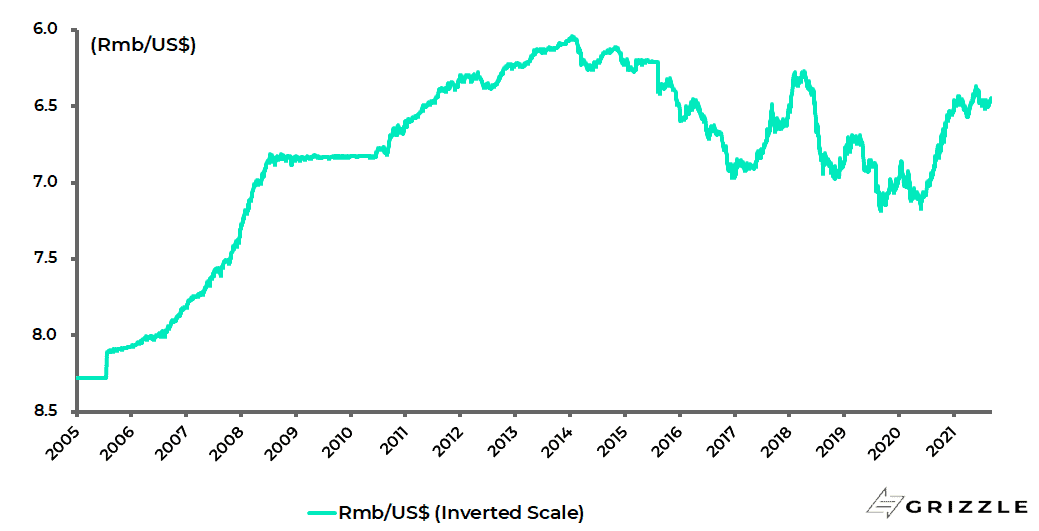

The Chinese renminbi remains in an upward trend against the US dollar, even though the pace of appreciation has slowed markedly this year.

The renminbi has risen by 1.3% against the US dollar year-to-date, following a 6.7% appreciation in 2020.

Renminbi/US$ (inverted scale)

The currency has certainly not yet been destabilised by the ongoing turmoil as regards the regulatory driven sell-off in Chinese internet stocks, many of them still listed in New York, recently discussed in this column (“The US Listed Chinese ADR is Dead, Invest in the Mainland Instead”, 2 September 2021).

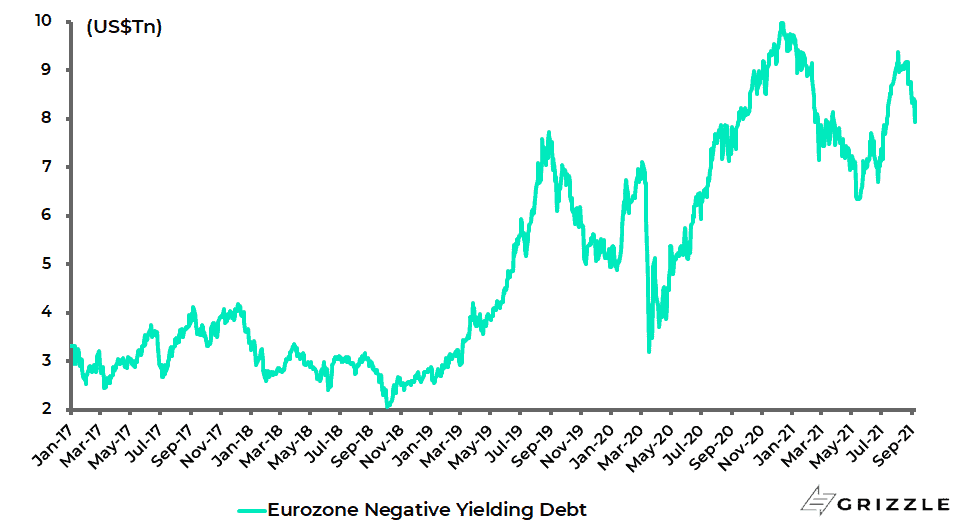

It is certainly the case that the Chinese leadership continues to view Beijing’s hard money policy as in stark contrast to the currency debasement policies that prevail in the G7 world, as signaled most dramatically by the continuing near record amount of negative yielding debt in the Eurozone.

The total amount of Eurozone debt with negative yields surged to US$9.38tn in early August, the highest level since mid-January, compared with the peak of US$9.98tn reached in mid-December last year; though it has since declined to US$8.22tn.

Eurozone negative yielding debt

If the US Keeps Hurting the Dollar, China Wants Another World Currency

In this context, it should be remembered that China has been consistent in criticising America’s unorthodox monetary policy ever since former Federal Reserve chairman Ben Bernanke first launched quantitative easing back in late 2008.

This prompted then PBOC Governor Zhou Xiaochuan to write a paper published by the Bank for International Settlements in March 2009 calling for a new international currency system based on the Special Drawing Rights (SDR) and not the US dollar (see BIS article: “Reform the international monetary system” by Zhou Xiaochuan, 23 March 2009).

The SDR is an interest-bearing international reserve asset created by the IMF.

It is now based on a basket of international currencies comprising the US dollar, yen, euro, sterling and renminbi.

The renminbi joined the SDR basket on 1 October 2016.

China Thinks the US Will Blink First on Tariffs

This is why it was interesting to read a report of comments made recently regarding the American economy, and its dependence on China, by Jin Canrong, an influential academic economist at China’s Renmin University in Beijing (see Asia Times article: “Will China bail out Biden?” by David Goldman, 31 July 2021).

They are interesting because they reflect what this writer has been told mainland technocrats in China think about the American economy in the light of the massive Covid triggered monetary and fiscal stimulus.

That is that America has entered an inflationary period and that the strong renminbi will add to this inflationary pressure.

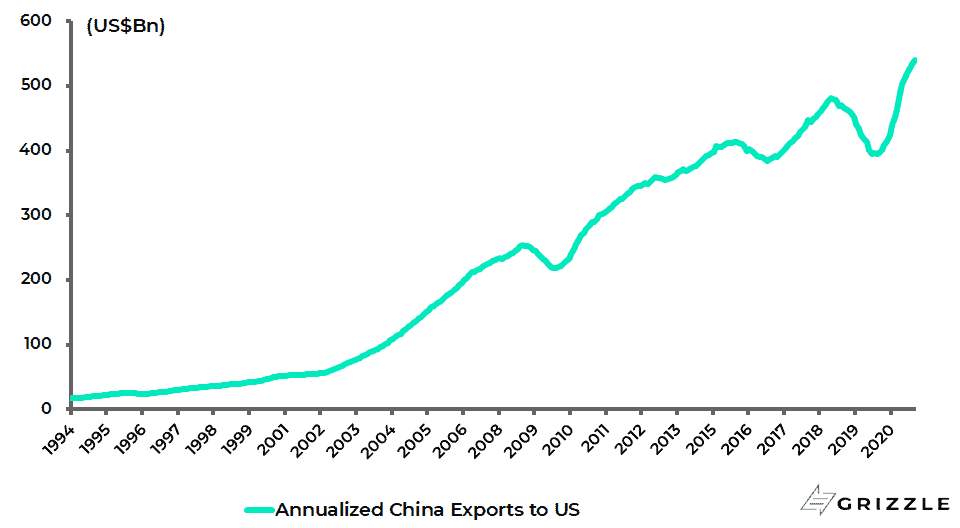

Professor Jin Canrong highlighted the continuing dependence on Chinese imports in an environment where US consumer demand has been stimulated by fiscal and monetary stimulus.

Total imports from China were running at an annualised US$540bn as at the end of August.

Annualised China exports to the US

He went on to argue that strong demand for Chinese imports, in the context of the strong renminbi, will aggravate inflationary pressures in the US.

But Jin makes another interesting point.

This is that this trend will lead to pressure to abolish the Trump administration’s tariffs on Chinese goods which have made them more expensive for American consumers.

Indeed Jin cited a comment made by US Treasury Secretary Janet Yellen about how tariffs on Chinese goods had hurt American consumers, as they obviously have.

On this point, Yellen said in an interview with the New York Times in mid-July: “Tariffs are taxes on consumers. In some cases it seems to me what we did hurt American consumers, and the type of deal that the prior administration negotiated really didn’t address in many ways the fundamental problems we have with China” (see New York Times article: “Yellen says China Trade Deal Has ‘Hurt American Consumers’”, 16 July 2021).

Whether Jin is right, and he could well be, it is interesting that this is what Beijing thinks as it will shape the Chinese leadership’s policy.

It is also interesting that Jin is advising the Chinese leadership to keep Sino-US relations “combative without breaking down” with a decision in Washington, say to drop the Trump tariffs, creating room for a possible rapprochement.

This is certainly possible.

Still the risk, with the bilateral consensus against China so entrenched in Washington, is that President Joe Biden will feel unable to look soft on China in the run-up to the November 2022 Congressional elections even if those elections are still 14 months away.

Easy Money Fed Policies are Largely Benefitting the Rich

Meanwhile, there continues to be criticism of the Federal Reserve, concerns shared by this writer, about the role monetary policy has played driving wealth inequality, via asset price inflation, since the original adoption of quantitative easing.

Clearly, this argument is not accepted by the Fed.

Still, this writer was reminded of the continuing role played by the Fed, in terms of stimulating asset price inflation, by an article on the second-quarter results of four major American banks (see Financial Times article: “US lenders offer a tide of ‘cheap money’ to the wealthy”, 26 July 2021).

The main point of interest is that the share of total loans made by the wealth management arms of JPMorgan Chase, Bank of America, Citigroup and Morgan Stanley accounted for 22.5% of the four banks’ total loan books at the end of last quarter.

In dollar terms they rose to more than US$600bn, up 17.5% YoY.

As a result, according to the same article, JPMorgan and Citi are now lending more money to a small number of ultra-high net worth clients than to their millions of credit card customers and clearly credit card borrowers are paying way higher rates.

The average interest rate on a US bank credit card is still 16.2%.

Meanwhile, from the standpoint of the wealthy, borrowing against potential illiquid assets makes perfect sense since it can be very tax efficient.

For example, it avoids paying high capital gains tax on the sale of an asset. Non-American readers may not know that, in Democrat-governed states like California and New York, federal and state capital gains tax combined on long-term capital gains is 37.1% and 34.7%, respectively.

The above is an example of one of the many distortions created by 12 years of unorthodox monetary policy in America.

And in many respects it is even worse in the Eurozone after seven years of negative rates, with many wealthy private banking clients being paid to borrow.

Still, this writer would also add that it makes total sense for the wealthy to keep borrowing against their assets since the assumption has to remain that the G7 central banks will not be able to escape continuing unorthodox monetary policy and the obvious way to hedge resulting ongoing currency debasement is to own physical assets, be it equities, real estate or gold, or digitally scarce sources of value such as Bitcoin.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.