It is now more than 14 weeks since the US-Israel attack on Iran, and there remains a remarkable lack of collateral damage in the markets, particularly the US stock market, given the continuing closure of the Strait of Hormuz during this period.

The explanation of course remains the ongoing celebration of the AI capex trade, and the related positive earnings revisions discussed here recently (see Why The AI Picks-and-Shovels Boom May Be Peaking, 13 May 2026), with the issue now whether the pending mega IPOs signal the peak in AI euphoria. There has to be a good chance that that will prove to be the case.

It is now clear that the rules governing IPOs are going to be changed to accommodate the interests of the promoters.

Most importantly, in the case of SpaceX, the company is going to be “fast-tracked” into the indices at a higher weighting than the percentage of the company due to be floated.

For example, Nasdaq’s new rules, effective 1 May, include eliminating minimum float requirements for new listings and allowing so-called “fast index inclusion”.

The rules will allow large-cap new listings like SpaceX to join the Nasdaq-100 index after only 15 trading days compared with the previous minimum seasoning period of three months.

The minimum 10% free-float requirement is also removed while, for the purpose of calculating the index weight, a mega-cap with a small free-float will be valued at three times its initial free-float (see Financial Times article: “New Nasdaq rules offer SpaceX free liquidity”, 2 May 2026).

Such “fast tracking” of new listings into indices has never happened before in America, so far as this writer is aware.

The significance of the move is clearly that it will force passive funds to buy the shares uptil the relevant weighting in the index.

Meanwhile, according to the updated S-1 filing last Wednesday, SpaceX plans to sell 555.6m shares at a fixed price of US$135 per share, raising US$75bn in the IPO which would value the company at US$1.77tn, meaning only a 4.2% free float.

But it will be treated as having a 12.7% float for the Nasdaq-100 index weighting calculation.

These valuations are in the context of a company which had an annual revenue of US$18.7bn last year and an estimated US$27bn this year, according to Bloomberg. SpaceX is expected to start trading on the Nasdaq on 12 June.

It is also worth noting that MSCI’s existing methodology already includes a rule for the fast-tracking of large IPOs.

This states that large IPOs are eligible for early inclusion after 10 trading days if they meet certain size thresholds and may qualify even with a low free float.

This is relevant as the inclusion of such mega IPOs in America will increase the US weighting in the MSCI AC World Index.

For now the US weighting at 63.4% is still below the all-time high of 67.2% reached on 24 December 2024.

This writer had thought that the biggest risk to the base case that the US reached an all-time peak share of world stock market capitalisation at the end of 2024 was that the hyperscalers successfully monetise their AI capex.

This is clearly not this writer’s base case. But these new listings create another such risk, at least theoretically.

The other key change in the listing rules appears to be that insiders will be able to sell their shares quicker than normal.

The standard rule is that insiders have to wait 180 days after an IPO.

But in the case of SpaceX, according to the S-1 filing, insiders can sell up to 20% of their eligible locked-up shares after reporting earnings for the second quarter ending 30 June and, if the stock is trading at least 30% above the IPO price, an additional 10% can be sold.

Revisiting China’s Stock Market

Meanwhile, amidst the near all-consuming focus on AI and the pending IPOs, it is worth looking again at the China stock market which remains out of most global investors’ focus.

In the mainland recently it remains clear to this writer that the “slow bull market” (慢牛市) remains the mantra of the central government as regards the stock market.

The goal remains clear: for the stock market to replace the deflating property market as the main source of wealth generation.

If this is the plan, there remains a lack of evidence that the Chinese middle class has yet bought into the long-term equity story, even though the growth of institutional investors has been dramatic in the last many years in a mainland A share market that used to be almost completely dominated by retail investors.

The main driver of the growth in institutional equity investment has been the life insurance companies, which now have in some cases more than 20% of their assets in equities at government prompting.

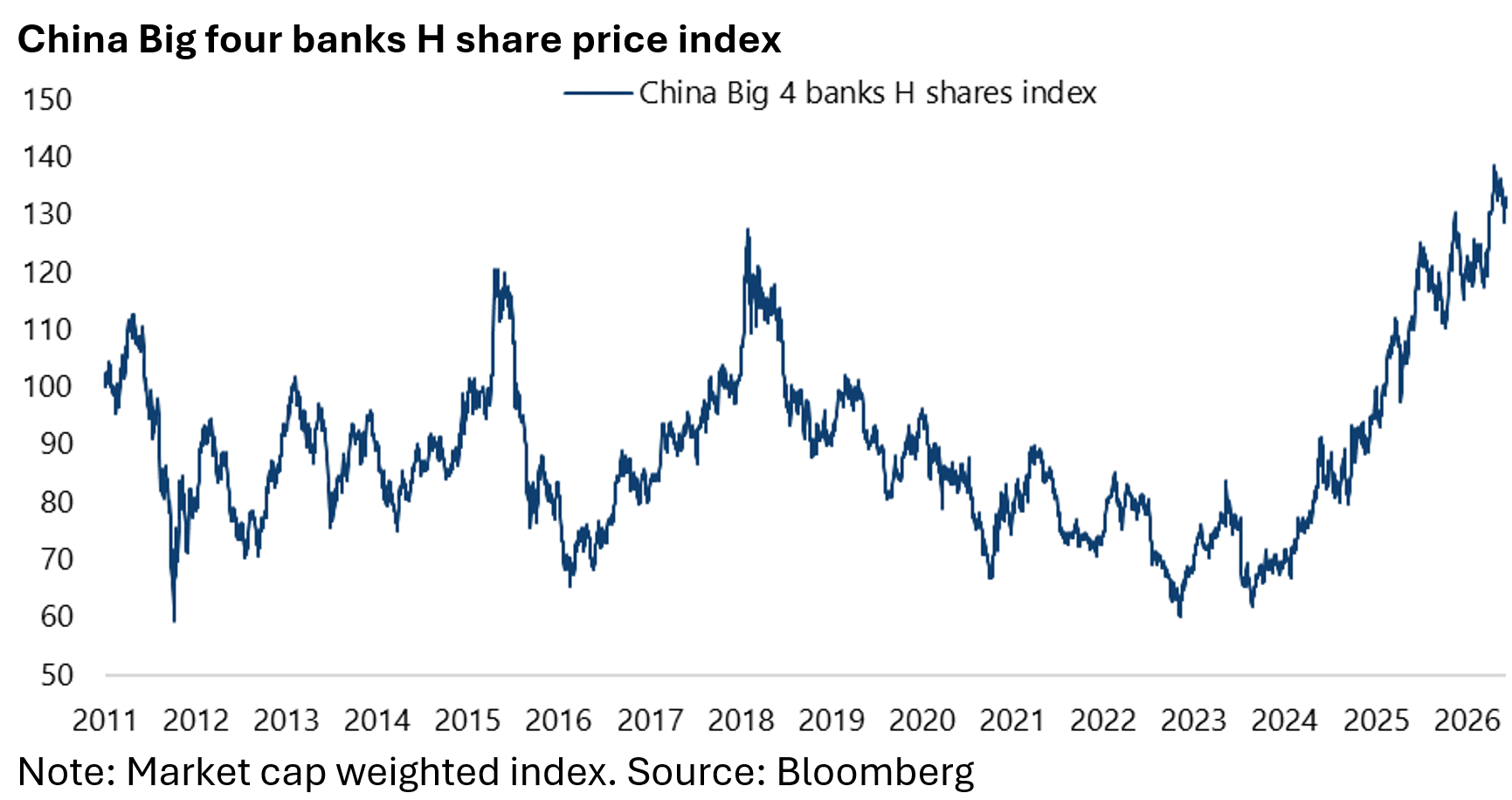

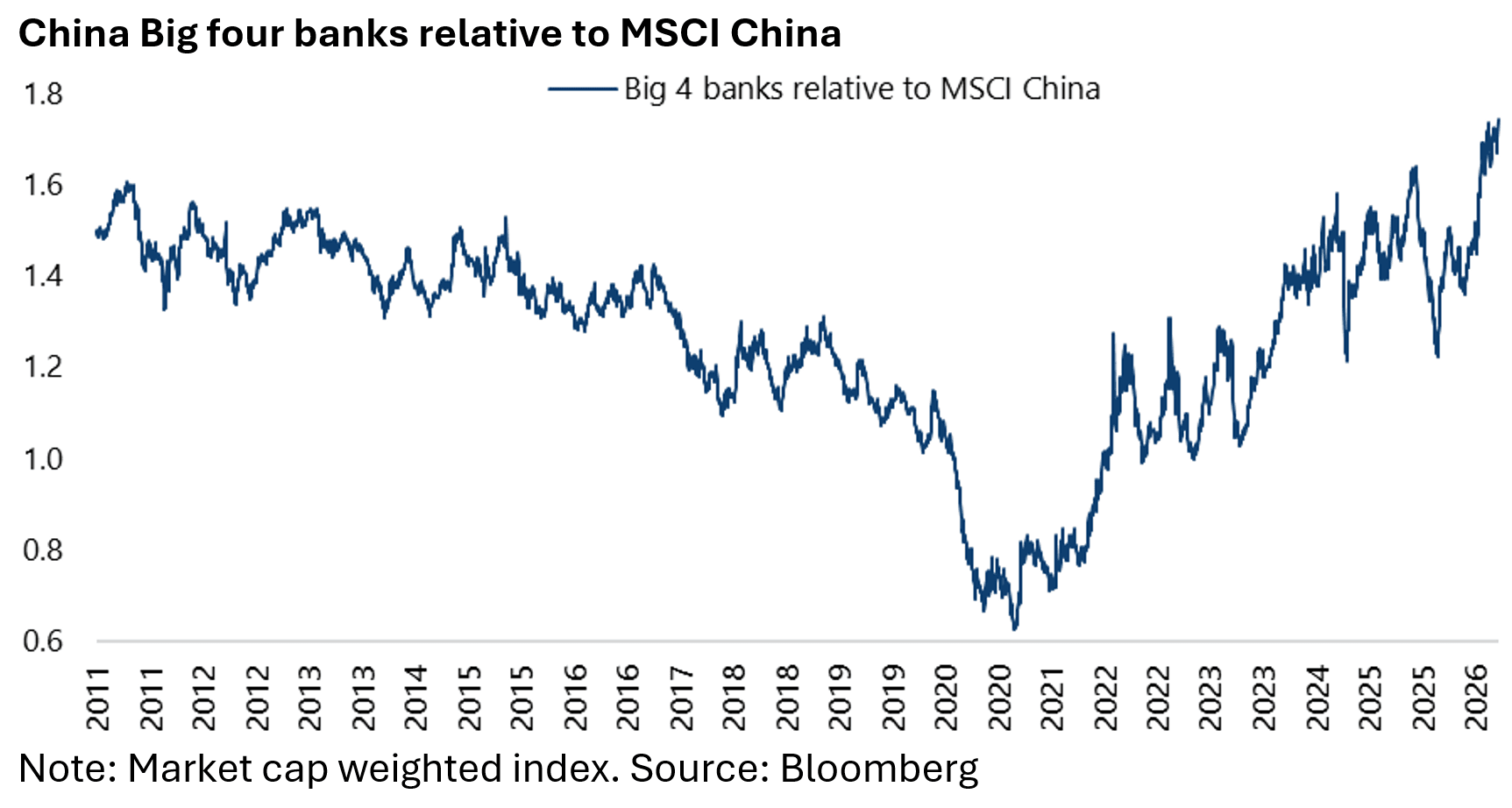

This remains one of the main reasons for the continuing outperformance of the major bank stocks.

They have continued to pay out attractive dividends even in the context of continuing deflation and a deflating residential property market, both of which would normally be very negative for bank stocks.

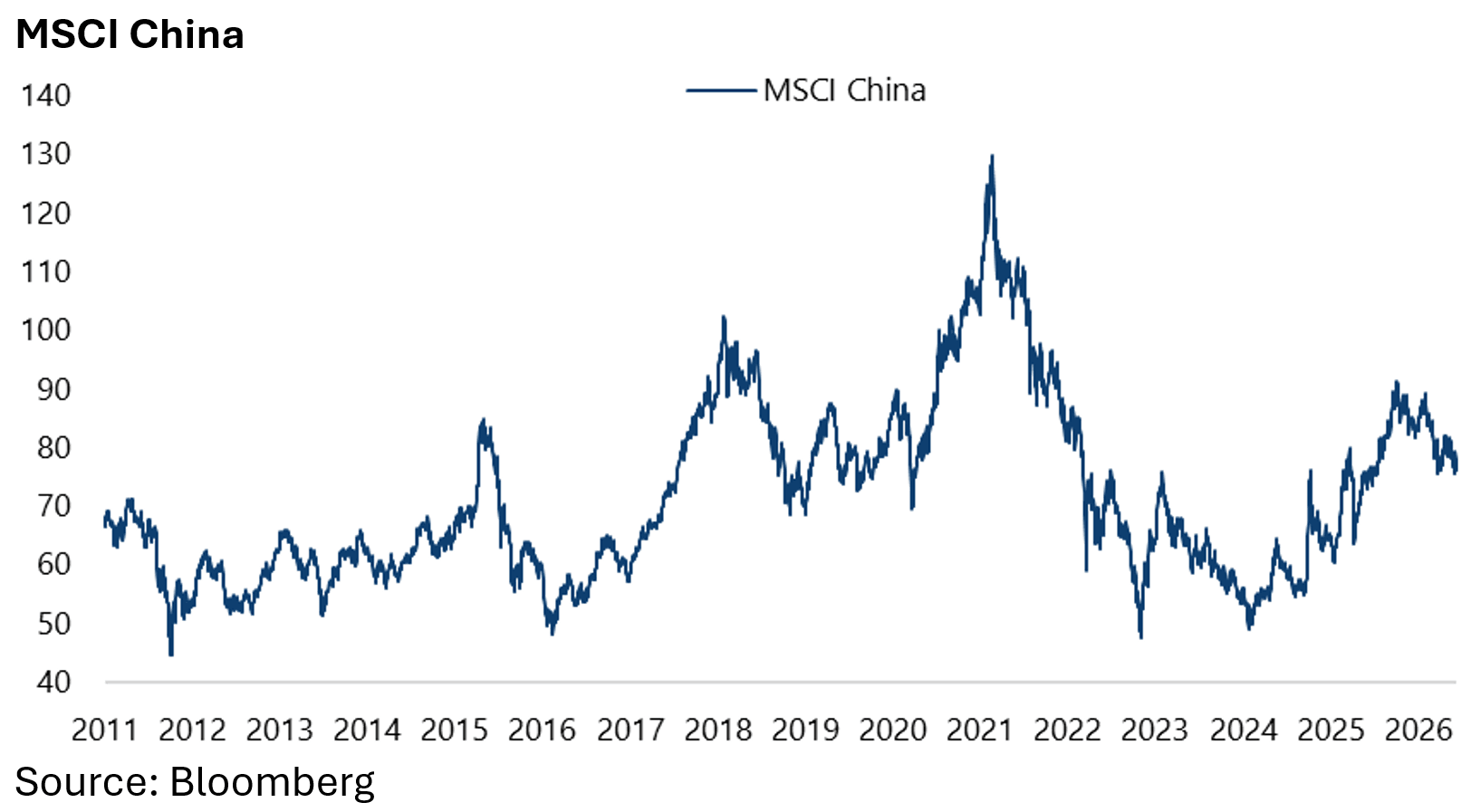

The Big four banks’ H share prices have risen by 66% since the beginning of 2021, compared with a 30% decline in the MSCI China over the same period.

The same banks have an average dividend yield of 4.9%. Similarly, the CSI 300 Banks Index has outperformed the CSI 300 by 35% on a total-return basis since the beginning of 2021.

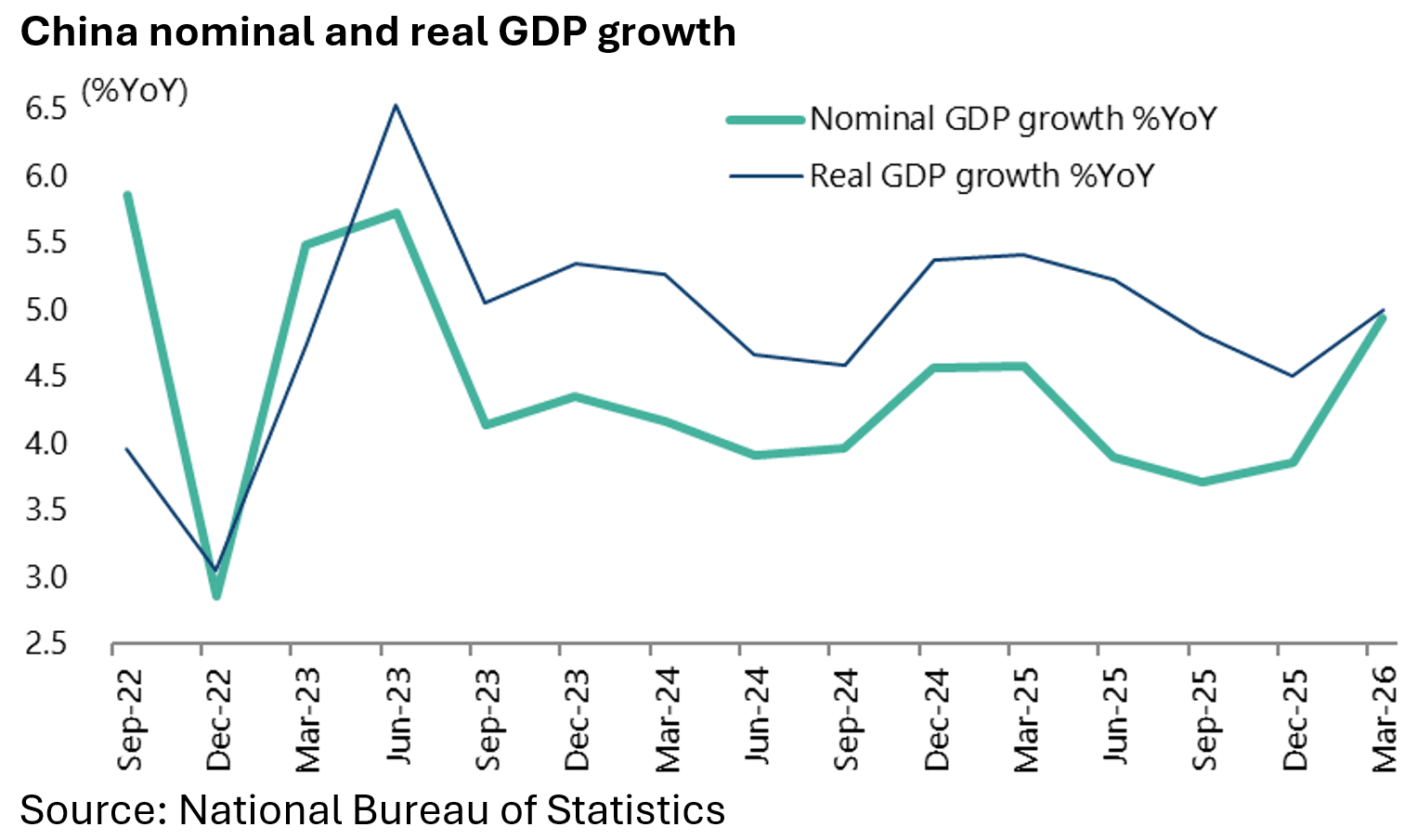

The stock market as a whole has continued to perform satisfactorily since bottoming in September 2024 in a macro environment where nominal GDP growth has been lower than real GDP growth for the past 12 quarters and a micro environment where price competition between leading players has remained brutal in high-profile sectors such as electric vehicles and e-commerce, though in both cases there are some reasons to believe that the competitive feeding frenzy may be on the point of peaking.

Source: National Bureau of Statistics

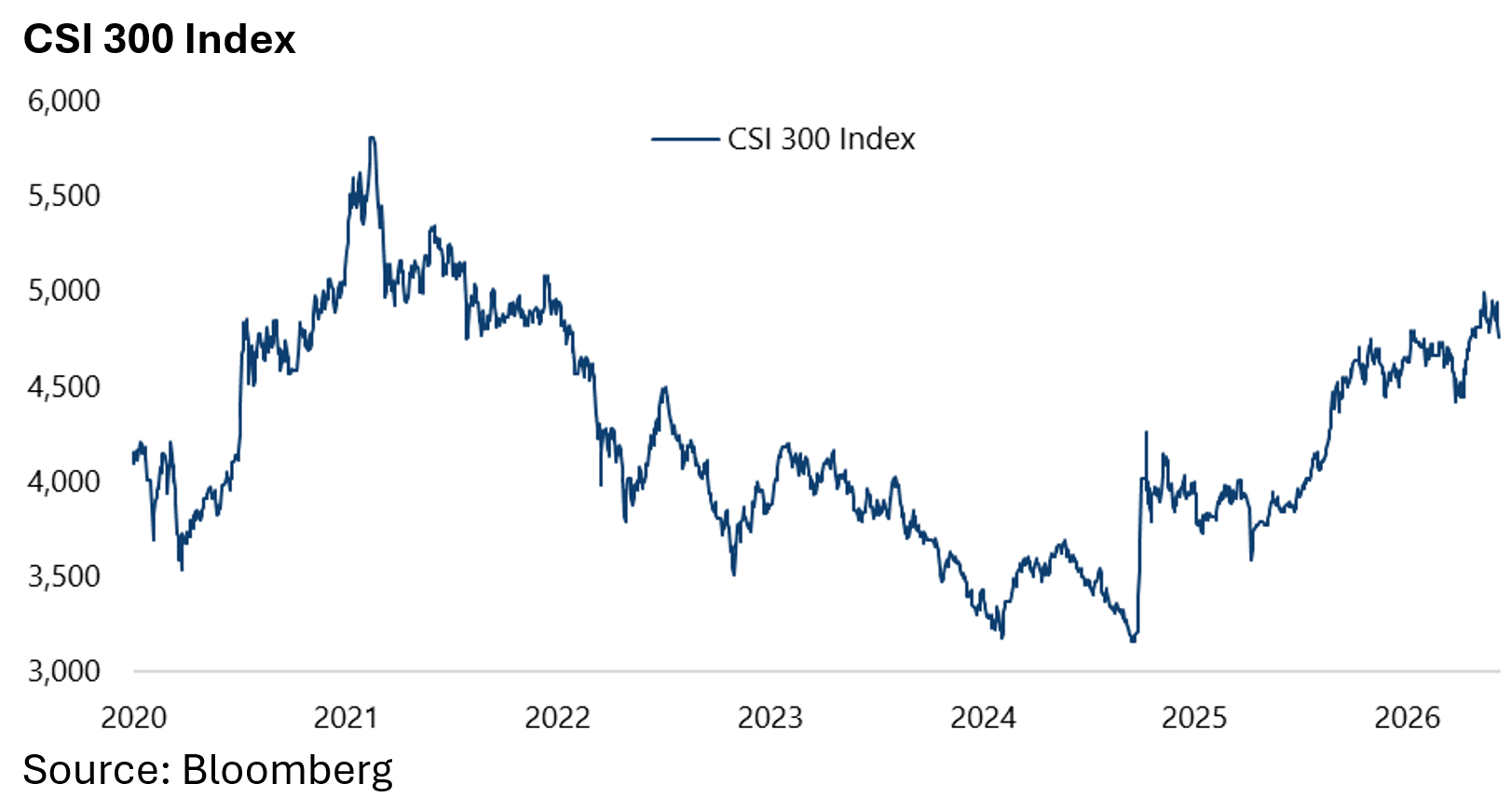

The CSI 300 Index has risen by 51% since bottoming in September 2024, while MSCI China is up 55% from its low in January 2024 .

Still, this remains a stock market where pricing power is at a premium as regards individual companies, which is why investors are most on the lookout for quasi monopolies in areas prioritised by the government, which of late has meant primarily companies in the tech hardware and industrial spaces.

Meanwhile, from an overall stock market standpoint, the government, and in particular the responsible regulator, the China Securities Regulatory Commission (CSRC), remain supremely focused on preventing another boom-bust cycle, which has been the fate of all China bull markets in the reform era.

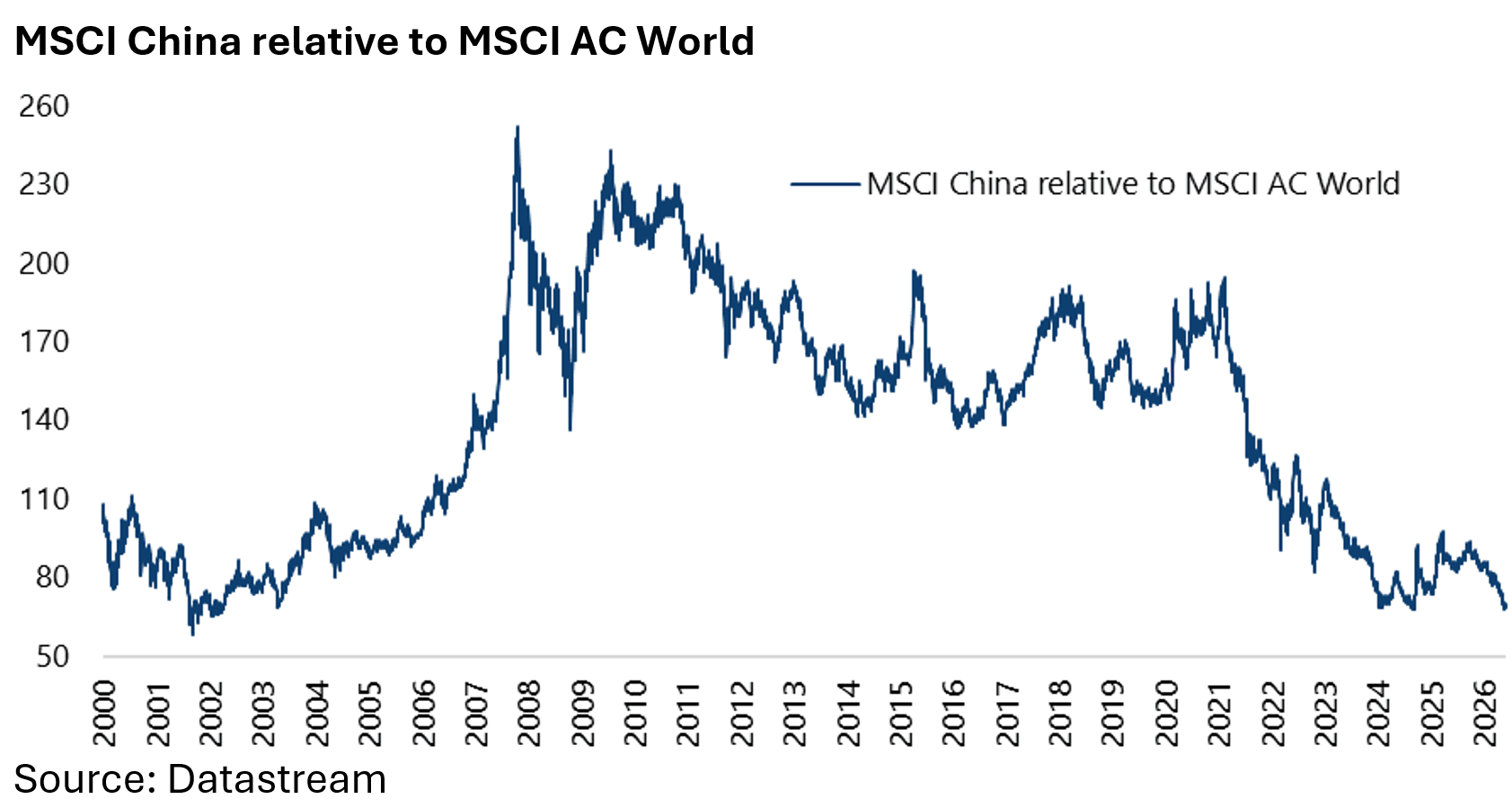

This is also the reason why MSCI China has underperformed the MSCI AC World Index by 72% since November 2007.

China and the “Slow Bull Market”

The base case is that this time will be different precisely because the government is focused on preventing another boom-bust outcome as a result of the need for another driver of wealth aside from property, given that there is, based on the latest data, Rmb172tn (US$25tn) in household deposits while property is down on average around 40% from the peak in China’s four major cities based on secondary market prices.

There have been even worse declines in the smaller cities where there has also been a collapse in transactions.

Still, there are now growing hopes that the residential property market is bottoming out in the major cities, given the relative lack of negative equity.

That said, there is no expectation of an imminent rebound.

So there is a clear need to promote the stock market.

As a result, the regulators have continued to promote higher dividend payout ratios and increased share buybacks, while they have also continued to control the supply of equity.

The result is that the stock market has been generating net cash for investors in the sense that dividends and share buybacks have been running ahead of IPOs and secondary issuance.

Thus, the onshore market distributed an estimated Rmb2.6tn of dividends last year and bought back Rmb143bn of shares, while equity issuance totaled Rmb1.2tn, including Rmb132bn of IPOs.

To help incentivise this process, the return on equity has been elevated as a key reference point to target for managers of state-owned enterprises, as opposed to net profits.

There has also been since October 2024 a Rmb300bn PBOC relending facility to help finance share buybacks.

This policy context has not been seen in any other bull cycles in China and is perhaps the best reason to give the benefit of the doubt to the “slow bull market” story.

Meanwhile, the other way the authorities have been seeking to reduce the risk of another boom-bust cycle is for the so-called national team to sell stocks when share prices rise too rapidly.

The Incentive for Chinese Households to Invest in Stocks is Growing

Meanwhile, the incentive to invest in equites must be growing, given declining interest rates and the lack of a visible recovery in the property market.

There are about Rmb50tn of 3-year household deposits due to mature this year, or 30% of total household deposits.

When that money was fixed three years ago, the three-year deposit rate was 3.5%. It is now 1.2%.

Valuations remain undemanding.

MSCI China now trades at 11.6x 2026 consensus forecast earnings assuming 13.4% earnings growth, while the CSI 300 is on 15.4x 2026 forecast earnings assuming 19.7% earnings growth, according to IBES.

Still, the deflationary backdrop clearly limits the potential for multiple expansion, with nominal GDP growth of only 4.9% YoY in 1Q26, which is why investors will pay a big premium for evidence of pricing power.

China Rushing to Replace any Reliance on Nvidia

Meanwhile if the political signaling in China of late has been on the need to do more to boost consumption, the evidence remains that the central government remains primarily focused on technological upgrading and independence, in terms of a lack of reliance on others, as reflected in the official signals that China no longer needs Nvidia chips.

Such is the negative consequence for the US of the decision in October 2022 to control the exports of advanced semiconductors to China.

Coming months will see IPOs of China’s leading DRAM and NAND flash makers which will also cause global investors to focus more on the growing competitiveness of China in the semiconductor area.

The China Securities Regulatory Commission (CSRC) disclosed on 19 May that NAND flash maker Yangtze Memory Technologies Corp (YMTC) has completed its so-called IPO tutoring filing registration, marking the start of its mainland A-share listing process (see Global Times article: “Two memory chipmakers push ahead with IPOs as epic progress signals China chip industry upgrade”, 19 May 2026).

YMTC is now expected to be trading in the Shanghai Stock Exchange’s STAR Market by late 2026.

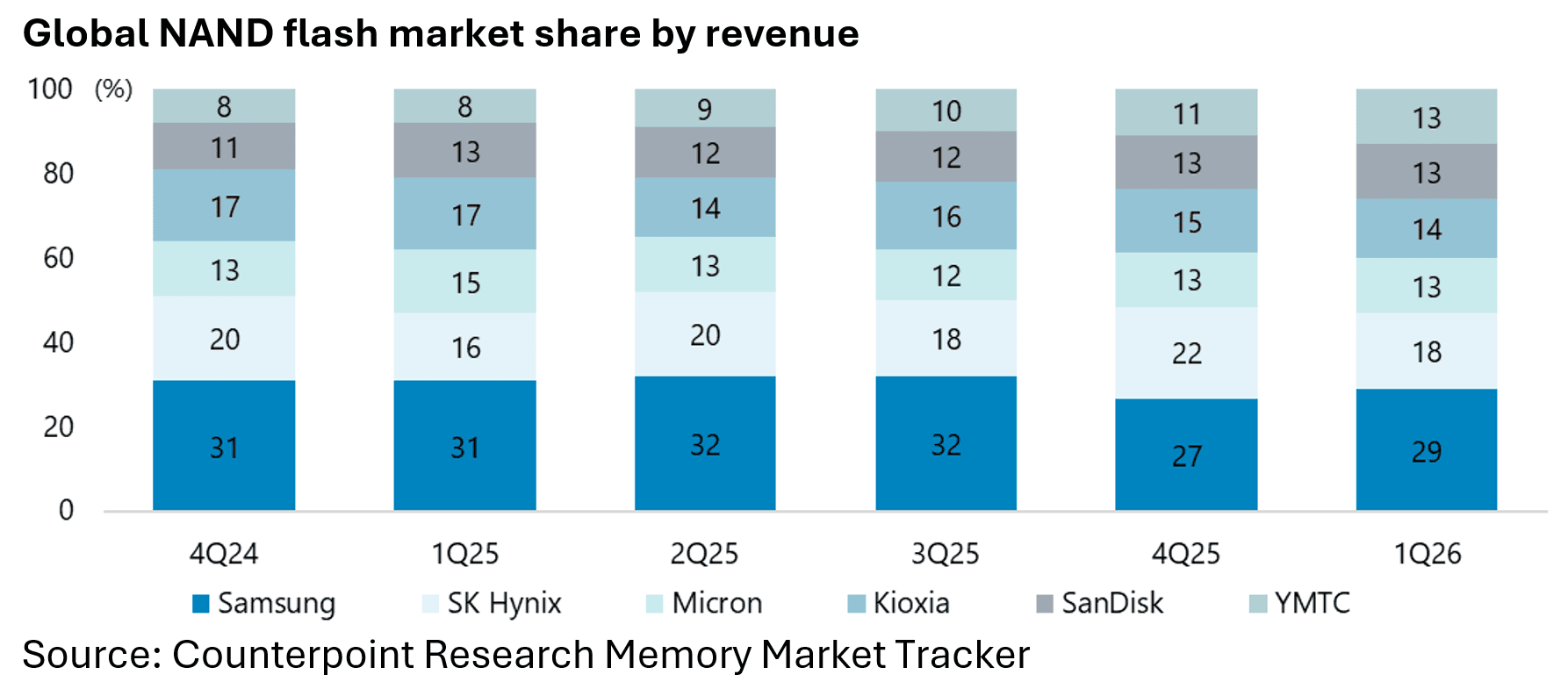

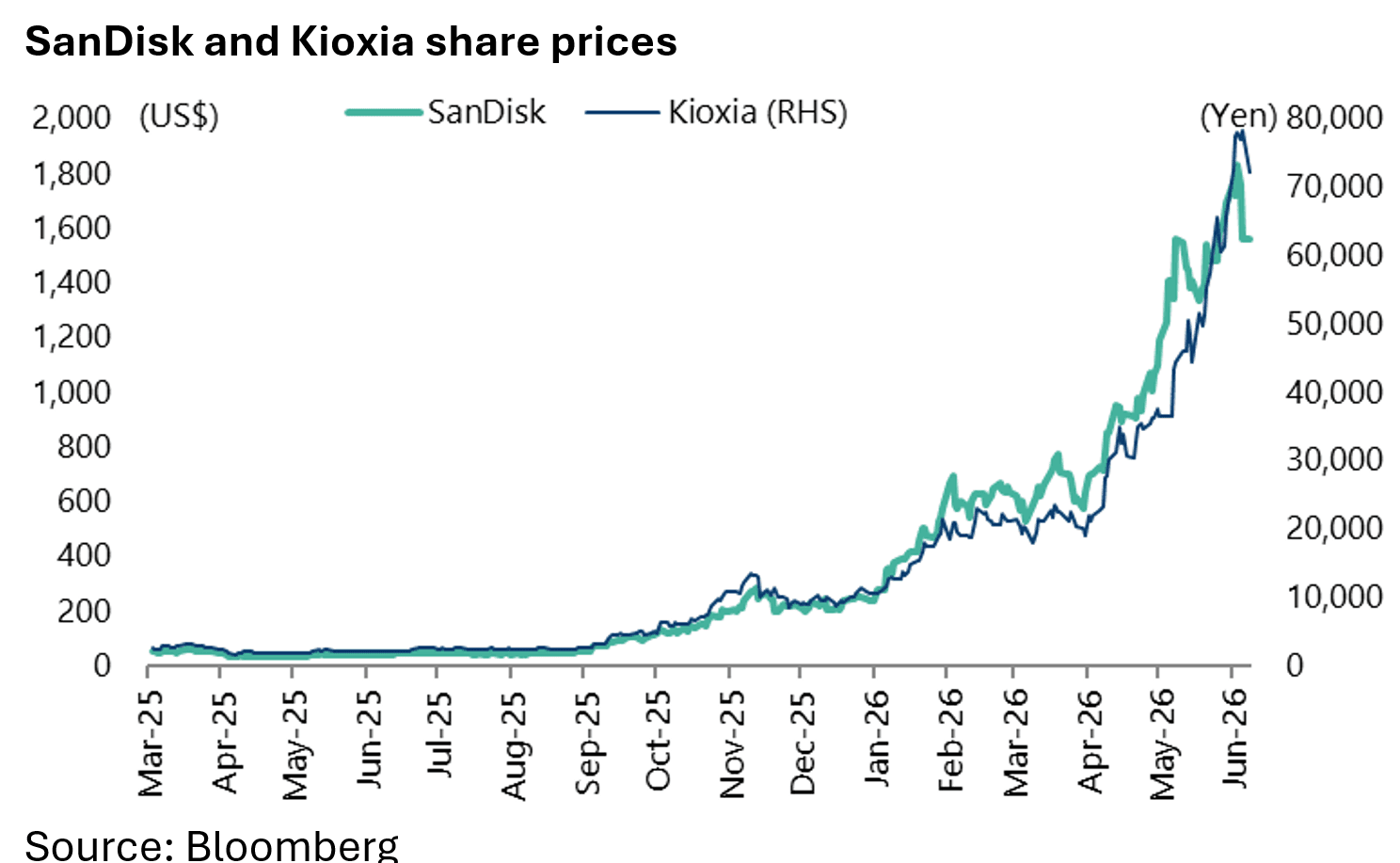

The company’s revenue exceeded Rmb20bn in the first quarter, more than doubling from a year earlier, while its NAND flash chip output accounted for more than 10% of the global market with a market share of 13% in the first quarter compared with shares of 13% and 14% respectively for two of the most high flying tech stocks in recent months, namely US-listed SanDisk and Japan-listed Kioxia.

YMTC is apparently at a similar level of technical expertise to its US and Japanese competitors, as reflected in its healthy market share.

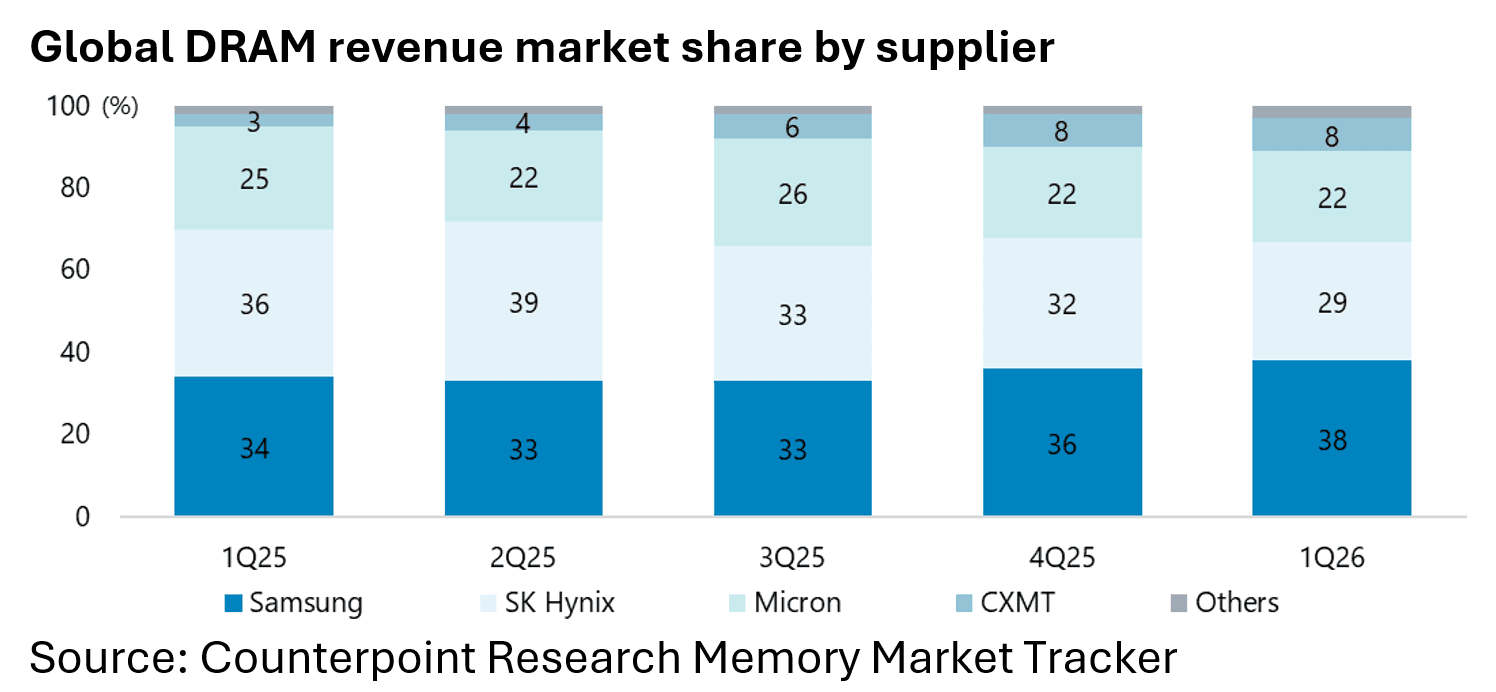

The leader in NAND flash globally remains Samsung Electronics with a 29% market share in 1Q26, a quarter when the total NAND flash market grew by 90% QoQ to US$46bn, according to Counterpoint Research.

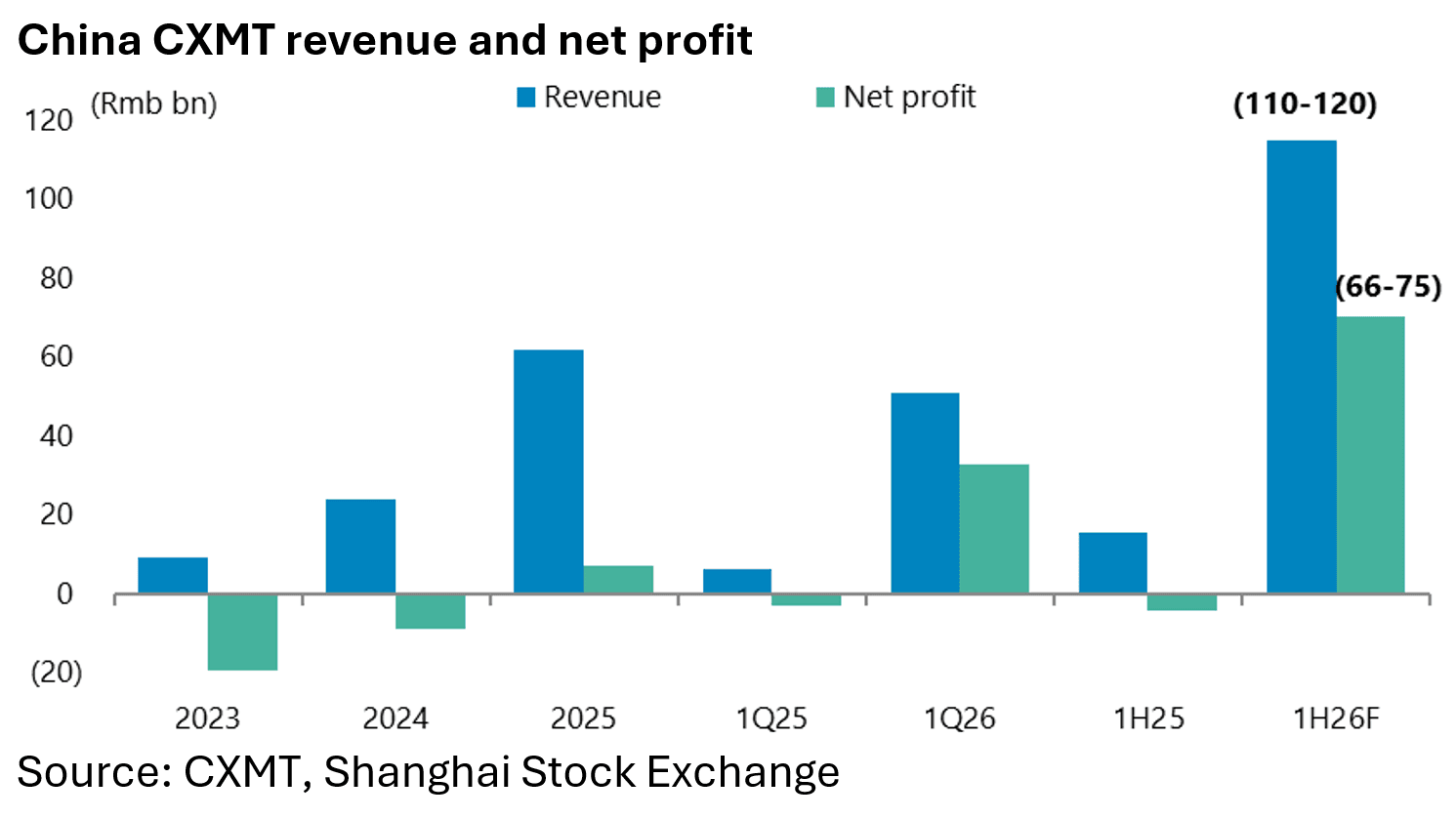

On a related theme, China’s leading DRAM maker ChangXin Memory Technologies’ (CXMT) application for an IPO in the Shanghai Stock Exchange’s STAR Market was approved in late May (see Global Times article: “CXMT Corp passes IPO review, plans 2nd-largest fundraising after SMIC”, 27 May 2026).

The company plans to raise Rmb29.5bn (US$4.36bn), which will be the second-largest IPO in the STAR Market after China foundry Semiconductor Manufacturing International Corporation (SMIC) in July 2020.

The listing is expected to occur in 3Q26.

The CXMT prospectus reflects the same explosive growth which has triggered the dramatic surge in profits reported by the world’s three dominant DRAM makers, Hynix, Micron and Samsung Electronics, who between them have an oligopolistic market share of 89% in 1Q26.

But CXMT is growing fast from a low base.

The company, according to the prospectus, expects revenue in the first half of this year to reach Rmb110-120bn marking growth of over 600% YoY.

While first half net profit is expected to reach Rmb66-75bn (US$9.8-11.1bn), compared with a net loss of Rmb4.1bn in the first half of 2025.

Still, by way of comparison, this is only 15-17% of the forecast first half net profit of Hynix this year.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.