Domino’s Pizza (NYSE: DPZ) released their second quarter 2020 earnings, beating street estimates on the bottom line.

The largest pizza company in the world based on global retail sales, announced revenue of $920M, beating analyst estimates by 0.7%, and up by 13% year over year.

The company’s earnings per share also beat street consensus by 33% at $2.99, which is above last year’s same quarter of $2.19.

Domino’s US sales rose 19.9% year over year, but International sales slumped by 8.1% year over year.

Although the global pandemic has forced the company to shut down it’s dine in operations as with most other restaurant chains, the earnings beat is largely attributed to its delivery and carryout operations, which has allowed the company to keep its stores mostly open globally.

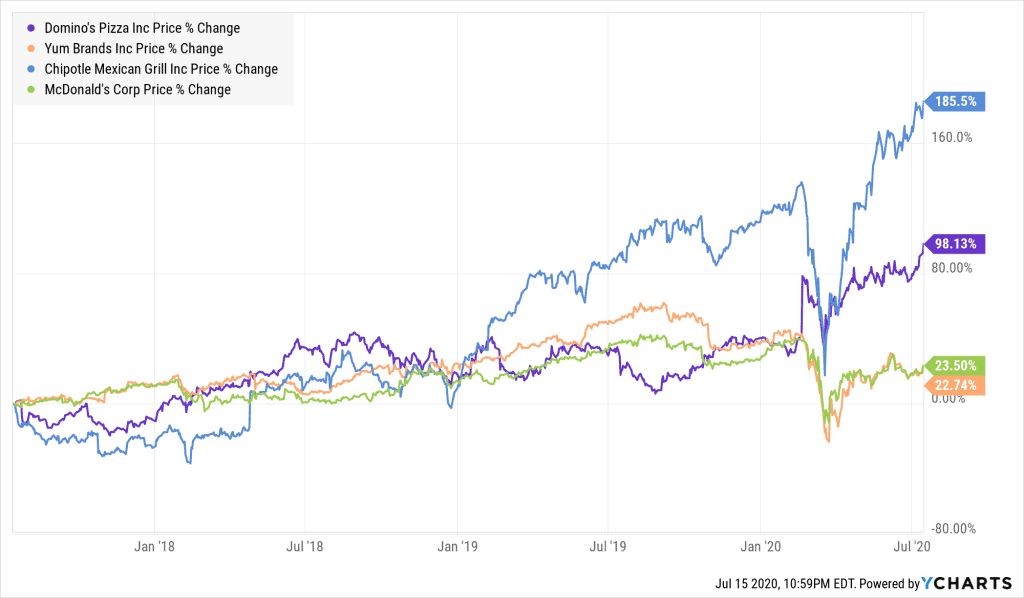

Performance versus Peers

As virus lockdown measures have begun easing, Dominos has taken the opportunity to open up 39 more stores in the US and 45 more stores internationally.

The combination of strong operational performance and store growth has driven Dominos share price relative to peers (McDonalds & Yum Brands) over the last 3 years.

Chipotle’s share performance leads Dominos due to its higher revenue and cash flow generation. Investors also appreciate its vast new investments in delivery services and partnerships with Uber Eats, and Grubhub, allowing its stores to operate at close to full capacity. This has led Chipotle’s to see its digital orders grow by roughly 80% year over year, resulting in an addition nearly 10,000 jobs to its workforce.

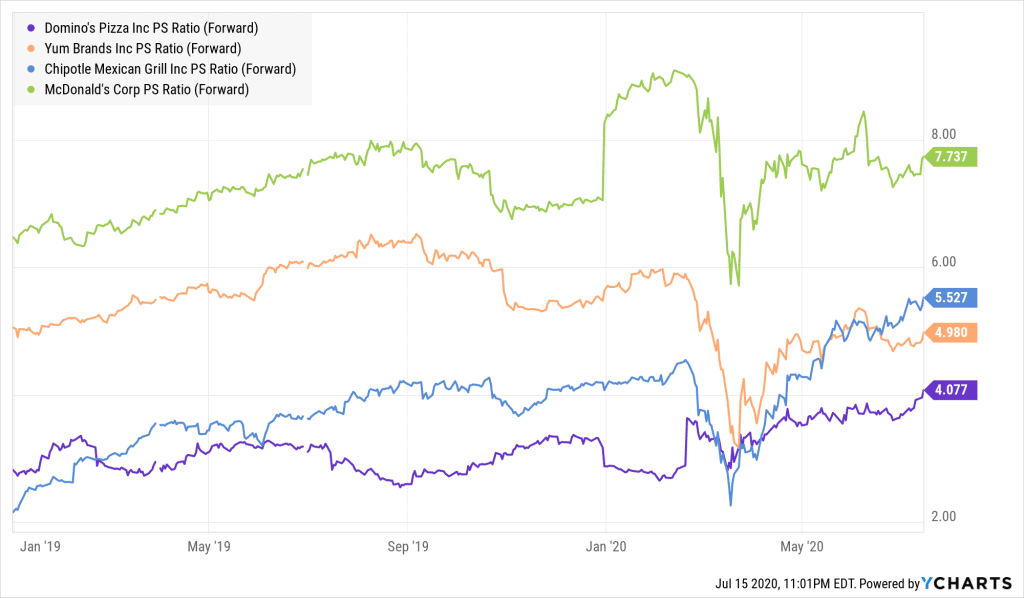

Last Slice

Among it’s peers Domino’s is trading at the lowest forward Price-to-Sales multiple, 4.1x versus the peer average of 6.0x.

Given Dominos strong relative growth and operational performance there is a a potential valuation re-rating opportunity for the shares.

There are very few companies growing top-line revenue by 13% year-over-year in the middle of the pandemic, there’s scarcity value in Domino’s slice of growth.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.