The “Blue Wave” is clearly the base case in the forthcoming US presidential election.

Still, markets have become nervous again of late because of renewed concern about a contested election result and related fears of civil strife in America.

Remember there is the contentious issue of postal votes, of which 57m have already been cast.

Still, with Covid cases continuing to rise in America, the prospects look difficult for the Donald since Covid has now become the dominant factor in the election.

The 7-day average daily case count in America has now risen by 129% since mid-September to a record 78,738.

US Covid-19 7-Day Average Daily New Cases and Deaths

COVID-19 is Biden’s True Running Mate

This is the last thing the 45th American president needed, which is why polling in the marginal battleground states has continued to move in Joe Biden’s favour and the betting odds have continued to show rising confidence in a Democratic win.

Betting markets predict that Biden’s odds to win are now 63.8%, up from 54.5% in late September; while Donald Trump’s odds have declined from 45% to 35.3% over the same period, according to poll tracker RealClearPolitics.

US Presidential Election: Betting Odds

While Biden is now leading Trump by 3.1ppts in the six key marginal states, interestingly, this is down from 5ppts in mid-October.

In this respect, it has become clearer than ever that Covid-19 is Biden’s main running mate.

It also has to be said that Biden has performed much better than would have been expected two months ago, while the Democrats have done an effective job of keeping the radical side of the party out of sight during the campaign.

US Presidential Election Opinion Polls in Six Battleground States

Green New Deal and Big Tech in the Crosshairs

If he wins Biden is most likely to reward the Bernie Sanders’s faction of the party with one major policy on their agenda.

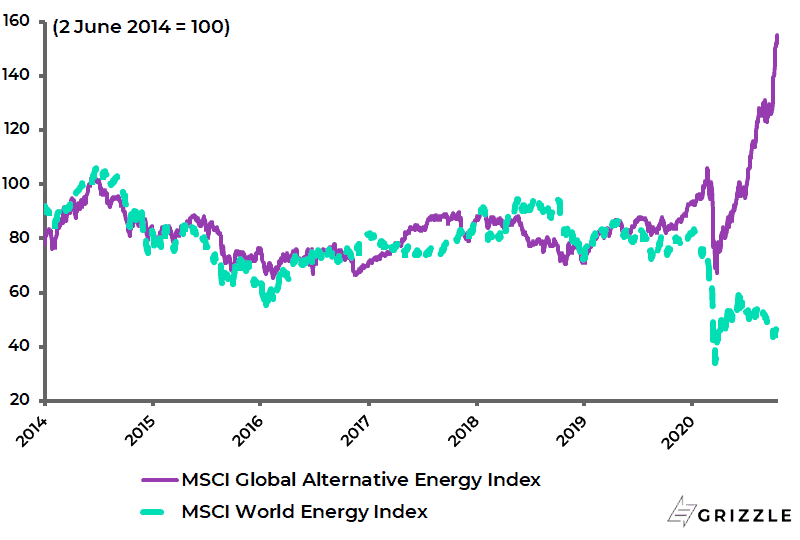

That is the US$2tn Green New Deal, which is why alternative energy stocks have gone vertical as confidence in a Biden victory grows while energy stocks have been smashed yet again.

The MSCI World Energy Index has declined by 33% in US dollar terms on a total-return basis since early June, while the MSCI Global Alternative Energy Index is up by 43% over the same period.

MSCI Global Alternative Energy Index and MSCI World Energy Index

As for another favoured policy of the radical side of the Democratic Party, namely a regulatory attack on Big Tech, that is more likely to be diluted under a Biden presidency.

There is no doubt that the case for targeted taxation and regulation of US Big Tech is compelling, as has long been argued by Elizabeth Warren, and was also spelled out in great detail in the release on 6 October of a 451-page report by the antitrust sub-committee of the House of Representative’s Judiciary Committee on this issue (Investigation of competition in digital markets: Majority staff report and recommendations, by Subcommittee on Antitrust, Commercial and Administrative Law of the Committee on the Judiciary, 6 October 2020).

Two of the more eye-catching proposals in that report to rein in what are described as “digital behemoths” are “structural separations to prohibit platforms from operating in lines of business that depend on or interoperate with the platform” and “prohibiting platforms from engaging in self-preferencing”.

This was followed by the US Justice Department’s antitrust lawsuit against Google filed on 20 October.

This writer agrees with the view of Tim Wu, a law professor at Columbia University, who wrote in a column in the New York Times this past week that the case against Google is “far simpler than many commentators seem to think” (see New York Times international edition: “The winter of antitrust has ended”, 23 October 2020).

Why, for example, with its dominant market share of search estimated at 88%, does Google need to pay Apple billions of dollars in annual payments unless it is to preserve its position and keep potential competitors at bay?

Apple now receives an estimated US$8-12bn in annual payments – up from US$1bn a year in 2014 – in exchange for building Google’s search engine into its products (see New York Times article: “Tech rivals’ détente is worth billions” by Daisuke Wakabayashi and Jack Nicas, 26 October 2020).

As a result of all this, it would seem to be the case that meaningful action to curb the monopolistic power of Big Tech is coming in the next five years on the antitrust theme.

But the critical issue is just how aggressive it will be.

The obvious Silicon Valley firms are very close to the Democratic Party establishment, and indeed essentially coopted that establishment during the eight years of the Obama administration.

For this reason, there will be efforts to resist the more aggressive policies an Elizabeth Warren or a Bernie Sanders would like to implement.

Such policies could include windfall taxation of Big Tech, compelling these companies to unwind deals where they have bought a competitive threat, be it Facebook with Instagram and WhatsApp or Google with YouTube, as well as a provision saying that these companies can no longer both own the platform and be a contributor to the platform.

Further potential reforms would be to make social media companies have the same responsibility that media companies face for content, and stopping them using data without paying for it as has been the practice under the highly lucrative model of so-called surveillance capitalism.

If all the above was implemented on a five-year view, it could decimate the market capitalization of these companies.

Obviously, that is an extreme outcome. But it is also not impossible.

In the meantime, this writer sticks with the base case, until proven wrong: namely, that Big Tech’s outperformance in the American market has peaked out on a relative basis. The six Big Tech stocks’ share of S&P500 market cap rose from 18% at the start of 2020 to a peak of 26.2% on 1 September and is now 24.6%.

US Big Tech Stocks’ Share of S&P500 Market Cap

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.