Twilio Inc. (NYSE: TWLO) , one of the leading providers of cloud communications platforms reported their second quarter fiscal 2020 earnings that beat top and bottom line analyst expectations, while raising third quarter guidance.

However, the run up of this stock since the beginning of the pandemic seems to have begun correcting itself after-hours, due to the lower than expected EBITDA performance.

EBITDA came in at $9.5M, lower than the $13.55M analyst estimate by 30%.

On the other hand, the company generated $400.8M of revenue, above the street consensus by 3.6%, and 45.7% higher year-over-year.

Investors would also be pleased to know that this was well above management’s revenue guidance of between $365M and $370M.

Another key growth metric to point out is that the company’s active customer base rose by 23.6% year-over-year to over 200K.

Earnings per share came in at $0.09/sh, 208% above analyst estimate of $-0.083, and 94% higher year-over-year as well. This was also above management’s expected range of ($0.11)/sh to ($0.08)/sh.

Irrespective of the EBITDA miss leading to an after-hours correction, the company is on track to gaining further market share thanks to management’s raised revenue guidance for the next quarter of being between $401M to $406M.

Valuation Analysis

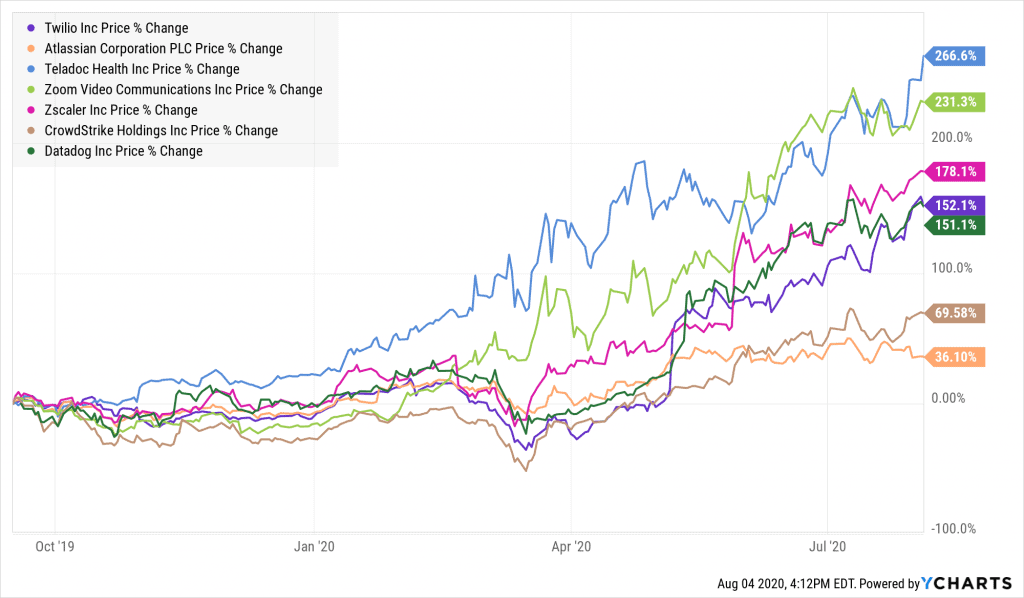

The pandemic has been a great contributor to many tech companies, particularly to those operating in the cloud. As shown by the surge in share performance of some of the many tech names below, Twilio has gained an average return in comparison.

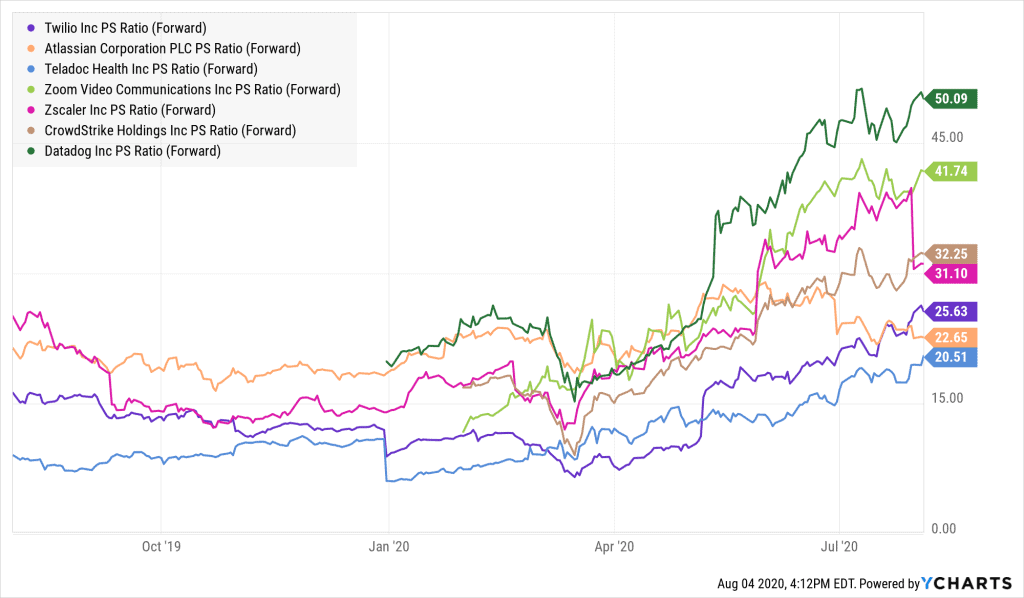

This is also reflected on the company’s Price to Sales multiple chart, where it enjoys an average premium of 25.63X.

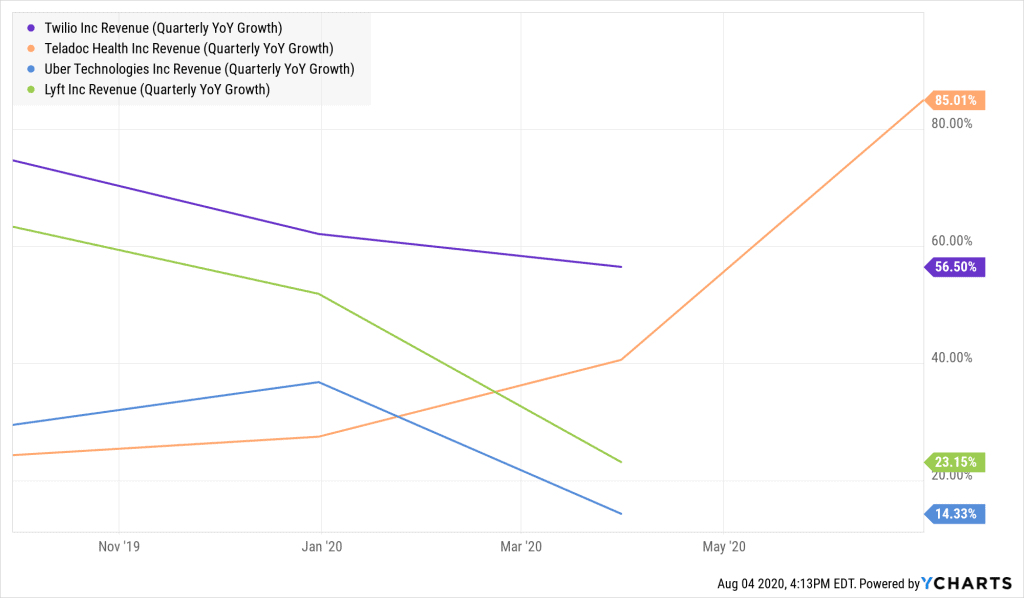

The average performance is perhaps due to the decline in usage of the company’s cloud computing platforms by the now handicapped ride sharing services, like UBER.

This is now increasingly being compensated by the rise in demand of different sectors and services, such as telemedicine offered through Teladoc, and other food delivery services in respect to social distancing.

In regards to this, the following chart depicts the relationship between Teladoc’s rising revenue growth, and the revenue decline of UBER, which has influenced Twilio’s quarterly revenue to grow by 56.5% but at a decreasing rate however.

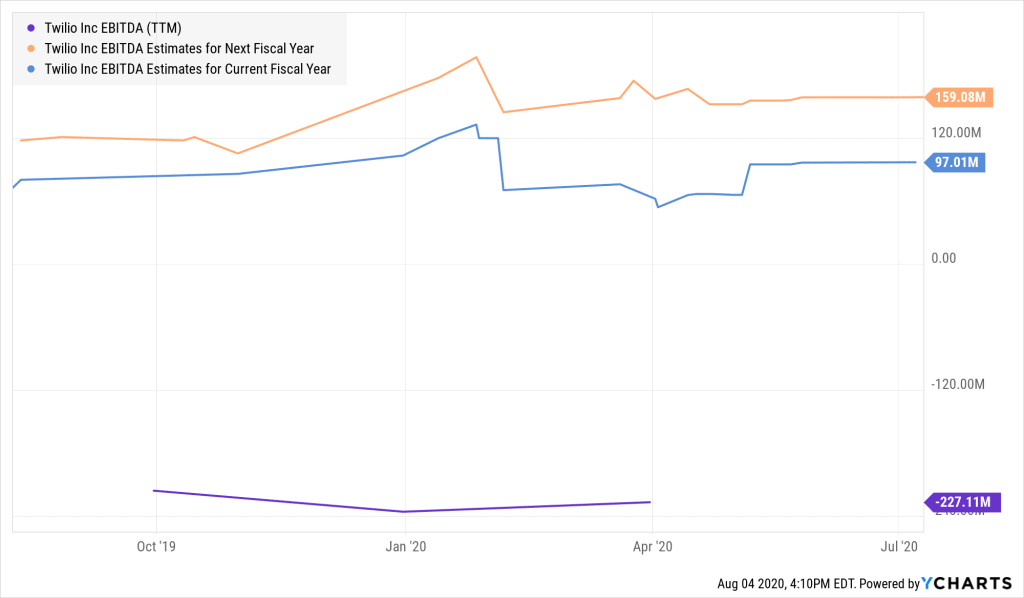

Regardless, analysts have a favoured higher outlook on the company’s current and next fiscal year’s EBITDA, which is much higher than its current trailing twelve months generated EBITDA as illustrated below.

Final Take

Although the poor EBITDA performance may have hampered the confidence of some investors, we believe that this is a temporary distraction of what is to come. The losses in revenue from ride sharing services are continuing to be over shadowed by the rise in popularity from other services, such as telemedicine.

As Twilio is continuing to restructure its business model and infrastructure to better service this rising demand, while gaining further market share as depicted by the higher management guidance for the third quarter, it is worth noting that this company presents a good growth opportunity for the coming quarters.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.