The base case here since May 2020 has been that the Federal Reserve will adopt some form of yield curve control when faced with the cyclical evidence of recovery coming out of the pandemic, which is likely to be stronger than consensus estimates because of the unleashing of massive pent up demand.

This is no longer the subject of just an academic debate since the US bond market is now selling off and the yield curve is steepening.

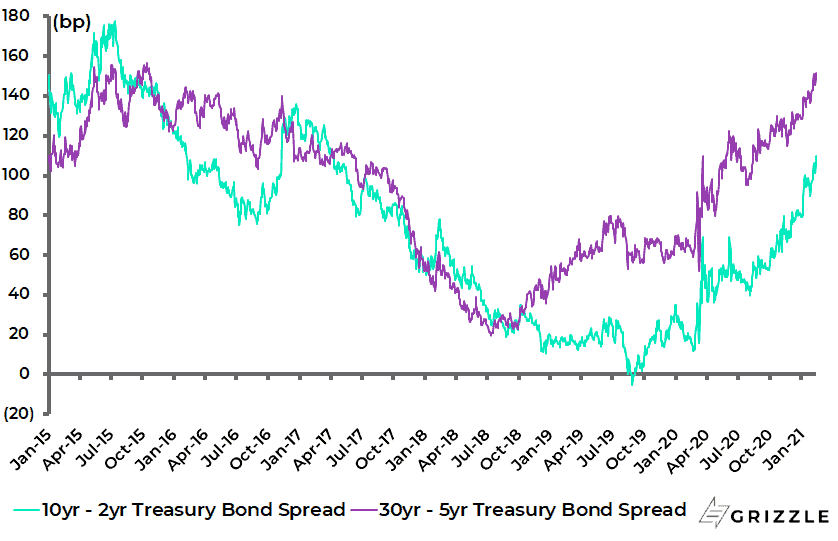

The spread between the 10-year and 2-year Treasury bond yield has risen by 31bp so far this year and by 70bp since early August 2020.

While the yield spread between the 30-year and 5-year Treasuries is up 23bp year-to-date and 56bp since late July 2020.

US Yield Curves (10Y-2Y and 30Y-5Y Treasury Bond Yield Spreads)

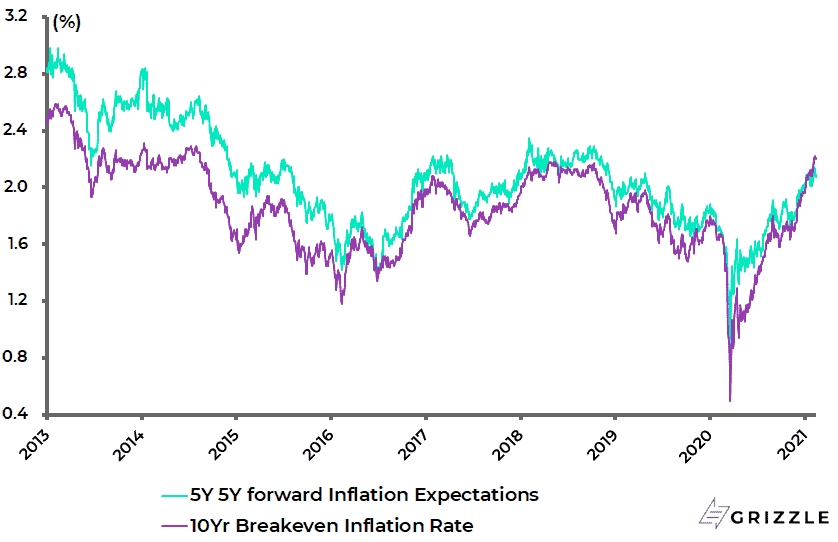

It is also the case that inflation expectations continue to pick up.

The US 5-year 5-year forward inflation expectation rate has risen by 4bp year-to-date and is up 35bp since early November to 2.07% and was 2.14% on 5 February, the highest level since December 2018.

While the 10-year breakeven rate has risen by 22bp so far this year and is up 57bp since early November to 2.21% and was 2.22% on 9 February, the highest level since August 2014.

US Inflation Expectations

Still there is a lot of scepticism about whether the Fed will really try to fix bond yields in line with the base case outlined here.

There is also growing skepticism as to whether the Fed will really remain so doveish when the evidence of cyclical rebound becomes clearer.

These are certainly valid points to raise.

Meanwhile, the Federal Reserve has sought to give itself more room in terms of its public announcements.

Thus, Federal Reserve vice chairman Richard Clarida, noted recently that a transitory increase in price pressures could send inflation over the Fed’s 2% target in the spring as a result of the base effect but he expected that to be “transitory”.

Clarida’s purpose in mentioning this was to make the point that such an increase in inflation would not cause the Fed to counter it with a more restrictive monetary policy.

Indeed he noted that his economic outlook was consistent with the Fed maintaining its monthly US$120bn purchases of Treasury bonds and agency mortgage-backed securities for the rest of this year.

He also stressed that the Fed has given itself room to overshoot formally the 2% target in line with the announcements made at the FOMC meeting last September following the conclusion of the Fed’s 18-month-long strategic review.

To be precise, he stated that the Fed expected to keep the federal funds rate at the current 0-0.25% range until “inflation is on track to moderately exceed 2% for some time”.

It should be noted that the Fed has remained deliberately vague on how much it can overshoot 2% and for how long.

All this is to be expected.

Still if it is the case that yield curve control is considered unlikely by investors, then the market action in response to such a policy is likely to be all the more dramatic since it will not have been discounted.

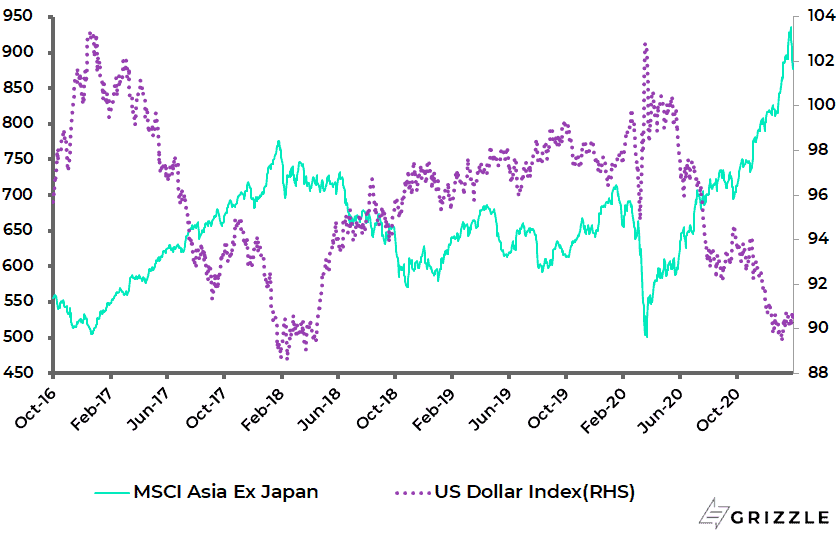

US Dollar Index and MSCI AC Asia ex-Japan Index

But what about if the US bond market revolted against such a move to peg yields?

The base case is that the US Treasury bond market will accept the Fed’s signal, as was the case in Japan when the Bank of Japan imposed yield curve control in September 2016, or indeed in Australia in March last year when the Reserve Bank of Australia adopted yield curve control by setting a target for the 3-year government bond yield.

Still from a Federal Reserve perspective, if the US central bank becomes concerned that higher bond yields threaten economic recovery, it makes sense to move sooner rather later. Certainly, the longer the Fed takes to peg yields the better the chance for a bond market revolt.

Meanwhile the winner from yield curve control, just as with continuing quanto easing, will be the world of finance and those geared into rising asset prices.

In this respect, the view held here since former Fed chairman Ben Bernanke first went unorthodox in late 2008 is that monetary policy has been a major driver of the income polarization in America that has become such a divisive political issue both on the political right and the political left.

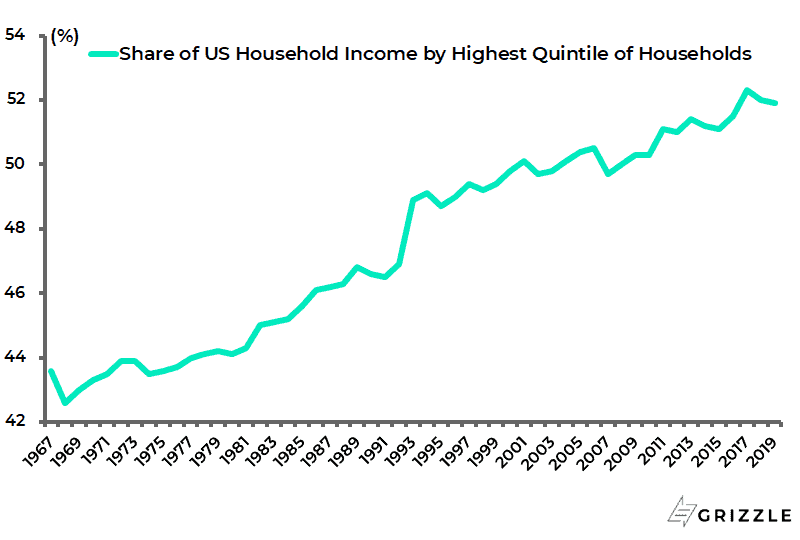

In this respect, it is interesting to note that the share of household income earned by the top 20% in America has been on a rising trend since 1968, though it declined marginally during the Trump years.

Thus, the share of household income by the top quintile of American households rose from 42.6% in 1968 to a peak of 52.3% in 2017 and has since declined to 51.9% in 2019, according to the Census Bureau.

Share of US Household Income by Highest Quintile of Households

Clearly, such a trend is not healthy.

Such data are fuelling calls on the political left for the likes of universal income.

This is why if this writer is wrong, and the Fed does start to tighten meaningfully there will be a political reaction, as well as a market reaction which could well make the taper tantrum of 2013 look like a picnic.

That political reaction will come from the progressive wing of the Democrat Party which believes in Modern Monetary Theory and wants to see central bank monetization used explicitly to fund political programmes, be it universal income, socialised healthcare or cancellation of student debt.

This is a potential point of contention with the Democrat Party establishment which is mainly represented in Joe Biden’s cabinet appointments to date.

But, for now, there is nothing to argue about since the Fed remains on easing mode and Biden is signing up for a massive new multi-trillion-dollar stimulus.

Talk in Washington is of stimulus packages totalling US$3-4tn in 2021 comprising both a short-term up to US$1.9tn Covid relief package and a longer-term US$1-2tn infrastructure plan, with the latter likely to be financed in part by stock market unfriendly tax hikes.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.