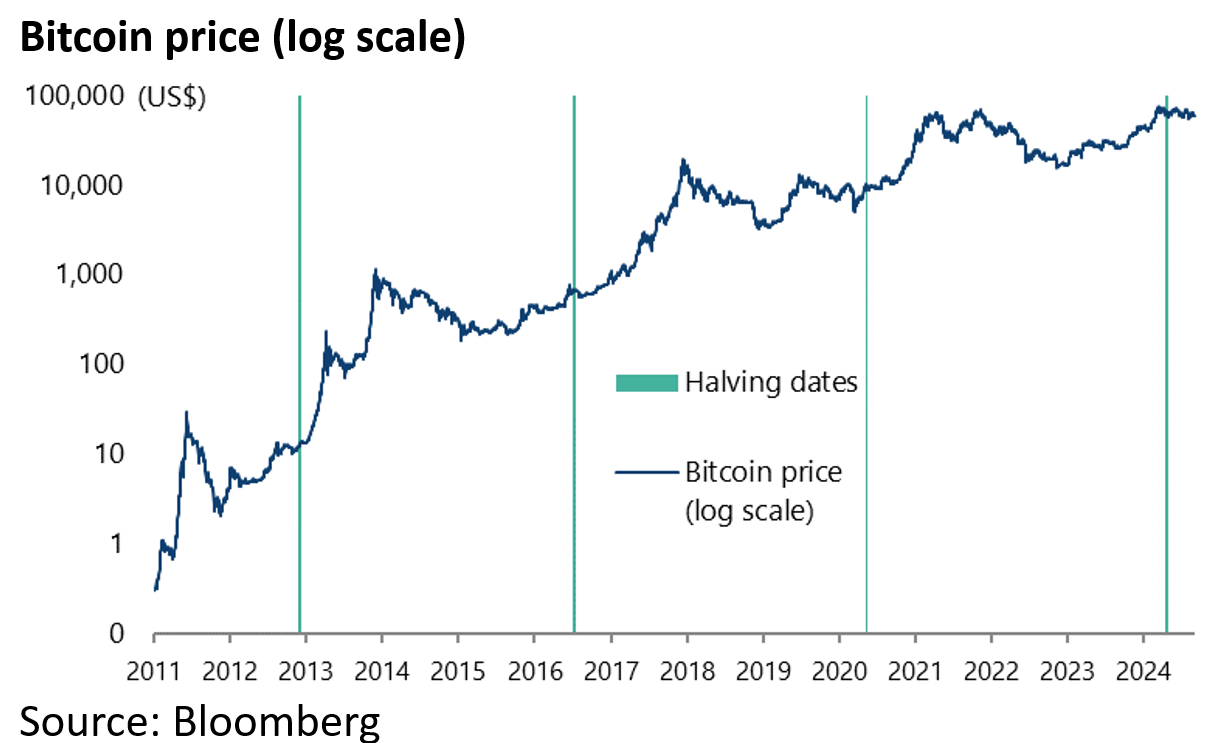

This writer still believes in Bitcoin.

Still it is worth noting that the recent extended period of healthy consolidation has been in the context of forced selling of nearly 50,000 Bitcoins by the Saxony state government in Germany.

50,000 is not a small amount.

The Saxony government came into possession of these Bitcoins as a result of criminal proceedings launched against an illegal TV/movie streaming site, Movie2k, which was shut down back in 2013.

According to the German news magazine Stern, the main operator made a deal with Dresden public prosecutor’s office whereby he voluntarily granted the German authorities access to his holdings of 49,858 Bitcoins after he was unexpectedly released from prison in January pending trial.

The somewhat bizarre point is that the state has been selling the Bitcoins even though the trial against the platform operator has not even begun yet.

The Dresden Public Prosecutor’s Office announced recently that the “market-stabilizing” sale of approximately 49,858 Bitcoins was successfully completed between 19 June and 12 July with the proceeds from the sale amounting to €2.64bn.

Presumably, the German authorities have been selling because they fear that the Bitcoin price might collapse.

The value of the Bitcoins confiscated was worth around €1.96bn at the time of the seizure in mid-January, according to the recent announcement.

But to believers in Bitcoin it makes no sense to have sold so soon after the halving in April, which is historically a big positive for the Bitcoin price in the following 12 months.

Mt. Gox Also a Forced Bitcoin Seller

Meanwhile, there is also another source of supply holders of Bitcoins will have to absorb.

That is that the former largest crypto exchange globally, Mt. Gox, which went bust in 2014, made further repayments to its creditors in July releasing yet more Bitcoins into the market.

Mt. Gox said in late June that it would start repaying its creditors in Bitcoins from the beginning of July.

It announced on 21 August that it has so far repaid over 19,000 creditors, out of an estimated total of 24,000 creditors.

As of 31 August, an estimated 96,790 or over 68% of the 141,686 Bitcoins owed to Mt. Gox creditors had been distributed, with the defunct Bitcoin exchange still holding 44,900 Bitcoins worth about US$2.6bn, according to blockchain analysis platform Arkham Intelligence.

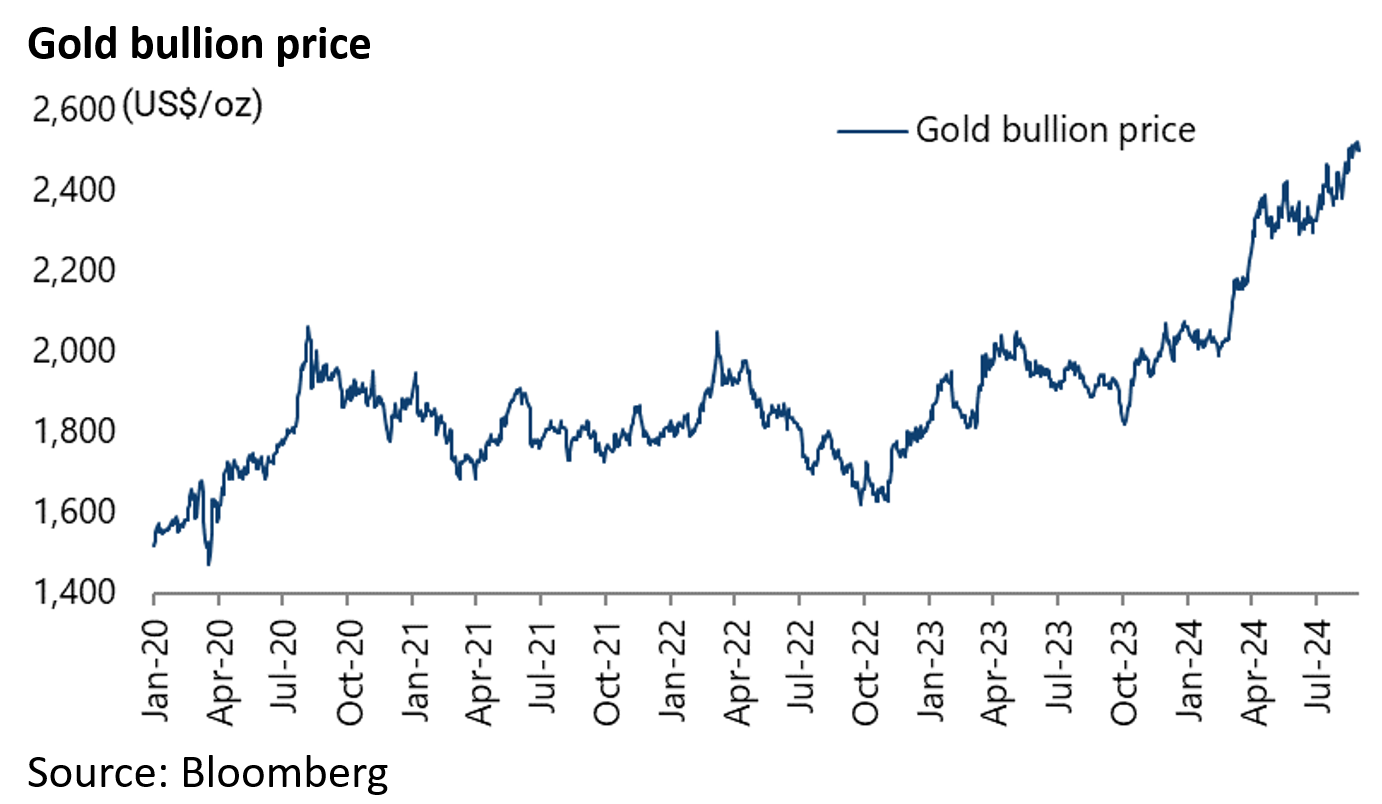

Gold is in a Much Better Spot

If that is the state of play as regards digital gold, gold itself reached a new closing high of US$2,524.6/oz on 27 August.

In this context, it is worth noting that there has been of late initial evidence of inflows into Western gold ETFs.

Gold ETFs’ holdings have risen by 73 tonnes or 2.9% from a recent low of 2,504 tonnes in mid-May to 2,578 tonnes, after declining from a recent high of 3,321 tonnes in April 2022 and a record high of 3,453 tonnes in October 2020, according to Bloomberg.

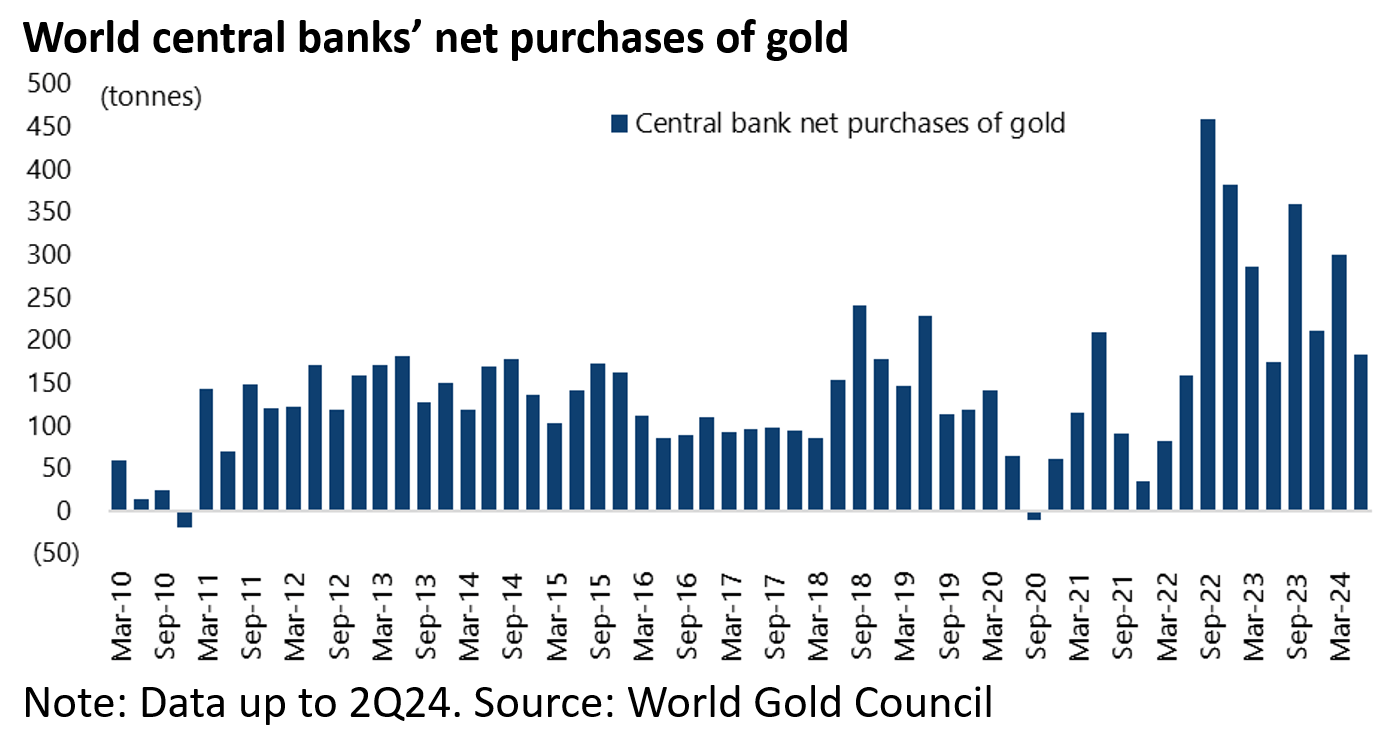

It also should be noted that world central banks bought a net 483 tonnes of gold in 1H24, after buying a record 1,082 tonnes in 2022 and 1,030 tonnes in 2023, according to World Gold Council data.

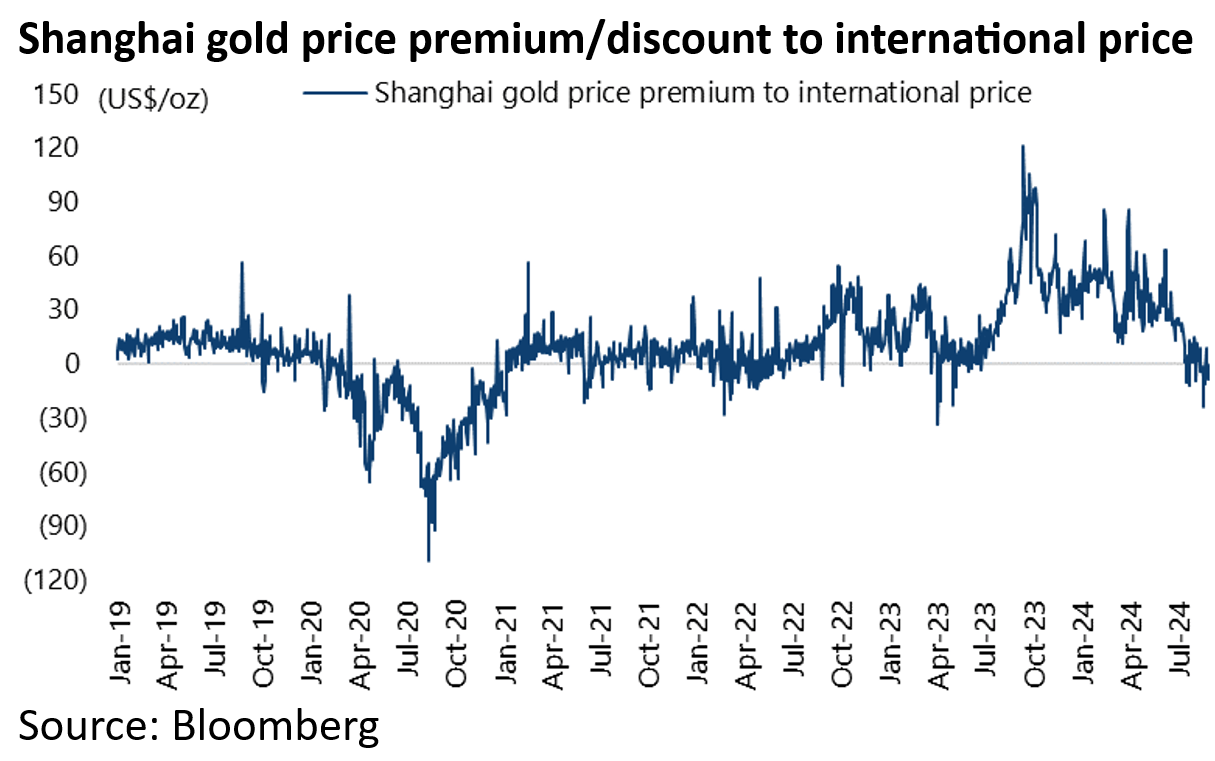

A Pullback By Chinese Buyers is a Risk to Watch

If these are the positives for gold, as is the increased expectations of renewed Fed easing, a nearer term negative has been recent evidence of weakening Chinese demand as reflected in gold recently moving to a discount in Shanghai for the first time since June 2023.

The Shanghai gold price has declined from a US$63/oz premium to international prices in mid-June to a US$23/oz discount on 20 August, the biggest discount since early April 2023, though it rose to only a US$8/oz discount at the end of August.

Bottom-up evidence of weakening demand in China also came with the release of quarterly data by Hong Kong-quoted Chow Tai Fook on 23 July, a retailer of gold and jewellery.

It reported a 20% YoY decline in retail sales value in 1QFY25 ended 30 June, with same store sales (SSS) declining by 26% YoY in the mainland and by 31% YoY in Hong Kong/Macau.

The latest macro data also shows weakening Chinese consumer demand for the yellow metal.

According to the National Bureau of Statistics, retail sales value of “gold, silver and jewellery” at enterprises above a designated size declined by 10.4% YoY in July.

The same data point was down 1.0% YoY to Rmb192.9bn in the first seven months of 2024, compared with a 13.3% YoY increase in 2013.

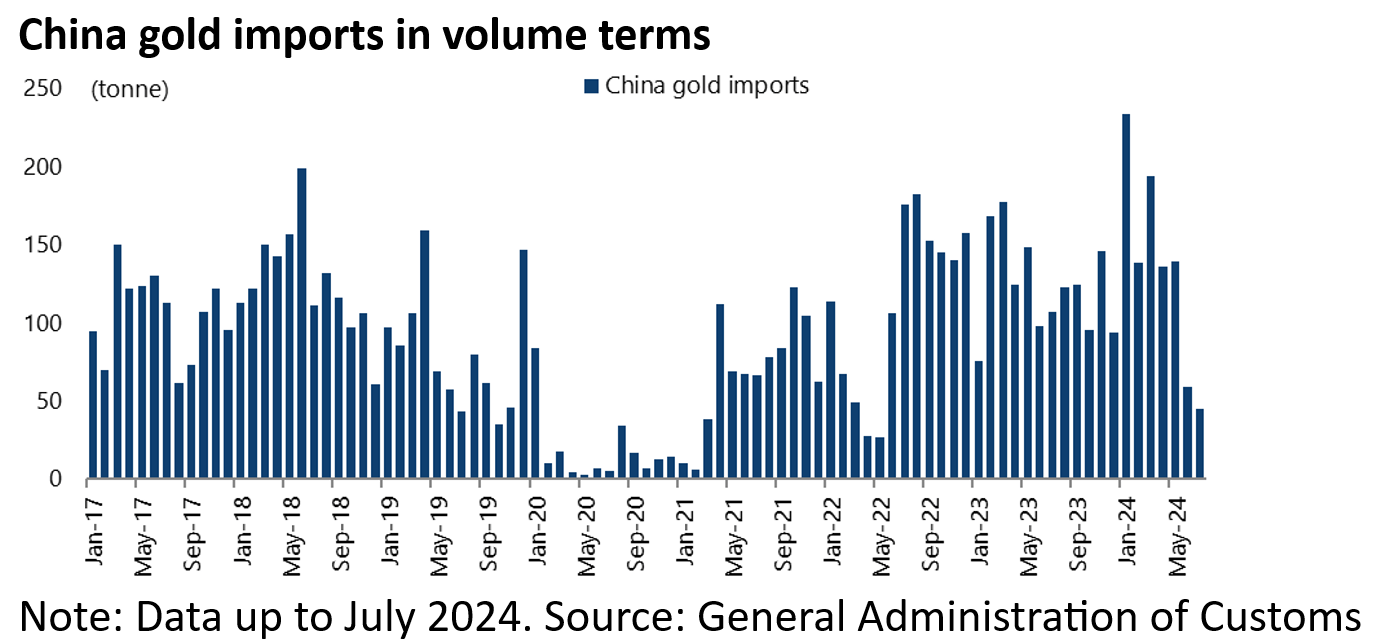

Meanwhile, China gold imports plunged by 24% MoM and 58% YoY to 44.6 tonnes in July, the lowest level since May 2022.

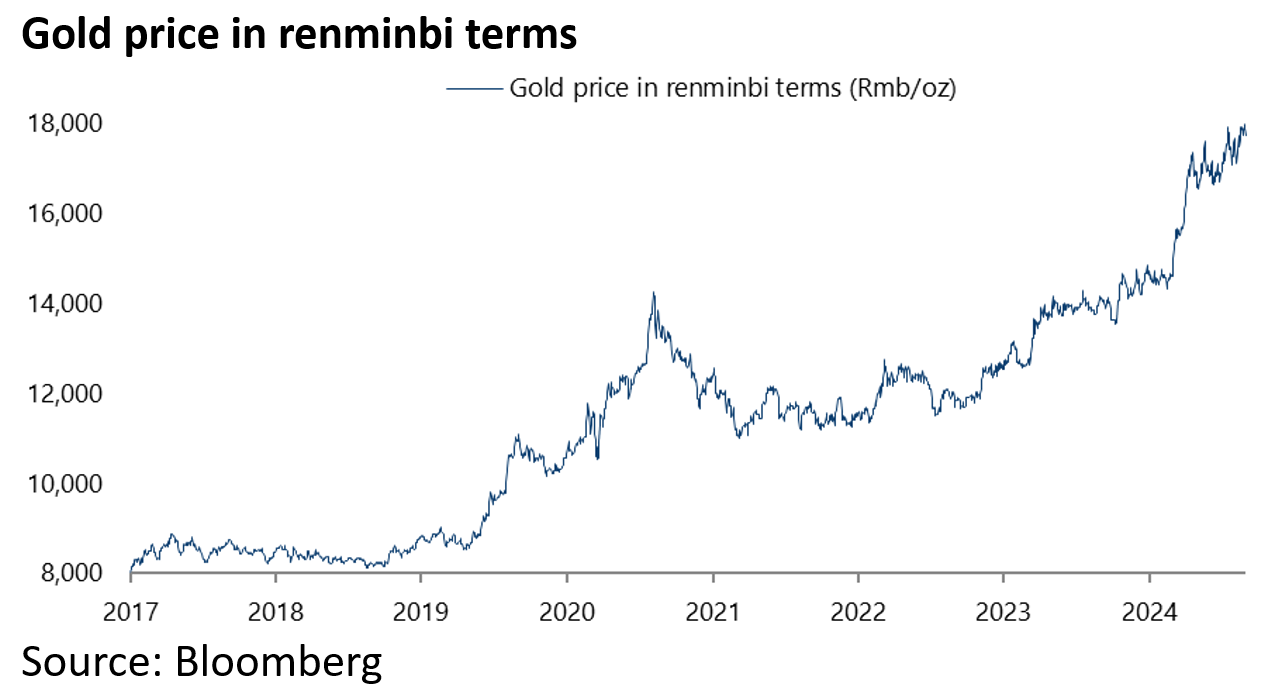

Such data presumably reflects Chinese consumers’ resistance to rising gold prices in renminbi terms. The gold bullion price in renminbi terms has risen by 41% since the beginning of 2023.

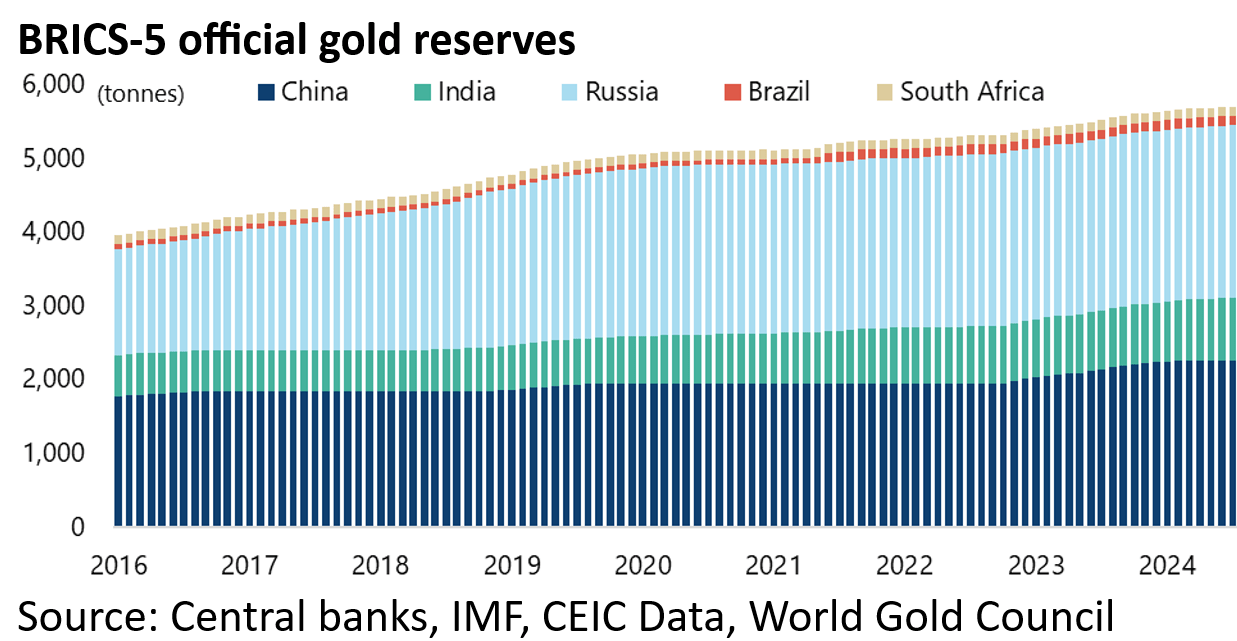

Meanwhile, official gold reserves in the original five BRICS members (Brazil, Russia, India, China and South Africa) have now risen by 442 tonnes or 8% since the start of 2022 to 5,701 tonnes at the end of July, with China’s official gold reserves rising by 316 tonnes or 16% over the same period to 2,264 tonnes and India’s gold reserves up 92 tonnes and 12% to 846 tonnes.

Still it is worth pointing out that the original BRICS members’ gold reserves remain well below America’s official stated gold holdings of 8,133 tonnes and the Eurozone’s 10,770 tonnes.

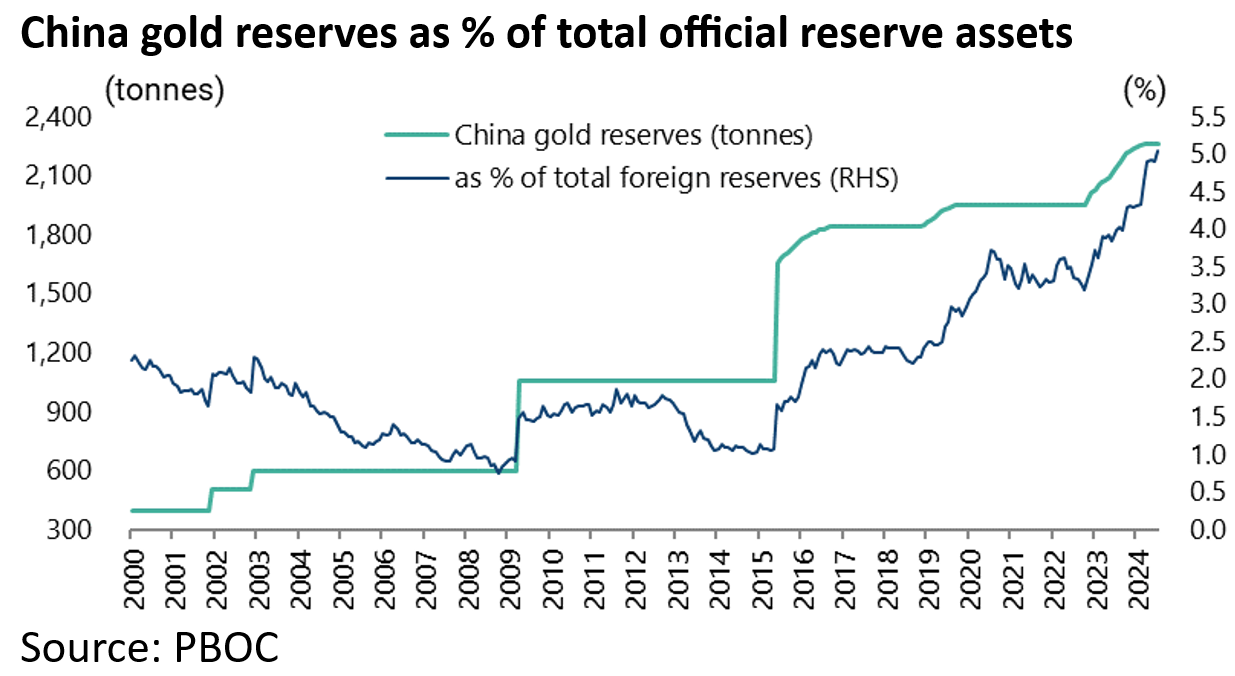

More importantly, after the 16% increase in gold reserves since October 2022, China’s total official gold reserves still account for only 5.1% of total official reserves assets.

But whether that figure captures all China’s holdings of gold, for example holdings by sovereign wealth funds and the like, would seem highly unlikely.

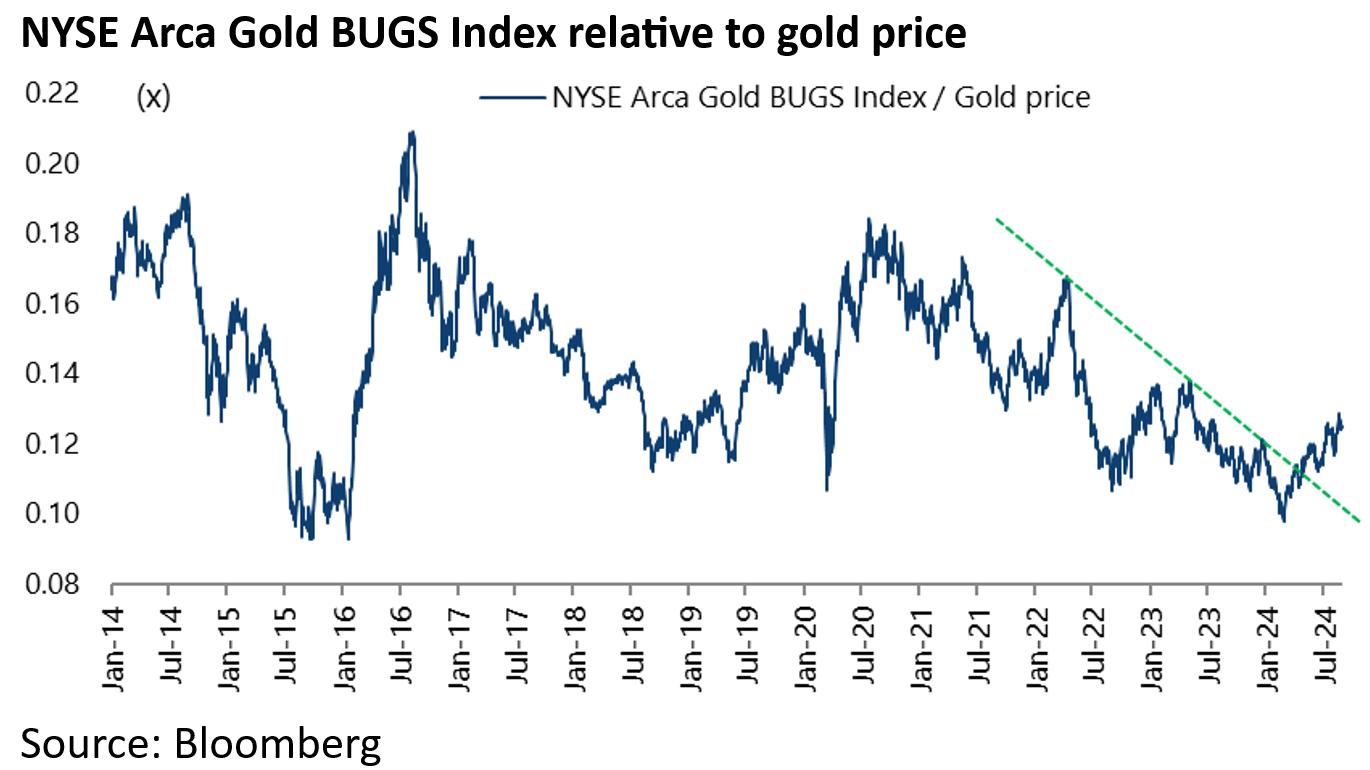

Finally on gold, it is worth noting that gold mining stocks have finally started to outperform gold bullion.

The NYSE Arca Gold BUGS Index has outperformed gold bullion price by 7.2% since 7 August and by 28.1% since the relative bottom reached on 28 February.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.