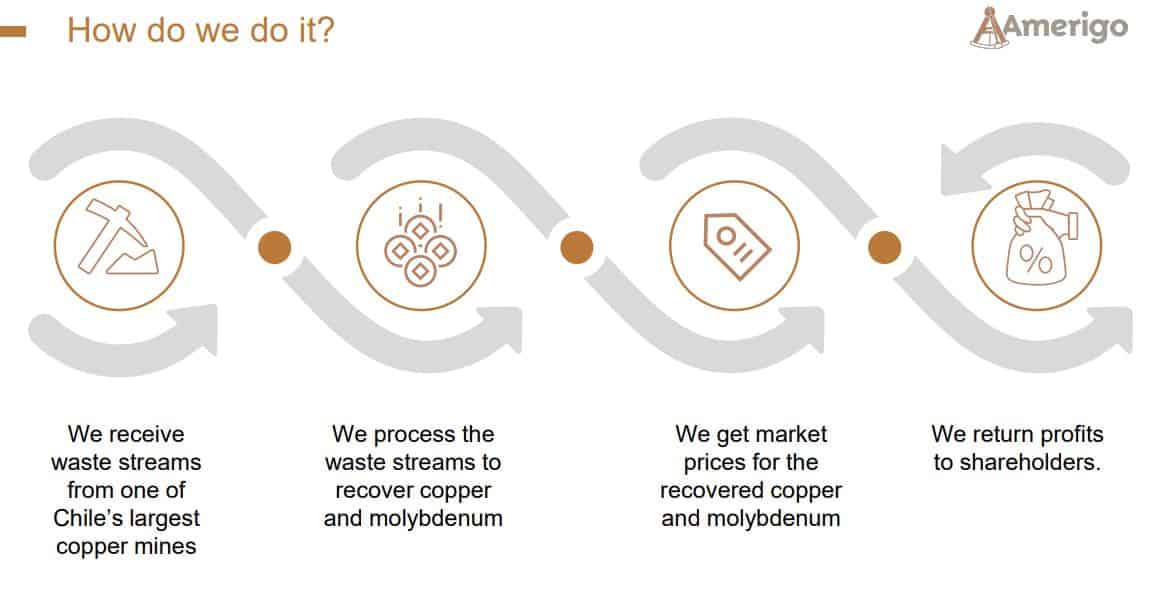

Amerigo’s Unique Business Model

Amerigo produces copper without a copper mine, they recover copper from tailing waste streams at Chile’s largest copper mines.

They process the waste to recover the copper along with molybdenum – the concentrate product they produce is the same concentrate produced by traditional mines.

Amerigo is able to produce critical metals without traditional mining.

Amerigo is the only company producing copper in this unique way at this scale, they produce the same quantity of metal as a midsize copper company.

The Sustainability of Amerigo’s Operations

The copper is being recovered from the waste stream, the copper is sitting there already and would be wasted if Amerigo didn’t process it.

They get the waste stream to their plant through gravity, so there isn’t a lot of transportation involved – they function as a mine-less operation.

Additionally, all their operations are powered by green energy.

Since Aurora took over the company 2 years ago Amerigo has rebranded to highlight the clear sustainability characteristics of the company.

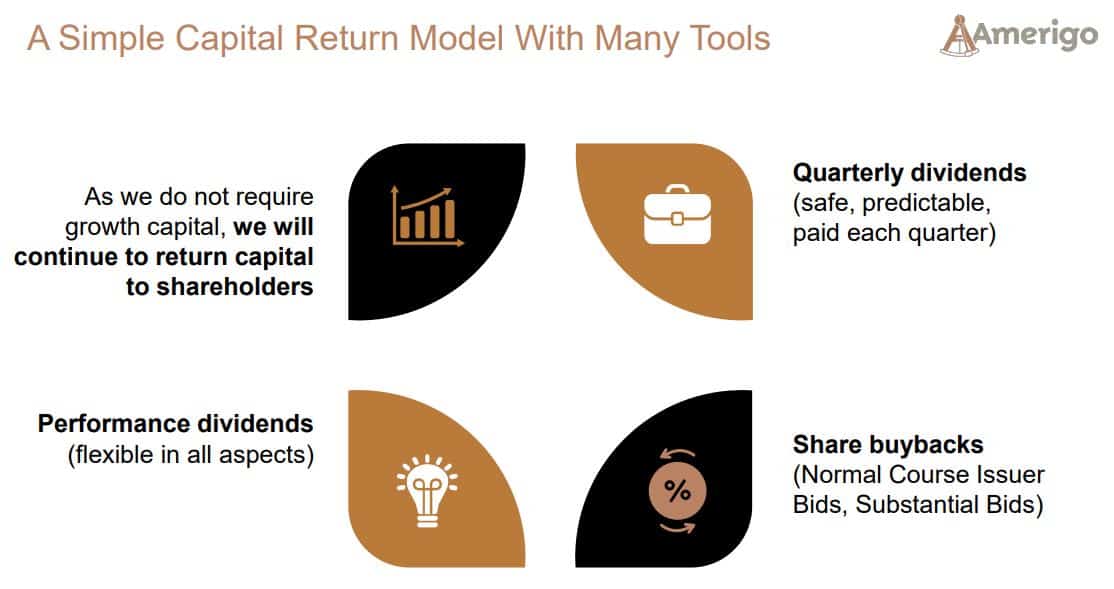

Amerigo’s Dividend Yield (12%) Proposition to Investors

Amerigo is in a sweet spot of their corporate development where they don’t have to invest a significant amount towards capex, they are at a mature stage.

The company has three tools they utilize for their capital return policy:

- Quarterly dividend – it’s set to be a reliable and protected dividend

- Share buybacks – AMG has bought back 10% of their shares outstanding in the last year

- Performance dividend – haven’t deployed yet, in periods of high copper prices they will distribute.

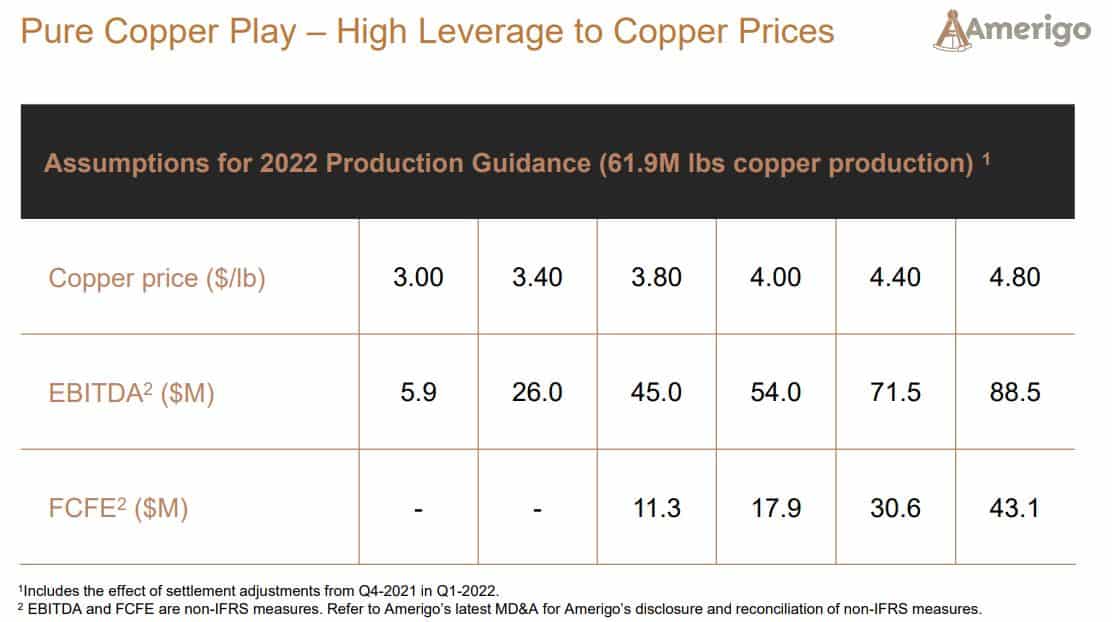

Amerigo’s Cash Flow Leverage to Copper Prices

For 2022 guidance producing 62M pounds of copper production, the leverage is significant – the leverage of a $1 in the copper price from 3.80/lb to 4.80/lb equates to an increase from 11M to 43M of free cash flow.

They’ve entered 2022 with a strong balance sheet, they can withstand a period of sustained lower copper prices – protect the base dividend and to have the ability to deploy additional cash to shareholders when the copper price is strong.

Amerigo Leverage to Spot Copper Prices

Amerigo – Mining Company or Water Treatment Company?

The core business proposition is a better analogy with a wastewater treatment company.

The real differentiator is that a wastewater plant gets a flat fee, while Amerigo gets full exposure to market prices – a utility on steroids.

Amerigo’s Mine Life

The company currently has a contract that runs till 2037, it originally ran to 2021 and was extended. This is a contract that has a high likelihood of being renewed at 2037.

The life of mine for Codelco’s El Teniente from where Amerigo gets their waste stream is 2082.

How the Company Manages Water Risk

Chile has been facing drought conditions for a number of years; Amerigo has the benefit that most of the water they receive is in water contained in the waste material.

The company also has to be intelligent on how they use the water, water thickeners allow’s Amerigo to circulate and reuse much of the water they use.

Amerigo can also store water on site, they currently have on storage over 5 million cubic meters of water.

To learn more about Amerigo Resources visit the company’s website HERE

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.