Delta Air Lines (NYSE:DAL) reported its second quarter fiscal 2020 results ended in June pre market today that dissapointed analyst expectations, causing shares to trade lower pre market.

The company generated $1.468B of revenue, above analyst estimate of $1.415B by 4%, but was down by 88% year over year.

Adjusted earnings per share were a loss of ($4.43)/sh, a 4% miss to consensus estimates of ($4.25)/sh by a margin of 4%.

The company’s EBITDA loss was a staggering -$4.023B, though still came in 45% lower than what the street was expecting.

Delta’s reported expenses were sightly above management’s expected value by 17%.

The only question investors need to answer is if Delta can afford to pay interest expense and other bills until the virus is a distant memory.

However, when considering the fact that the US has seen a surge in virus cases recently, it is uncertain that the economy may not reopen fully in the near future, which means Delta may not be able to operate back to its break even capacity.

Valuation Breakdown

As with cruise lines, and other companies in the travel/transportation sector, airline company revenues were decimated due to the pandemic. With a current system capacity of 15%, the loss of revenue is very significant for Delta Air Lines.

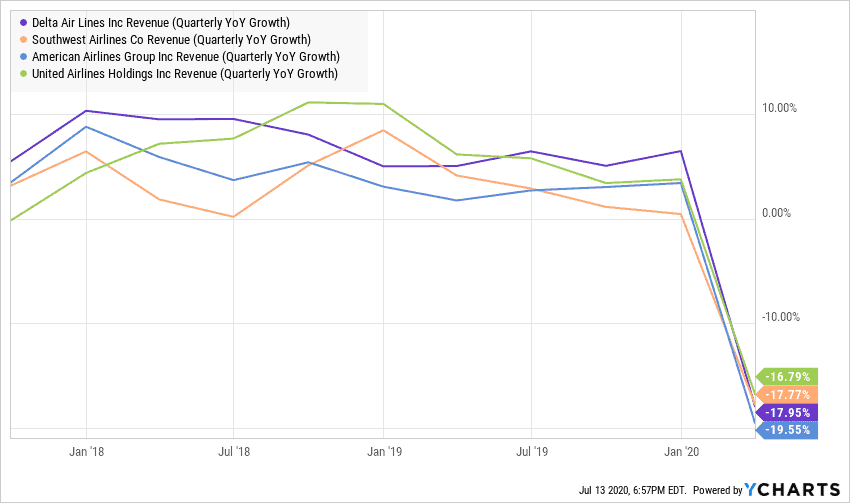

COVID-19 only hit in March and still these company’s reported significant declines in revenue last quarter.

This quarter’s earnings show us the industry is still hanging on for dear life.

As long as consumers are wary of flying, the industry has a capacity problem.

Revenue Growth is Down Big

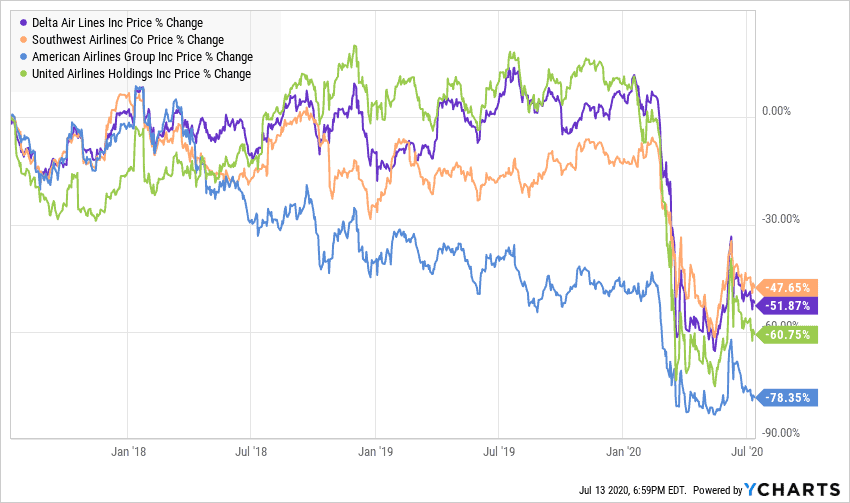

As a result of the industry woes, Delta Air Lines’ stock value along with its peers has declined by more than 45% since the beginning of the lockdown.

Airline Stock Price Performance

The limitation of travel for only essential needs, has forced Delta to borrow heavily.

Debt increased 39% from last quarter in order to finance operations.

Given that the company already had a very high Debt to EBITDA ratio of 49.2X in the previous quarter, the company is under considerable pressure to finance its debt obligations especially since EBITDA was not positive for the reported quarter.

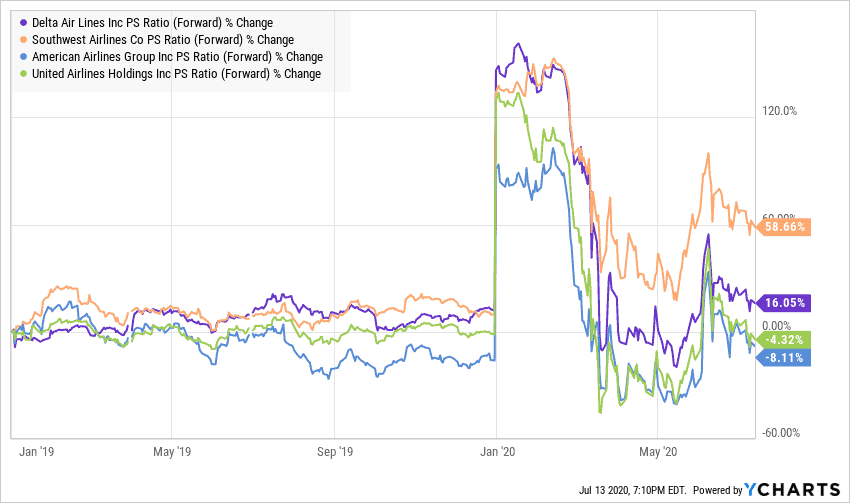

This concern is another reason as to why investors discounted Delta’s share price in the recent months as shown on the PS chart below.

According to the chart, Southwest Airlines’ share value trades at a higher premium compared to Delta. This is particularly because in comparison to both company’s previous quarter’s Debt to EBITDA ratio, Southwest’s ratio was around 50% less than Delta’s.

Southwest’s EBITDA margin at 4.75% was also more favourable than Delta’s EBITDA margin of 4.20% in that same quarter too.

Final Remarks

Although the company reported disappointing earnings results, it still managed to slightly beat management’s revenue target by 17% year over year.

Yet the company’s debt levels are a major concern, especially given that the company operates at a 15% capacity. The recent spike in virus cases in the United States adds further doubt to whether the economy would be able to reopen soon, which could force the industry as a whole to pile on more debt to survive.

Therefore, we suggest investors to keep their distance away from Delta Air Lines until a clear indication is given by the government about the reopening of the economy, which could result in Delta to operate at least above 60% capacity if so.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.