Constellation Brands, Inc. (NYSE: STZ) reported its first quarter fiscal 2021 results ended in May pre market today that had mixed results. In spite of that, shares traded higher pre market .

The company generated $1.96B of revenue, below analyst estimate of $1.97B by 0.4%, and down by 6.4% year over year.

Earnings per share however exceeded street consensus of $2.04, by 19.7% at $2.44.

The company’s EBITDA at $735.7M also beat analyst estimate of $687.02M by 7.1%, and its EBITDA margin was higher than last fiscal year’s first quarter by 7.6%.

Valuation Overview

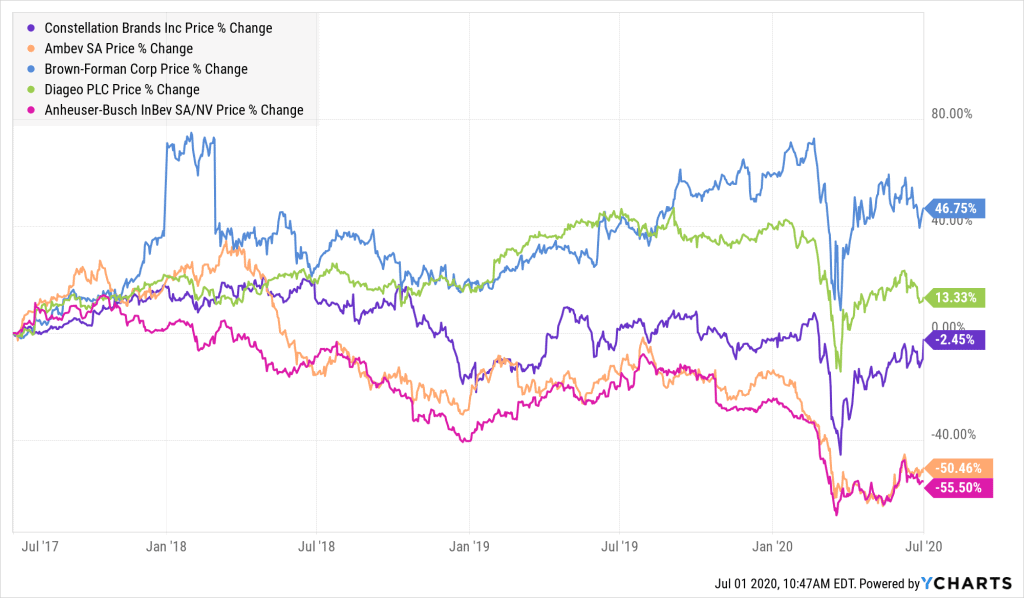

Even while being one of the largest beer import company in the US, based on the following chart Constellation Brands ranks third in terms of its share price gains.

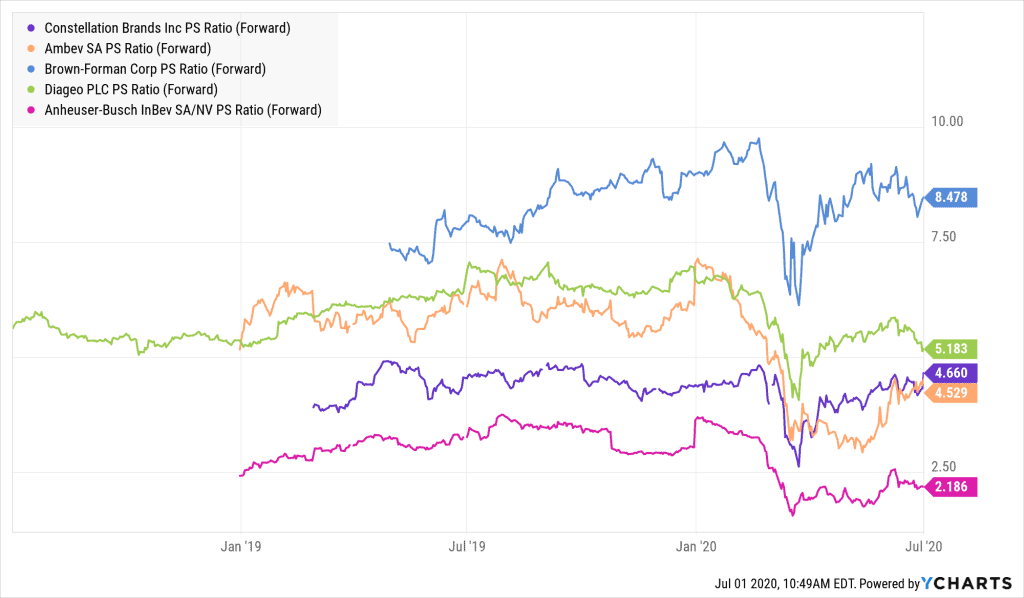

Therefore, naturally its PS multiple is amongst the third highest in the sector as well.

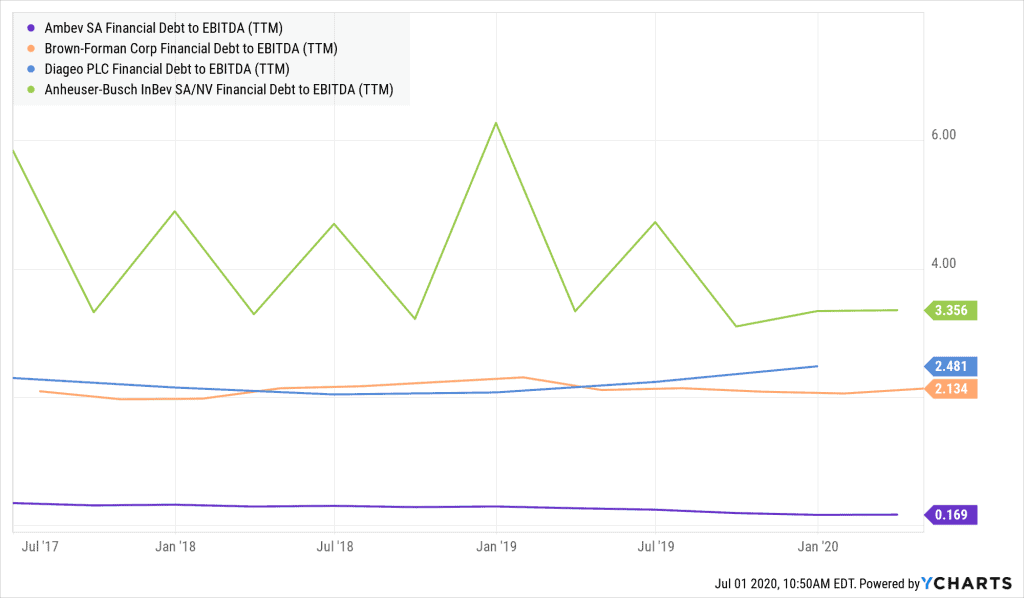

In our opinion this is largely due to the fact that Constellation Brands’ debt load has investors worried. According to today’s earnings, the company reported its debt in the current fiscal year to be at $12B, which is about 4 times its annual EBITDA.

As a result in comparison to its peers, the company is more levered.

However to their credit, the company has lowered its debt burden by 9% year over year, but the underlying issue of staying committed to its debt covenants is a risk worth considering.

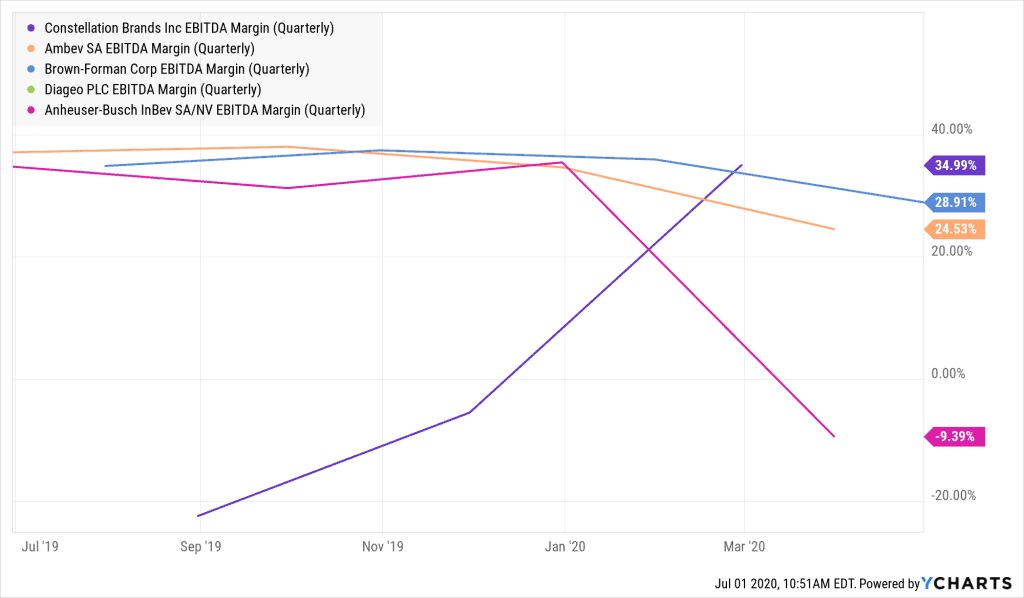

Despite of this, the company stands out amongst its peers when taking into account that its EBITDA margin is the highest as illustrated by the following chart.

According to its recent Q1 earnings, its updated margin is 37.5%. This suggests that its operational performance is very efficient regardless of its high debt.

Forward Outlook

Even though the company’s PS ratio is negatively impacted by its above industry average debt levels, we believe that their ability to generate a higher EBITDA margin proves that their share price deserves to be traded higher.

Additionally, the company was the first in its space to ever dip its toes into the cannabis sector when it partnered up with Canopy Growth back in 2018.

Although it is yet to reap the benefits of this collaboration, the company deserves credit for being the first to recognize the enormous prospects cannabis will offer in the near future.

So far through its proxy David Klein, who is the CEO of Canopy Growth, massive restructuring efforts were executed to better stream line its cannabis partner. This led to Constellation Brands up its stake in Cannopy to 38.6% on May of this year.

The current global pandemic has also certainly enhanced the credibility of this partnership when cannabis production and sale was deemed an “essential service”.

Due to these reasons, we believe that Constellation Brands deserves to trade higher in the near term.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.