Attention has returned to the conflict in Ukraine with the launch of the Russian offensive in the Donbas area of Eastern Ukraine.

As hopes of a negotiated peace agreement have faded in recent weeks, expectations have grown for a protracted drawn-out conflict.

In market terms, oil has bounced as deal hopes have faded while the territorial claims on both sides have hardened, most particularly on the Ukrainian side.

Meanwhile, oil has also got a boost from growing expectations that Europe will seek to ban Russian oil imports, if not yet gas imports.

This follows a ban on Russian coal announced in April which will be phased in over four months.

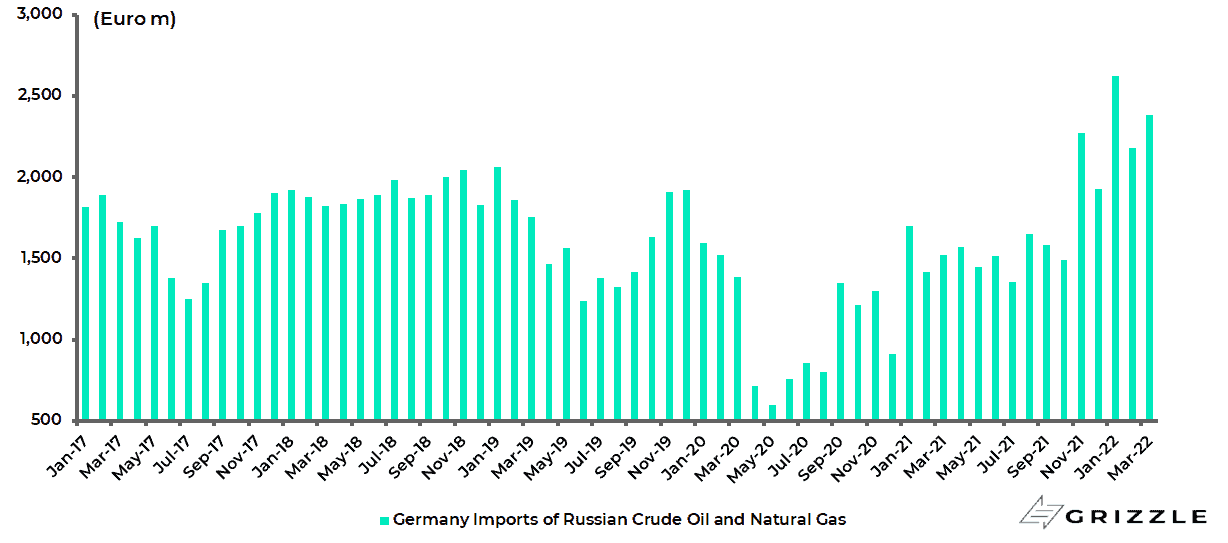

Russian oil is not insignificant for Europe since it provided the EU with a quarter of its oil and oil petroleum product imports in 2020 with Germany obtaining 34% of its oil from Russia.

Still, the really decisive issue is gas where Germany’s dependence on Russia is much greater at 55%.

In the long run the direction of travel is clear in terms of Europe becoming much more dependent on American LNG but that will take several years to happen given the need to build the necessary LNG terminals.

But in the near term, a renewed intensification of the military conflict has the clear potential to lead to growing pressure on Europe, and in particularly on Germany, to ban Russian gas also.

Remember Germany is paying Russia €80m a day for its oil and gas.

German imports of crude oil and gas from Russia totaled €7.2bn in January-March.

German imports of Russian crude oil and natural gas

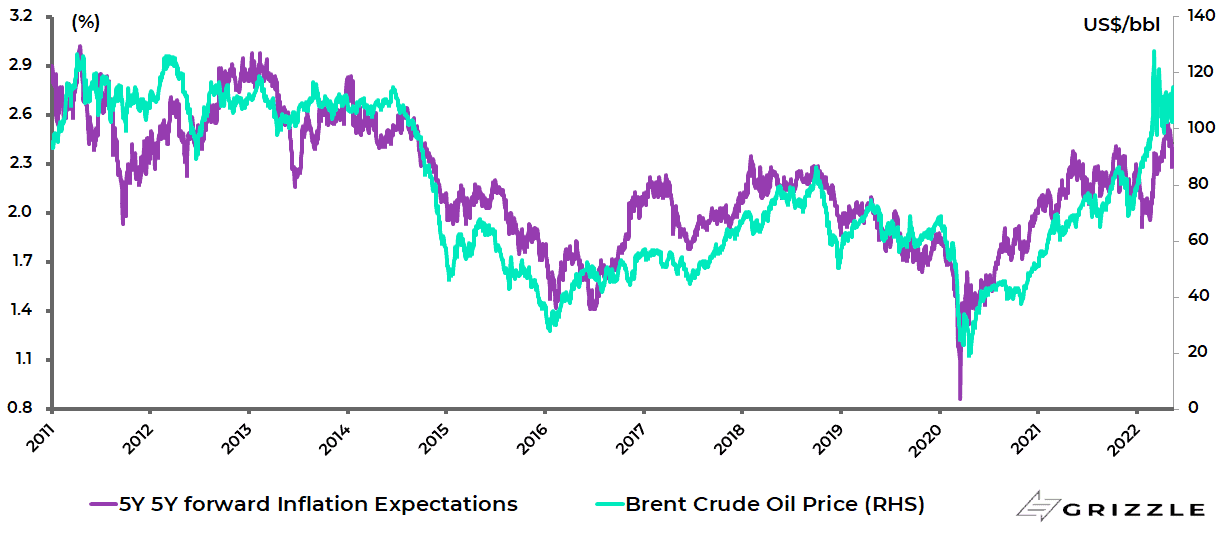

Oil and Inflation Expectations are Fast Friends

The above means it makes sense to remain constructive on energy stocks while investors still need to keep in mind the long-term correlation between the oil price and US five-year five-year forward inflation expectations.

A further surge in the oil price has the clear potential to make the Fed’s monetary tightening cycle even more challenging.

Brent crude oil price and US five-year five-year forward inflation expectation rate

Financial markets remain focused on such matters as the Federal Reserve tightening cycle and the fight for Donbas.

This is entirely understandable.

Still, there is an important issue in Asia.

How Much Growth Will China Sacrifice for COVID?

That is the extent to which China is willing to sacrifice growth in its continuing effort to suppress the Omicron variant.

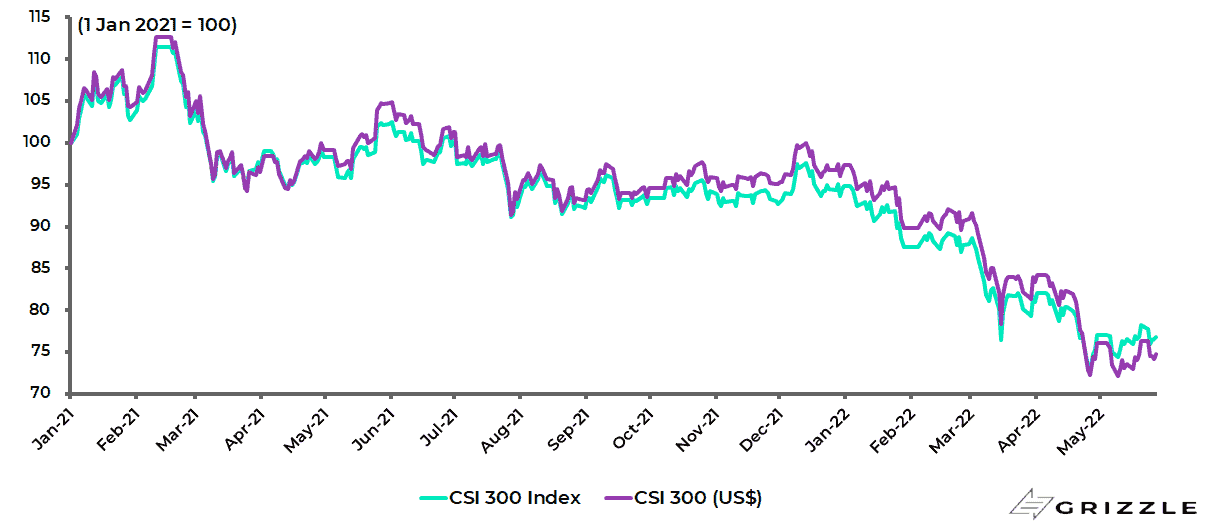

For now there seems to be no willingness to abandon the policy, closely identified with Chinese President Xi Jinping, which is why the Chinese stock market has remained under negative pressure despite a growing number of easing policies.

The CSI 300 A-share Index is down 19% year to date in local currency terms and 23.2% in US dollar terms.

China CSI 300 Index

Source: Bloomberg

The official line on Covid was made crystal clear in an article in the Study Times published in April by Ma Xiaowei, director of the National Health Commission, which called on China to stick with the policy and oppose “erroneous” thoughts of “coexisting with the virus”.

Ma further commented that an abandonment of preventative measures and a relaxing of “treatment” risked overwhelming China’s medical facilities given the country’s large population.

That line was further reconfirmed at the Politburo meeting on 5 May (see Xinhua News Agency Chinese article: “中共中央政治局常务委员会召开会议 习近 平主持会议”, 5 May 2022).

The meeting of the Politburo Standing Committee of the China Community Party, chaired by Xi Jinping, reiterated that China will “unswervingly adhere to the ‘dynamic clearing’ policy and resolutely fight against any words or actions that distort, doubt or deny China’s anti-COVID policy”.

If this is the official line it certainly contrasts with the article on Weibo written by Zeng Guang, the former chief epidemiologist of the Chinese Center for Disease Control and Prevention back on 28 February (see Global Times article: “West’s ‘coexistence with virus’ should not be standard for China’s anti-epidemic strategy: Top Chinese epidemiologist”, 1 March 2022).

This called for a road map for “Chinese-style coexistence” with Covid to be presented at an appropriate time in the near future.

Still, it is now clearly the case that, if there have been officials calling for such a policy, they have lost the argument.

It also means that the Covid suppression policy is now identified even more closely with Xi.

This will not matter if the scenes seen in Shanghai over the past two months are not repeated nationwide.

For then it will be possible to blame local officials in the city of 25m for not implementing Xi’s policy properly.

It is also the case that it is widely believed that Shanghai is not Xi’s favourite city.

Still Xi is taking a risk with continuing to pursue such a policy since it assumes the highly infectious Omicron can be controlled.

This is a major assumption, to put it mildly, even taking into account the Communist Party’s undoubtedly formidable powers of control.

A loss of control of Omicron, combined with the economic damage caused by the lockdowns, would constitute a double whammy negative for China; and in the Chinese cultural context a loss of face for the leadership five months ahead of the 20th National Congress of the Chinese Communist Party when Xi is due to be reappointed.

It is also the case that the continuing lockdowns will serve to extend the Omicron cycle in China whereas in India, for example, the Omicron “boom-bust” cycle occurred over a period of just eight weeks.

Can China Afford to Lose Control of Omicron?

There has been, unsurprisingly, growing focus on the economic damage done by the lockdowns over the past month and more.

China’s Ministry of Industry and Information Technology, for example, said in April that it had identified 666 companies in Shanghai in the semiconductor, automobile, equipment manufacturing and biomedicine sectors as priority firms that needed to resume work and production.

Similarly, Vice Premier Liu He, Xi’s chief economic technocrat, called on 18 April for the issuance of sufficient national unified travel passes to ease severe logistical problems caused by truck drivers being told to quarantine for 21 days if they came from areas categorised as risky.

To enable such a policy, Liu suggested that results of so-called nucleic acid tests (i.e. PCR tests) issued within 48 hours should be recognised across the country, and that authorities should not restrict logistics workers’ travel on the grounds of waiting for test results.

While seemingly sensible, such policies are ultimately seeking to mitigate the adverse practical consequences of the Covid suppression policy itself.

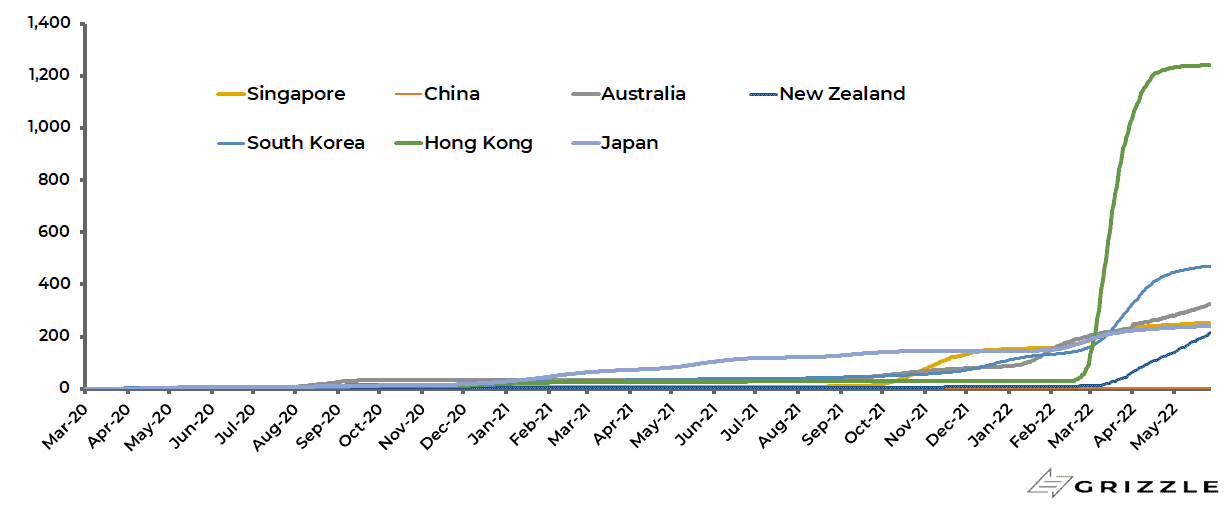

Yet the danger of relaxing the Covid suppression policy, or for that matter losing control of Omicron, is clear from the chart below showing that cumulative Covid deaths per 1m of population in Hong Kong surged from 30 in February to 1,241 on 27 May, compared with 3.6 in mainland China.

This is apparently the highest Omicron death rate in the world.

Yet China has, like Hong Kong, failed to prioritise vaccinating the elderly.

A total of only 63.6% of Chinese aged over 60 have had the required three doses of the Sinovac or Sinopharm vaccines as of 26 May, which is what is required to make them effective.

A repeat of Hong Kong’s experience would lead to 1.7m deaths in China adjusted for the differences in population.

Cumulative Covid deaths per million of population in Asia

Meanwhile, it is clear that the economic impact of Covid suppression in China, in terms of depressing demand, means that the oil price is lower than it otherwise would be.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.