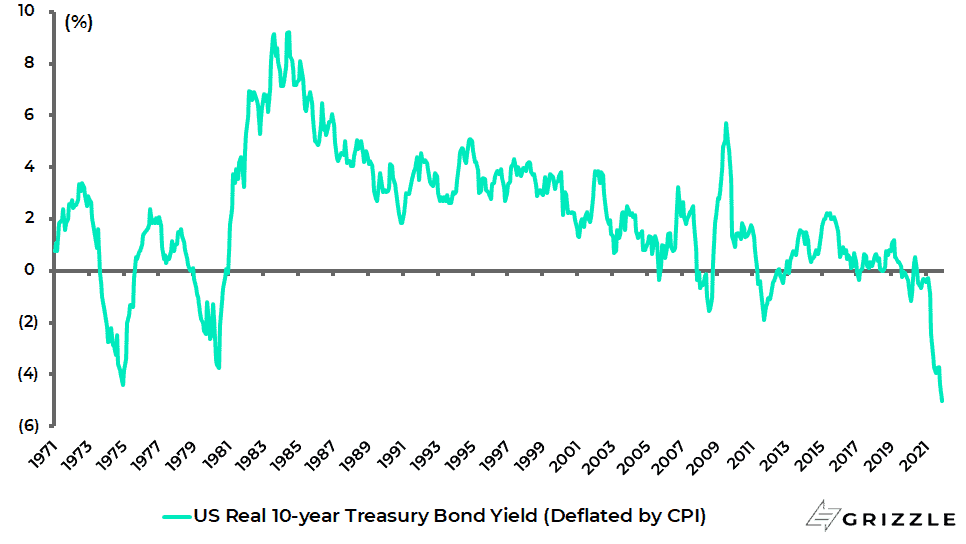

For now it remains the case that inflation has not been this high relative to Treasury bond yields since at least the 1960s.

The real 10-year Treasury bond yield, deflated by CPI, has fallen to a negative 5% at present, the lowest levels since at least 1962.

US real 10-year Treasury bond yield deflated by CPI

Expensive Workers will Stimulate a new Investment Cycle from Companies

Meanwhile, another positive for the American economy is that a tightening labour market, rising wages and

strong demand should lead to more incentives to increase productive capacity via a renewed capex cycle.

This is another reason to expect a pickup in private investment in America aside from the government incentivised decarbonisation energy transition agenda.

It certainly looks increasingly to be the case that the share buyback model has peaked in America following a period where private sector capex growth in America has collapsed.

Thus, US real private non-residential investment growth has fallen from 12.9% YoY in 1Q12 to a negative 0.2% YoY in 1Q20 prior to the pandemic, while S&P500 quarterly share buybacks rose from US$84bn in 1Q12 to a record US$223bn in 4Q18 and were US$199bn in 1Q20.

US real capex growth and S&P500 quarterly share buybacks

On a related point, it is also worth highlighting that US new corporate credit, as measured by the YoY increase in non-financial corporate sector debt, has been running below annualized S&P500 share buybacks during most of the past decade.

US corporate debt growth and S&P500 annualised buybacks

Source: Federal Reserve, S&P Down Jones Indices

The above-anticipated change in trend is not necessarily bad for the stock market but it is clearly another reason to own more cyclical stocks in the portfolio.

Meanwhile, growth stocks will be under downward pressure relative to cyclical stocks if the Fed really gets serious about raising interest rates as opposed to just slowing its asset purchases which is what tapering means.

On this point, money markets are now anticipating 75bp of Fed tightening in 2022 compared with none at the start of this year.

But just how hawkish is the reappointed Powell really going to be.

MSCI World Growth Index relative to Value Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.