The re-opening dynamic has clearly been a positive factor.

Still, the most plausible explanation for the US stock market’s extraordinary resilience since the March low is the massive increase in the Fed’s balance sheet.

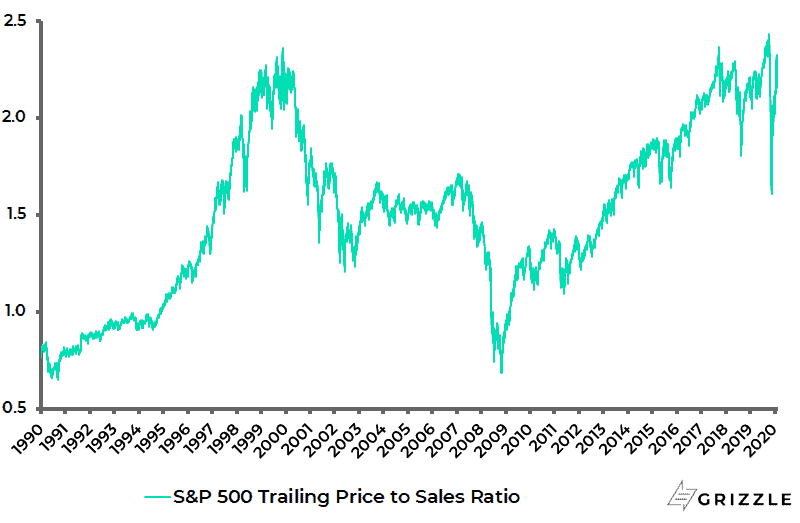

The S&P500’s trailing price to sales ratio has risen from the recent low of 1.61x reached in March to 2.17x, though it is still below the record high of 2.43x reached in February.

S&P500 Trailing Price to Sales

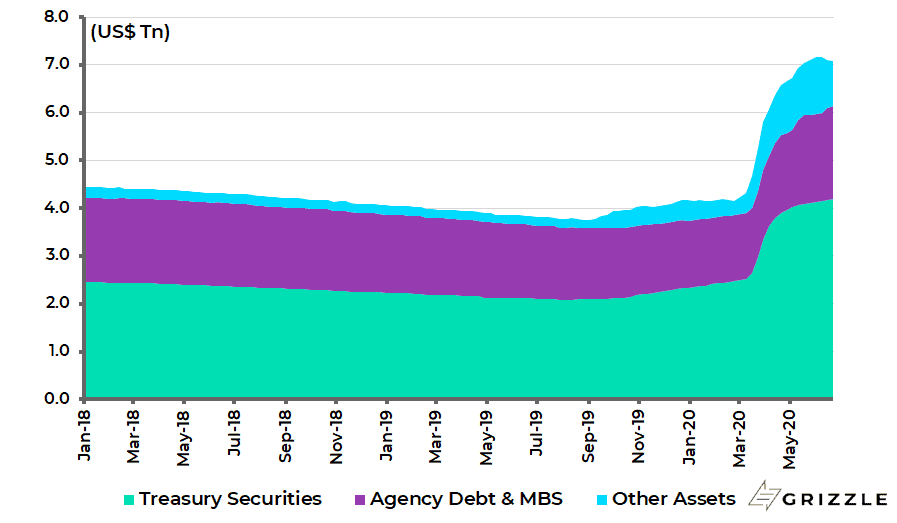

While the Fed’s balance sheet has risen from US$4.2trn at the end of February to US$7.1trn.

Federal Reserve Balance Sheet

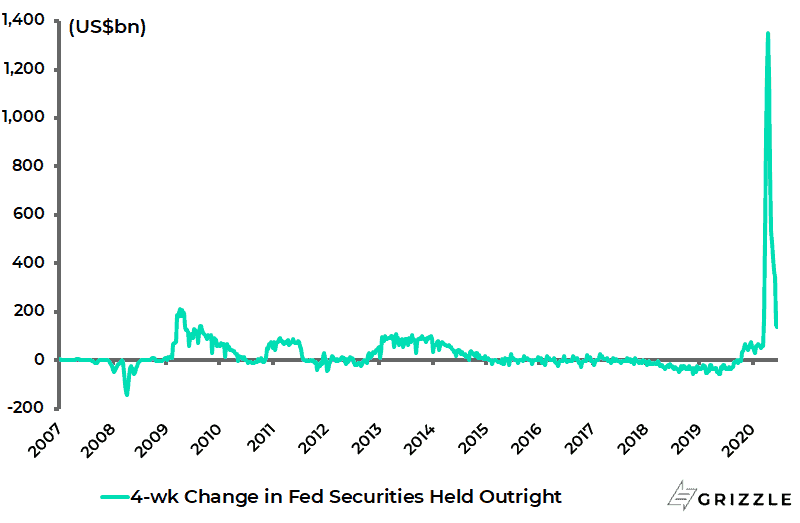

Still, the rate of that expansion has been slowing in recent weeks.

Indeed, the Fed balance sheet has declined by US$15bn in the past four weeks, compared with an increase of US$1.77trn in the four weeks to 8 April.

Four-week Change in Fed balance sheet

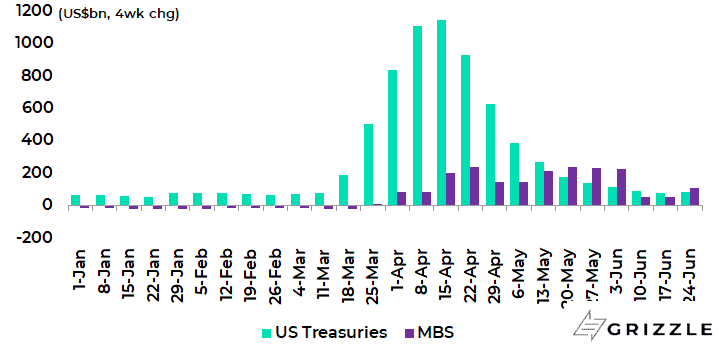

That said, the Fed has remained anxious to assure investors that “unlimited” quanto easing will be around for a while.

Thus, the Fed stated in the last policy meeting on 9-10 June that it will increase its holdings of Treasury securities and agency MBS by at least the current pace of US$80bn and US$40bn per month respectively over the coming months.

Four-week Change in Fed Holdings of US Treasuries and MBS

If the original purpose of the Fed’s actions was to curb market panic, and a resulting credit convulsion, continuing net purchases of Treasury bonds, amongst other things, will help to assuage concerns about the funding of the surging US fiscal deficit.

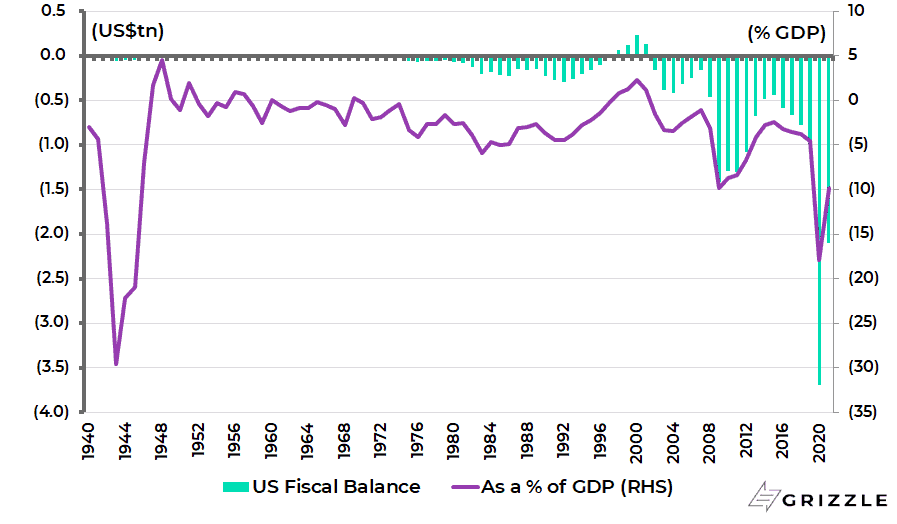

The Congressional Budget Office forecasts that the fiscal deficit will soar to US$3.7trn or 17.9% of GDP this fiscal year ending 30 September and US$2.1trn or 9.8% of GDP next fiscal year.

This will be the biggest fiscal deficit relative to GDP since 1945.

US Fiscal Balance

What about Yield Curve Control?

The word from recent Fed speeches seems to be that this will not come just yet, which means there has been scope for Jerome Powell to engage in some more “forward guidance”.

He has not quite repeated former Fed chairman Ben Bernanke’s extraordinary pledge in August 2011 not to raise interest rates for two years, a pledge that triggered the mother of all carry trades for the private banking “wealth management” industry.

Still he did almost as much in his post-meeting press conference on 10 June, saying that “we are not even thinking about thinking about raising rates”.

Meanwhile, New York Fed President John Williams told Bloomberg Television last month that yield-curve control is “a tool that could potentially complement forward guidance and our other policy actions” and so is something policymakers are “thinking very hard” about (See Bloomberg article: “Williams says Fed thinking ‘hard’ about yield-curve control”, 27 May 2020).

So introducing price controls in the Treasury bond market remains definitely on the Fed’s agenda.

What about the timing of future yield-curve control? It is most likely to be implemented when there is upward pressure on longer-term bond yields as a result of expectations of economic recovery.

That, of course, is to assume that the projection of V-shaped recovery hopes for the third quarter become a reality.

And that clearly depends on avoiding a so-called second wave.

The base case of this writer on the virus remains that of the late Dr. William Farr, a 19th century British epidemiologist, namely that it is a 3-4-month cycle.

Still this writer is not a doctor, let alone an epidemiologist.

So, it is necessary to follow the data, most particularly since the risk of a renewed surge in infections has got to be greatest in the US given the extreme politicization of Covid-19 there and the resulting lack of a coordinated re-opening.

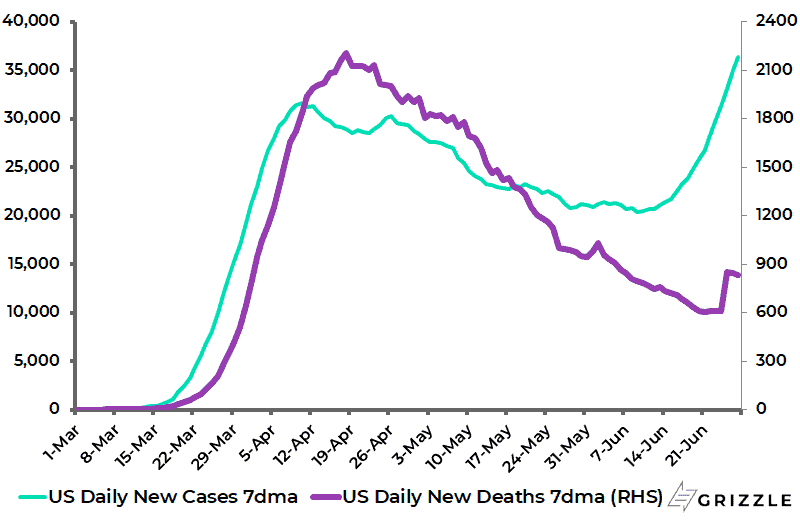

For now, the cases are rising again in America.

The 7-day average daily new cases in America have risen by 72% so far in June to 36,408/day.

But the encouraging point is that deaths are declining.

The number of daily new deaths in America is now 62% below the peak reached in April.

US Average Daily New Cases and Deaths

If one explanation for rising cases is re-opening, another is increased testing.

As for the declining death rate, the hope must be that it signals the virus is becoming less virulent, as well as the fact that cases are rising amongst younger people who are less worried about getting infected for the understandable reason that they are much less at risk.

Meanwhile, monetary easing, combined with growing hopes of a V-shaped recovery, also explain why the US stock market has all but ignored the protests sweeping American cities in recent weeks.

But what does matter for the American stock market is how the protests affect, if at all, the US presidential election in early November.

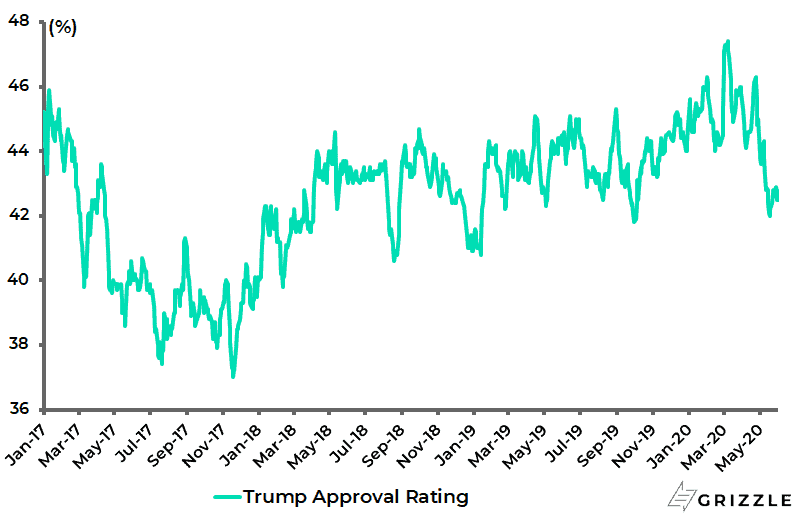

The law and order issue will give Donald Trump an opportunity to consolidate further the support of his base even though, for now, he continues to decline in the opinion polls.

Trump’s average approval rating has declined from a peak of 47.4% at the start of April to 41.6%.

President Donald Trump’s Average Approval Rating

When a Liquidity Event Turns into a Credit Event

Still, the critical swing factor in the election has to be the course of the virus, and the risk of a renewed spike.

For this reason, it is worth looking again at what happens if the base case here is wrong and Farr’s law does not apply, and the world is really destined for a “new normal” where every meeting is virtual and no one is traveling because of a renewed second wave.

Then, obviously, a liquidity event turns into a credit event since, while the Fed can encourage corporate bond investors to front-run the central bank’s anticipated purchases of such bonds, at a certain point it becomes relevant whether the company in question is generating any revenue.

Still even in the event of such a dire deflationary outcome, at a certain point, the negative impact of the virus on the economy and people’s livelihood caused by the lockdowns becomes a bigger negative than the disease itself, most particularly for people aged under, say, 50.

In this writer’s view, this issue kicks in big-time after three months of lockdown in the developed world and much quicker in the developing world where there are no welfare states and where young demographics make the lockdowns even more questionable from a cost-benefit analysis.

This is why India and Indonesia, for example, have both reopened their economies this month even though Covid-19 cases have continued to trend higher.

It is also why the view here is that economies will not be locked down again in the event of second waves, and that renewed outbreaks of Covid-19 will be managed at local levels. And the best way to do that is clearly contact tracing.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.