Amazon reported earnings for the 1st quarter of 2020 that missed analyst expectations.

The stock is down 4% after hours due to the earnings miss and comments from management that they plan to ramp up spending, eating up all the operating income investor’s are used to.

The company did see a revenue surge as consumers were forced to buy fewer products in person, but that surge came with ramped up costs which caused earnings to disappoint.

Operating income was $4Bn down 9% from a year ago.

Revenue of $75.5Bn beat estimates of $74.09Bn by 2%

The big news was earnings missed expectations by a full 21% coming in at $5.01/sh compared to a consensus estimate of $6.32/sh.

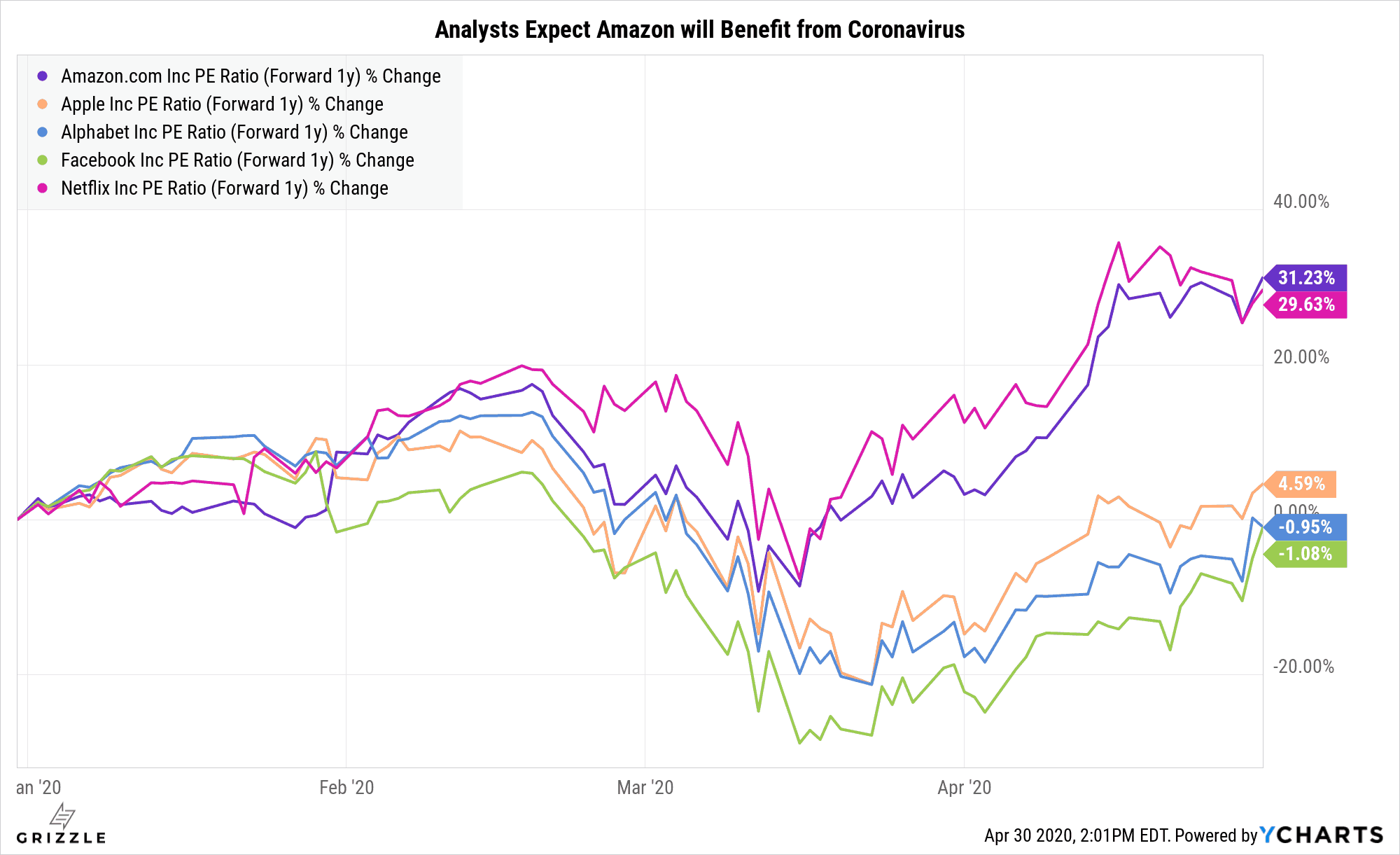

Amazon is one of the few company’s analysts think will be better off due to the global pandemic.

The company is seeing a spike in online sales and has increased headcount by 20% just since march, telling us the sales increase rumors are real.

[su_panel]Amazon remains an amazing company and an attractive stock. The price you are paying now is below the 2018 peak and seems reasonable for a company seeing faster growth as a result of the North American stay at home orders. The stock was a bargain in march but is now simply fairly valued in April [/su_panel]Market Expects an Even Stronger 2020 than Before the Pandemic Began

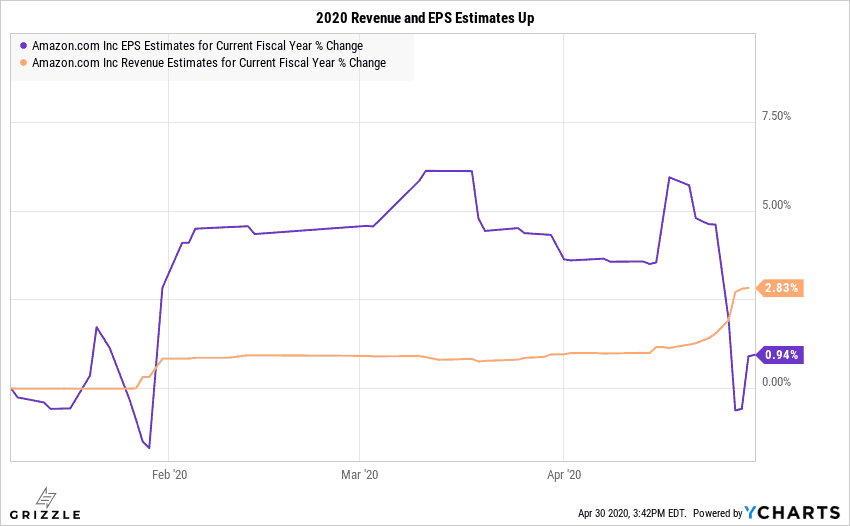

Analysts also think the company is better off with revenue estimates up 3% for the year and earnings estimates up slightly.

No doubt analysts know the company will see higher sales, but that will come at the cost of ramped up headcount and increased costs to protect workers from the Coronavirus which explains why the earnings increase is expected to be minimal.

Coronavirus Actually Benefitting Revenue and Earnings Estimates

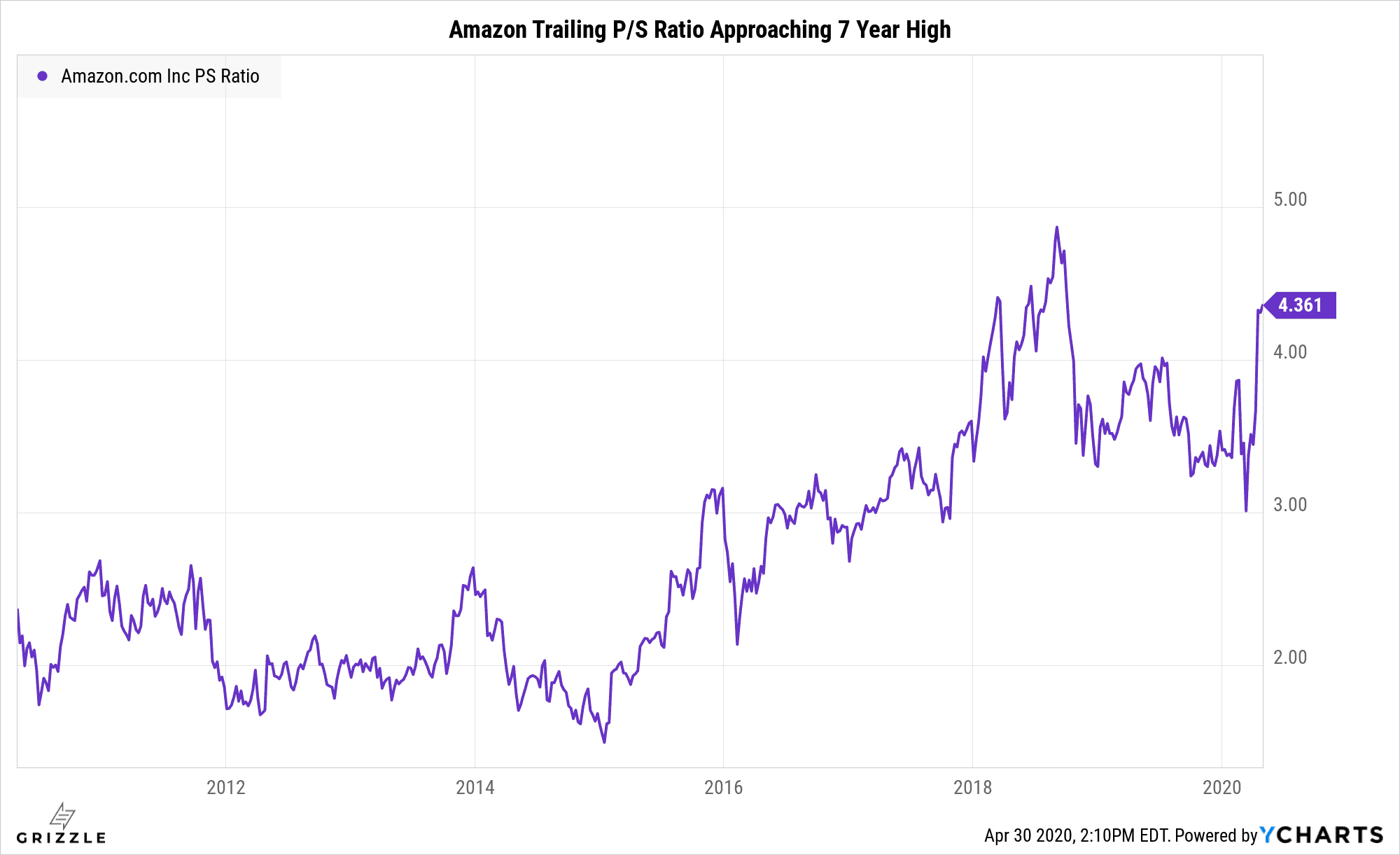

Looking at the trailing multiple of sales an Amazon investor is currently paying, we see the stock is no longer trading for any type of discount.

The P/S multiple of 4.4x is back above the peak in February and approaching the all-time post tech bubble peak of ~5x.

Price to Sales Multiple Near a 20 Year High

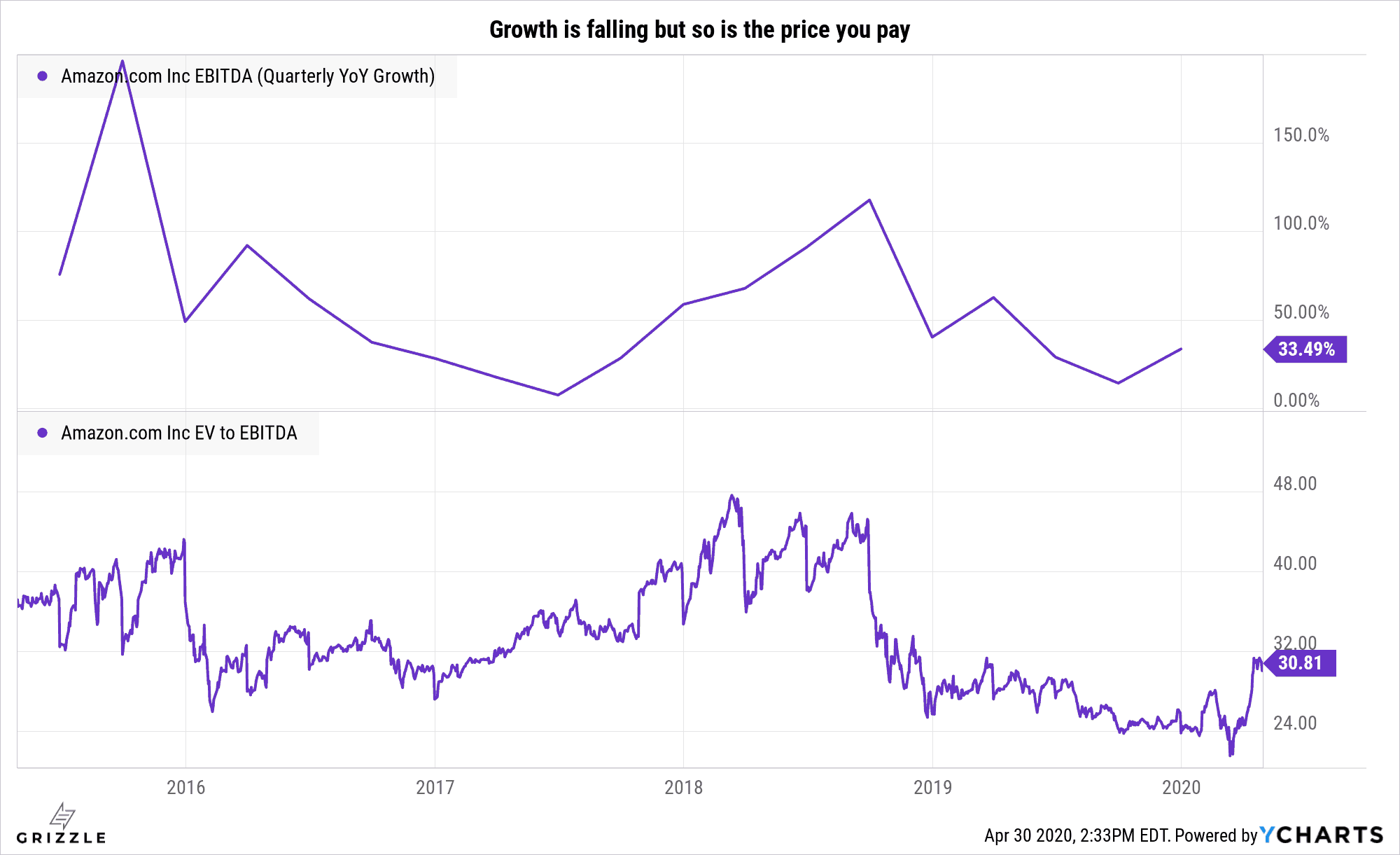

However, if we ignore net income and look at cashflow instead, the true value of this company starts to come into focus.

Yes the cashflow growth rate has been slowing for years now, but the multiple of that cashflow an investor must pay to own the stock has been falling as well.

We can see that Amazon was actually more expensive in the fall of 2018 than it is today, even with the 45% run the stock has been on in the last month.

If growth is actually picking back up as a result of the Coronavirus, Amazon simply looks fairly valued now, compared to slightly cheap in March.

Amazon is a juggernaut and continues to innovate at every turn.

As long as Jeff Bezos is in control your chances of making money over a 1-3 year time horizon are very high.

North America is also not out of the woods yet with the Coronavirus and if infections surge once again and consumers spend more time at home, the stock is going even higher.

Amazon EV/EBITDA is Not Crazy

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.