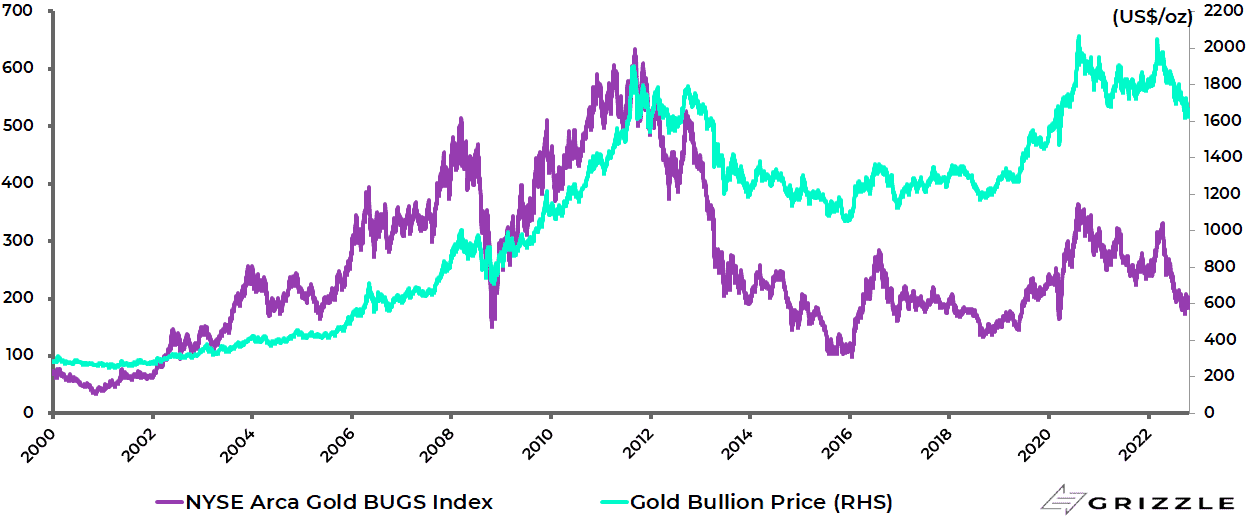

This has so far been an annus horribilis for gold mining stocks with gold stocks underperforming a declining gold price, as the mining companies have suffered a double whammy of a declining gold price and rising costs leading to deteriorating margins.

The NYSE Arca Gold BUGS unhedged gold mining index is now trading at the same level as in August 2005 when gold was US$430/oz.

The index is down 23.1% so far in 2022, compared with a 10.1% decline in the gold price.

Gold bullion price and NYSE Arca Gold BUGS unhedged gold mining index

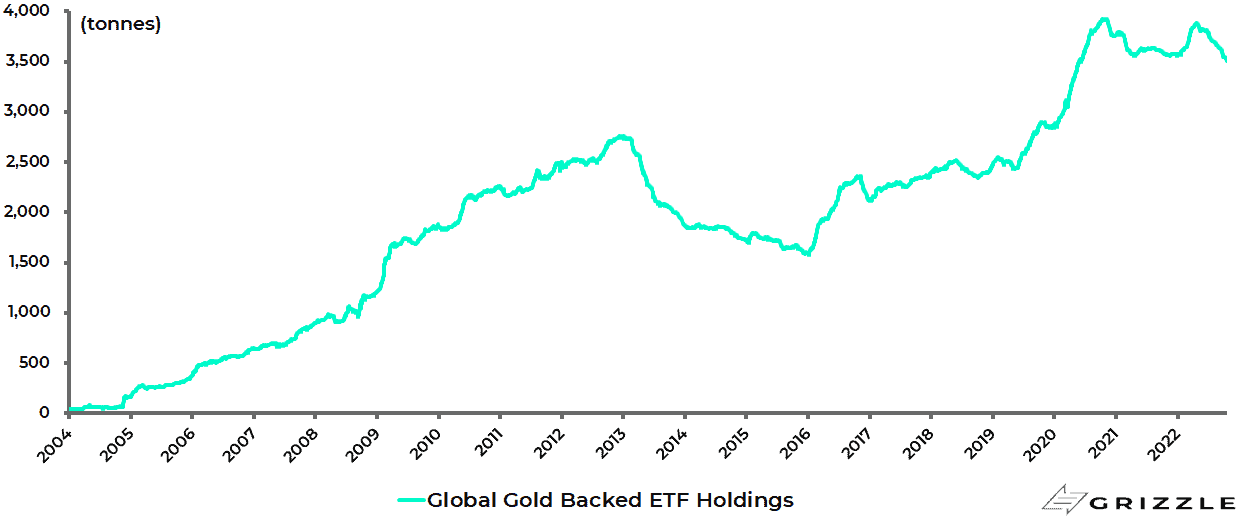

Meanwhile, the inflows into gold ETFs seen earlier this year have completely unwound.

Global gold ETFs’ holdings rose by 317 tonnes from 3,572 tonnes at the start of this year to a recent high of 3,889 tonnes on 22 April and have since declined by 386 tonnes to 3,503 tonnes as of 21 October, according to the World Gold Council.

World Gold ETF holdings

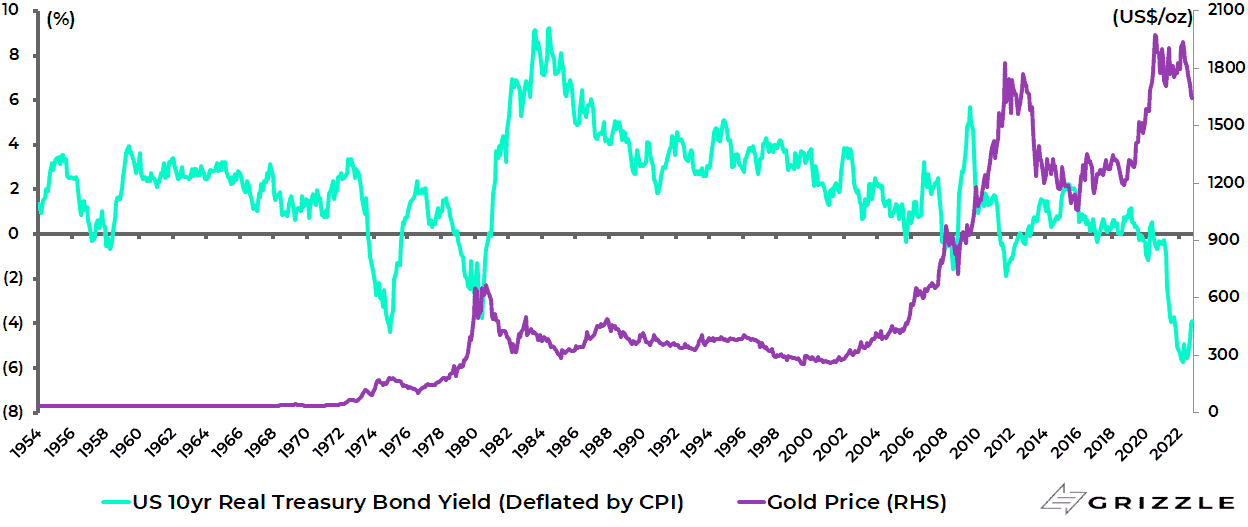

There is no surprise that gold should be under pressure in US dollar terms given dollar strength and the almost schizophrenic mood swing engaged in by the Fed since Pivot Powell’s U-turn last November.

But if gold’s weakness this year in US dollar terms does not surprise, much more disappointing was the yellow metal’s failure to rally more last year before the Fed’s U-turn in November when inflation was on the rise and interest rates were becoming ever more negative.

Gold price and US real 10-year Treasury bond yield (deflated by CPI)

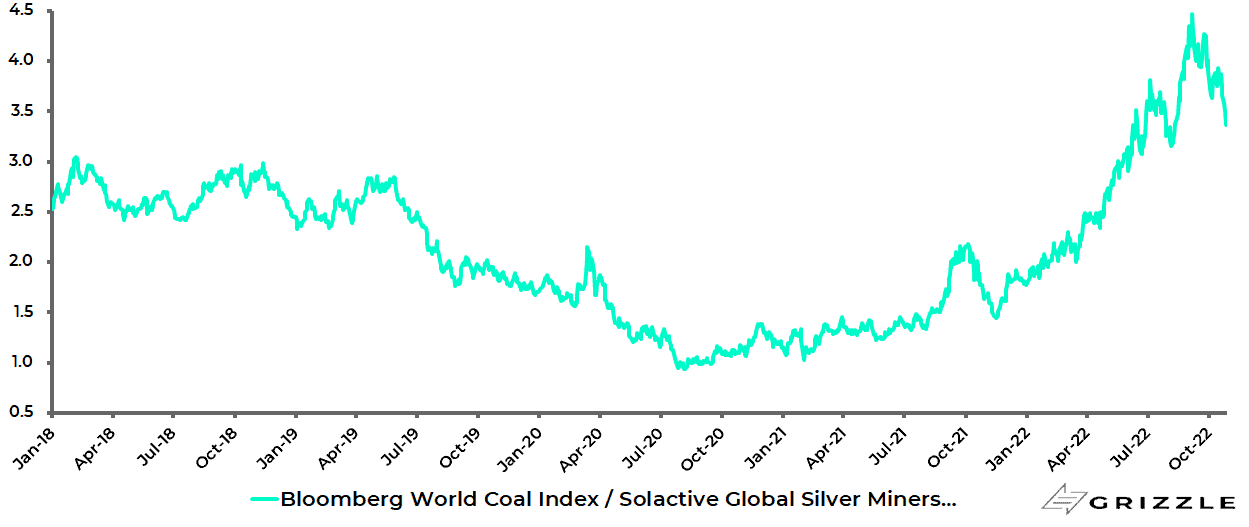

Still there is no doubt that gold, and higher beta silver, will be the key beneficiaries of any sudden change in Fed stance, be it driven by sudden recessionary concerns and/or a related decision to fudge the 2% inflation target.

In this respect, the potential for a dramatic market switch from energy to precious metals can be seen in the chart of the relative performance of coal and silver stocks since silver peaked in August 2020.

Thus, the Solactive Global Silver Miners Index has declined by 50% since peaking in August 2020, while the Bloomberg World Coal Index is up 83% over the same period.

Bloomberg World Coal Index relative to Solactive Global Silver Miners Index

Still, interestingly, the world coal stocks index has underperformed the silver stocks index by 23% since early September.

Meanwhile, the silver price has declined by 34% since peaking in August 2020 while coal prices are up 664% over the same period.

Rising Operating Costs Getting you Down, Own the Royalties

With gold mining companies contending this year with rising costs, it is also worth noting the attractions of the royalty business model where investors get leverage to a rising gold price without being exposed to the operating risks of running a mine, including rising costs.

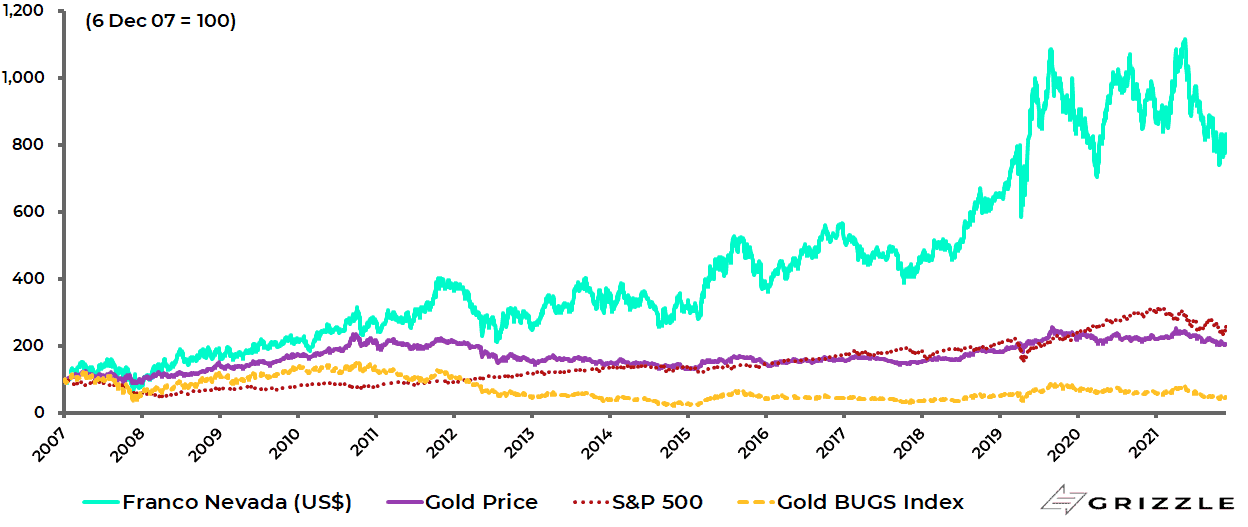

This can be seen in the 15% compound annual growth rate (CAGR) in US dollar terms achieved by Franco-Nevada, the largest royalty company, since it was listed in December 2007 compared with the 7%, 5% and -5% CAGR achieved, respectively, by the S&P500, gold and the NYSE Arca Gold BUGS Index of unhedged gold mining stocks over the same period.

Franco-Nevada relative to S&P500, gold and gold mining stocks

Gold is Still Figuring Out How to Content with Competition from Digital Assets

One continuing negative for gold is demographics, in the sense of whether millennials will ever have any interest in investing in gold given Bitcoin’s status as an alternative store of value.

It is therefore interesting to note a World Gold Council initiative called Gold247.

One of the goals of this initiative is to utilise blockchain technology to allow for gold to be traded as a digital asset via tokenisation.

As a baby boomer, this writer finds it hard to abandon the notion that a key part of gold’s appeal is that it is physical.

Still allowing it to be owned via tokenisation should broaden gold’s appeal to a universe of younger buyers.

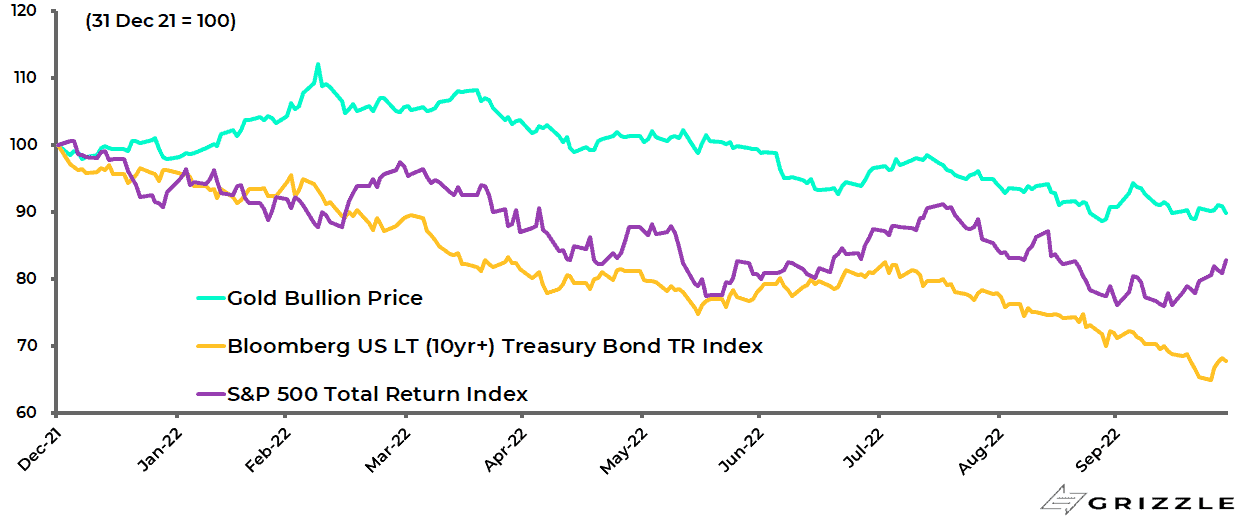

It is also the case that, despite Fed hawkishness, gold’s performance so far in 2022 has been much better than the S&P500 or long-term Treasury bonds, down 17% and 32% respectively.

Gold, S&P500 and Bloomberg US long-term (10Y+) Treasury bond index

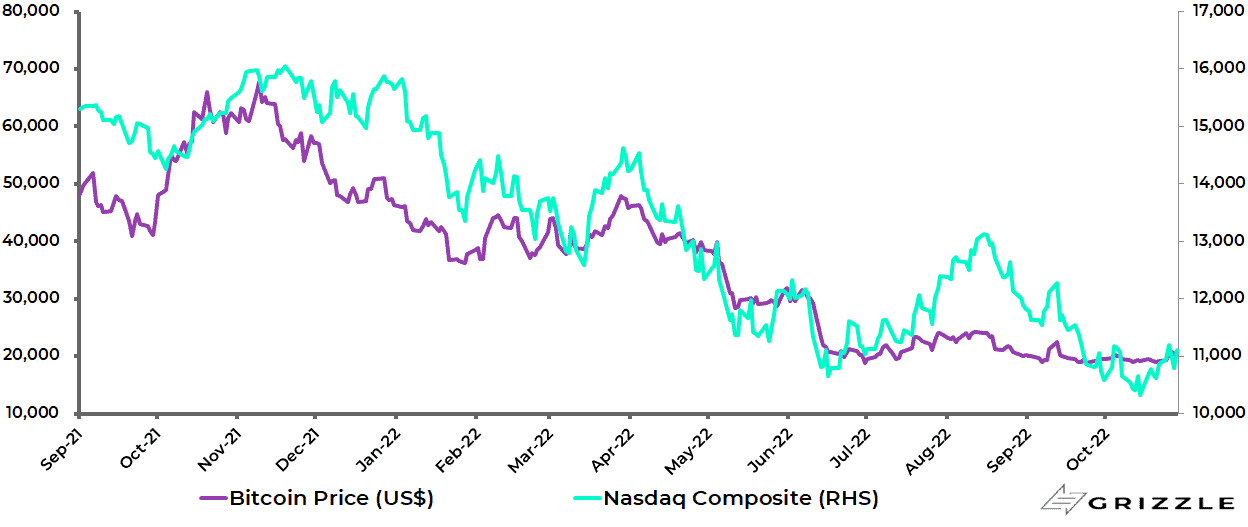

Bitcoin, on the other hand, has been extremely correlated to Nasdaq ever since markets started to worry about Fed tightening.

The correlation between Bitcoin price and the Nasdaq Composite has been 0.92 since September 2021.

Bitcoin price and Nasdaq Composite

When it Comes to Protecting Purchasing Power, Gold is Still Working

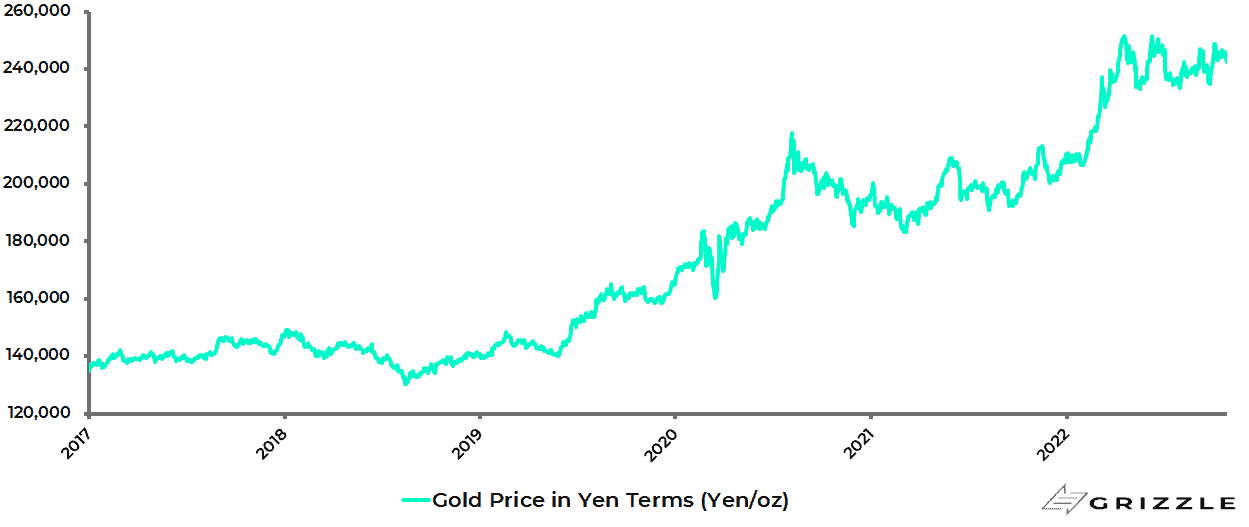

Meanwhile, for those people living in countries where central bank policy is actively undermining the currency, such as the Japanese, gold has performed its traditional role of preserving purchasing power.

The gold price in yen terms has risen by 15.2% year-to-date.

Gold price in yen terms

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.