Shares of Veeva Inc. (NYSE:VEEV) declined sharply on Wednesday, as traders bought the rumour and sold the fact of another upbeat earnings report. Despite the pullback, Veeva remains one of the top-performing technology stocks of 2019 thanks to surging revenue growth.

Q2 Earnings Summary

- Earnings: $0.55 per share

- Revenue: $266.9 million

For its fiscal second quarter, Veeva earned $79.2 million, or $0.50 per share, compared with $50.3 million a year ago. Adjusted earnings were $87.7 million, or $0.55 per share, which was much higher than the $0.49 expected.

The cloud service provider said revenues surged 27% to $266.9 million, up from $210 million a year earlier. Analysts in a median estimate were calling for $259.3 million. The revenue jump puts Veeva on track to exceed $1 billion in annual sales, according to Bloomberg.

Management expects the strong tailwind to continue into the present quarter, with revenues projected to reach between $274 million and $275 million. Adjusted per-share earnings are forecast in the $0.54-$0.55 range, according to company guidance.

For fiscal 2020, the company expects to generate $1.062 billion in revenues. Full-year adjusted earnings are forecast to fall within $2.11 and $2.13.

VEEV: A Standout Performer

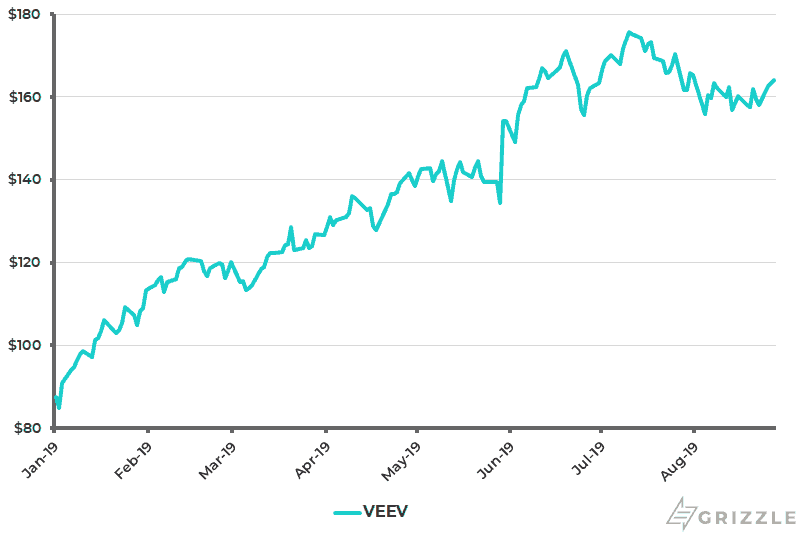

Although Veeva’s stock declined on Wednesday, it has been one of Wall Street’s standout performers for 2019. Even if we factor Wednesday’s 3% slide, VEEV is up more than 81% year-to-date. That’s much better than the S&P 500’s information technology index, which has gained nearly 26% over the same period.

The stock is up eightfold since going public back in 2013 and has a total market capitalization of $22.9 billion.

At current values, VEEV is down more than 11% from its all-time high achieved last month.

Veeva’s stellar performance puts it on the cusp of overbought levels, according to company fundamentals. At its current price, VEEV trades at 23 times fiscal 2020 sales estimates, much higher than the average multiple of 12 over the last three years. Investors should proceed with caution when considering this technology play.

Conclusion

Veeva may be a tad overvalued based on current and projected revenues, but investors are clearly paying a premium for future growth. CEO Peter Gassner recently told Bloomberg that his company feels a lot like Salesforce in its very early stages.

“I was at Salesforce.com very early, so I know what it’s like,” Gassner said. “We’re just early.”

Disclaimer: Author holds no investment position in Veeva at the time of writing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.