Ride-hailing platform Lyft (NASDAQ:LYFT) reported results that overall beat analyst expectations and warned investors about a very uncertain future.

The stock is up about 16% in after-hours trading demonstrating investors are happy with a less than expected fall in customer revenue as the Coronavirus pandemic began.

Revenue came in at $955 million, 15% better than consensus of $830 million and only slightly below management guidance of $1.06 billion which management recently backed away from.

Revenue growth of 23% decelerated from last quarter’s growth of 52% demonstrating a maturing ride-hailing market even though Lyft is benefitting from less driver and rider discounts.

Riders on the platform hit 21.2 million, up only 3% from last year which is much slower growth than what the company put up last quarter.

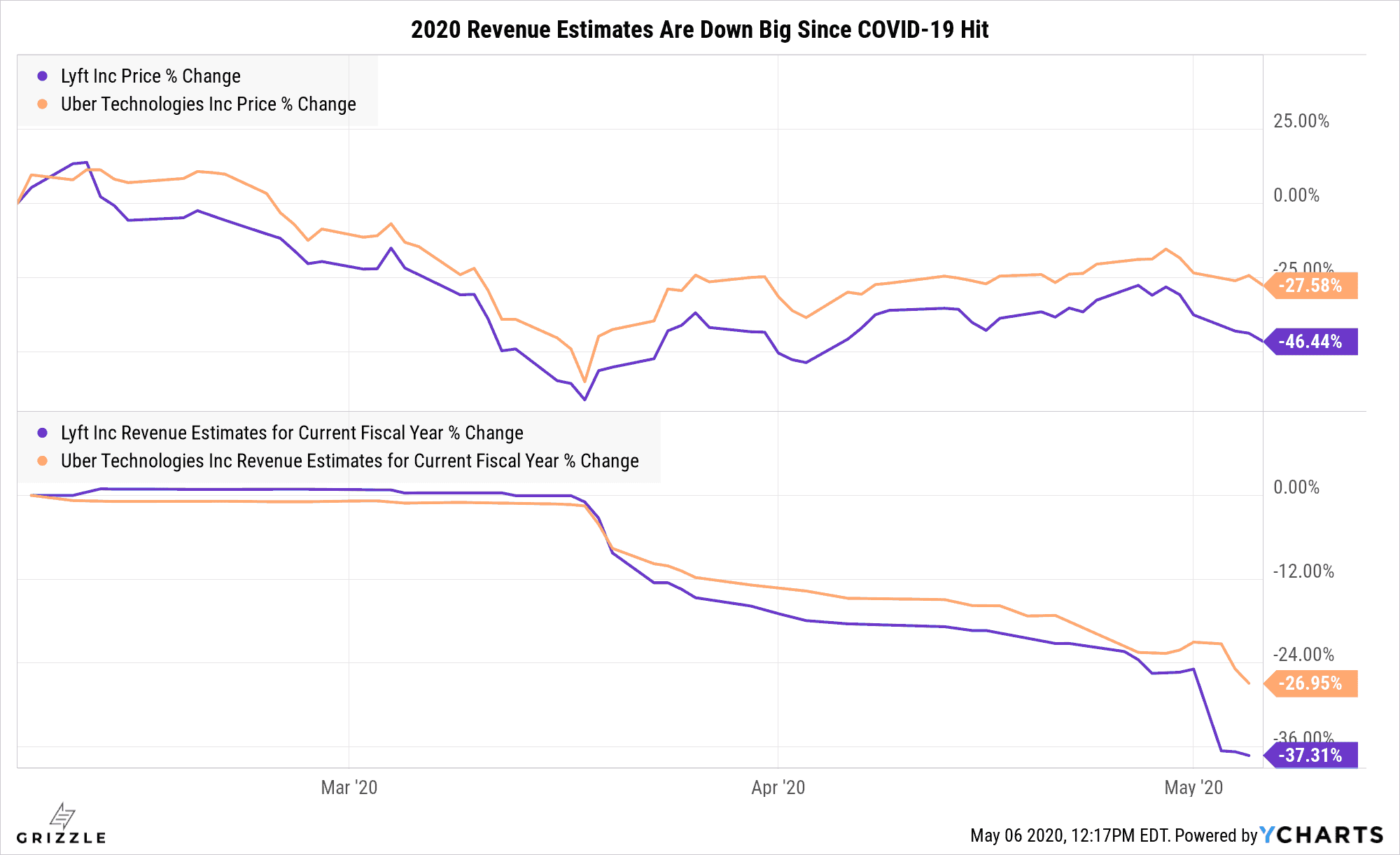

Lyft’s Price to Sales Multiple is Down, Uber’s is Not

Competition in the ride-hailing space is fierce, and we have no way of knowing how profitable or unprofitable Lyft can ultimately be.

Couple fierce competition with a world that may not go back to hailing a cab anytime soon and this is not the stock you should you buying in a Coronavirus world.

Years of Cash Left at Last Quarters Spending Rate

There is nothing to get excited about with Lyft and Uber at this point.

Yes they are growing relatively quickly for the car manufacturing business, but growth is nothing special for companies who bill themselves as tech stocks.

If they can turn the EBITDA losses into EBITDA gains, then valuations start to look more interesting.

Even Tesla at an eye-watering $780/sh doesn’t look so overvalued next to Uber and Lyft with their steep losses.

Ride-Hailing Compared to Car Manufacturing

| 2020 Estimates | Price/Sales | Revenue Growth | EBITDA Margin |

| Lyft | 2.8x | 29% | -15% |

| Uber | 3.6x | 39% | -15% |

| Tesla | 5.3x | 21% | 16% |

| Honda | .32x | 2% | 8% |

| Ford | .17x | -1% | 7% |

Uber vs Lyft Compared

Uber and Lyft currently look very similar.

Longer term the only big difference will be in the growth rates and profit margins.

Uber is making a bet that Eats and other businesses Lyft does not have will contribute to better growth AND margins.

Though both companies are guiding to a profit in 2021, these estimates are at risk.

Lyft in particular only has the ride-hailing business which is maturing, and though there is a slowing in discounting right now, price competition could pick back up again which would cause Lyft’s losses to balloon again.

Key Metrics (Uber vs Lyft)

| Uber | Lyft | |

| Rider Growth YoY | 26% | 28% |

| Quarterly Revenue YoY | 42% | 63% |

| Operating Margin YTD | -37% | -34% |

| 2020 Price/Sales Estimate | 3.6x | 2.8x |

Below is our view of where the buy and sell signals are for Lyft stock.

The stock isn’t worth more than $88 by 2030 in our current outlook and based on the output of our tool, the current stock price of $26 is still too expensive given the uncertainty around the Coronavirus.

Grizzle’s Guide to Trading Lyft

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.