https://www.youtube.com/watch?v=7hvYgUktGOk

Beloved New York City Burger Chain Shake Shack (NYSE: SHAK) reported results that largely met numbers from the earnings preview a few weeks ago.

The stock is flat in after-hours trading Monday as the market digests management’s guidance about the future.

Revenue of $143 million was in-line with guidance from 3 weeks ago of $143 million and missed analyst estimates for revenue of $145 million by 1%.

The earnings of -$0.03/sh were below analyst estimates for a loss of -$0.01/sh.

[su_panel]Shake Shack is burning $1.4 million a week and has 6 months of cash left if they keep paying all their leases or more than a year if they stop paying rent. With the multiple unchanged since the pandemic, you are betting the virus will only last another 6-9 months if you buy the stock above $52/sh. We recommend waiting for confirmation that life will go back to normal before diving into this stock. [/su_panel]

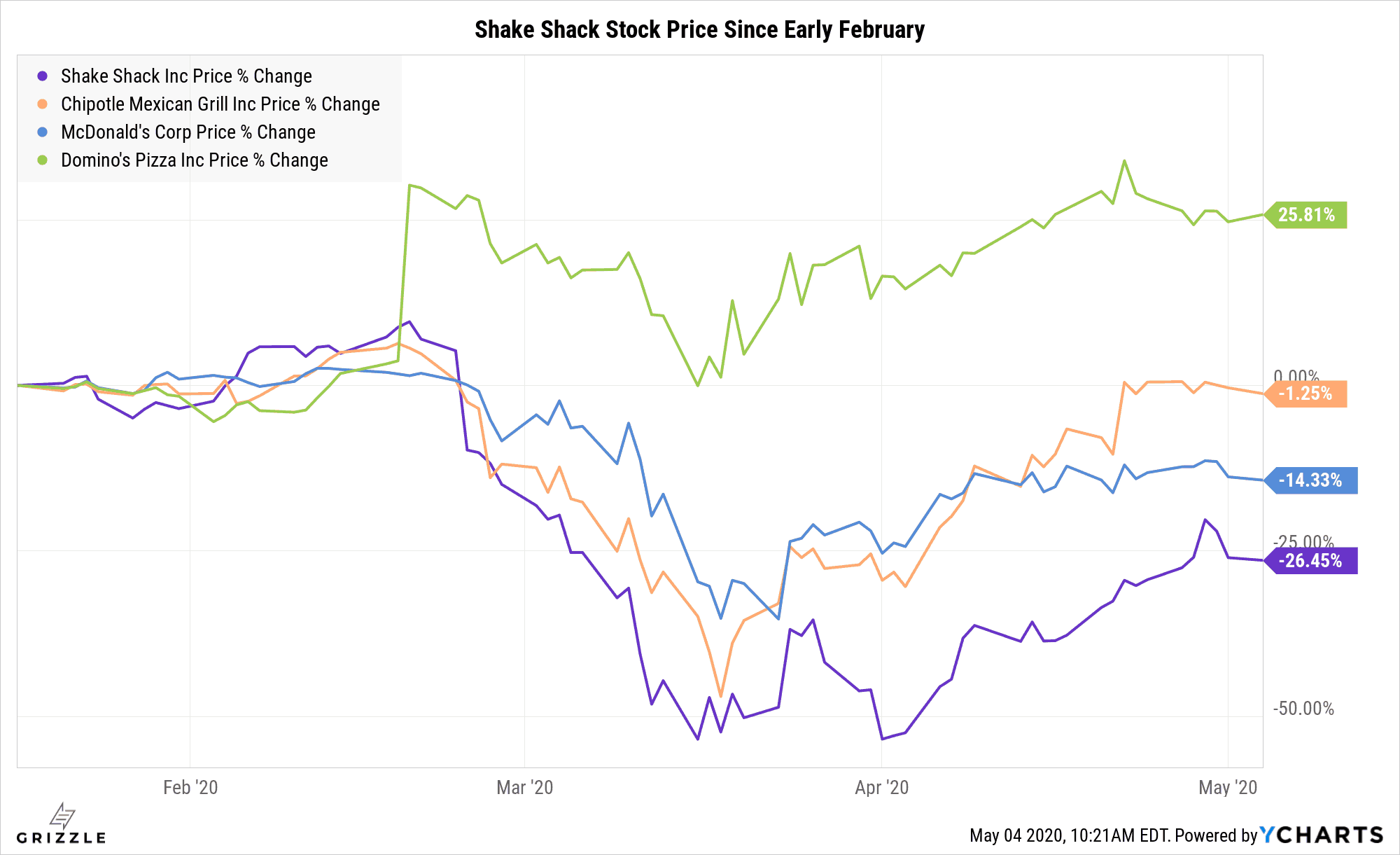

SHAK Stock Price Underperforming Other Fast Food Peers

Analysts are expecting a significant fall in revenues for Shake Shack both this year and next.

The fall in revenue is driven by two factors, store openings and same-store sales.

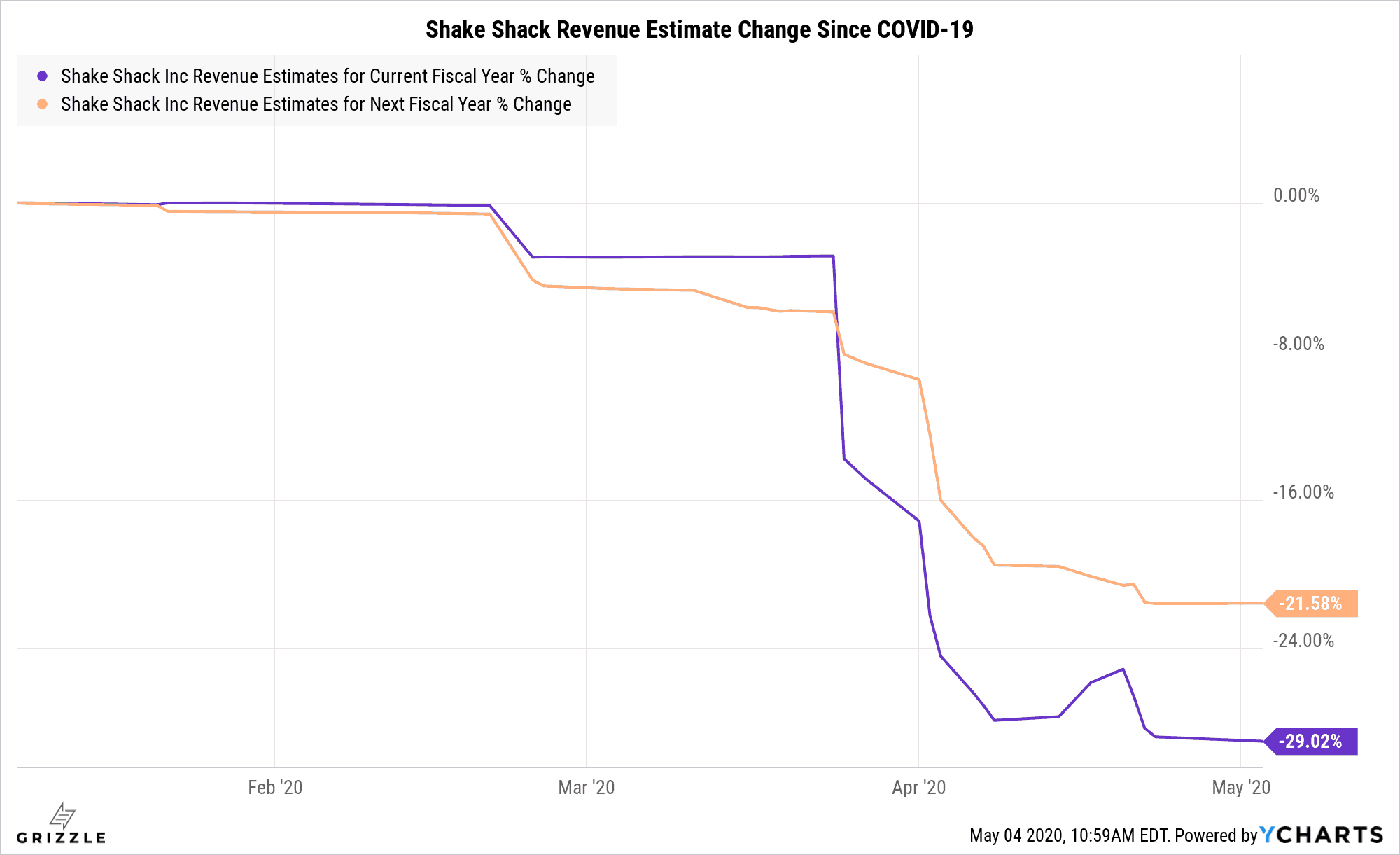

Revenue Estimates Down 20%-30% Since COVID-19 Hit

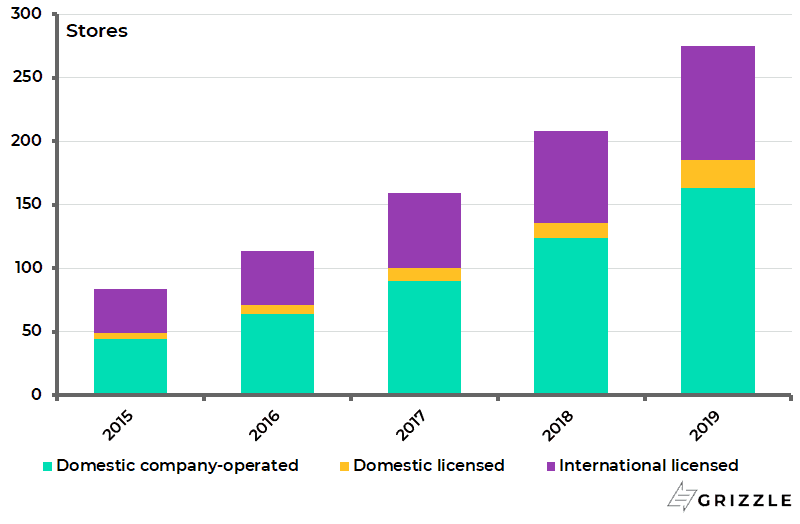

The company had planned to open 64 new stores in 2020 which would have been a growth rate of 23%.

SHAK Store Growth (Licensed vs Owned)

Now they are guiding to putting all of these construction projects on hold, so cut out that source of revenue growth.

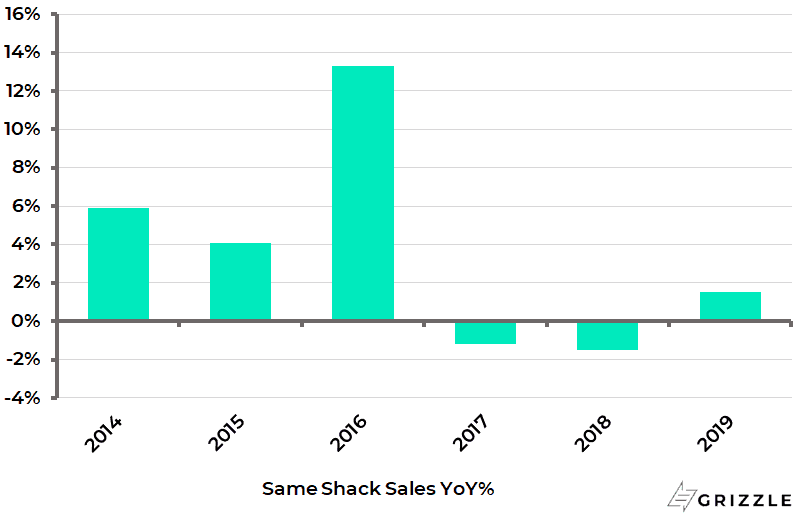

Next, we need to look at sales from existing stores which have been flat to down over the last few years as the U.S. market becomes more saturated with Shake Shacks and competition increases.

So Shake Shack is already struggling with growth at company-owned stores, but add on the pandemic and management warned investors in April that sales were down 12.8% in the first quarter and 26% in March.

[su_panel]Analysts are basically assuming the sales decline in March will continue over the entire year. As long as the virus continues to disrupt daily routines, these estimates aren’t overly conservative in our view. [/su_panel]Same-Store Sales Growth by Year

SHAK Now Back to Pre-COVID Multiple

Back in the middle of February, the market thought Shake Shack would generate $720 million of revenue this year.

Fast forward to today and estimates are now for $523 million of revenue, down 30%.

So while the stock price is down 25% this year, the multiple is right back to where it was before the pandemic.

The stock price has merely adjusted down with the decrease in expected sales.

This means if the market becomes more conservative for any number of reasons, Shake Shack’s stock price could take a hit even if revenue estimates stay right where they are.

| $MM | |

| Sales Pre-COVID | 720 |

| Sales Post-COVID | 523 |

| Mkt Cap Pre-COVID | 2,764 |

| Mkt Cap Post-COVID | 1,943 |

| Price to Sales (Pre) | 3.8x |

| Price to Sales (Post) | 3.7x |

| % Change in Price/Sales Multiple | -3% |

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.