There was an interesting development in the US stock market in April.

There were significant net outflows from US domestic equity ETFs for the first time this year, though inflows have resumed since.

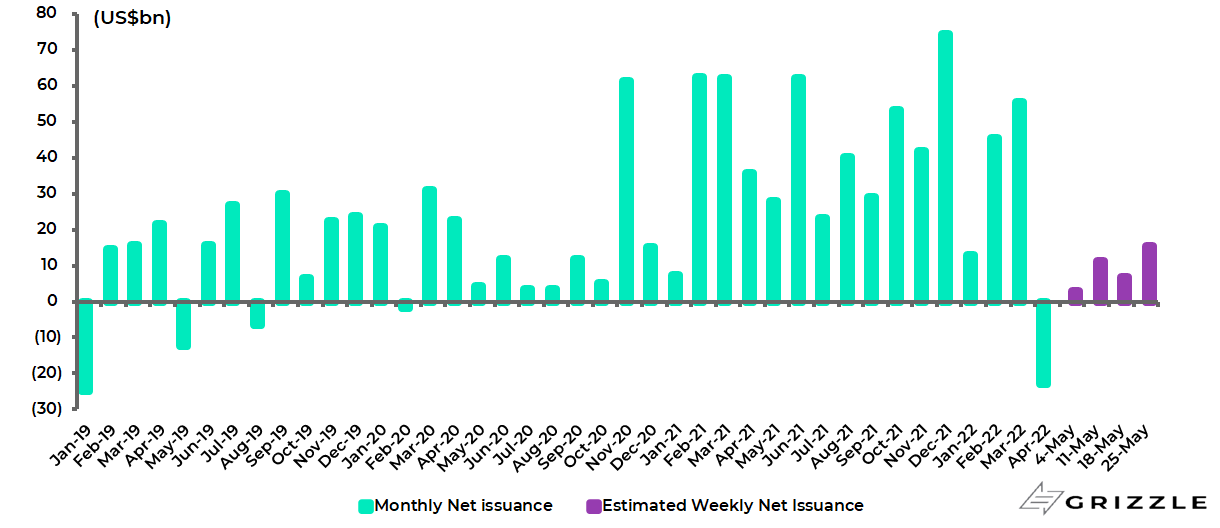

US domestic equity ETFs recorded a net outflow of US$23.1bn in April, the biggest monthly outflow since January 2019, according to the Investment Company Institute.

But they have since recorded estimated net inflows of US$36.3bn in the first four weeks of May.

US domestic equity ETF flows

Data up to the week ended 25 May 2022. Source: Investment Company Institute

And because many of the ETFs own the same big cap stocks, it is likely to lead to significant declines in the previous market leaders.

There are for example, 14 ETFs traded in America indexed to the S&P500 with total assets under management of US$1.1tn at the start of this year.

Admittedly, this process is already well underway with Netflix down 73%, and the company formerly known as Facebook down 50%, at their worst points this year.

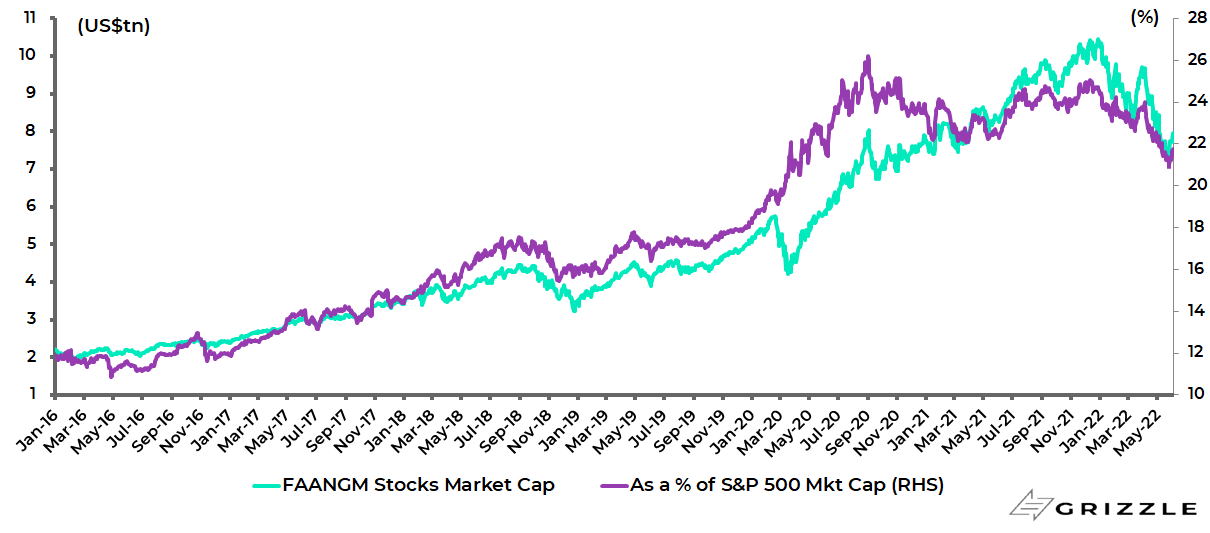

The above market action merits renewed focus on the updated chart below of US Big Tech stocks as a percentage of S&P500 market cap, but also of the Big Tech stocks in market cap terms.

Thus, the six Big Tech stocks, including the five FAANG stocks and also Microsoft, now account for 21.5% of the S&P500 market cap, down from 24.4% at the end of 2021 and a peak of 26.2% on 1 September 2020.

While the combined market cap of these stocks has declined by 26% from the peak of US$10.45tn on 27 December 2021 to US$7.73tn.

US Big Tech stocks’ market cap and share of S&P500 market cap

Source: Bloomberg

Two Quarters of Losses Could Trigger ETF Major Redemptions

For this will constitute a major psychological blow to the long-entrenched “buy the dip” mindset.

And clearly, the more equities fall, particularly widely owned equities like the FAANGs, the more it has a macroeconomic impact given the significant amount of US household wealth invested in listed equities.

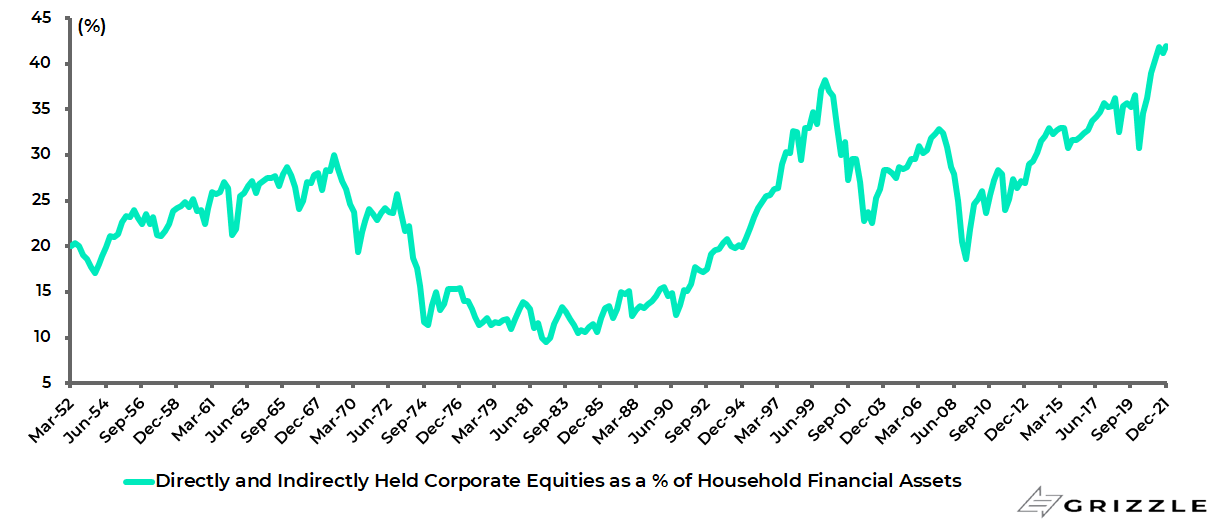

Directly and indirectly held corporate equities accounted for a record 41.9% of US households’ financial assets at the end of 2021.

Directly and indirectly held corporate equities as % of US households’ financial assets

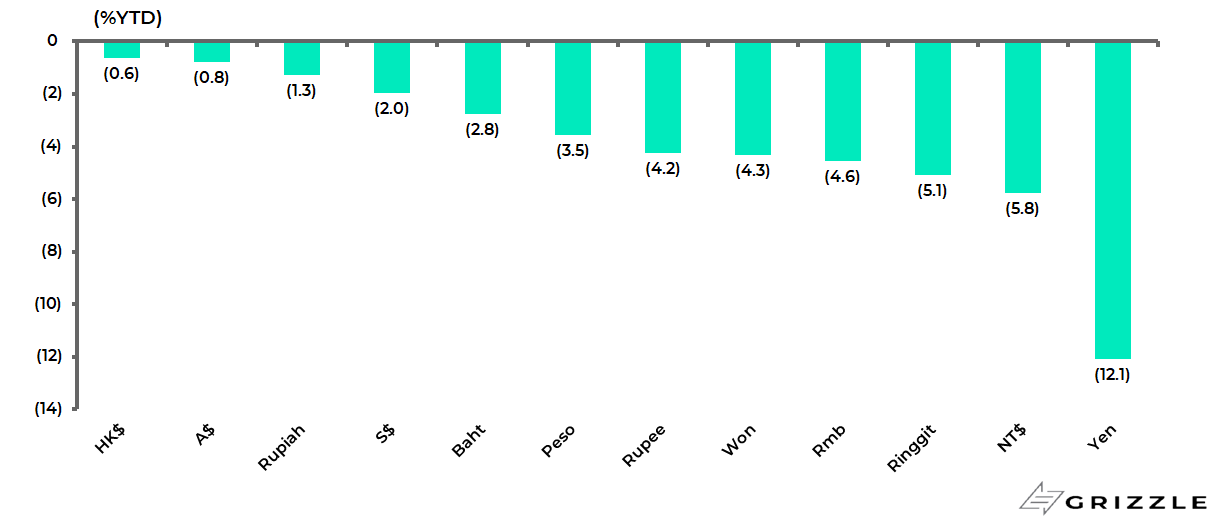

Why Hasn’t The Dollar Strengthened More vs Asian Currencies?

Meanwhile, it has been interesting to this writer that the US dollar has not rallied even more this year given the rhetorical hawkishness of the Federal Reserve with the real dollar strength against the yen in an Asian context. The yen has depreciated by 12.1% against the US dollar so far in 2022.

Asian currencies against the US dollar (Year to date 2022 performance)

Still, it is the case that the increased market focus on the negative risk to China growth caused by China’s continuing Covid suppression policy has now caused the mainland authorities to allow some renminbi depreciation, a trend also influenced by net foreign outflows from China’s bond market in the past three months to April.

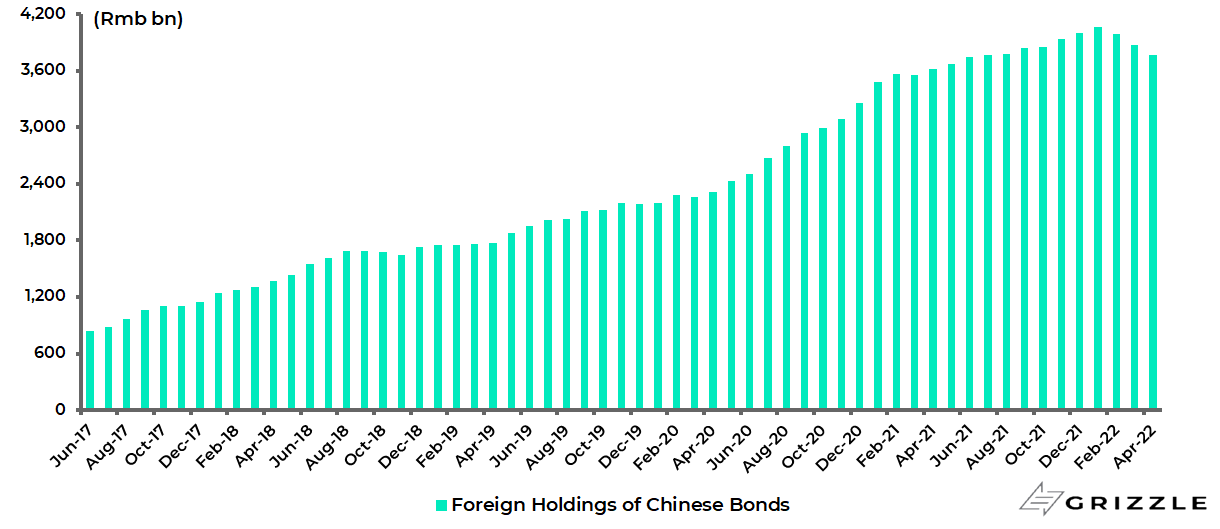

Foreign holdings of China bonds have declined by Rmb301bn or 7.4% from the peak of Rmb4.07tn at the end of January to Rmb3.77tn at the end of April.

Foreign holdings of China bonds

As a result, the renminbi has depreciated by 4.4% since 18 April.

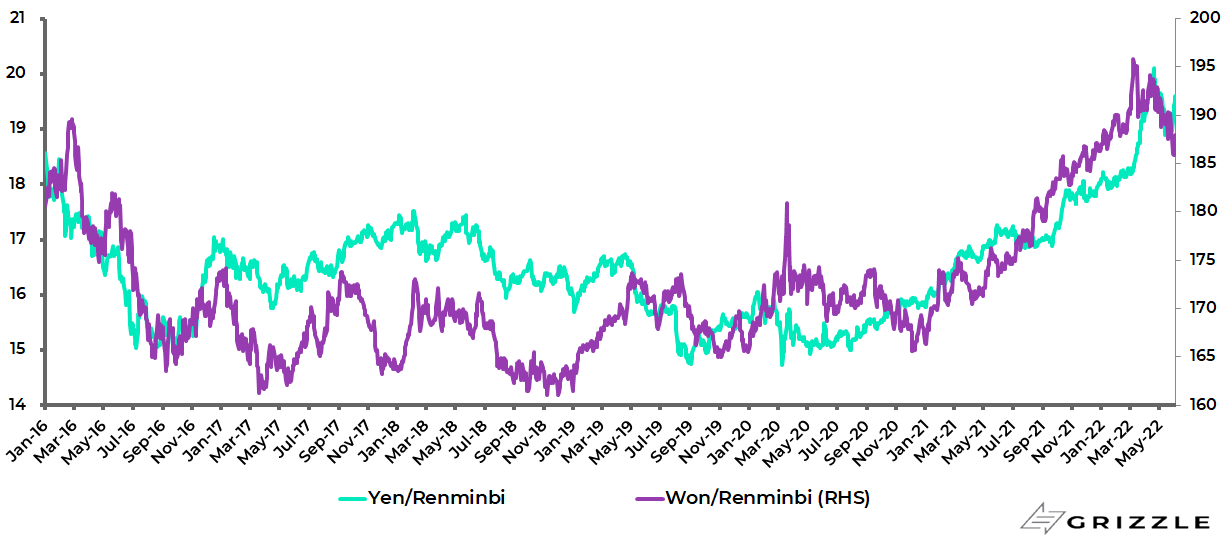

This is a natural market-driven development given that China is easing at a time when the Fed is tightening; though another influence on Beijing policymakers will undoubtedly be that the yen and the won had by mid-April depreciated by 22% and 14% respectively against the Chinese currency since the start of 2021.

Yen and won against the Renminbi

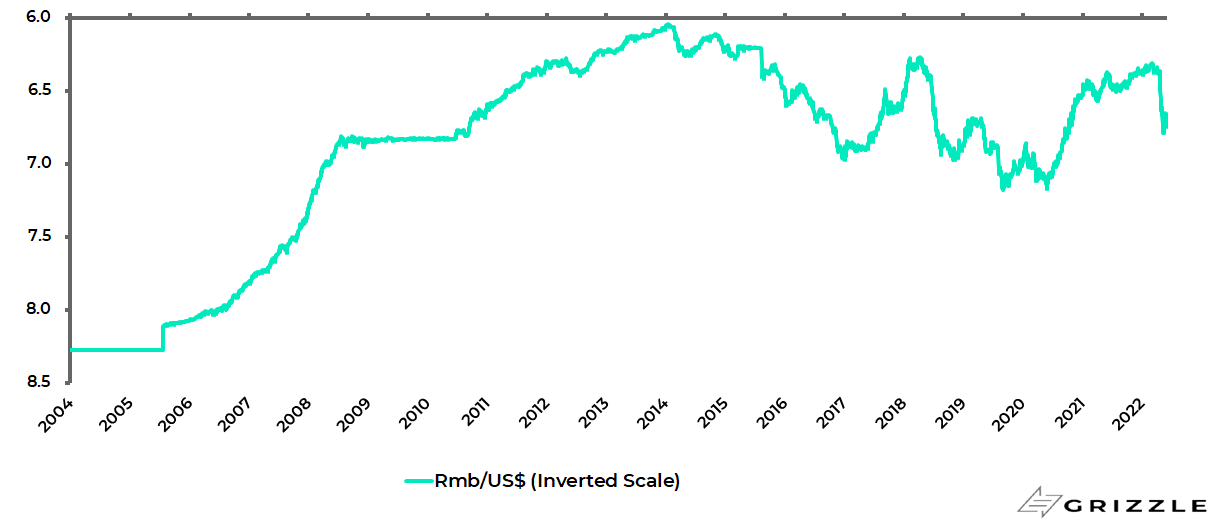

Still, the base case is that this renewed weakness in the renminbi will be a pause to refresh not the beginning of a major renminbi devaluation.

Indeed the renminbi is likely to depreciate by less than the two previous periods of depreciation when the Chinese currency declined by 13.3% against the US dollar between 2014-2016 and by 13% between 2018-2020.

This is in the context of the 24% appreciation since July 2005 when the Chinese currency was moved off its previous peg.

Renminbi/US$ (inverted scale)

Remember that China revalued the renminbi by 2% against the US dollar on 21 July 2005 to Rmb8.11/US$ and moved to a “managed floating exchange rate regime based on market supply and demand with reference to a basket of currencies”, to quote from the PBOC’s official statement at the time.

It should also be remembered that the last two periods of moderate renminbi depreciation were marked by excitable forecasts of a renminbi collapse made by the usual suspects.

What Comes Next for Chinese Money Policy?

Meanwhile, the PBOC has made various moves to ease monetary policy further in recent weeks, including cutting mortgage rates.

Such moves may be understandable but they are almost irrelevant in terms of the ongoing negative impact on growth of China’s Covid suppression policy.

In this respect, the technocrats continue to try to mitigate the negative consequences of the Covid suppression policy, now more clearly than ever identified with President Xi Jinping.

The problem remains that this suppression policy does not seem practical in the context of the highly infectious Omicron, even if it worked for the Delta variant.

Yet China continues to prioritise mass testing over vaccinating the elderly which, so far as this writer is concerned, seems the wrong policy.

About 36% of Chinese aged over 60 have still not had the required three doses of the Sinovac or Sinopharm vaccines which is what is required to make them effective.

The technocrats’ continuing efforts to support growth, while entirely understandable in the circumstances, reflect evidence of a bifurcated central government in Beijing which this writer has to admit to not having seen before.

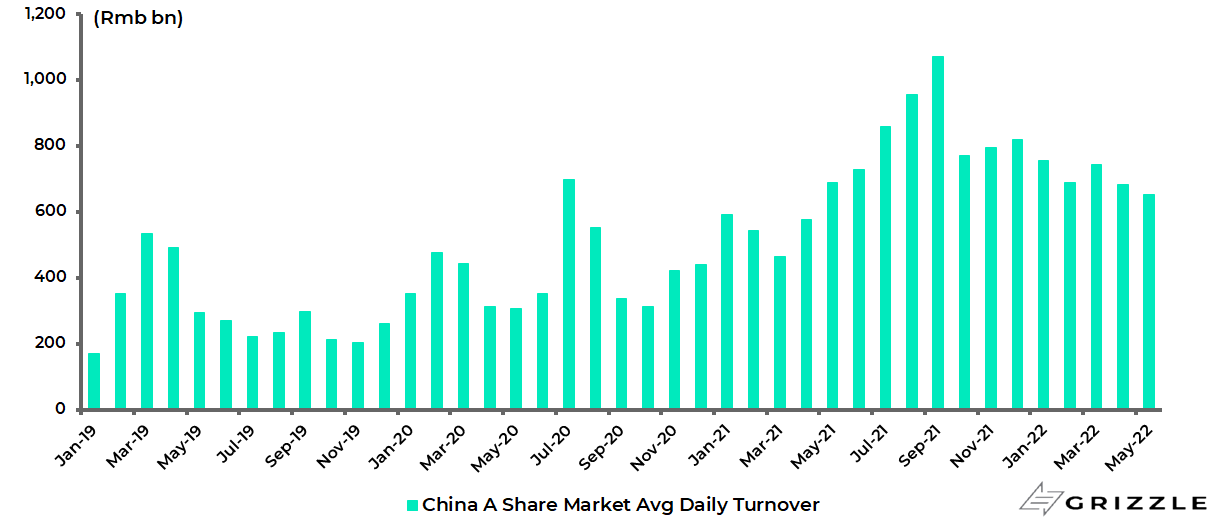

Meanwhile, the risk-off sentiment triggered by the continuing Covid suppression policy, and related lockdowns, is evident from the collapse in trading volumes in the A-share market and also the renewed decline in margin debt in the context of a CSI 300 Index which is down 17.2% year-to-date.

Average daily turnover in the A share market has declined by 39% from Rmb1.07tn in September 2021 to Rmb653bn in May.

China A-share market average daily turnover

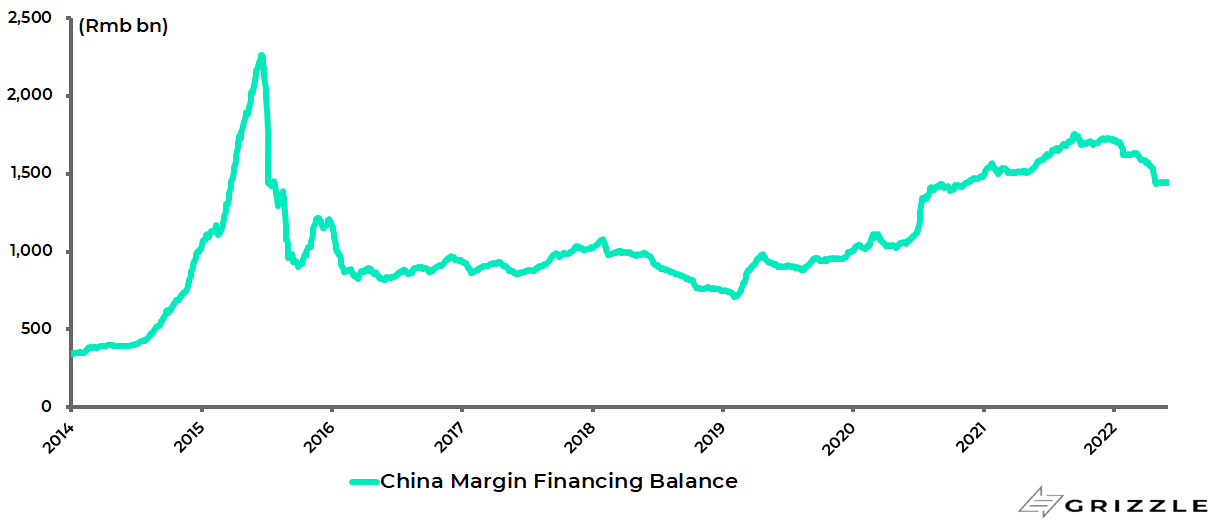

While China’s margin financing balance has declined by 18% from the recent high of Rmb1.76tn reached in September to Rmb1.44tn.

China margin debt balance

Meanwhile, as the lockdowns have proliferated, downward earnings revisions have risen.

This is why the only thing that matters in Chinese equities in the short term is the Covid suppression policy, in terms of rolling lockdowns, and the related path of the pandemic.

Clearly, any sign of a real relaxation in the policy would likely trigger a melt-up in Chinese equities.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.