It has, of late, become increasingly relevant to talk less about the retreat from globalization and more about the increasing balkanization of the global economy.

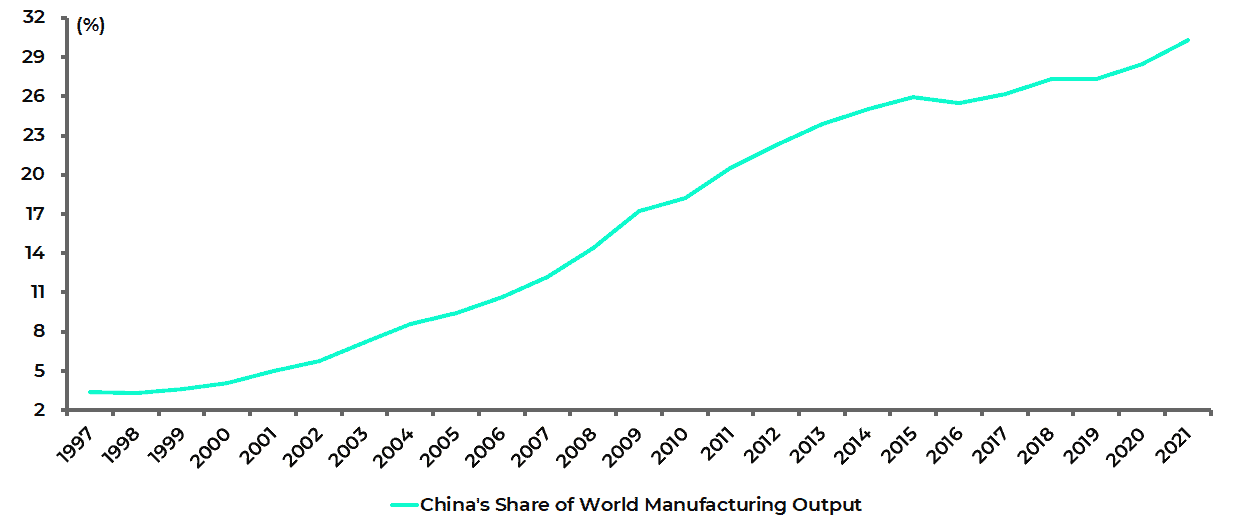

This trend is also encouraged by the growing desire to reshuffle global supply chains and reduce dependence on China which still accounted for 30% of world manufacturing output in 2021.

China’s Share of World Manufacturing Output

This used to be driven primarily by economic considerations, such as the increase in wage costs in China, but such considerations are fast being overtaken by geopolitical ones.

Semiconductors are the New Currency of Conflict

This is most dramatically the case in the semiconductor space with US$52.7bn subsidies now being offered by Washington to encourage semiconductor fabs to be built in America in spite of the significantly higher costs.

This is in addition to the US attempt to stop the selling of advanced semiconductors to China, first announced in October 2022 and discussed here previously (“The Shadow Semiconductor Wars Explained”, 23 November 2023).

Meanwhile, a further US attempt to isolate China came with the announcement at the end of February that companies who take the US chip subsidies will not be able to increase production in China.

The same trend is also evident in energy where the traditional environmentalist goal of promoting decarbonisation is also increasingly linked with energy security issues as a result, in part, of events in Ukraine.

Again America has led the way with its US$738bn so-called Inflation Reduction Act passed last August, including US$391bn in spending on climate and energy programmes.

This legislation, known as the IRA, offers up to US$7,500 per vehicle tax credits to American buyers of EVs which undergo final assembly in North America.

In order to comply for the tax break, it is also necessary that, starting this year, at least 50% of vehicle battery components must be manufactured or assembled in North America and that at least 40% of their critical minerals are sourced from the US or from countries which have free trade agreements with the US.

These thresholds will be increased gradually to 100% by 2029.

It is likely to promote tit for tat retaliation with the Eurozone now seemingly destined, sooner or later, to come up with its own version of the IRA, potentially running into the trillions.

Such a plan will raise the issue of how it is funded though the current political composition of the German government, with its obsession with all things green, will clearly favour such a policy.

EU Internal Market Commissioner Thierry Breton is calling for a plan called the “Clean Tech Act” which would open the door to aid for clean tech products like solar panels and batteries.

He also wants to adjust state aid rules to help various industries grapple with energy costs and counter US subsidies.

Meanwhile, the president of the European Commission, Ursula von der Leyen, said in a speech at the annual gathering of the Davos mob on 17 January, and also reiterated in her address at the plenary session of the European Parliament on 18 January, that the European Commission’s answer to the IRA will be a so-called “Green Deal Industrial Plan” which will make Europe “the home of clean tech and industrial innovation on the road to net-zero”.

To help make this happen, the EU will put forward a new “Net-Zero Industry Act” to simplify and fast-track permitting for new clean-tech production sites.

Indeed the European Commission presented on 1 February its proposal for a “Green Deal Industrial Plan for the Net-Zero Age”, which outlines the actions that the Commission intends to take to stimulate investment in the “net-zero industry” within the EU.

A New Global CAPEX Cycle

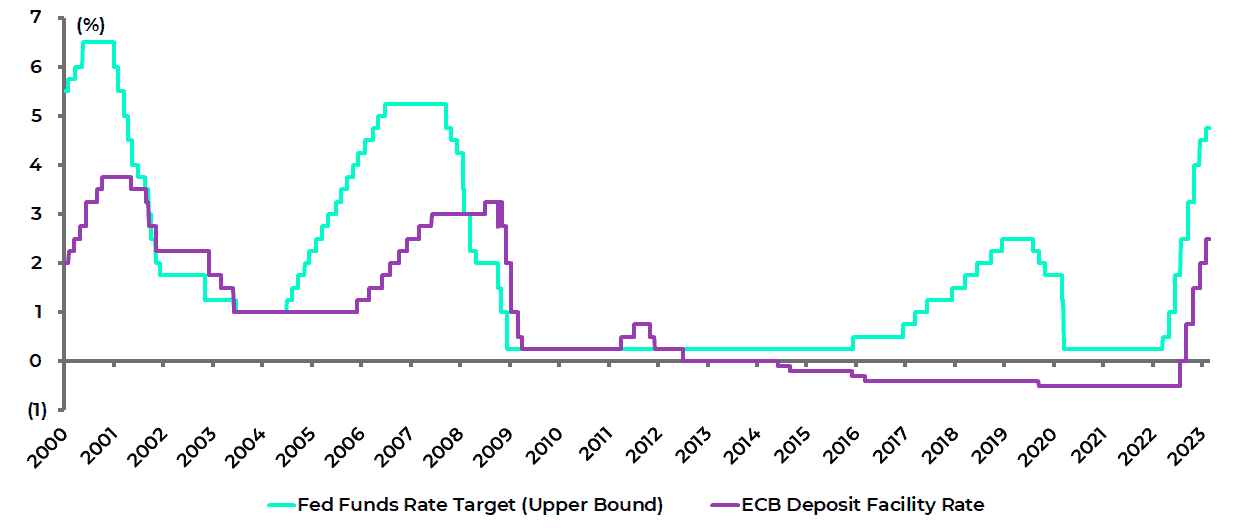

The macroeconomic consequence of all of the above is that the desire to re-shuffle global supply chains, as well as to promote what can be termed economic greening, will become drivers of a new global capex cycle, the political pressures for which will only grow if there is a recession in the G7 world induced by the monetary tightening cycle which kicked off only a year ago, with the Federal Reserve having now raised rates by 450bp and the ECB by 300bp, with a further 87bp and 150bp of tightening currently assumed by money markets.

Fed Funds Rate and ECB Deposit Facility Rate

But this capex cycle will be fundamentally inflationary in nature, given that politically driven dirigiste agendas are driving it, in stark contrast to the deflationary impact of globalization which was driven primarily by free market forces.

This writer’s preference is for free market forces. But that is not the current direction of travel, at least in the G7 world.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.