If inflation and the commencement of a Federal Reserve tightening cycle have been dominating newsflow in the financial markets, as well as of course events in Ukraine, it is also the case that there is even a potential tightening cycle coming in Japan, the home of deflation in the last 20 to 30 years.

True, the Bank of Japan has continued to signal that it will enforce it’s now more than five-year-old yield curve control policy re-stating earlier this quarter that it stands ready to buy the 10-year JGB at a yield of 0.25%.

This stance was also confirmed at last week’s BoJ policy meeting.

Still, the problem with such a policy is that it means that the selling pressure will remain on the yen in a world where it is assumed that both the Fed and ECB are now tightening.

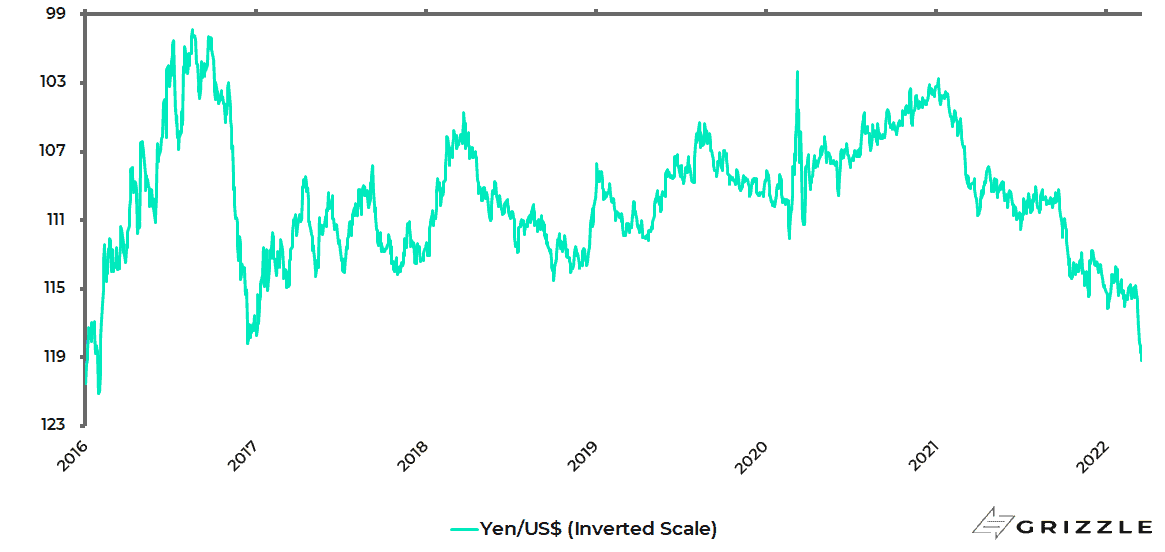

For the reality is that a further weakening of the yen, and it has already declined by 13.4% against the US dollar since the start of 2021, will lead to a further pickup in imported inflation pressures, most particularly as regards imported energy costs which have already risen significantly in a shock which has in turn started to damage Japanese consumer confidence.

Yen/US$ (inverted scale)

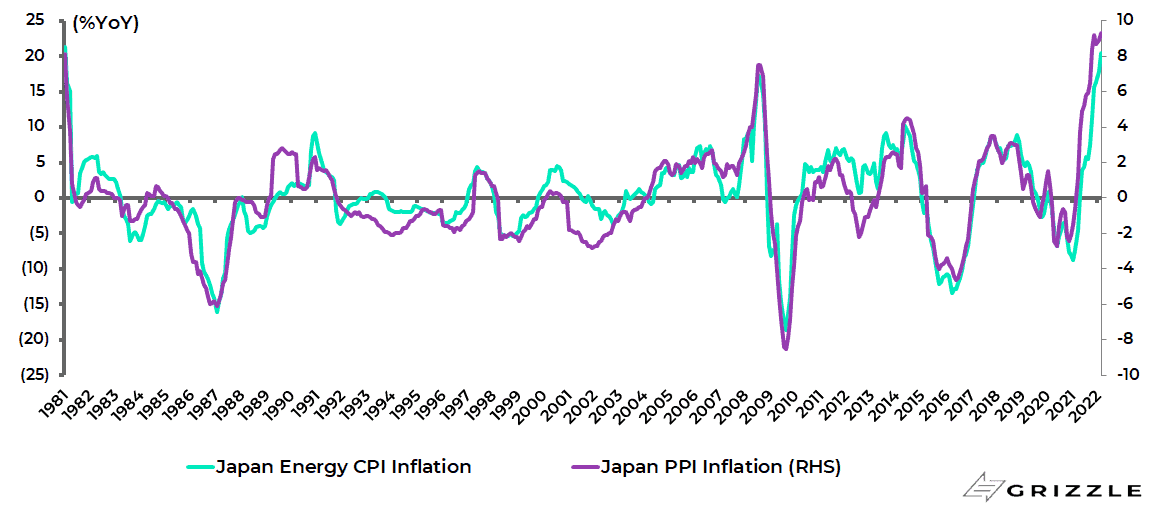

Japan energy CPI inflation rose to 20.5% YoY in February, the highest level since January 1981. PPI inflation also rose to 9.3% YoY in February, the highest level since December 1980.

Japan energy CPI inflation and PPI inflation

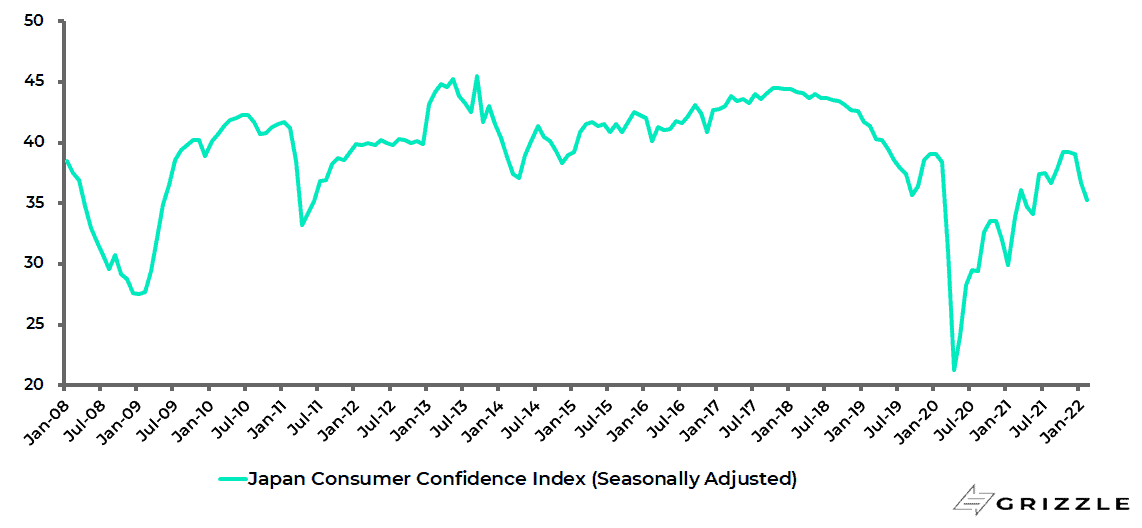

While the consumer confidence index declined by 2.4 points to 36.7 in January, the biggest decline since April 2020.

It was down a further 1.4 points to 35.3 in February, the lowest level since May 2021.

Japan consumer confidence index (seasonally adjusted)

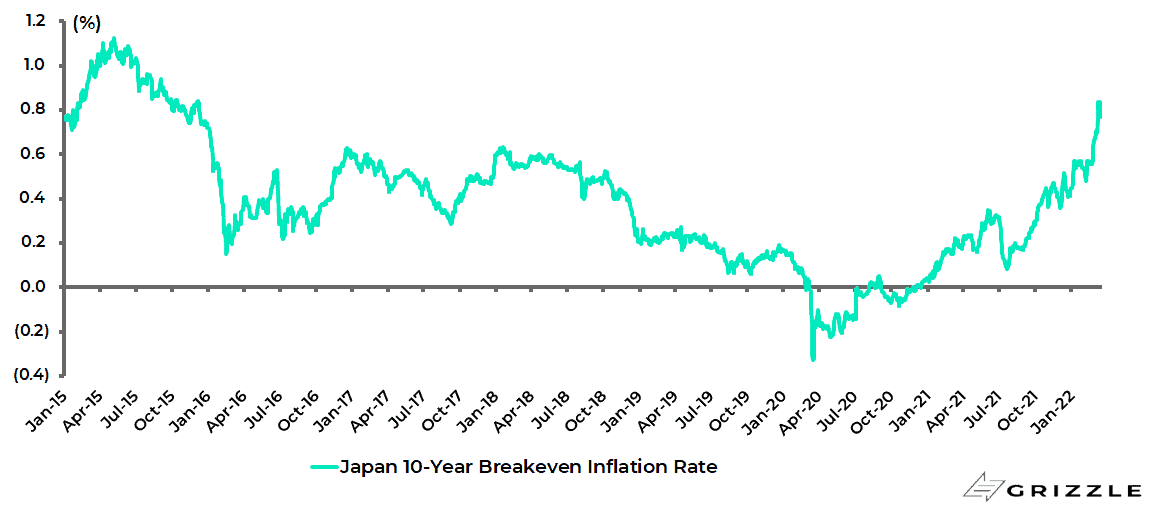

The above dynamic of imported inflation pressures is the most logical explanation for the continuing rise in inflation expectations in Japan.

The 10-year breakeven inflation rate has risen from 0.07% in July 2021 to 0.84% on 11 March, the highest level since October 2015, and is now 0.78%.

Japan 10-year breakeven inflation rate

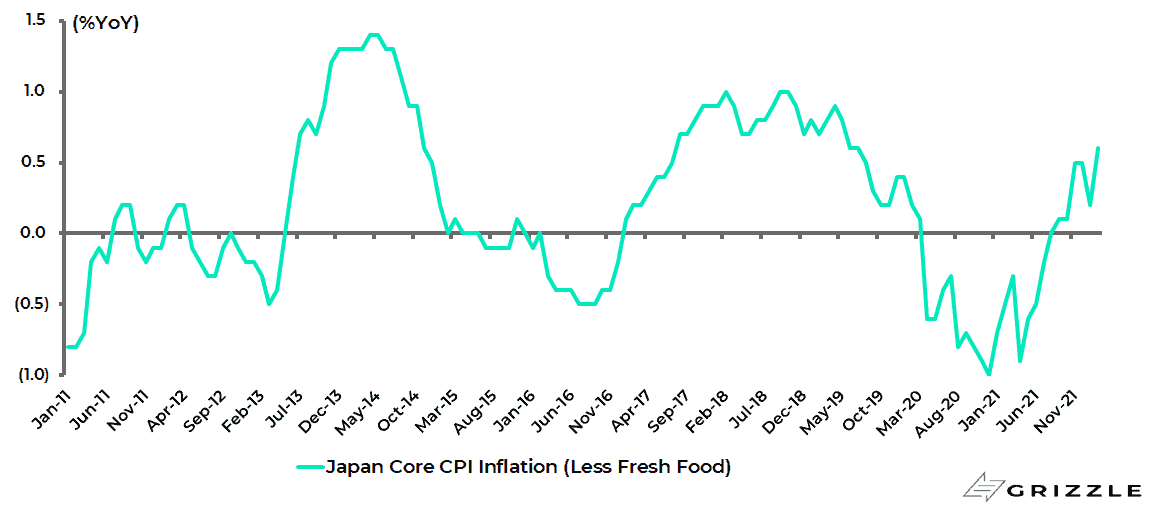

It should be remembered that the BoJ’s formal inflation target is core inflation which in Japan excludes fresh food but includes energy.

Japan core CPI rose by 0.6% YoY in February.

Japan core CPI inflation (excluding fresh food)

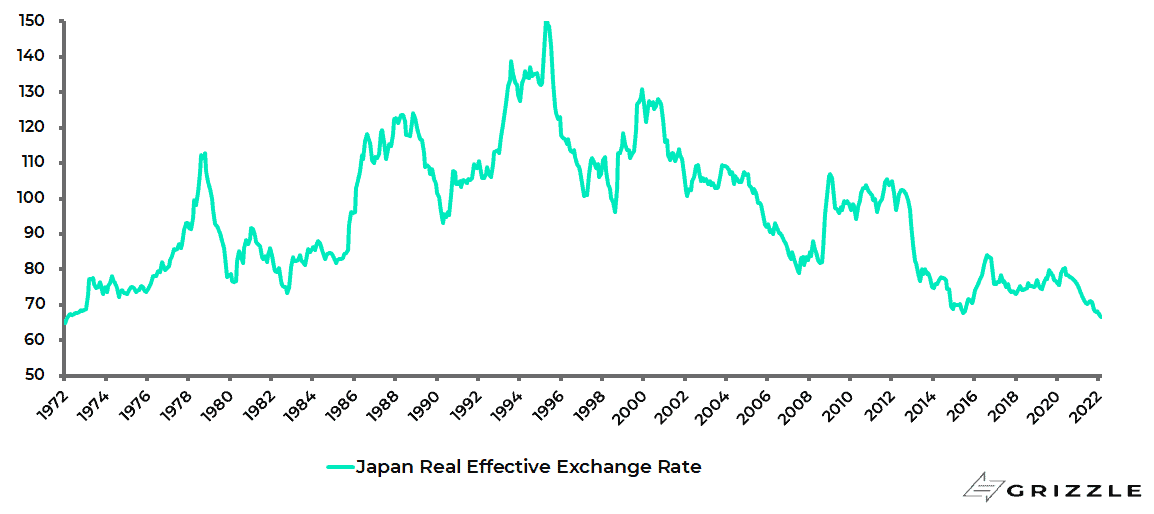

The near-term risk is therefore for a further sell-off in the yen in the context of current monetary policy even though the Japanese currency is fundamentally already extremely cheap on a real effective exchange rate basis.

The Japan real effective exchange rate is now 56% below the peak reached in April 1995 and is at the lowest level since February 1972.

Japan real effective exchange rate

The above is why a decision to end the always silly negative rate policy makes eminent sense.

It should be remembered that BoJ Governor Haruhiko Kuroda only made one negative rate move back in January 2016, when he moved the complementary deposit facility rate from +0.1% to -0.1%, and then refrained from any further such cuts as a result of massive blowback both from Japan’s financial sector and from Liberal Democrat Party MPs who had received negative blowback from their elderly saver constituents.

Indeed the word at the time was that Kuroda was essentially ordered by then prime minister Shinzo Abe to make no further moves into the negative territory.

If a possible “tightening” of Japanese monetary policy is possible in coming months, it also raises the question of how long the current policy of yield curve control can be maintained.

A possible adjustment of policy could be, for example, to target a higher yield by moving the upper limit on the 10-year JGB from 25bp to 50bp.

The Eurozone Will Likely Shrink Negative Rates This Year

Meanwhile, if Japan may see a retreat from negative interest rates, the same is also possible in the Eurozone where the deposit facility rate is a minus 0.5%.

In this respect, ECB Executive Board member and chief economist Philip Lane, who until recently had continued to play down, if not dismiss outright, the inflation risk, gave an interesting speech last month (see Philip Lane’s speech at MNI Market News Webcast: “Inflation in the near-term and the medium-term”, 17 February 2022).

The most interesting point is Lane’s admission that the “excessively-low” inflationary environment that prevailed from 2014 to 2019 might not re-emerge after the pandemic is over.

He attributed the reasons for this to both the “scale of the fiscal and monetary response to the pandemic” and the fact that the NextGenerationEU (NGEU) programme, otherwise known as the €750bn Recovery Fund, has provided “an important anchor for medium-term economic prospects, especially for the main beneficiaries” – of which Italy is by far the most important in terms of the continuing economic viability of the Eurozone as a political project.

Since then, Russia’s invasion of Ukraine and the resulting historic decision by Germany both to re-arm and to accelerate energy transition, and thereby reduce its chronic dependence on Russian energy, have only further increased the prospects for a pickup in inflation in the context of a more activist fiscal policy.

As a result, money markets are now expecting a rate hike of 10bp by the ECB in July and a total of 40bp of hikes in 2022.

But that would still leave the Eurozone with negative interest rates, though at least a start will have been made from exiting what has always been a crazy policy and one which is particularly damaging for European banks.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.