https://www.youtube.com/watch?v=XVunB3oOkDc

Global coffee powerhouse Starbucks (NASDAQ: SBUX) announced fiscal 2020 second quarter results that beat expectations slightly.

Revenue came in at $6 billion, 3% above the consensus estimate of $5.85 billion.

The performance marked a 5% decline over the same period a year ago when revenues were $7.1 billion.

Non-GAAP earnings per share of $0.32 met the consensus estimate of $0.32.

The results show that Starbucks sales are slowing from the Coronavirus, but not as bad as feared so far.

Most important in the release was management’s comments that they expect sales in China to rebound by their September quarter, though they will be down 30% next quarter compared to last year.

This guidance will set the tone for the next six months depending on if results are worse or better in China and secondarily the U.S.

Comparable store sales fell 10% globally. This was driven by 3% decline in the U.S. and a massive 50% decline in China. International comp growth was down 31% overall driven by China.

[su_panel background=”#d1cef4″ radius=”7″]Overall Starbucks earnings multiple means you are no longer getting a discount compared to earlier in the year, however, this is still a great company and with the troubles at Chinese rival Luckin Coffee you should feel comfortable owning this stock for the long term. [/su_panel]

Starbucks is Fairly Priced, No Longer Cheap but Not Yet Expensive.

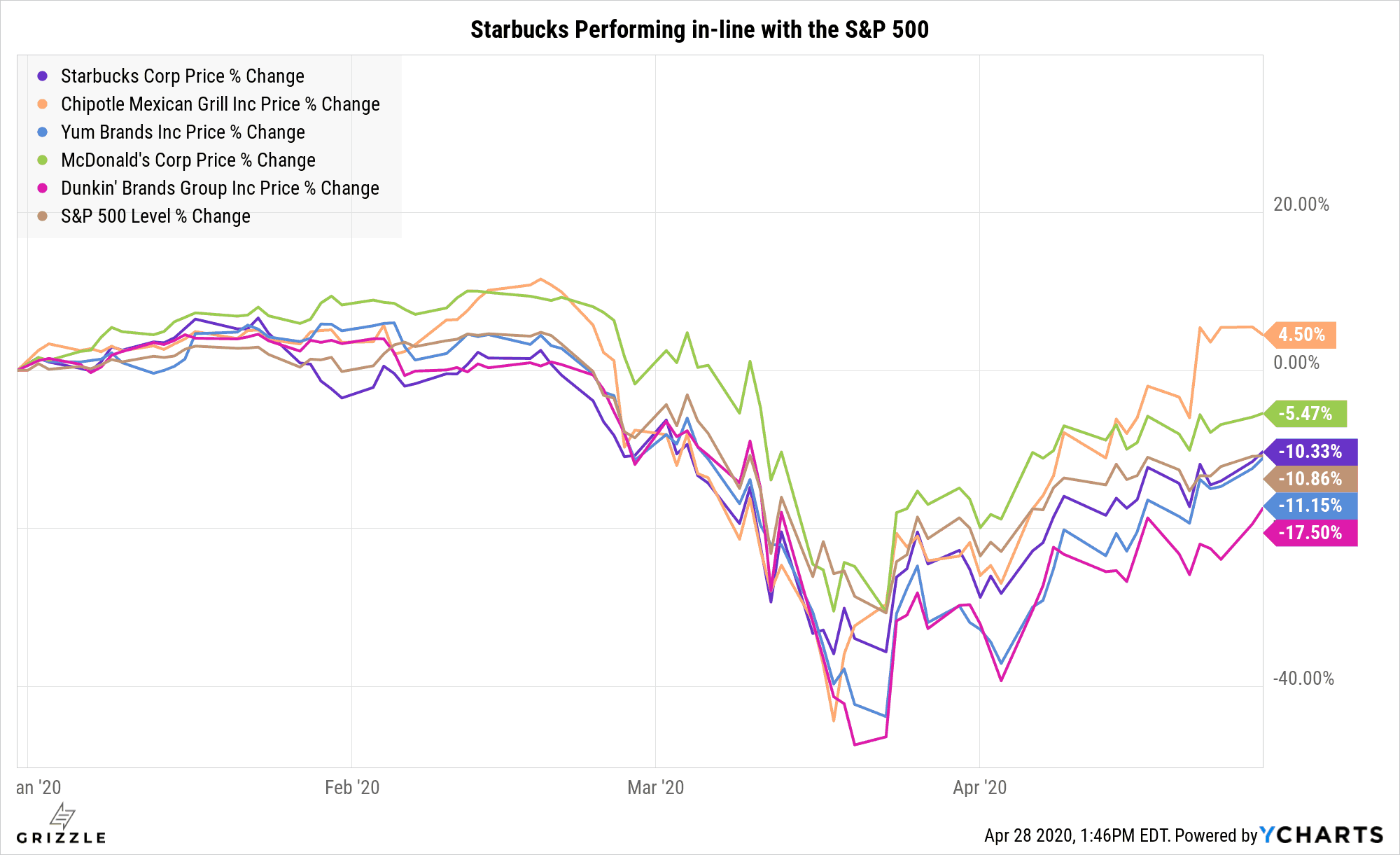

Starbucks Stock Performance vs Peers and S&P 500

Luckin Coffees Demise May Offset Coronavirus

The Asia-Pacific region is a key growth market for Starbucks.

Although it has faced competitive pressures from the increasingly popular Luckin Coffee (NASDAQ: LK) outlets, Luckin’s recent financial fraud could turn into a huge gift for Starbucks.

We will look for any color from management on an acceleration in China sales as an indication they are winning business back from Luckin.

If Luckin ends up closing all its physical stores, Starbucks will definitely see at least a short term boost in sales which could offset some of the negative sales pressure coming from the Coronavirus.

Company is Performing Great But Valuation No Longer Cheap

Starbucks’ latest results were encouraging despite the continuing coronavirus uncertainty.

The fast-casual restaurant industry has produced earnings growth of around 6% over the last five years while Starbucks has significantly outperformed with 16% growth.

Although profit growth is forecast to slow this year to around 8%, it is expected to be more than twice that of the industry.

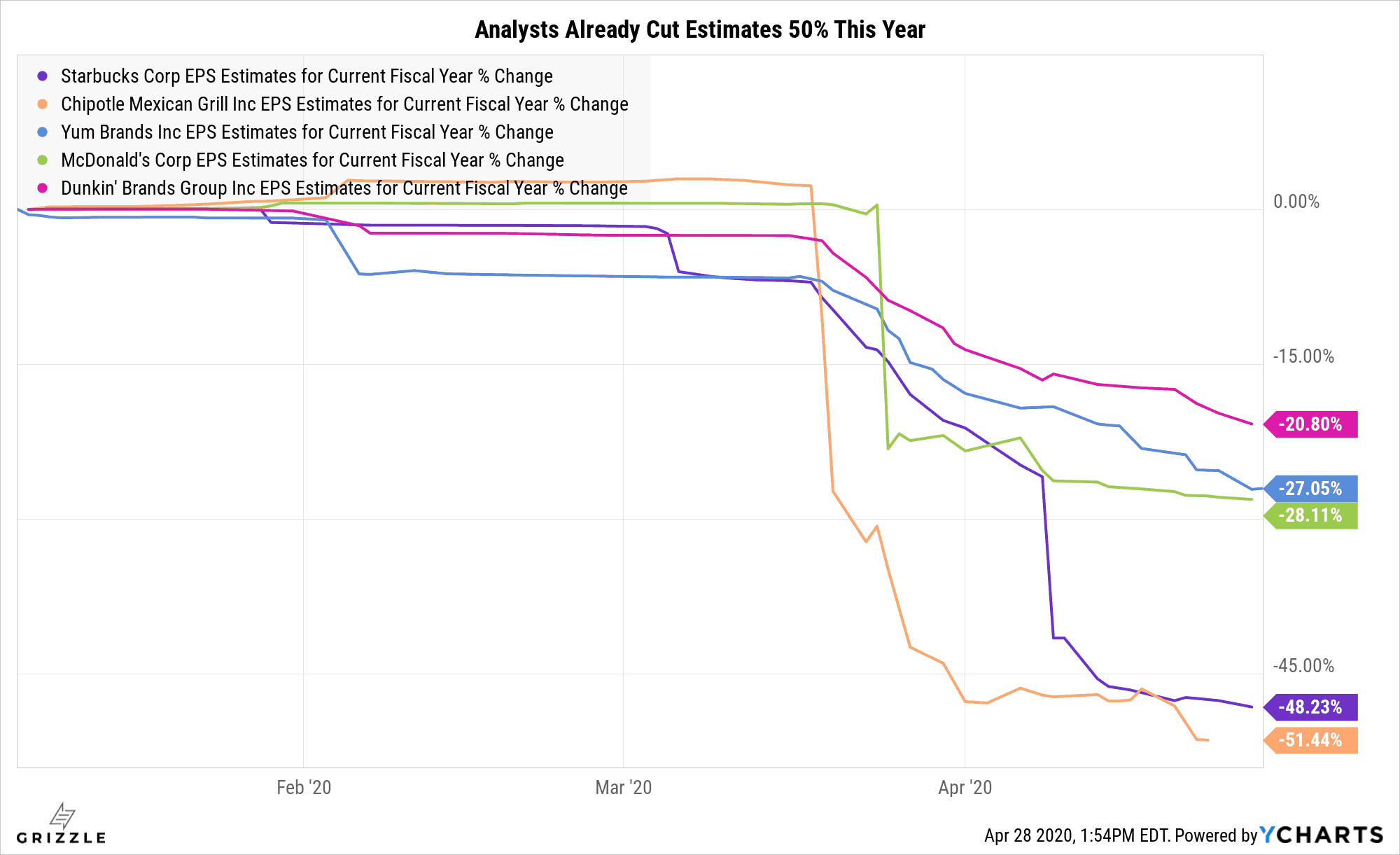

Starbucks stock price rebound has come even while analysts are cutting earnings estimates by 50%!

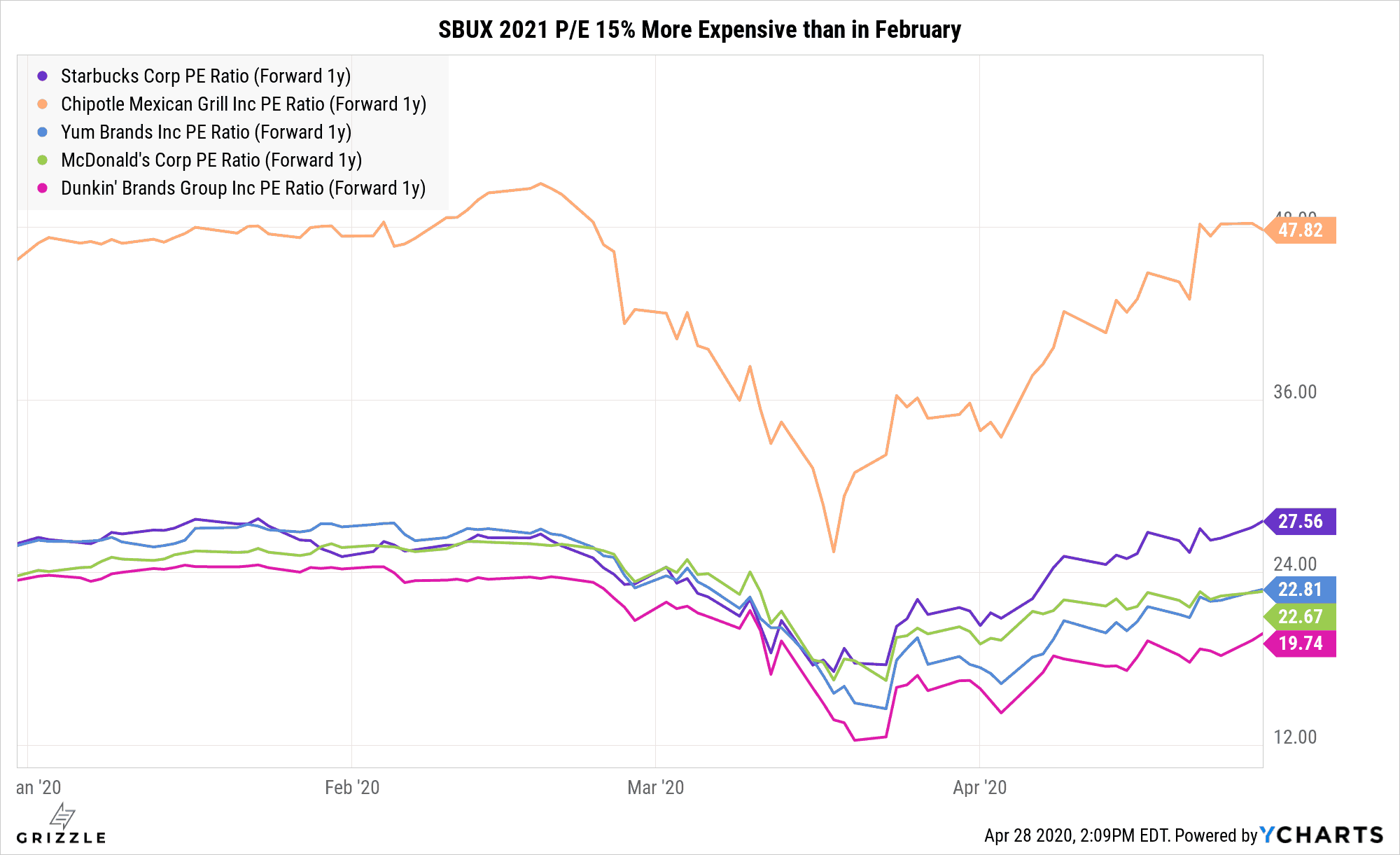

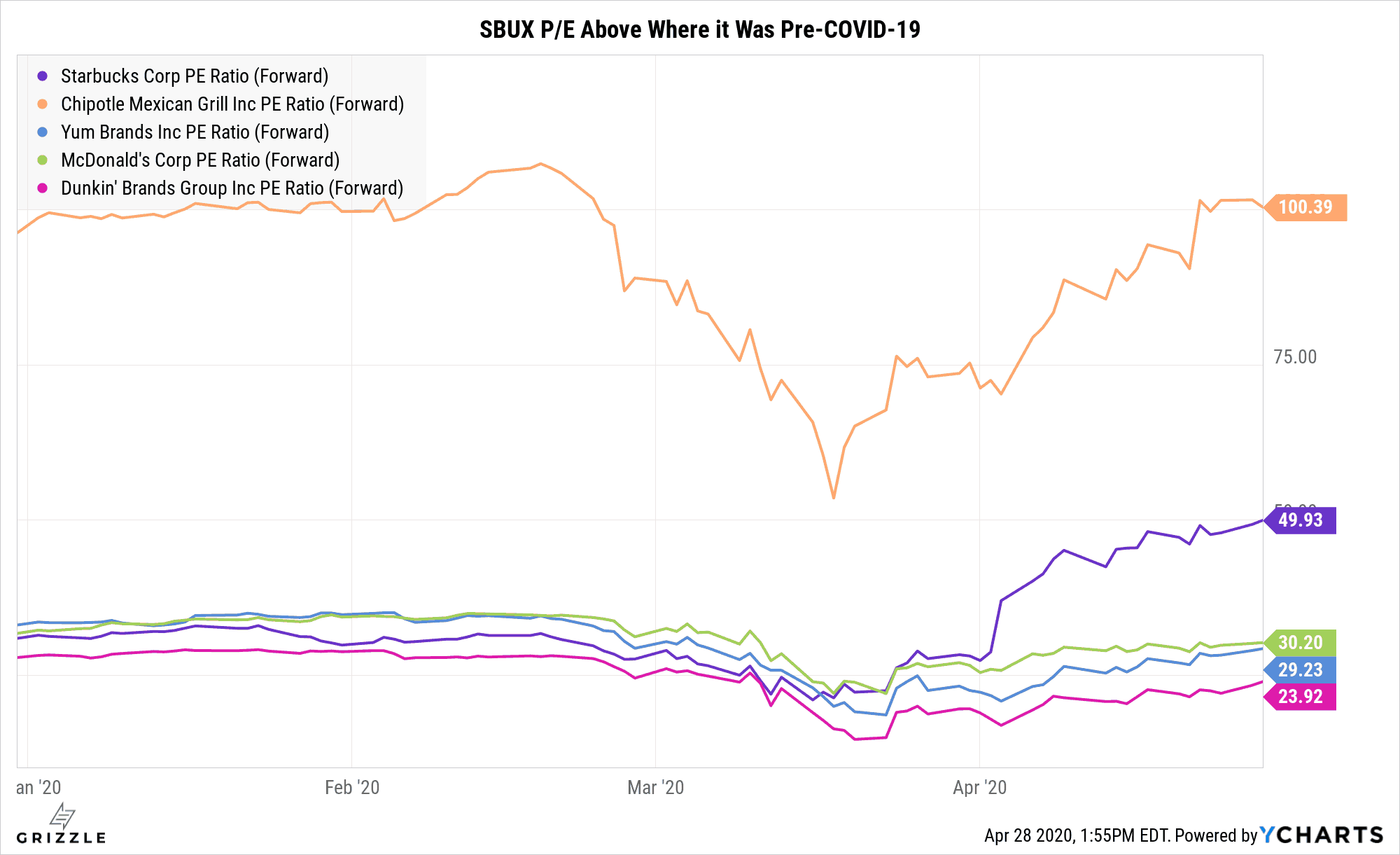

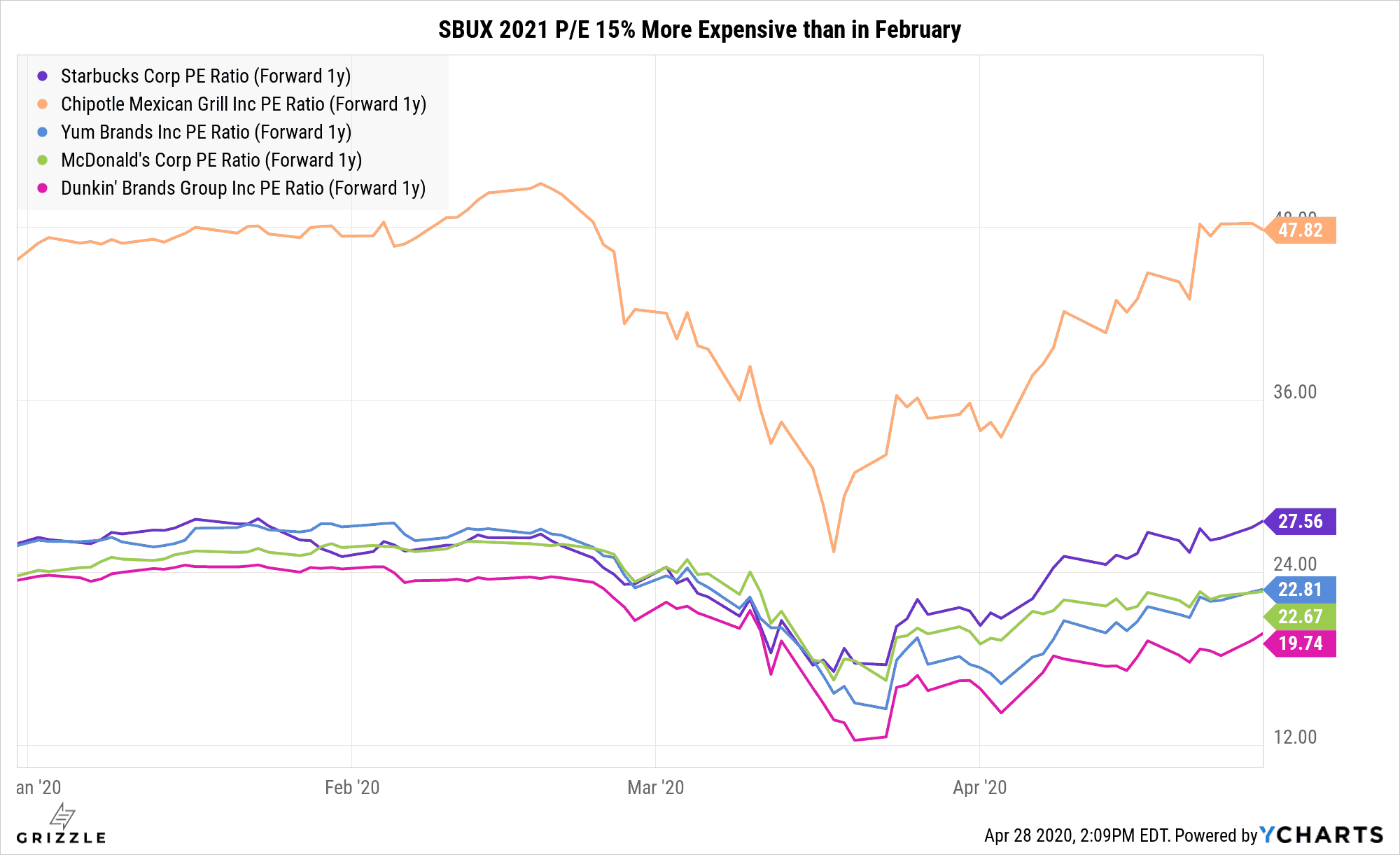

Starbucks 2020 P/E at a Record

But 2021 P/E Only 13% More Expensive Than it Was in February

With interest rates 1% below where they were in February it makes sense that multiple are flat.

They could even be higher and we still wouldn’t call this stock expensive.

There are still potential risks on the horizon for consumer demand, but with a lower cost of borrowing, a major competitor in trouble and a stellar track record, we think Starbucks remains a core holding in any growth portfolio.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.