The biggest risk to the pro-cyclical view has always been that the vaccines cease to be effective against the new variants, such as the Delta variant.

Concerns on this front have been growing again.

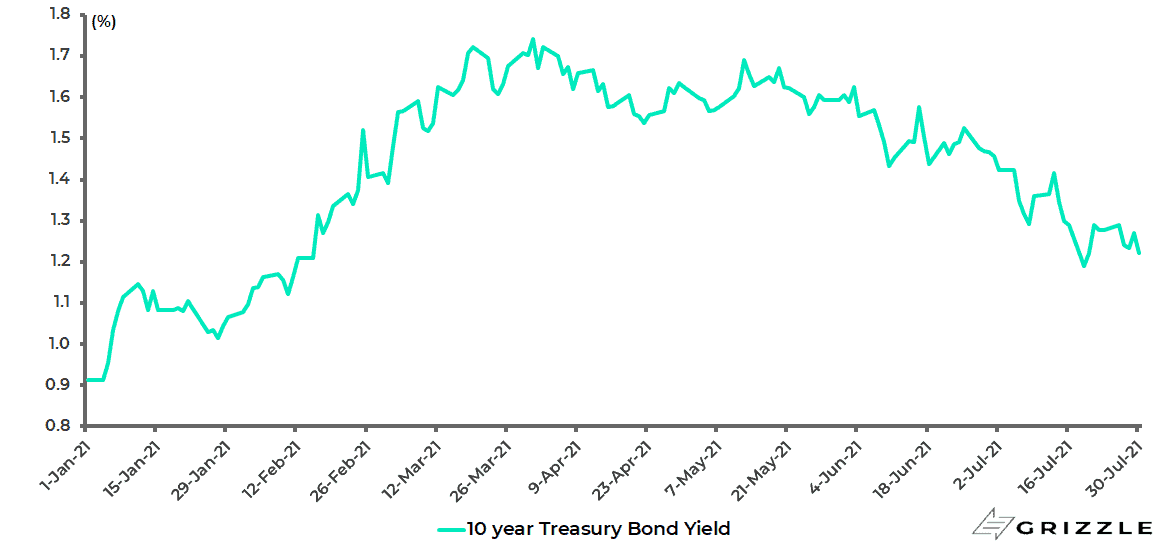

This is worth mentioning since it has to be wondered what has driven the dramatic US bond rally since the start of the new quarter with the 10-year Treasury bond yield down from 1.47% to a low of 1.13% on 20 July and 1.22% at the end of July.

US 10-year Treasury bond yield

Clearly, it is easy to blame it on algos and positioning, and the machines have clearly messed up the process of “price discovery” which is why many famous macro investors have retired from the game in recent years in terms of managing other people’s money.

Still it is worth keeping the Delta variant in mind in terms of news stories such as the one from Israel late last month (see Bloomberg article: “Pfizer Shot Halts Severe Illness, Allows Infection in Israel”, 23 July 2021).

The Israeli health ministry reported on 22 July that Pfizer’s vaccine protected only 39% of people from infection between 20 June and 17 July, down from 64% for the period between 6 June and early July and a previous 94% earlier this year before the Delta outbreak, though importantly it remains 88% effective at preventing hospitalisations and 91% against severe illness.

Since then the evidence of double vaccinated people getting Covid has grown though the encouraging point, for now, remains that the vast majority do not need to be hospitalised.

The other positive point is that mRNA technology is, seemingly, ideally suited for tweaking vaccines for new variants.

It is also the case that mutating viruses are meant to become more transmissible but progressively less violent which is what has so far been happening.

For now this writer will stick with the existing pro-cyclical view.

The last US employment payroll ldata was neither too hot nor too cold and therefore a sort of goldilocks.

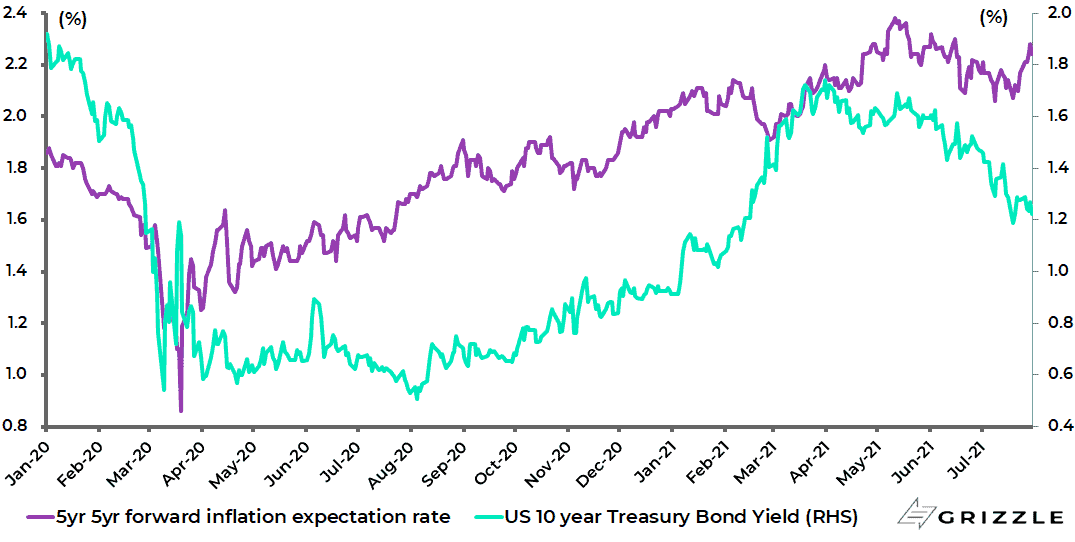

This, and the bond rally, leaves tapering concerns on hold. That said, it is worth noting that inflation expectations have not fallen nearly as much as bond yields which means rates have become more negative.

Indeed the US 5-year 5-year forward inflation expectation rate has risen from a recent low of 2.06% on 8 July to 2.24%, after declining from 2.30% in mid-June and a recent high of 2.38% in mid-May.

US 5-year 5-year forward inflation expectation rate and 10-year Treasury bond yield

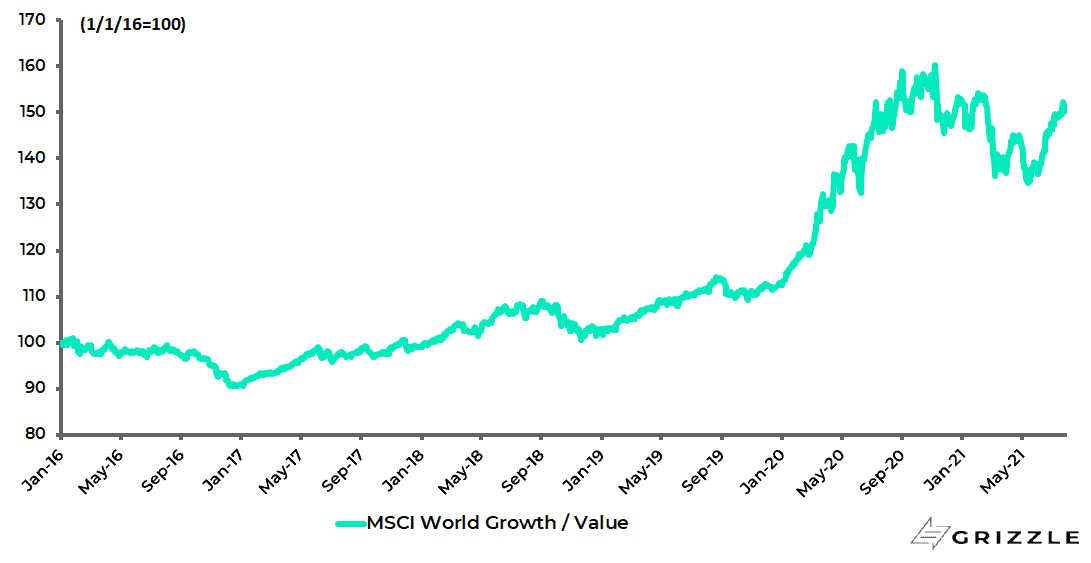

Meanwhile, the MSCI World Value Index has still outperformed the MSCI World Growth Index by 6.7% on a total-return basis since early November when Pfizer announced on 9 November that its vaccine was 90% effective.

MSCI World Growth Index relative to MSCI World Value Index

The Book on Inflation is Still Being Written

The key longer term question facing investors remains whether last quarter’s inflation scare was a transitory surge in price pressures driven by the unique circumstances of the pandemic, which is still the line maintained by the Federal Reserve and other G7 central banks; or whether it represents the beginning of a regime change to a more inflationary era.

The base case, as argued here over the past 15 months, has been that the policy response to the pandemic in the G7 world has set in motion dynamics that will lead to a change in investment regime; such as the growing merging of fiscal and monetary policy in the sense of G7 central banks indirectly funding more and more government spending as reflected in the expanding size of their balance sheets and the equally expanding size of G7 countries’ fiscal deficits.

Still the above trend is not set in stone since the assumption of regime change assumes a continuing unorthodox policy response and, most importantly, a continuing convergence of monetary and fiscal policy which at its most extreme in the case of America would involve the Federal Reserve severing the link between inflation and interest rates by fixing long-term bond yields via a policy of yield curve control.

It should be noted, again, that the Bank of Japan has been practicing yield curve control since 2016 while in the Eurozone the ECB seems to be moving ever closer to targeting nominal bond yields in what remains best described as a policy of closet yield curve control.

The ECB has also recently announced the results of its strategic review.

It has, in effect, implemented an average inflation targeting regime similar to the Fed’s where inflation is allowed to overshoot to make up for previous shortfalls.

Meanwhile, any policy of financial repression in America would confirm that the authorities are determined to inflate their way out by suppressing nominal interest rates and therefore real interest rates.

This would be a big deal in the case of America since the US dollar is the world’s reserve currency and, clearly, such a decision would not be taken lightly by the Federal Reserve.

Still the motive for fixing interest rates further up the yield curve is clear since the reality is that the G7 world cannot afford higher interest rates because of the increase in the nominal debt servicing burden that would represent.

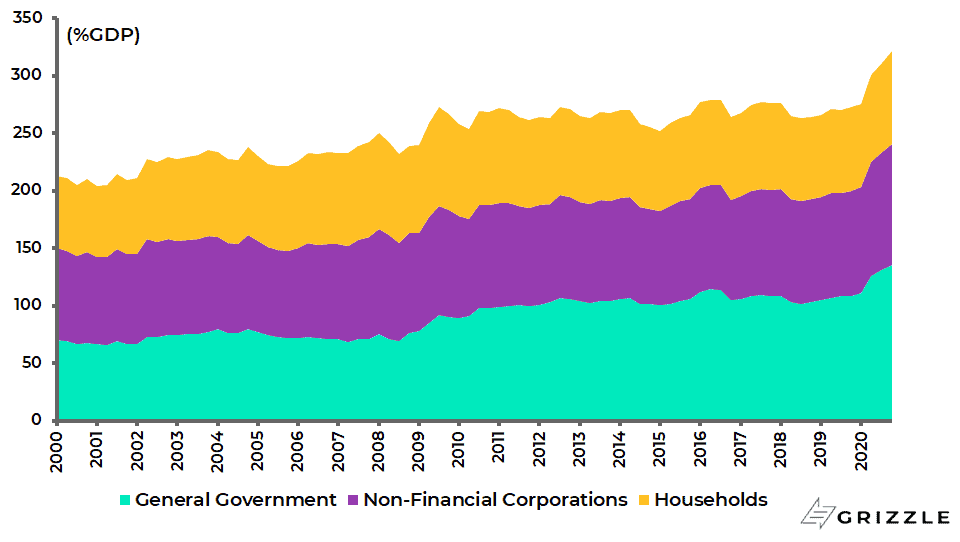

Thus, aggregate debt levels have increased massively since the global financial crisis of 2008 because public sector debt has been added on top of private sector debt as demonstrated by the latest BIS data.

Advanced economies’ (developed countries) aggregate non-financial sector debt as a percentage of GDP has risen by 89.3ppts from 232% in 3Q08 to 321.3% at the end of 2020, with general government debt to GDP rising by 66.5ppts from 69.4% to 135.9% over the same period.

Advanced economies’ aggregate non-financial sector debt to GDP

Debt Cycle May be Nearing a Peak

The above data suggests to this writer that the world is at the peak of a multi-decade long debt cycle, a debt cycle which received a massive catalyst 50 years ago this month when former US President Richard Nixon broke the last link of the US dollar with gold in August 1971.

This is at a time when the G7 world has become ever more interventionist in terms of the stated willingness of governments to spend money combatting perceived evils such as “global warming” and “inequality”.

In such a context, the political appetite for monetary and fiscal orthodoxy is minimal.

If this is the political reality, it is not one as yet admitted to by the relevant authorities including the Federal Reserve.

On this point, if monetary policy does turn surprisingly orthodox in the US in coming quarters, in terms of reining in central bank balance sheet expansion via so-called ‘tapering’ and resuming interest rate hikes sooner than expected, then the deflationary trend can definitely reassert itself even if the recovery out of the pandemic has occurred.

This is precisely because of the undoubtedly negative impact on growth resulting from the ever higher debt levels.

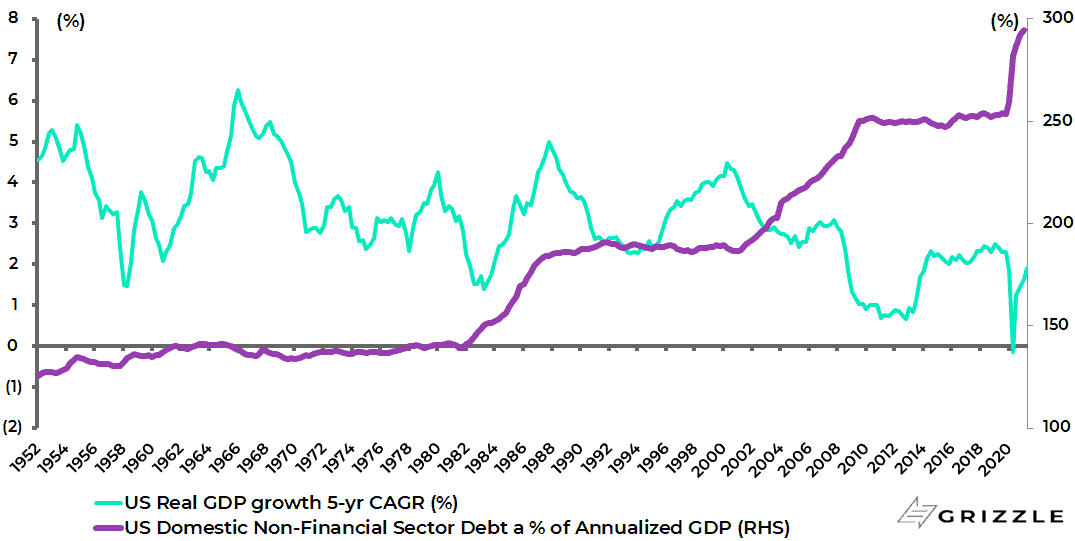

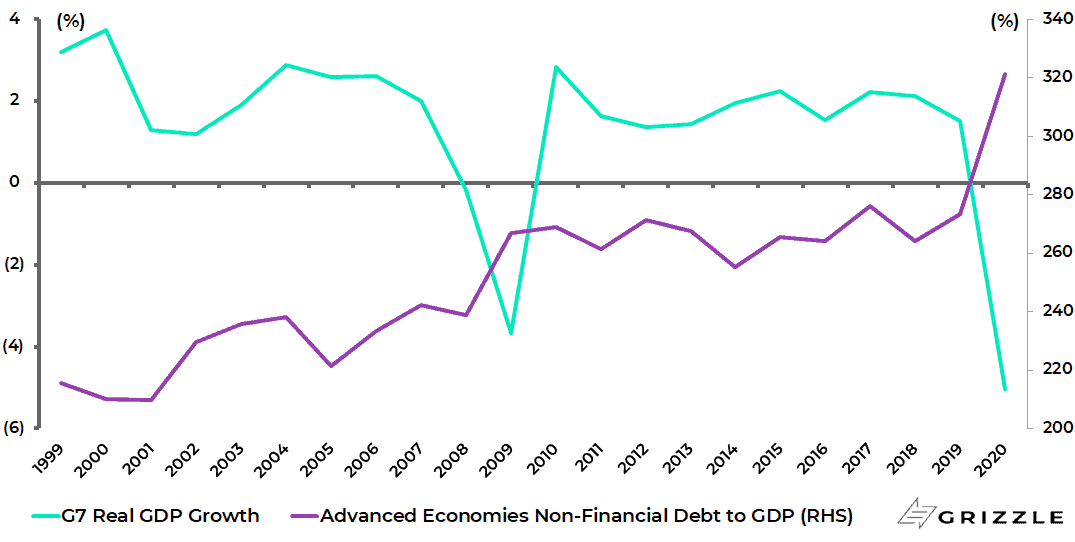

That this debt burden marks a growing constraint on growth is reflected in the reality that higher levels of debt have been leading in recent years, if not decades, to lower levels of real GDP growth in the G7 world.

This is clear from the American example as well as from the G7 example.

US real GDP 5-year annualised growth and non-financial sector debt as % of GDP

G7 real GDP growth and advanced economies’ non-financial sector debt to GDP

Inflation Will be Transitory if Banks Don’t Start Lending

The above is why it remains critical to this writer to keep a close eye on the credit multiplier, or the lack of one, in America.

And here it must be stated that the data, for now at least, does not confirm the change-of-investment-regime thesis, otherwise known as the-return-of-inflation story.

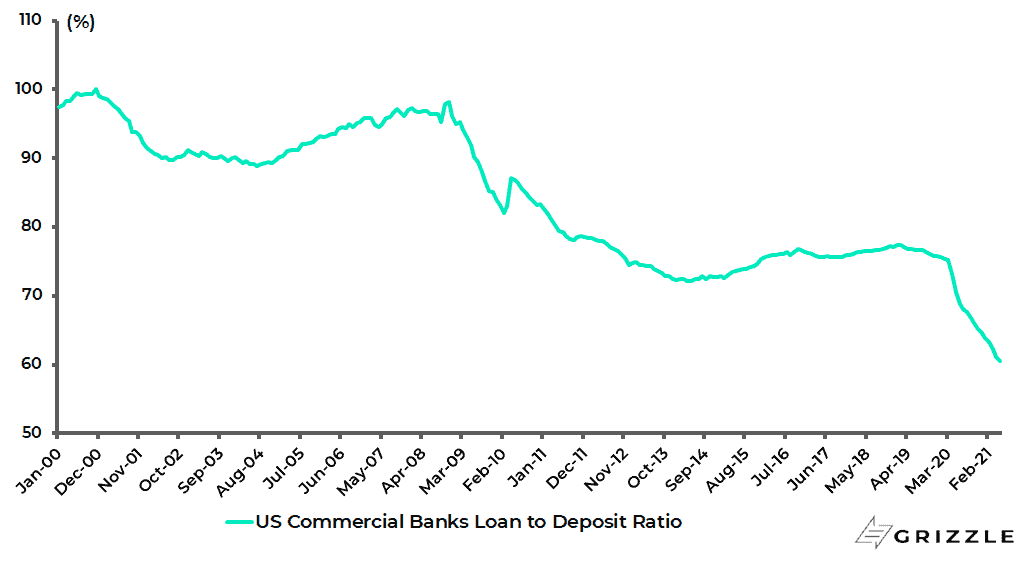

Thus, the loan-to-deposit ratio of the four major US banks fell to 51% in 1Q21 as deposits surged by 15.4% YoY driven by Covid-related transfer payments to households but loans did not.

True, much of the American economy was still locked down in that quarter. Still the loan-to-deposit ratio of the whole US banking system has continued to decline since then to a record low of 60.6% in June despite the re-opening with aggregate loan growth running at a negative 3.1% YoY in June, though up from -4.2% YoY in May.

US commercial banks’ loan-to-deposit ratio

Source: Federal Reserve

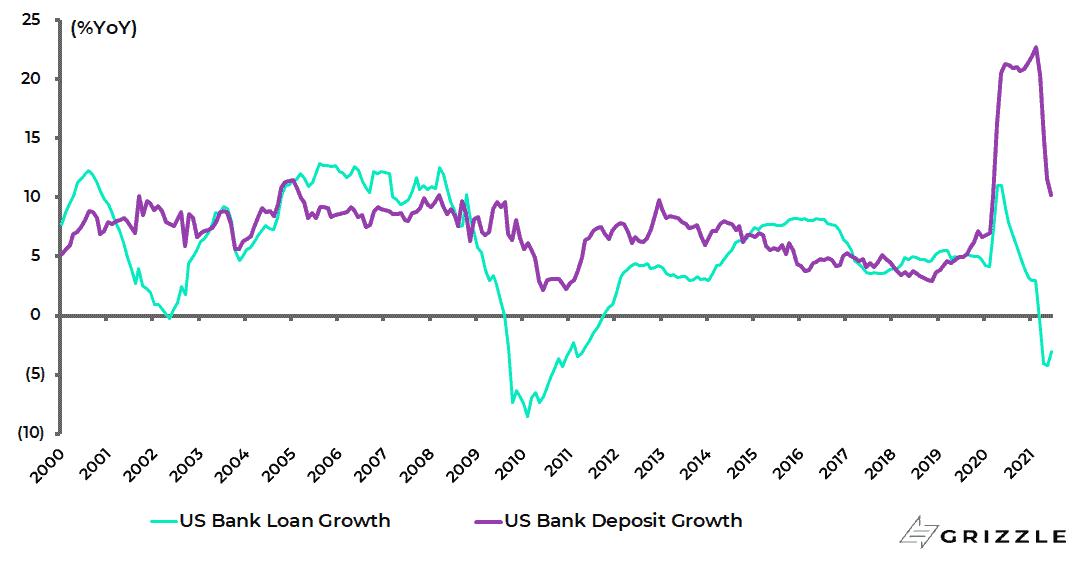

This is despite the fact that Fed surveys show that banks are increasingly willing to lend.

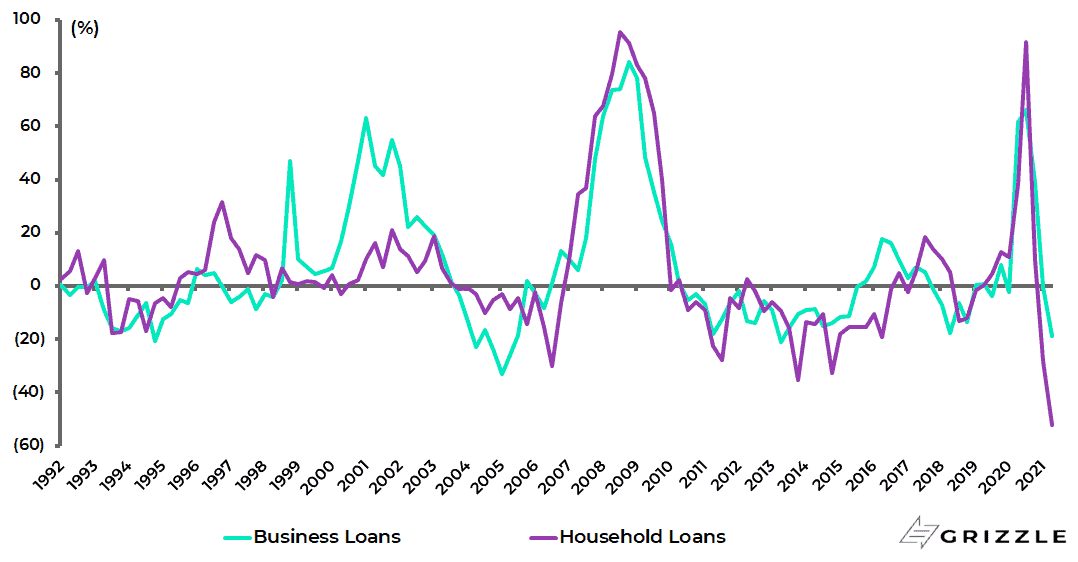

US bank loan growth and bank deposit growth

The Fed’s latest quarterly Senior Loan Officer Survey in April showed that a net 18.9% of US banks reported easing lending standards on business loans and a net 52.4% reported easing lending standards on household loans.

By contrast, a net 66% of banks tightened standards on business loans and 91.9% on household loans in July 2020.

US net percentage of domestic banks tightening lending standards

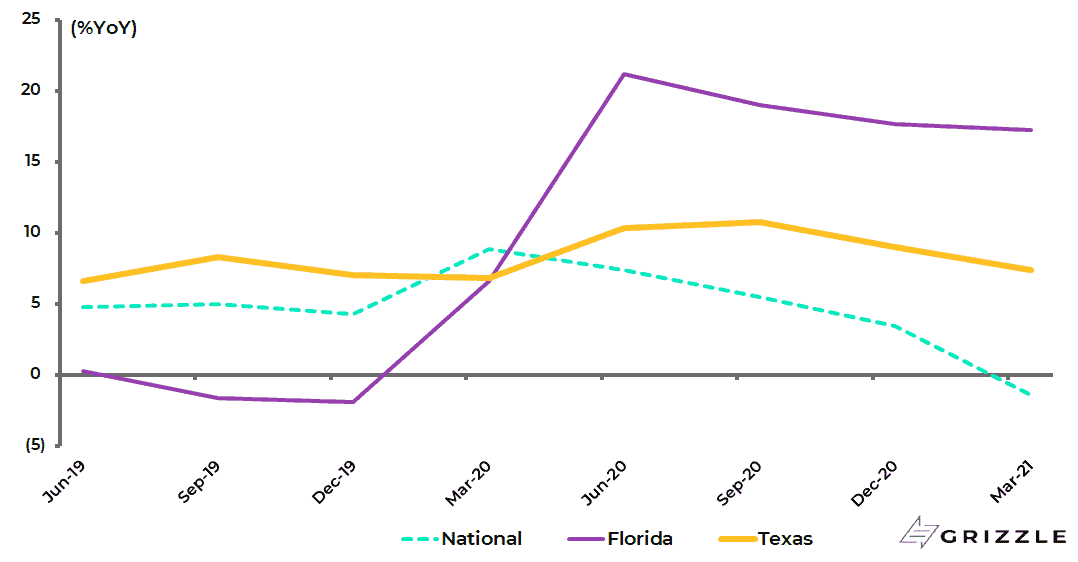

Still trends look much more promising in Republican governed states which re-opened first such as Florida and Texas.

Bank loans in Florida and Texas, for example, rose by 17.3% YoY and 7.4% YoY respectively in 1Q21, based on data from the Federal Deposit Insurance Corporation, compared with a 1.5% YoY decline nationally.

US bank loan growth in Texas and Florida

The Government is Starting to Take a Stronger Role in Where The Lending Goes

If the above is the current state of play on bank lending in America, it should be stressed again that a new form of political and fiscal activism is now in evidence, a trend where the pandemic has acted as the catalyst, with the election of the Biden administration in America committed to the most ‘’progressive’’ agenda in decades.

This is why, if bank loan growth continues to disappoint, the political pressure will likely grow for banks to be made to lend to politically desirable areas.

This could take the form of a continuation of, or expansion of, various forms of loan guarantees.

There is also the potential for a relaxation in post-2008 capital ratio restraints, most particularly again if lending is to politically correct areas such as “green” projects.

If this is the overriding political context in the Western world it is a resulting political reality that the central banks will be expected to finance such spending if tax revenues are not forthcoming.

So if markets remain, understandably in the short term, focused on central bankers’ every word and action, the game is without a doubt changing.

This is because G7 central bankers are in the process of becoming less important in the sense that when the pressure is on, they will likely be forced to accommodate financially the need for more government spending.

In this respect, there are many advocates of Modern Monetary Theory on the progressive wing of the Democrat Party in America.

If tax hikes cannot be passed through Congress to pay for spending programmes because of Republican resistance, the pressure will mount on the Fed to fund them.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.