European Fiscal Union & US Dollar Weakness

There have been several reasons why the US dollar has weakened in recent months, ranging from a soaring US fiscal deficit to ultra-loose Federal Reserve policy.

But another reason is the bid for the euro caused by a growing move towards fiscal union.

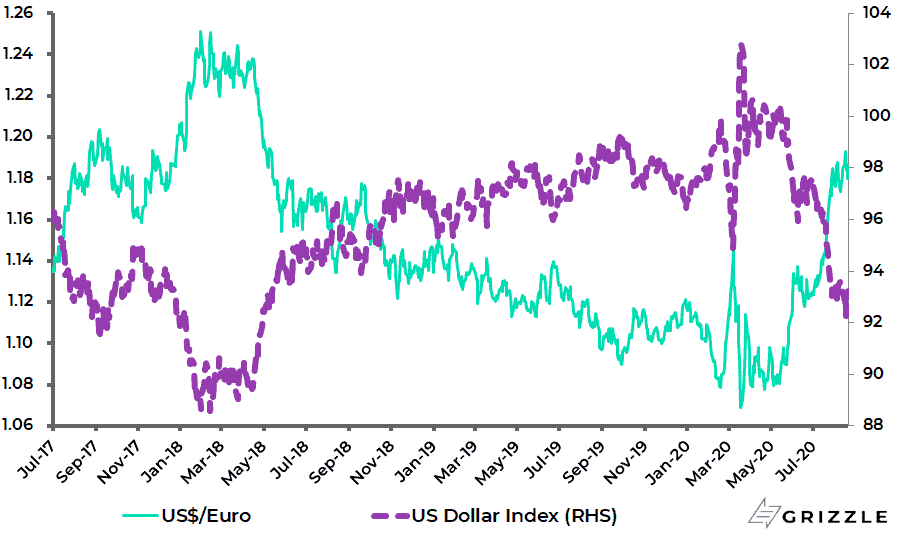

US Dollar Index and US$/Euro

This is a reference to the formal announcement last month of the €750bn European Recovery Fund which comprises a mixture of grants and loans (€390bn in grants and €360bn in loans), and with a re-distributional element in favour of what used to be known during the Eurozone Crisis as the “Pigs” (i.e. Portugal, Italy, Greece and Spain).

Italy alone, for example, is due to receive €209bn (€81bn in grants and €127bn in loans) from the fund.

The European Recovery Fund is also another example of Covid-19 acting as a catalyst for a major change in policy.

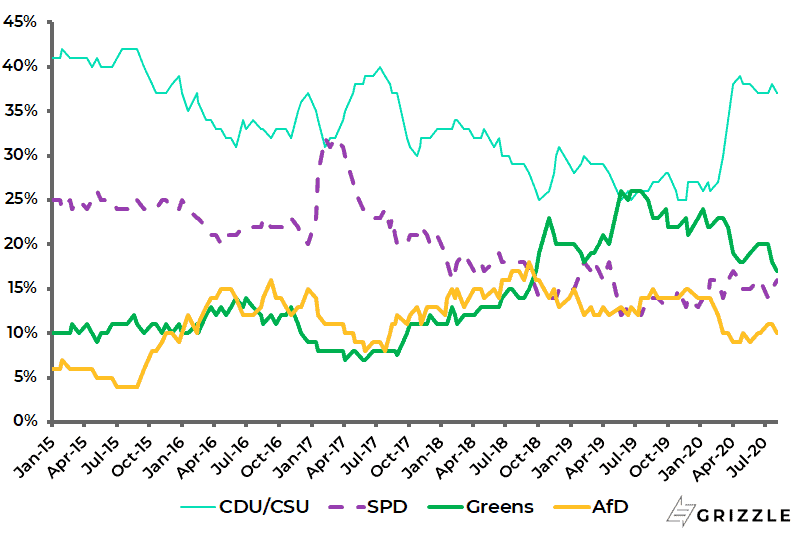

This is because German Chancellor Angela Merkel was only able to back the proposal for a mixture of grants and loans so publicly because of the big surge in her and her party’s popularity as a result of the perceived successful management of the virus in Germany.

Germany Opinion Polls: Political Party Support

The anticipation of the Recovery Fund has also given a bid to the euro which makes sense given the progress made towards promoting a so-called risk-free asset in the Eurozone.

The euro has appreciated by 12.5% against the US dollar since bottoming in March before peaking last week

Meanwhile, European equities would be a natural beneficiary if V-shaped recovery expectations return with a vengeance, causing yield curves to steepen as concerns rise that monetary policy is too easy.

COVID-19 Deaths are Far More Significant than Cases

Still, before this can happen investors have either to stop fretting about the virus or start celebrating the arrival of a vaccine.

As a believer in Farr’s Law, this writer’s base case remains that the vaccine will ultimately prove irrelevant.

But that will not stop financial markets being hyper-focused on any positive newsflow on the issue.

And there will likely be a lot of such newsflow, much of it speculative.

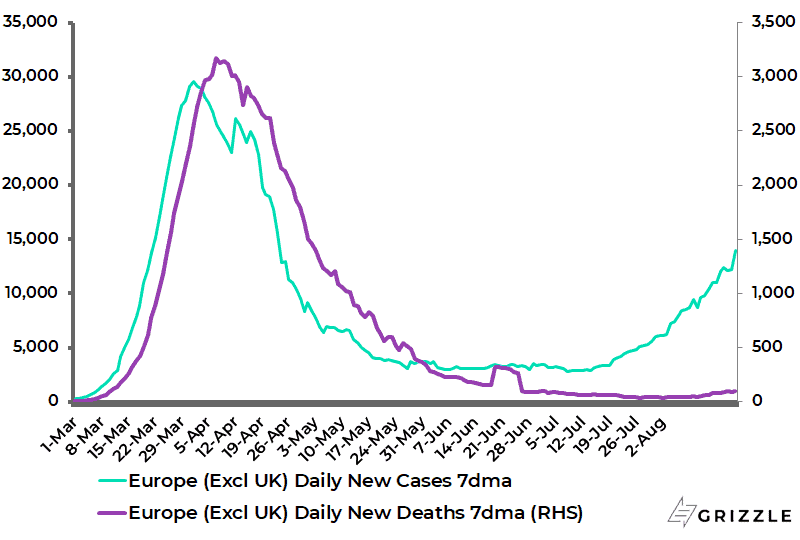

As for the trend in Covid 19, the trend in cases in Europe has picked up significantly in recent weeks as borders have re-opened for the summer holiday season.

The 7-day average number of daily new cases in Europe, excluding the UK, has risen nearly five-fold from 2,825 in early July to 13,967, though it remains 53% below the April peak.

But so far the pickup in deaths has not been significant.

The 7-day average number of daily Covid-19 deaths has risen from a recent low of 38 in early August to 103, but it is still 97% below the peak reached in April.

Europe ex-UK Covid-19 7-day Average Daily New Cases and Deaths

And it is surely the case that deaths are far more important than cases.

One reason for this is simply that, from an investment standpoint, markets are much more likely to react to rising deaths than rising cases since markets are driven, first and foremost, by fear and greed.

And rising deaths trigger increased fear.

But the other point is that death is a fact whereas rising cases, not matched by a similar pickup in deaths, can be spun both positively and negatively.

Anyone who wants to see the negative spin can watch CNN.

But rising cases, not matched by a corresponding pickup in deaths, suggests that the virus is in the process of burning itself out in line with Farr’s Law.

On that point, this writer recently came across an interesting article which attributed the following quote to William Farr, a quote which is relevant today:

For the record Farr, who was trained in medicine, mathematics and medical journalism, was born in England in 1807 and died in 1883.

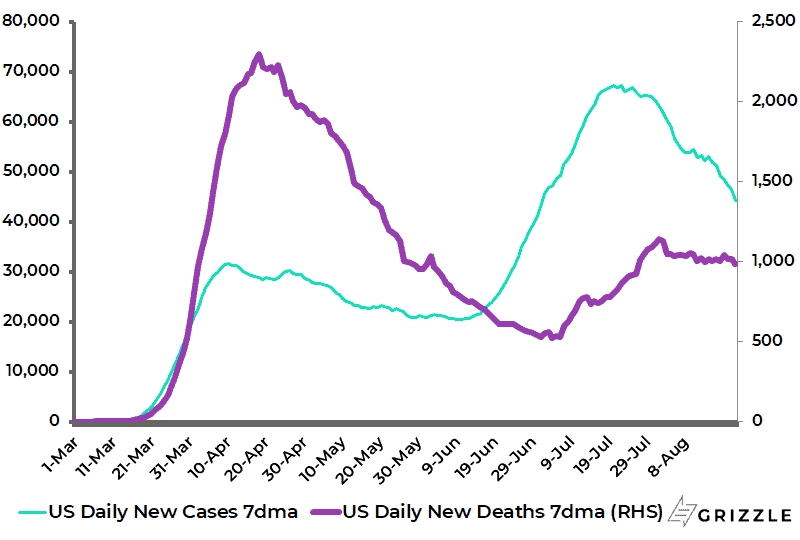

That death rates are far more important than cases is also suggested by the fact that the American stock market has continued to rally despite, until recently, rising cases.

One reason for this resilience is that death rates have been lagging.

Still, the positive point now is that cases in America are 34.4% below their peak in late July, though the decline in the death rate from the recent high is less marked.

The 7-day average number of daily deaths has declined by 13.4% from 1,140 on 1 August to 987.

US Covid-19 7-day average daily new cases and deaths

Trump Needs to Contain the Virus by November

A sharp decline in cases, and of course deaths, is badly needed by Donald Trump whom most observers have now written off as regards the outcome of the presidential election.

This may be premature but it is hard for Trump to win if the virus is still raging in November and it becomes a one-issue election, since the opinion polls show the Donald is viewed as having done a bad job on Covid-19.

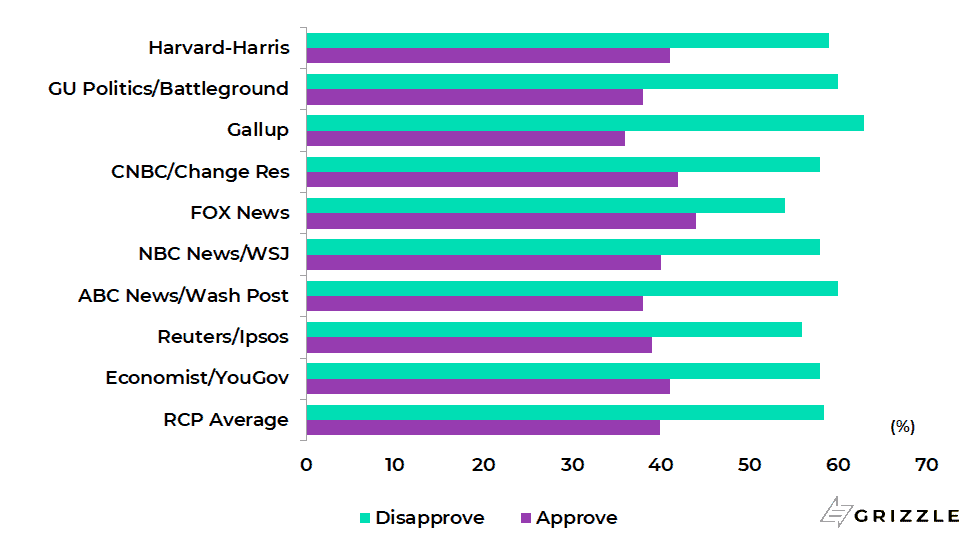

Opinion polls conducted over the past four weeks show that an average 58.4% of the respondents disapprove of the way Trump has handled Covid-19 and only 39.9% approve of it, according to poll tracker RealClearPolitics

And in this case perception is reality.

This means the Donald is in the opposite position of Germany’s Merkel.

Public Opinion Polls: Approval of President Trump’s Handling of Covid-19

Meanwhile, it looks for now as if Covid-19 cases peaked in America almost to the day that the 45th American president, doubtless bullied by his advisers, finally endorsed wearing a mask in late July.

This would be ironic.

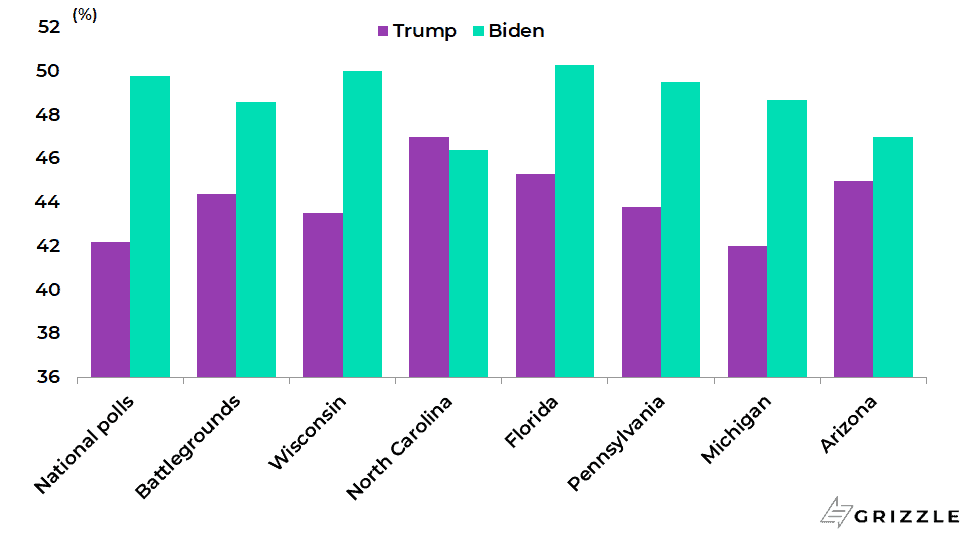

Meanwhile, with Trump still 4.2 percentage points behind in the polls in the key marginal states, the Democrats have done their best at this past week’s virtual Democrat Party convention to project a moderate image in order to try and win the middle ground.

Opinion Polls for November Presidential Election: National and Six Battleground States

The message was anti-Trump rather than detailed policy proposals.

This, clearly, makes political sense from the standpoint of the Biden campaign.

All this means that the outcome of the presidential election, as for the economy, is highly dependent on the future path of the pandemic.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.