Debt Brake, What Debt Brake

These are historic times in global politics and economics.

Take Europe, for example.

The US decision to hold talks directly with Russia in February was not surprising, given the public stance taken by Donald Trump on the Ukraine conflict prior to the presidential election.

Still, it was clearly a long-awaited wake-up call for the Europeans who do not appear to have listened at all to what Trump was saying in the campaign.

In this respect, love him or hate him, Trump has a track record of seeking to implement the policies he has campaigned on.

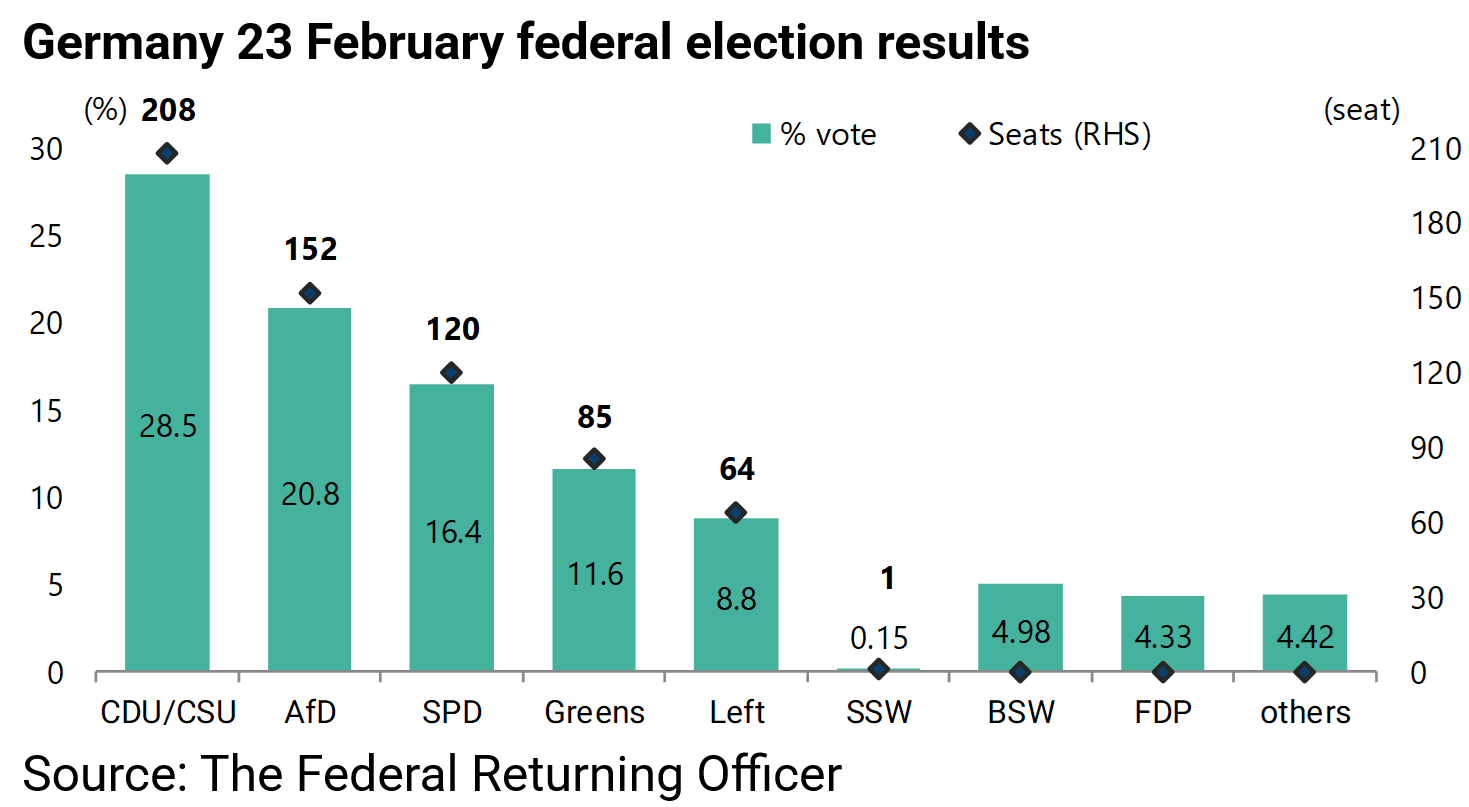

Helped by the stark messaging from Trump on the need for Europe to look after its own defences, Chancellor-to-be Friedrich Merz wasted no time in revising Germany’s so-called debt brake, making a mockery in the process of constitutional niceties following his victory in the 23 February German federal election.

Thus, CDU leader Merz 18 days after the election presented a bill to parliament, supported also by the SPD, to relax the country’s strict borrowing rules.

The legislation was passed on 21 March.

The goal is to exempt defence spending above 1% of GDP from the debt brake while there is also a plan for a €500bn infrastructure fund to be invested over 12 years.

The total projected increase in debt as a result of the above could be of the order of €900bn.

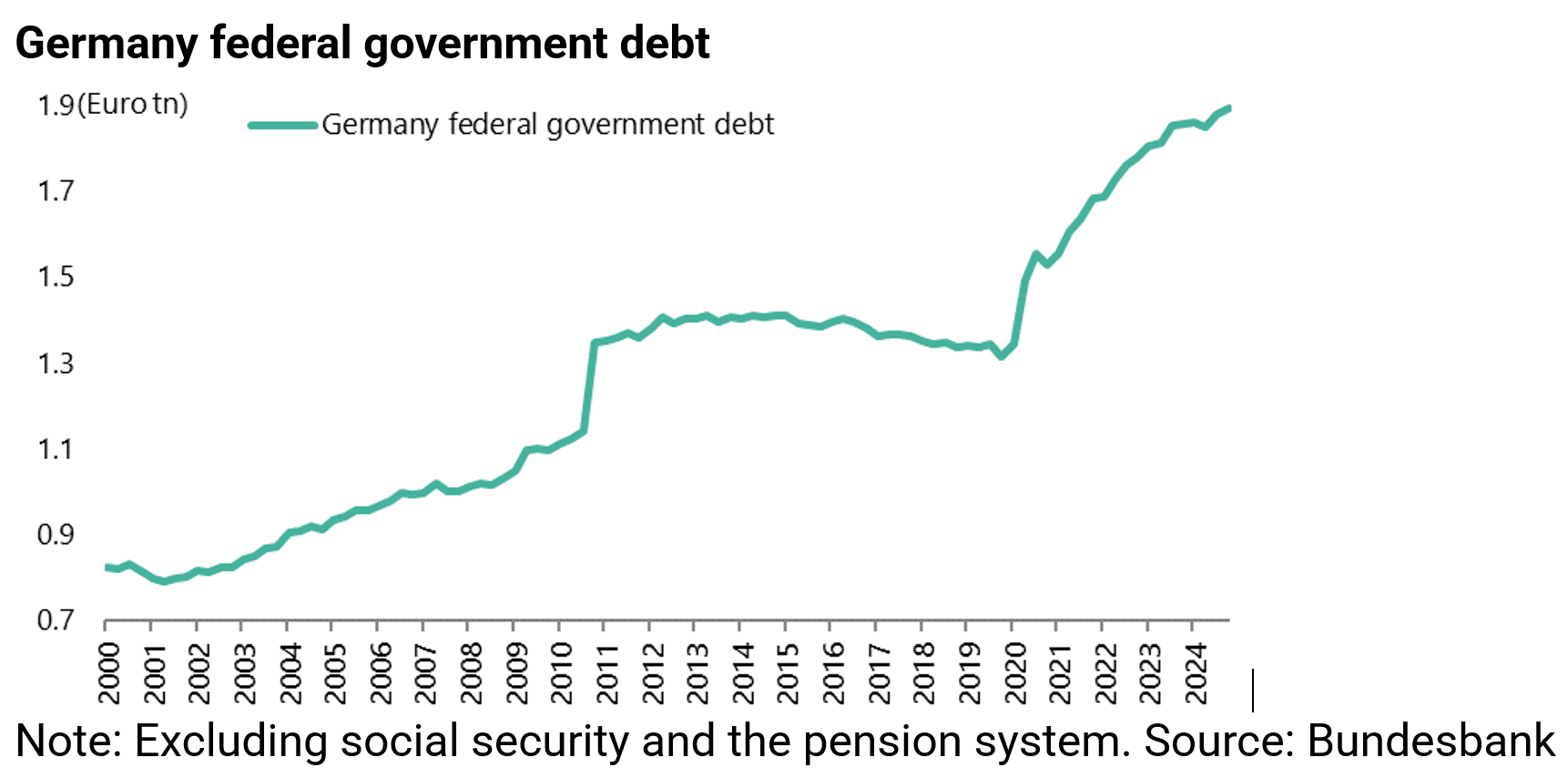

This is significant in the context of total German federal debt, excluding social security and the pension system, of €1.89tn at the end of 4Q24, according to the Bundesbank.

This swiftly executed revolution in fiscal policy, and it is no exaggeration to use that word, was made possible because the outgoing parliament, in the form of the Bundestag or lower house, remained in place until 25 March.

This mattered because a two thirds majority was required to pass the proposed changes.

That would have been much harder under the new parliament with the “far-right” AfD getting 20.8% of the vote and the two “far-left” parties getting a combined 13.8% in the election (see following chart).

Both were likely to oppose the measures

An Infrastructure Investing Renaissance is Coming to Europe

The icing on the cake in terms of the investment case for Eurozone equities would now be Germany under its likely new chancellor CDU leader, Friedrich Merz, actively embracing the recommendations of former ECB President and former Italian Prime Minister Mario Draghi’s report last September in terms of investing €750-800bn a year upgrading digital and physical infrastructure and actively pursuing banking and market union (see Draghi’s report: “The future of European competitiveness”, 9 September 2024).

This would amount to a change of policy, as Merz opposed the proposals of this report when it was first published because of his concerns about the EU “spiraling into debt” (see The European Conservative article: “German CDU Rejects Calls for Joint EU Loans”, 11 September 2024).

Trump’s tariff is the sort of catalysts which might trigger just a change in the German stance.

Indeed this writer thinks it is increasingly likely.

What Would a Resolution in Ukraine Look Like?

Meanwhile, this writer’s base case remains that for Washington to come to terms with Moscow on Ukraine will require a formal commitment that Ukraine is never joining NATO rather than cease fires and the like, with Ukraine becoming a buffer state.

The view is also that, if such a deal is made, Europe’s stated willingness to continue to fund the conflict will dissolve.

Resolution of Ukraine would clearly be a positive for most European equities.

DOGE’s Failure To Find Real Cost Savings is Bad for the Dollar

Back in America, criticism from the usual chatting classes has, unsurprisingly, been levelled at Elon Musk as he went about his business at DOGE.

Musk said in February that, once markets start to see the impact of DOGE in terms of the progress being made cutting federal debt, interest rates on Treasury securities would begin to fall.

This has raised the potential at least for DOGE to change the longstanding narrative of this writer, namely that Treasury bonds are in a structural bear market.

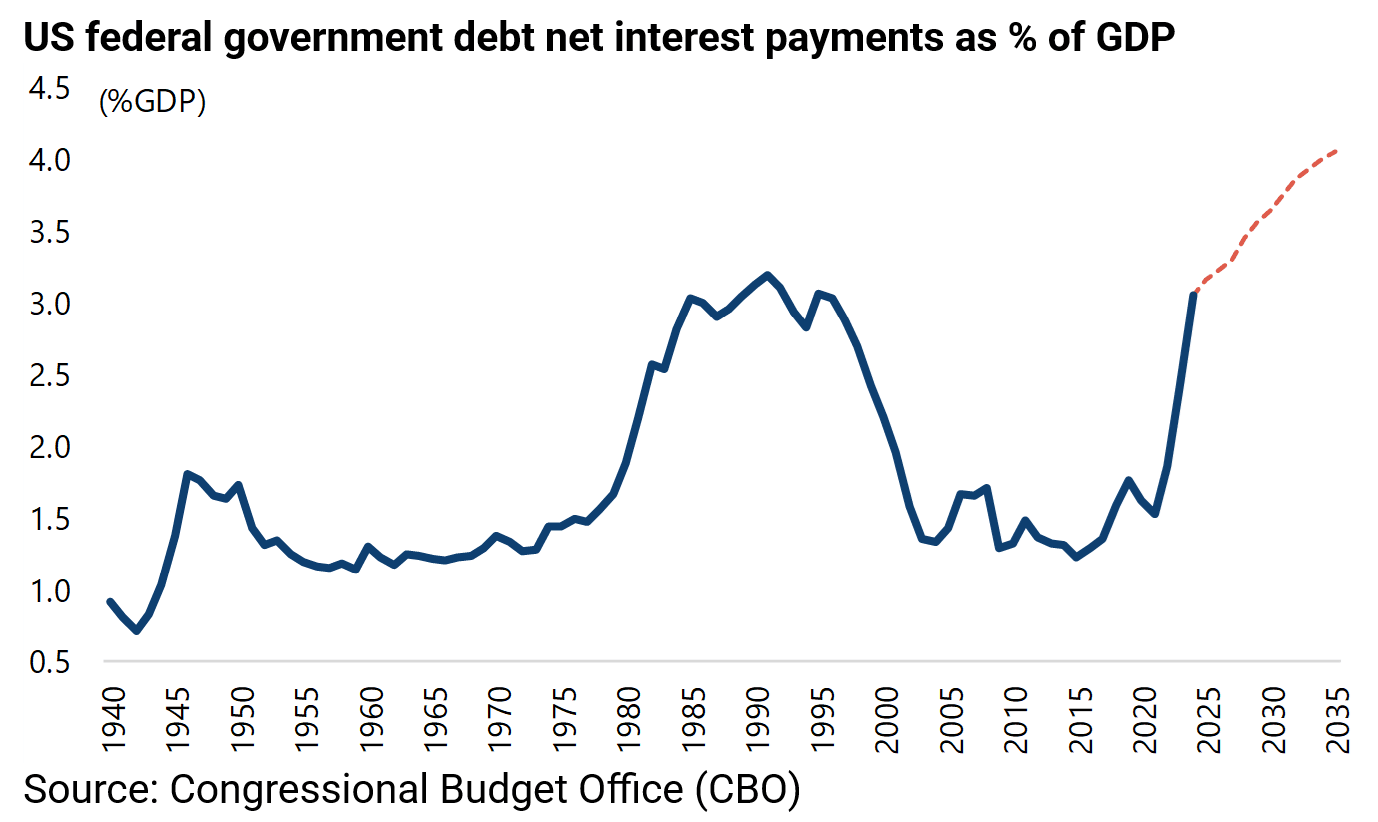

Certainly, any cut in interest rates will be welcomed, given that US federal debt net interest payments are projected by the Congressional Budget Office (CBO) to rise to 4.1% of GDP by 2035, the highest level since at least 1940.

They are currently 3.2%.

Still the DOGE narrative has now changed dramatically with Musk now reducing the anticipated/targeted savings to only US$150bn, compared with US$1tn anticipated last month and the original target of US$2tn.

It is also the case that Musk is now due to step down from DOGE in late May.

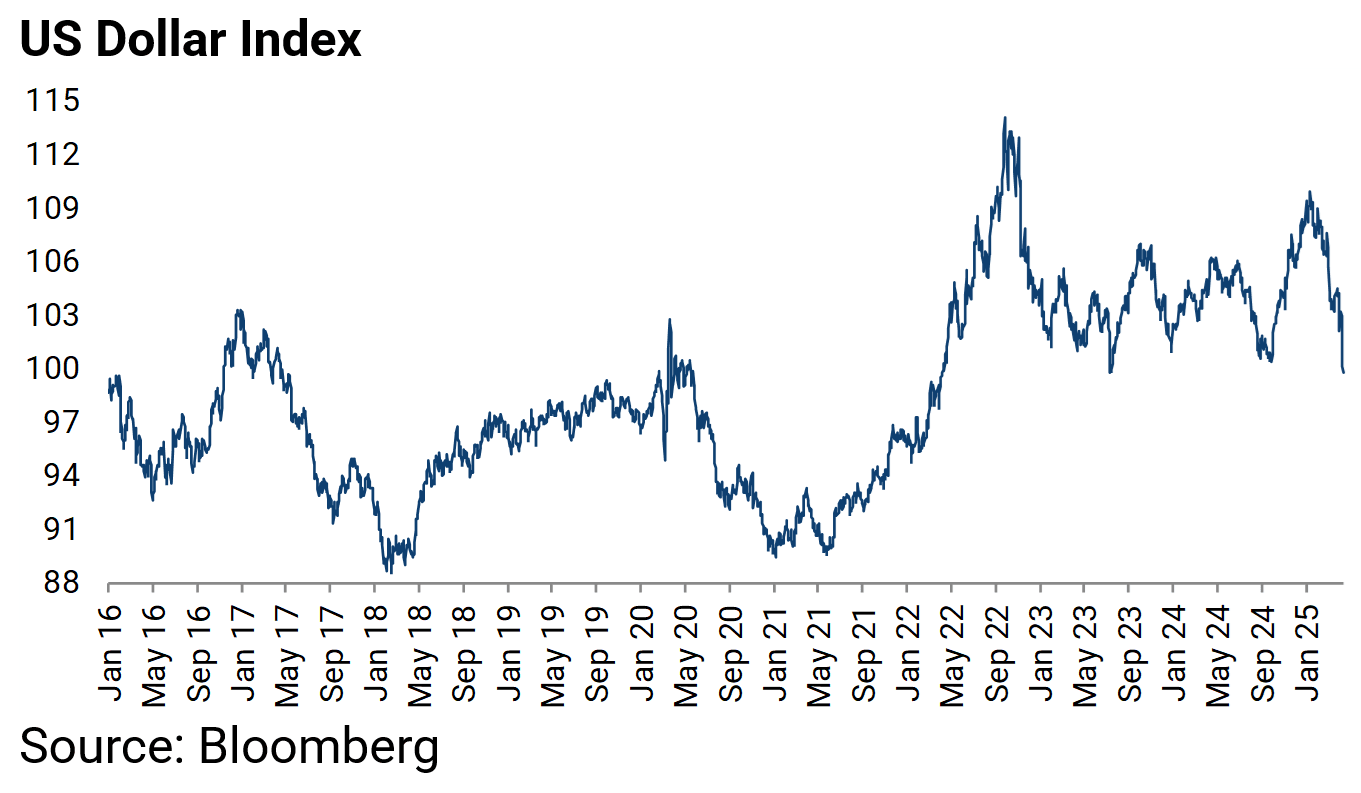

Such developments have to be dollar-bearish, which is why this writer’s base case remains that the US dollar peaked when Donald Trump took office on 20 January, which is also more or less what happened when he became president for the first time in January 2017.

The US Dollar Index then peaked on 3 January 2017, prior to Trump’s inauguration on 20 January, and subsequently declined by 15% to a low in February 2018.

As for this year, the US dollar index peaked on 13 January and has since declined by 9.5%.

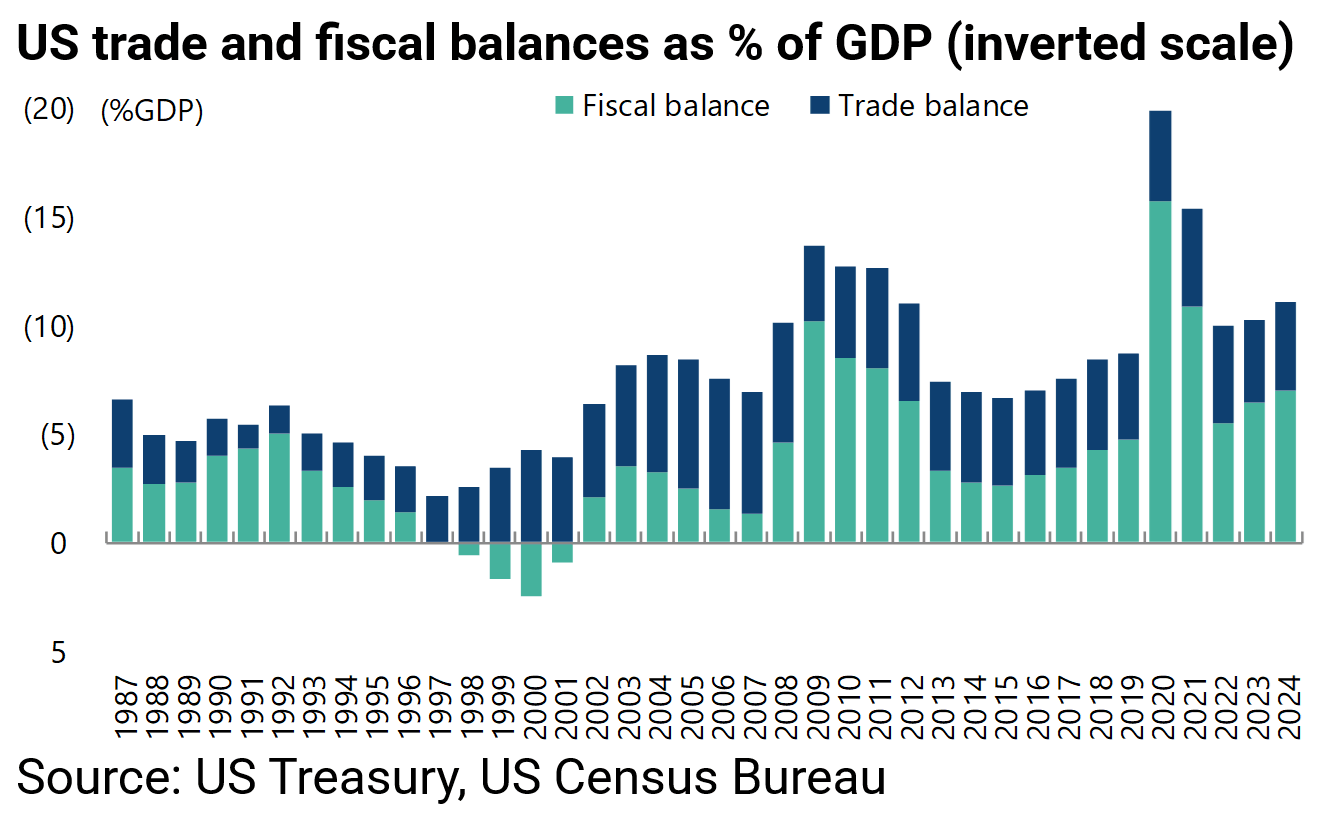

US Deficits Are Not Far Off Peak Levels

The other issue as regards the US dollar, which does not get the attention it probably merits, is America’s twin deficits with a fiscal deficit running at 7% of GDP and a trade deficit at 4.1% of GDP in the calendar year 2024.

This is not so far off peak levels going back to 1987, excluding the pandemic.

Annual trade and fiscal deficits as a percentage of GDP peaked at 13.6% in calendar 2009, though they were much higher at 19.9% in 2020 during Covid.

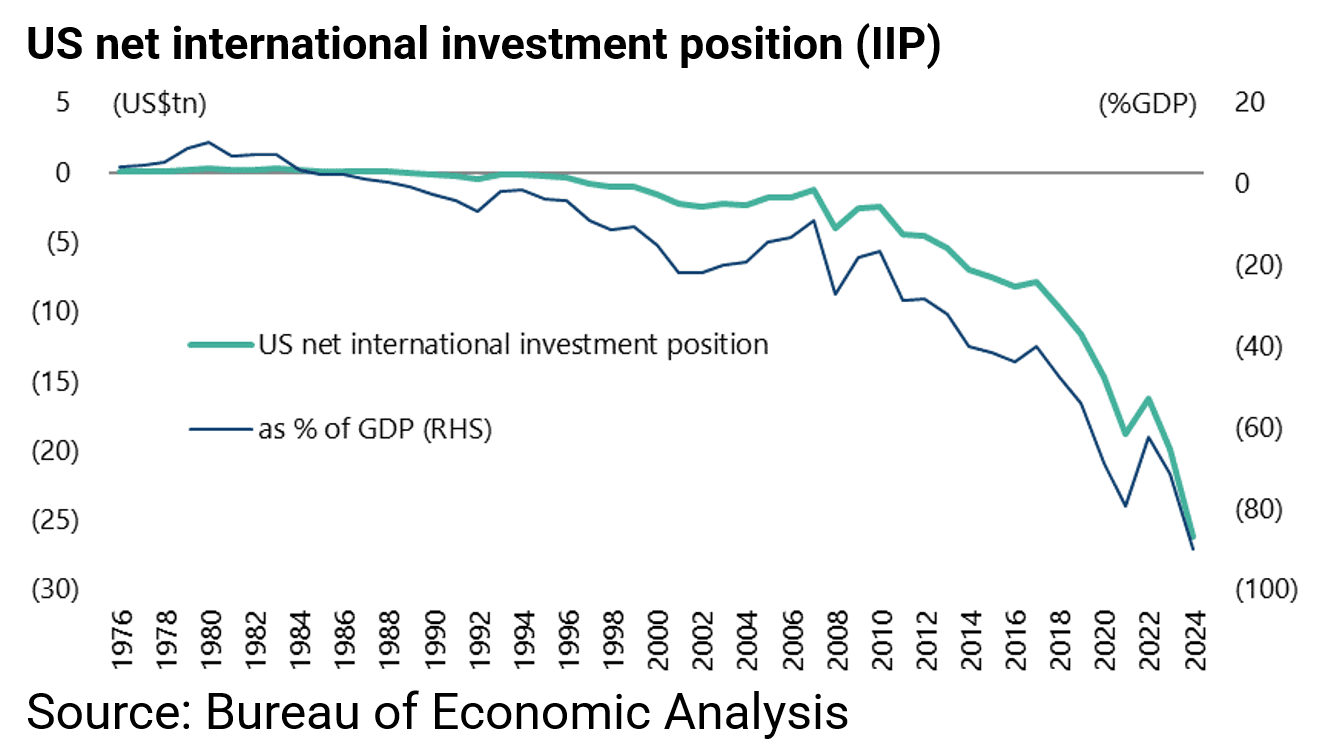

The Risk From Foreigners Owning a Record Amount of US Assets.

The other related extremely important issue is the deteriorating trend in America’s net international investment position (IIP), which essentially shows that foreigners have invested a lot more in America than Americans have invested overseas.

This measures the difference between US residents’ foreign financial assets and foreigners’ holdings of US assets.

Thus, the US net IIP deficit has risen from US$7.8tn or 39.9% of GDP at the end of 2017 to a record US$26.2tn or 89.9% of GDP at the end of 4Q24.

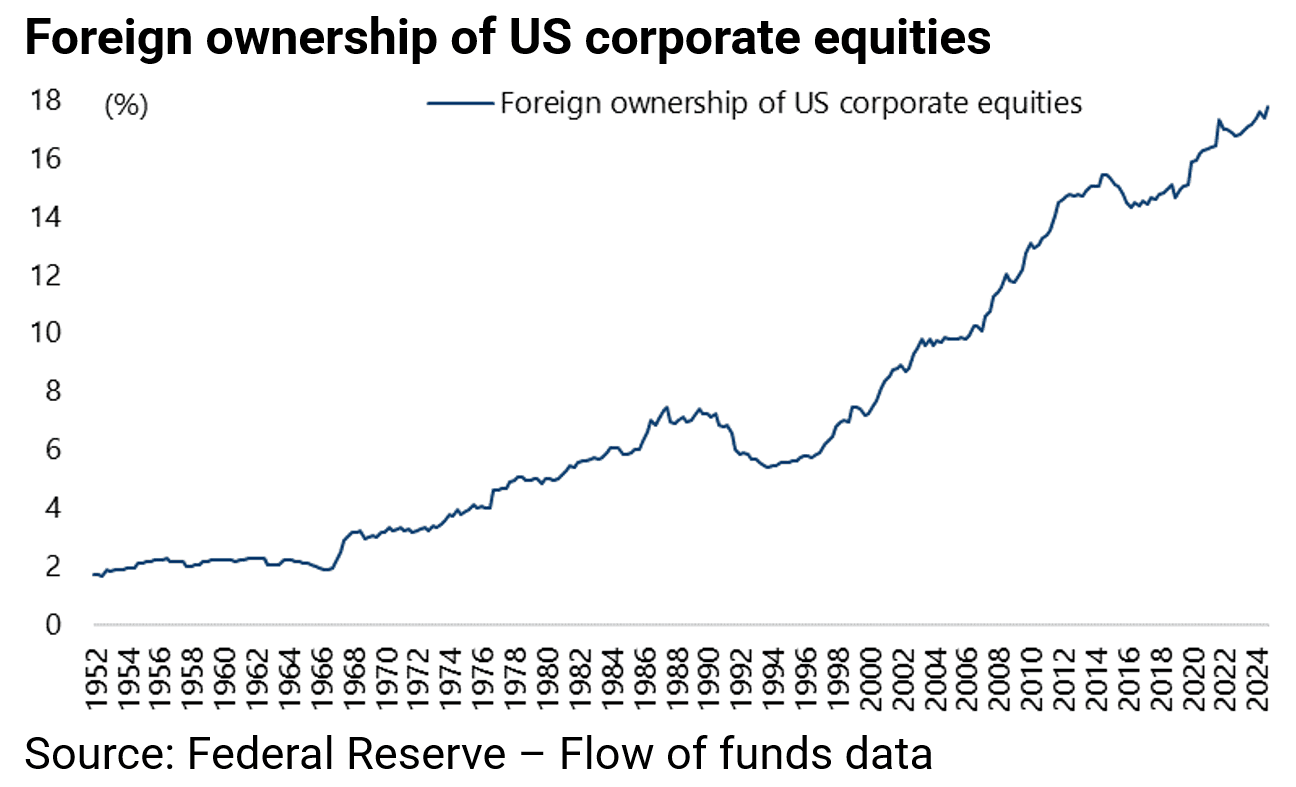

This trend at a stock market level has been reflected in recent record foreign ownership of equities.

Thus, foreign ownership of US corporate equities rose to a record 17.8% at the end of 4Q24, according to the Fed’s flow of funds data.

That is likely to be proven to be an all-time peak.

A Massive US Dollar Unwind is a Real Risk

All of the above is evidence of extremes, which creates the potential at least for a massive unwind out of US financial markets and out of the US dollar.

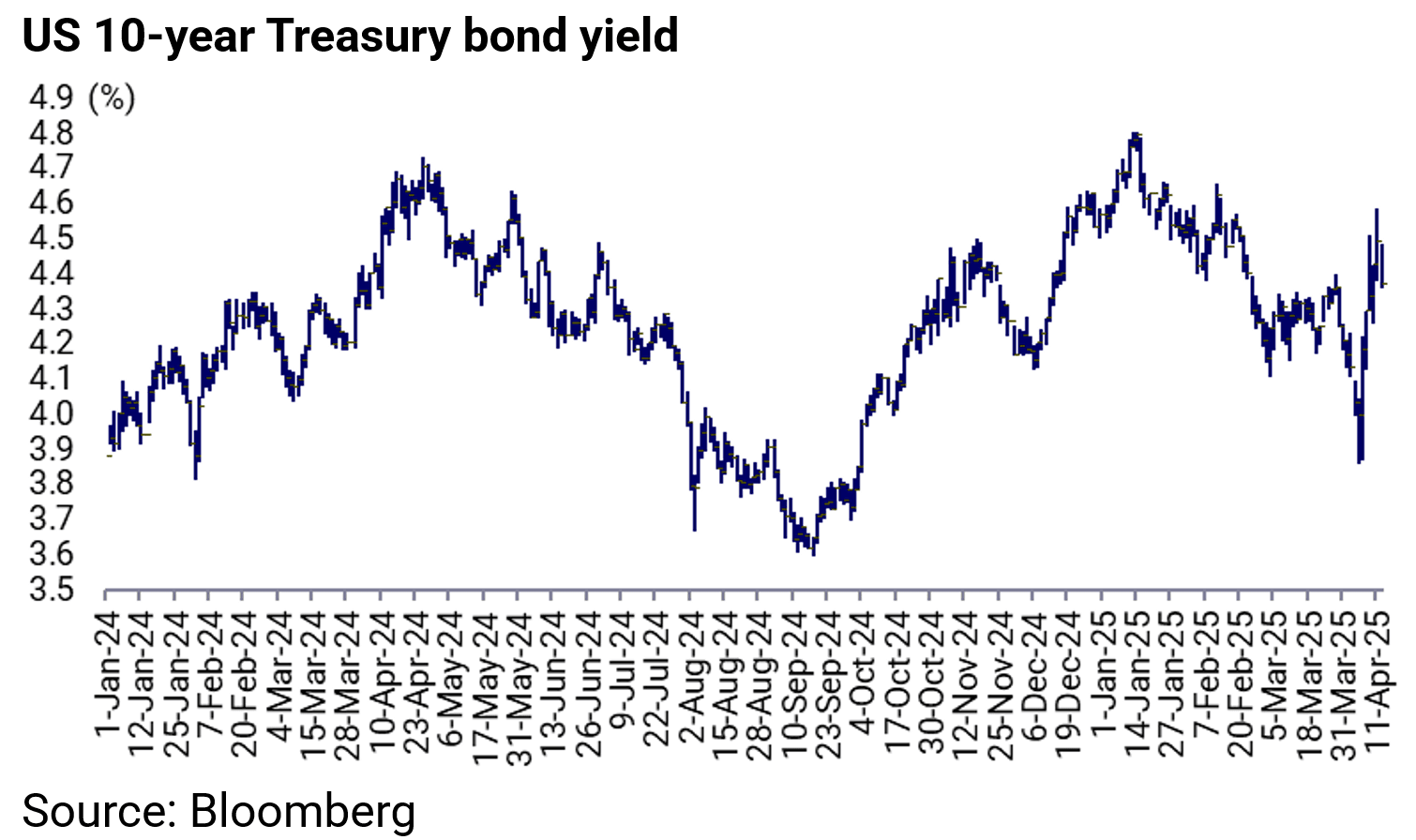

This is also why it remains a key issue whether supply concerns were behind the renewed sell-off in Treasuries last week.

The 10-year Treasury bond yield rose by 73bp from a recent low of 3.856% on 4 April to a recent high of 4.586% on 11 April.

Meanwhile, the focus on “American exceptionalism” late last year remains a sign of a major top in terms of America’s share of global stock market capitalisation, as previously discussed here (see “Why The Failure of DOGE is Our Base Case”, 11 February 2025).

There is only one area where the US is truly exceptional. That is the ability to print the reserve currency of the world.

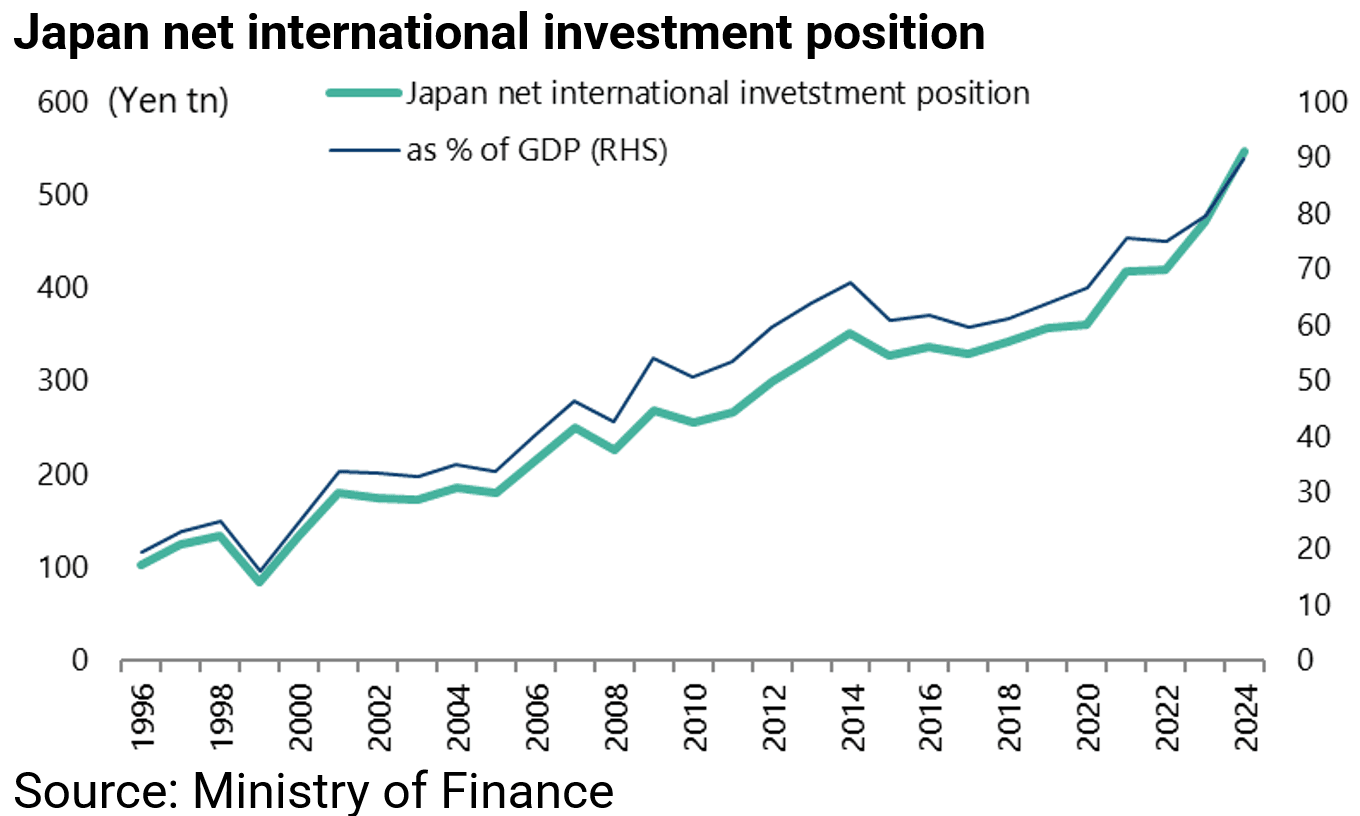

Repatriation of Capital a Huge Potential Catalyst for Japan

Meanwhile, if America is in hock to foreigners, the opposite is the case for Japan in terms of that country’s net international investment position.

Japan’s net international investment position has risen from ¥360bn or 66.7% of GDP at the end of 2020 to ¥547bn or 89.8% of GDP at the end of 4Q24.

This is why there remains a massive potential for repatriation of capital back into Japan.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.