Starbucks (NASDAQ: SBUX) announced their third quarter fiscal 2020 earnings results, beating top line analyst estimates, and posting better than expected Chinese sales performance.

This caused shares to trade higher aftermarket.

The company generated $4.2B of revenue, above street consensus by 2%, but -38% lower year-over-year.

Non-GAAP earnings per share however came in at ($0.46)/sh, 19% below analyst expectations of $-0.57.

Starbuck’s EBITDA for the reported quarter was ($330.5)M, which was 8% higher than analyst targets.

Additionally due to its important stake in the Chinese coffee market, investors are pleased to know that Chinese comparable store sales growth for the reported quarter was (19%), which was higher than management’s expectations of between (25%) to (35%).

In line with this growth, Chinese domestic revenue for the quarter was up by 63% quarter-over-quarter at $624.4M.

The better than expected performance in China, led management to revise their previously expected Chinese comparable store sales growth of (10%) to flat, be raised to (5%) to flat.

New Paradigm

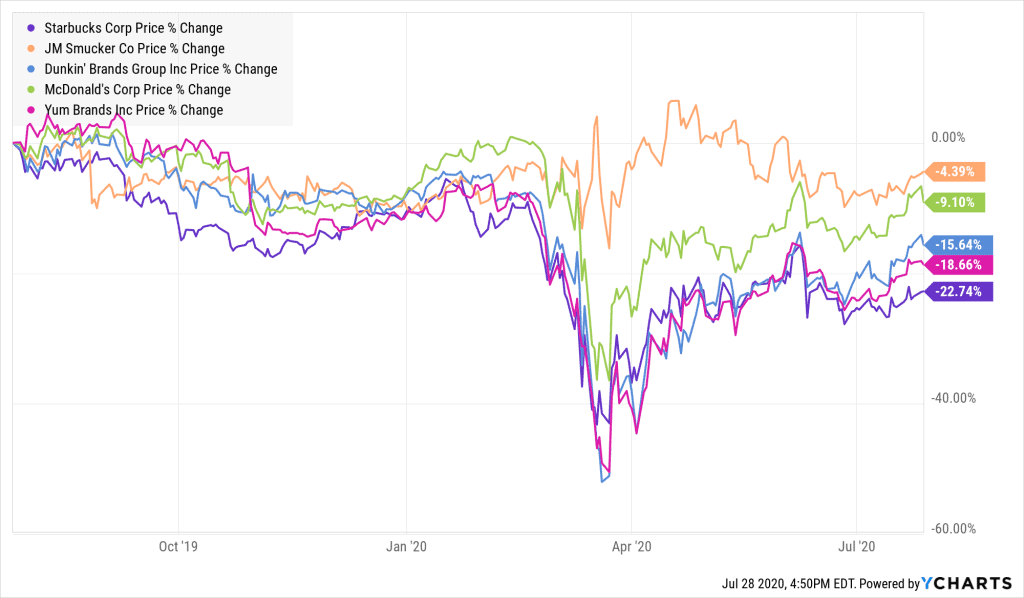

Regardless of its global outreach, Starbucks’ share performance has been dismal compared to its competitors.

As shown, compared to J.M. Smucker Co. Starbuck’s share price has performed poorly. The cause of this is most likely credited to the rise in demand for home-made coffee beverages.

The pandemic caused lockdown has led many coffee drinkers resort to home-made coffee beverages than ever before.

Even as the lockdown has now begun to ease in many areas, people have grown accustomed to either making coffee at the safety of their homes or getting delivered to their doorstep.

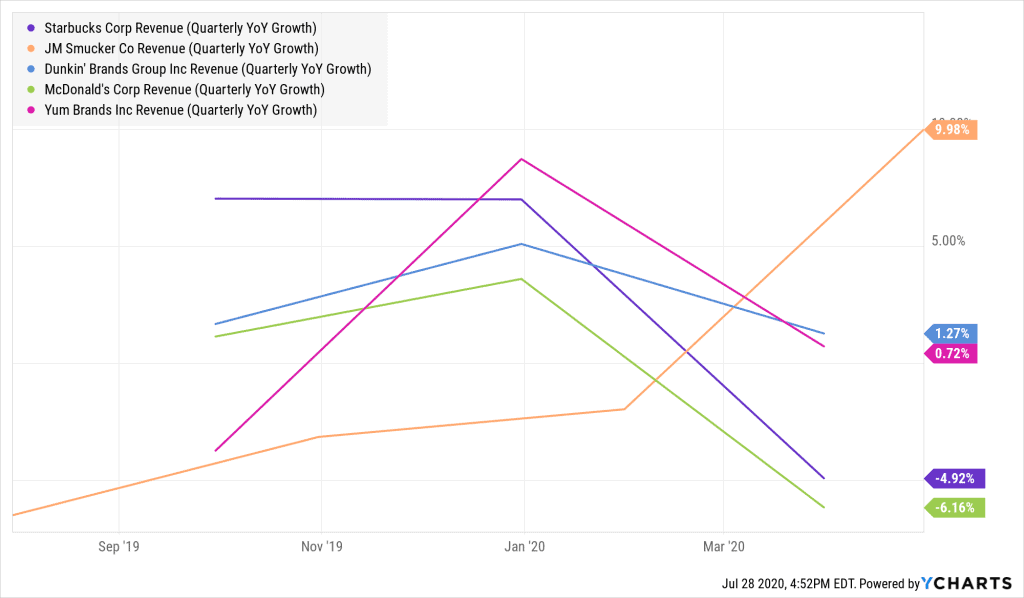

This trend has allowed J.M. Smucker Co.’s revenues to rise lately thanks to their popular Folgers Coffee products.

Their partnership with Dunkin’ Brands Group in selling Dunkin’ branded premium bagged coffee has also contributed greatly to their sales as well.

This is in stark contrast to the yearly revenue growth of Starbucks as illustrated below.

Although Starbucks also sells home-made coffee products, their scalability is not as great as Folgers coffee which is sold in almost every grocery chain.

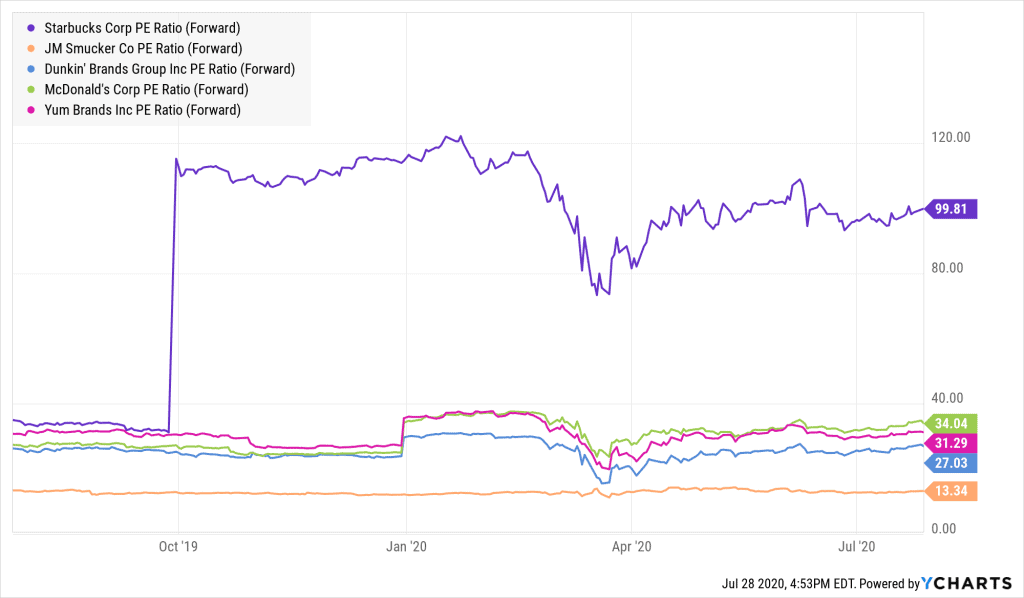

Yet the company’s shares are trading at a much higher price to earnings multiple than its competitors.

However, even though revenues for the quarter have recovered well particularly in China, Starbuck’s high PE multiple indicates that the shares are not cheap, especially given the fact that the pandemic has increased demand for at-home coffee products.

We still like Starbucks stock longer term as we expect growth will reaccelerate after the Coronavirus is a distant memory.

It cannot be overstated how big a deal the implosion of Luckin Coffee was to Starbuck’s fortunes.

Starbucks once again has the Chinese market to themselves and growth will benefit.

Yes the stock is expensive, but it’s for a reason. We are buyers

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.