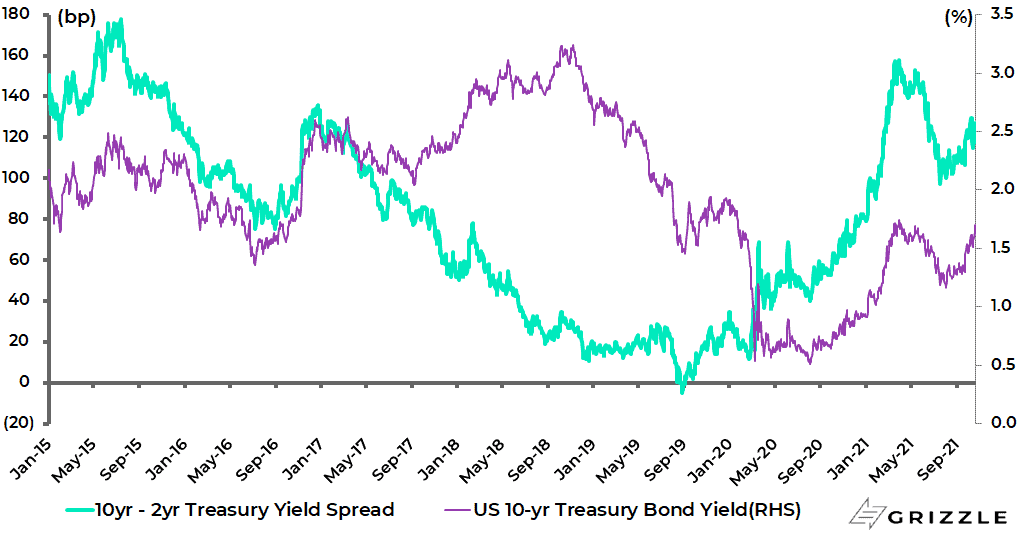

It is both interesting and logical that the Federal Reserve signal late last month that it will end the tapering earlier than expected has triggered a steepening in the yield curve.

The 10-year Treasury bond yield has risen by 33bp since 22 September to 1.63%, while the spread between the 10-year and 2-year Treasury bond yields is up 11bp to 118bp over the same period.

US 10-year Treasury bond yield and spread over 2-year Treasury yield

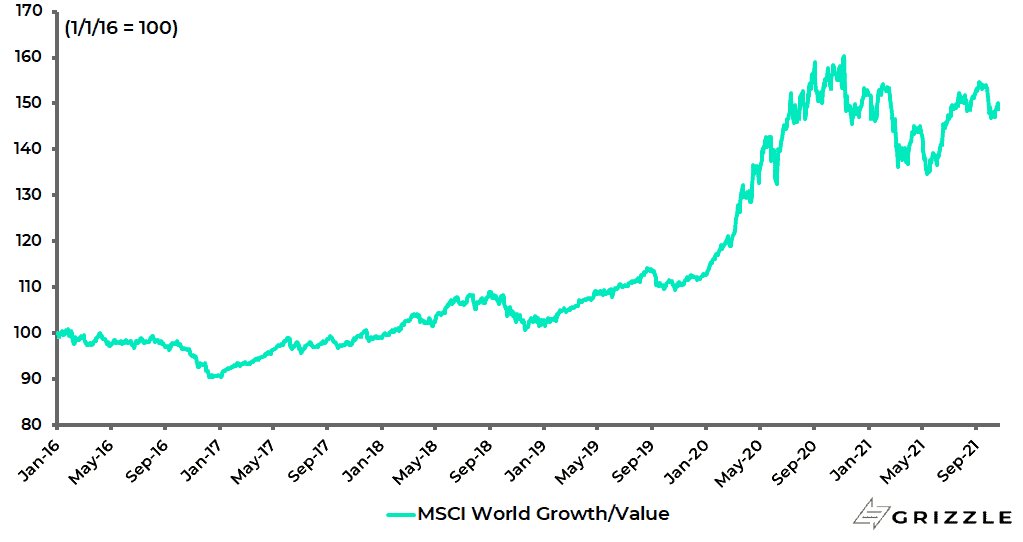

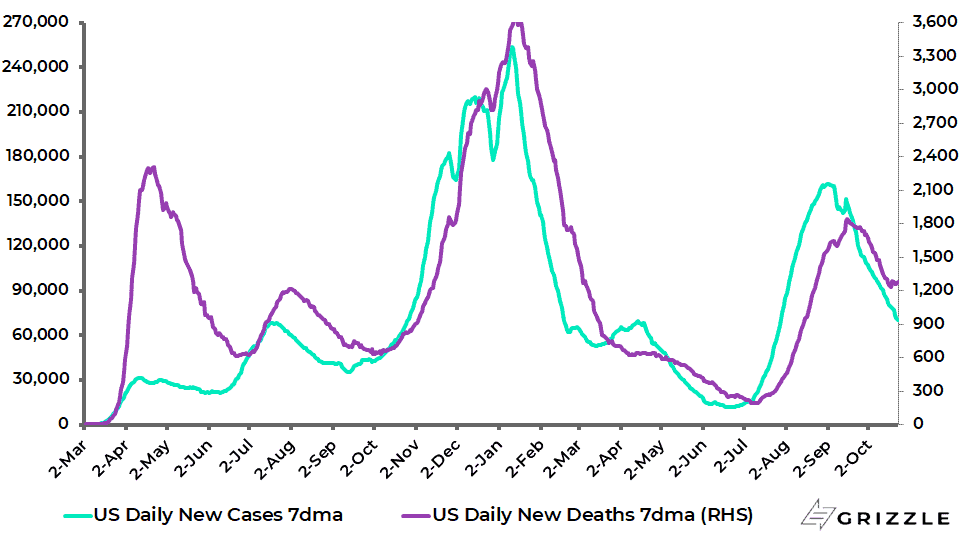

This in turn has continued to reactivate the cyclical trade in terms of a renewed outperformance of value over growth, with that move also helped by a further decline in US Covid cases.

The MSCI World Value Index has outperformed the MSCI World Growth Index by 3.6% since 21 September, while the 7-day average daily new Covid case count in America has declined by 57% from a recent high of 161,733 in early September to 70,153.

MSCI World Growth Index relative to Value Index

US 7-day average daily new Covid cases and deaths

Still, if cyclicals are outperforming again, the continuing move in energy prices poses a clear threat to growth because of the impact on consumers’ real incomes.

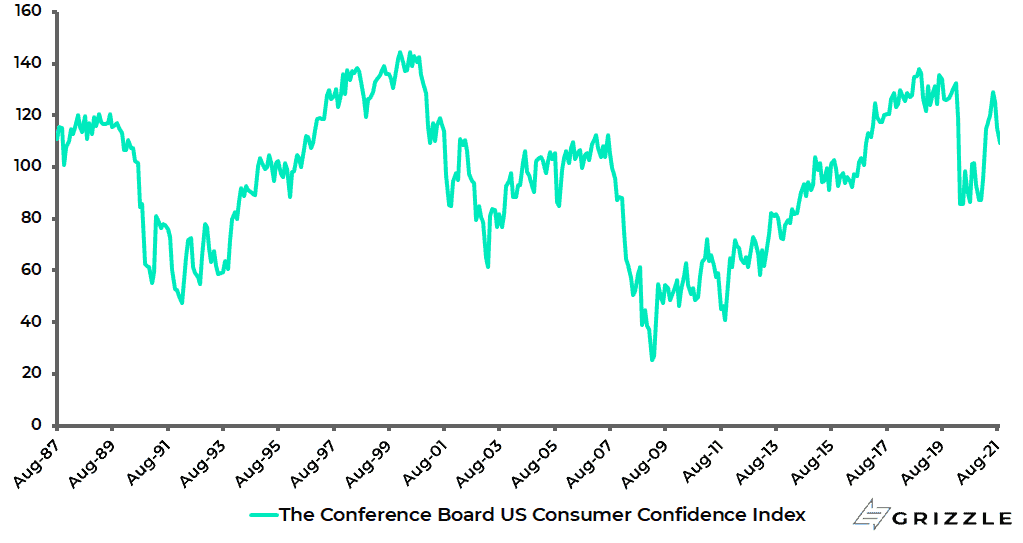

Interestingly, the latest US consumer confidence index shows continuing weakness.

The Conference Board’s US consumer confidence index fell from 115.2 in August and a recent high of 128.9 in June to 109.3 in September, the lowest level since February.

The Conference Board US consumer confidence index

The Chances of Stagflation are Not Zero

Here the risk remains of a stagflation scare of a type not seen since the 1980s.

Governments will be eager to try to shield consumers from the worst impact.

Italy is a recent example as a result of soaring natural gas prices. Italian Prime Minister Mario Draghi announced on 23 September a €3bn package to offset the increase in energy prices.

The plan is to freeze gas and electricity bills for up to 3m households while cutting the VAT on energy and waiving other related fixed charges for this quarter.

Draghi also warned that, without government intervention, gas prices would rise by another 30% and electricity bills by as much as 40% in the current quarter.

There is also growing focus on how the surge in gas prices in Europe is forcing a shift to oil-driven energy.

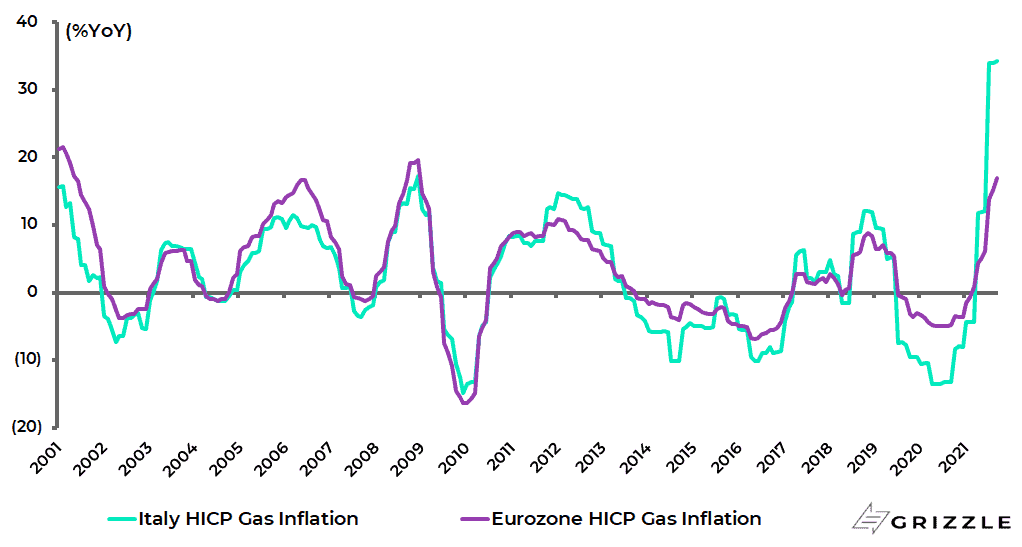

Italy’s consumer price inflation for gas rose to a record 34.2% YoY in September, compared with 16.9% YoY for the Eurozone.

Italy and Eurozone HICP Gas Inflation

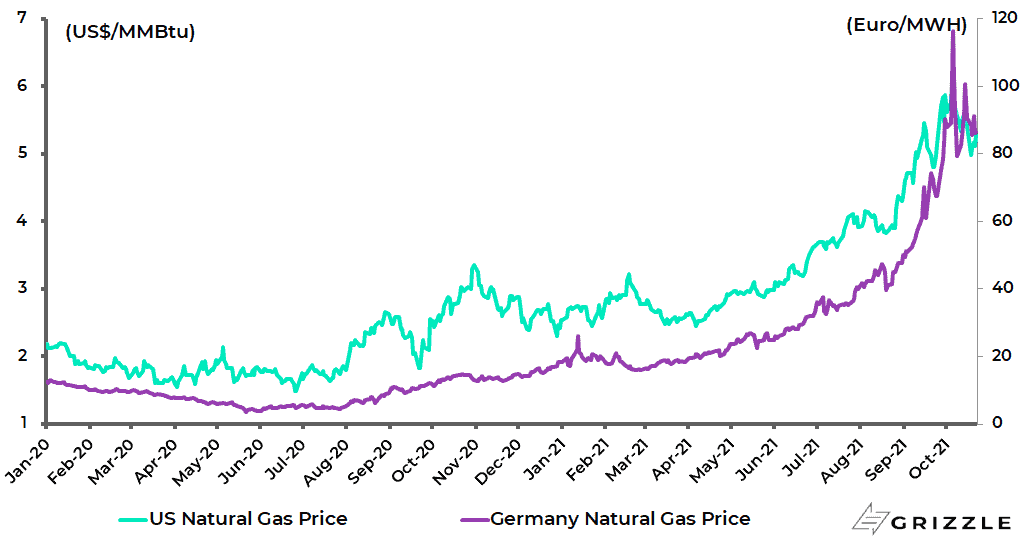

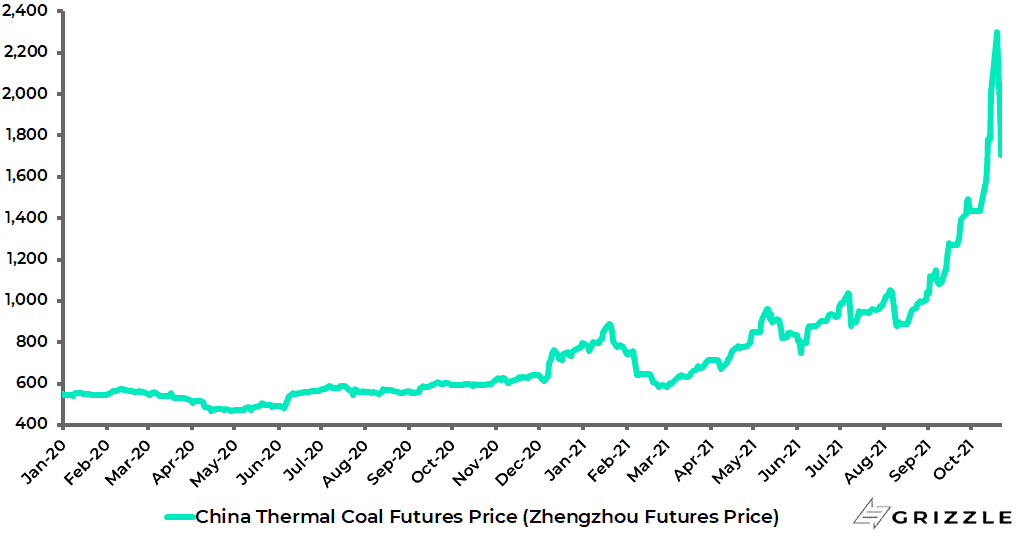

Meanwhile, natural gas price and coal prices have continued to rise.

Natural gas prices in America and Germany have now risen by 108% and 357% year to date, while the China thermal coal price is up 115%.

US and Germany natural gas prices

China thermal coal price

The Energy Transition is to Blame for High Energy Prices

Clearly there will be all kinds of focus on the “special circumstances” triggering these price moves.

But in the “big picture” what the world is looking at is the collateral damage to economic growth, and households’ real incomes, caused by the politically driven energy transition.

The same applies in China where government measures to reduce energy consumption are having a dampening impact on growth at the same time as the Chinese economy is facing the deleveraging spillover risk from the fallout from Evergrande.

Power shortages in China have in recent weeks spread to 20 provinces as they race to meet emission targets before the Winter Olympics in February.

The main causes for the power shortages are shortages of coal amidst the government’s efforts to curb energy consumption and so reduce carbon emissions.

China Property Lending is Opening Back Up

Fortunately, Chinese policymakers can ease up if they want to, and they have begun to do so as regards both property and the attack on emission.

On the property sector, banks will be allowed to lend more to the sector.

In this respect, the banks remain below the sectoral limits set for property lending by the regulators.

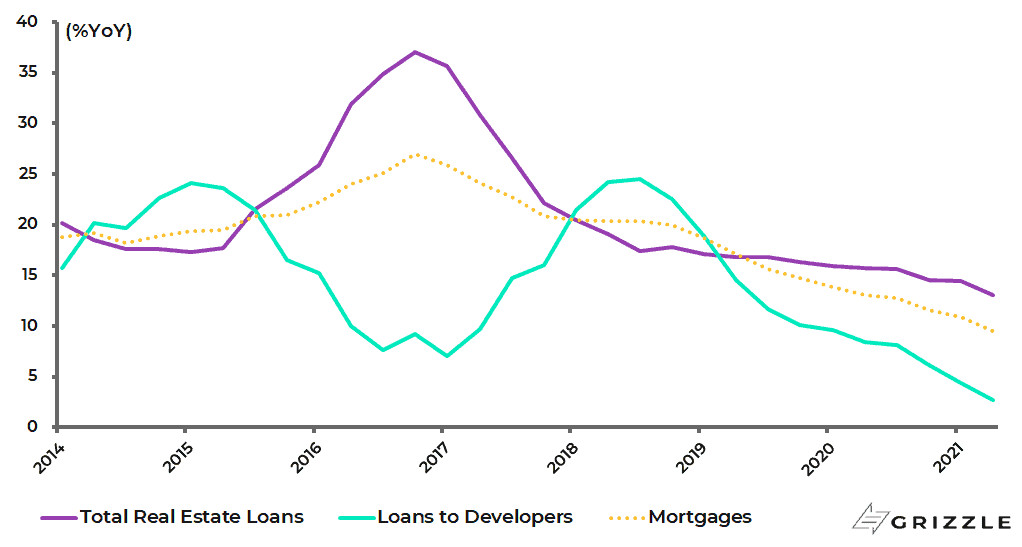

Total property-related bank loan growth slowed from 11.6% YoY at the end of 2020 to 9.5% YoY at the end of 2Q21, with the growth in lending to developers and mortgage loans slowing to 2.8% YoY and 13% YoY respectively at the end of 2Q21.

China property-related Bank Loan Growth

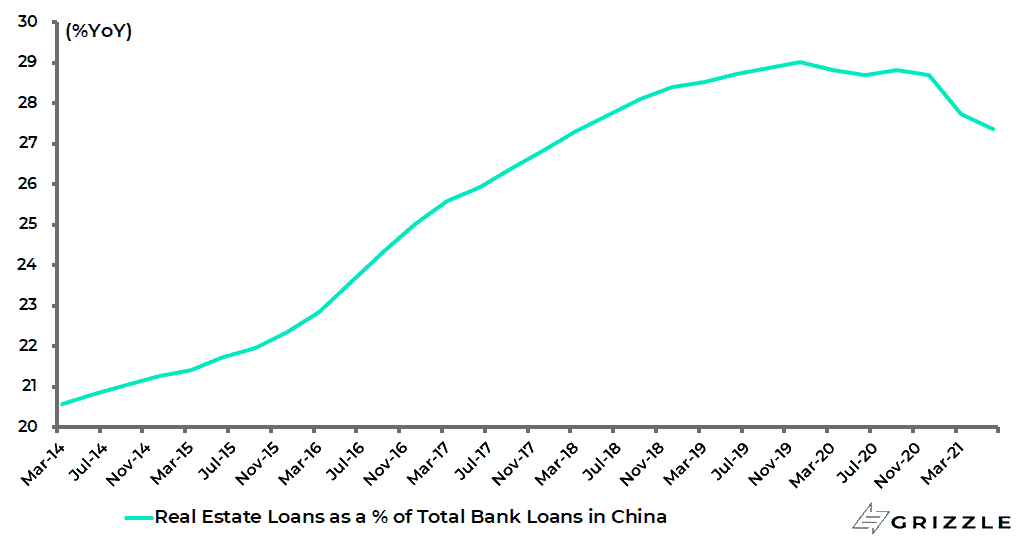

As a result, property-related loans accounted for 27.4% of total bank loans at the end of 2Q21, down from 28.7% at the end of 2020 and 29% at the end of 2019.

China property-related loans as % of total bank loans

At the end of last year the authorities set ceilings on the share of property lending in individual banks’ loan portfolios.

For the large banks, the ratio of outstanding property loans (including lending to developers and mortgages) to total loans is capped at 40%.

For medium and small banks, the corresponding ceilings are 27.5% and 22.5%, respectively.

Still, the Chinese Government will not, in this writer’s view, be willing to back away from the commitment to the “three red lines policy” in terms of certain developers not meeting the required specified leverage ratios, which is the reason for Evergrande’s liquidity crisis.

On this point, about 10% of the top 60 developers broke all “three red lines” limits resulting in restrictions on their ability to borrow.

Meanwhile, it is logical that Chinese government bonds have rallied in the context of the market focus on Evergrande and China’s so-called “Lehman moment”.

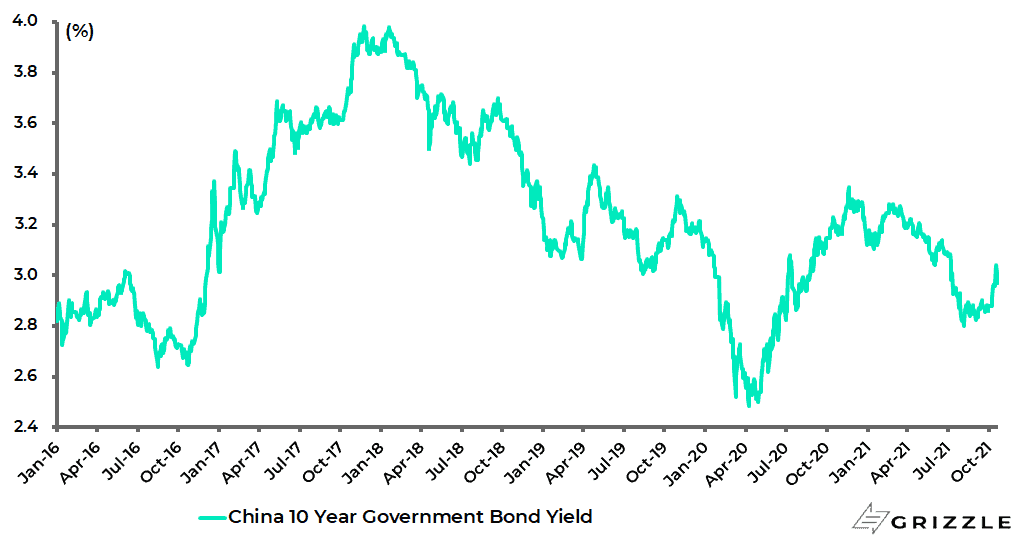

The 10-year China government bond yield declined by 28bp from 3.14% in mid-June to 2.86% at the end of September and is now 2.99%.

China 10-year government bond yield

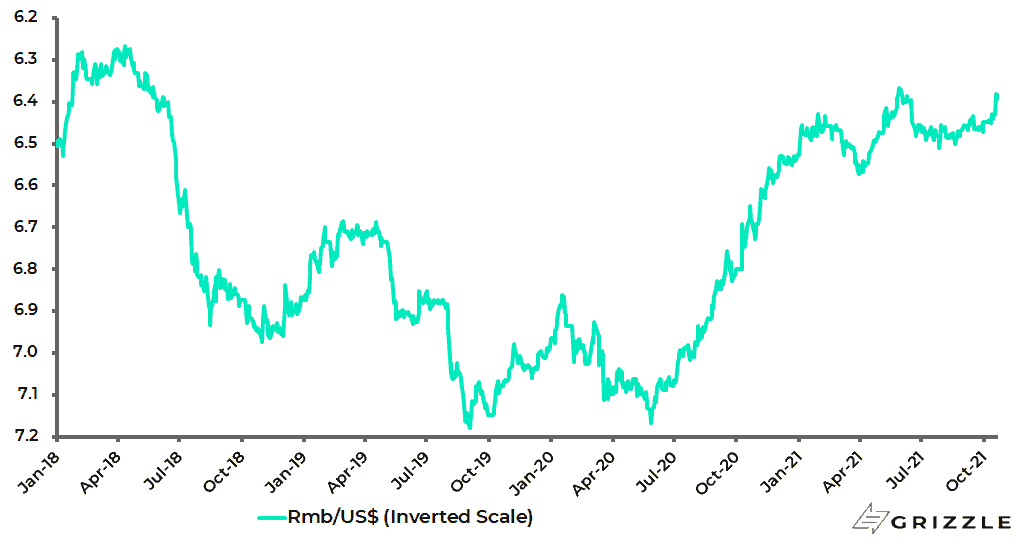

Meanwhile, the renminbi has also not weakened amidst the bearish focus on Evergrande in recent weeks.

The renminbi is up 2.2% against the US dollar year-to-date, following a 6.7% appreciation last year.

This writer remains long-term bullish on the Chinese currency.

Renminbi/US$ (inverted scale)

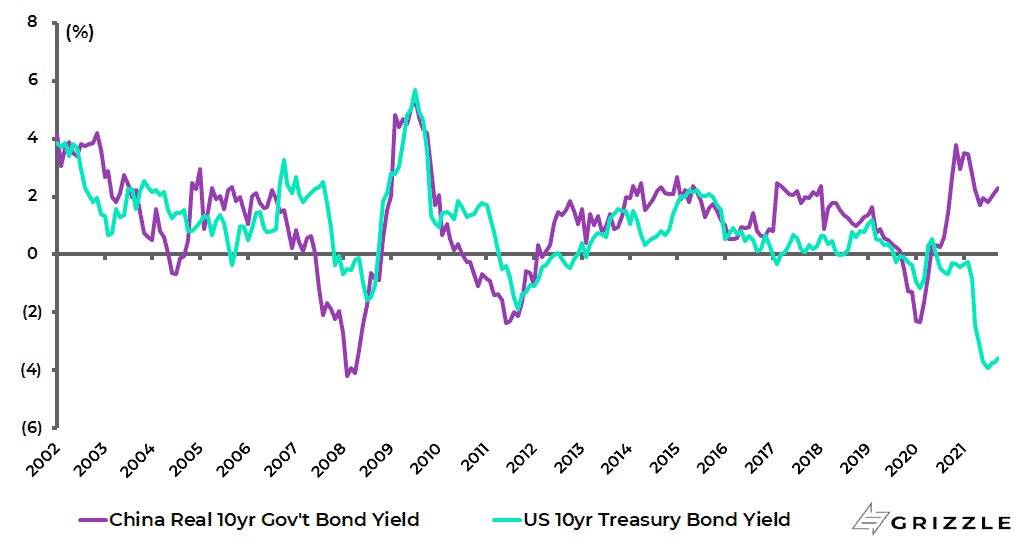

All this reflects the fact that, as has been written here many times before, the PBOC is the nearest thing the world has right now to the old Bundesbank, in that policy is more focused on the interest of savers, and not just debtors.

China’s real 10-year government bond yield, deflated by CPI, is now 2.3%, compared with a negative 3.6% for the US real 10-year Treasury bond yield.

China and US real 10-year government bond yield (deflated by CPI)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.