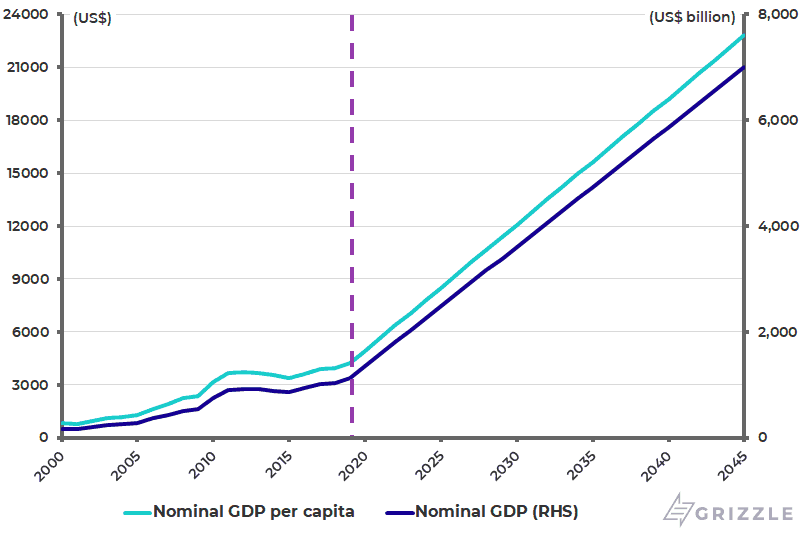

A point made in the inauguration speech on Oct. 20 of re-elected Indonesian President Jokowi caught the eye recently. The theme of the speech was to set out a goal of avoiding the so-called “middle income trap” by 2045. In Indonesia’s case, the target is to achieve a GDP per capita in Indonesia of Rp320m per year (US$22,800) or equivalent to 5.7x what it is today (US$4,000), and a GDP reaching US$7 trillion (equivalent to 6.6x today’s US$1.07 trillion) by 2045 (see following chart).

Jokowi’s GDP and GDP per Capita Target for 2045

Have Emerging Markets Peaked?

Jokowi’s speech highlights the challenge facing all emerging markets, a challenge that has increasingly concerned investors over the past year, in terms of whether the emerging market asset class has become outmoded as a concept, or in other words has reached its “sell by” date.

This is not an easy point for someone like myself, with a long-term interest in emerging markets, to concede. But it has to be admitted that there are some powerful arguments in favour of “the emerging markets have peaked” story, and it has to be admitted that Indonesia would certainly not be among the top five “emerging” candidates to avoid the “middle income trap”. For the record, the World Bank defines those countries with gross national income per capita between US$1,026 and US$12,375 as Middle-income economies.

Perhaps the best argument for the secular bear case for emerging markets is technological advance and the move from so-called “asset heavy” to “asset light” business models where the key driver of growth is the consumption of data not energy. This has gone hand in hand with accelerating technological developments in areas such as 3D printing and automation, which increasingly threaten the mass manufacturing model based on cheap labour.

In this context, I have heard stories of new auto factories in Japan which employ only ten people. True or not, the direction of travel is clear. Yet the growth-based model of mass manufacturing has been the core starting point of the developing country success stories in recent decades, be it Korea, Taiwan or, more recently, China.

Then there is the demographic issue. If the challenge facing China is to grow rich before it grows old, the same challenge applies to most other countries in the emerging market indices even if they did not have the equivalent of China’s extreme One Child policy introduced 40 years ago.

In 2002 I wrote a report called “The Real Pacific Century: Asia’s Billion Boomers” which highlighted the potential for a growing middle-class consumption story in Asia, a story that was heavily geared into the demographics. That story has played out since. But Asia’s demographic destiny has now changed significantly. While there are still some economies geared into population growth, of which Indonesia is one, the aging trend is accelerating fast.

Birth rates are declining in all the major Asian countries. This is interesting since 50 years ago, there was massive hype generated by the so-called Club of Rome report (“The Limits to Growth”), published in 1972, which warned of the horrors facing the world because of out-of-control population growth. That this prediction has proved so spectacularly wrong is one reason why I have always remained wary of similar scare stories or rather fashionable causes célèbres, be it “Peak oil” or, yes, “global warming”.

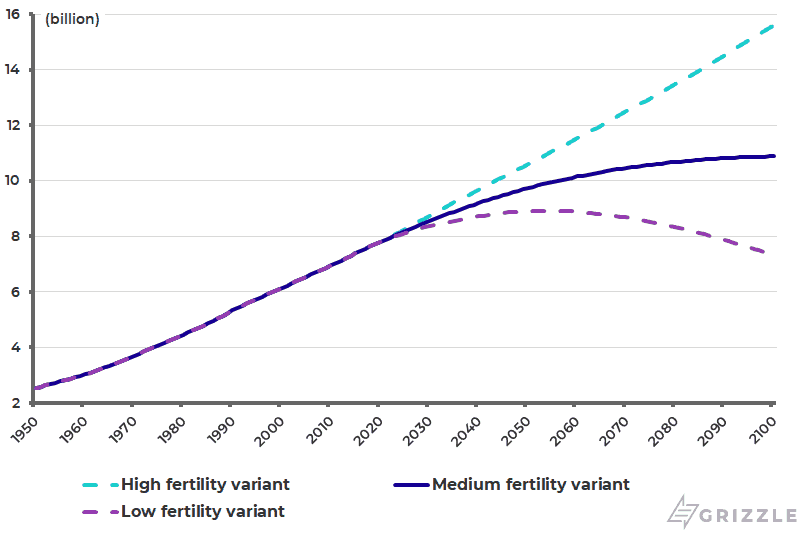

Meanwhile, the projected collapse in population growth rates could be potentially quite dramatic. On this point, I have recently read predictions that world population will peak and start to decline in three decades. As for the latest medium population projection by the United Nations, it predicts that world population will continue to rise from the current 7.7 billion to 10.9 billion in 2100, even though population growth is projected to slow from 1.1% in 2018 to 0.5% in 2050 and 0.03% in 2100. Still, the UN’s alternative “low-fertility variant” projection, which assumes a lower fertility than the medium projection, predicts that world population will peak at 8.9 billion in 2054 and will subsequently decline to 7.3 billion by 2100 (see following chart).

UN World Population Projections

This is why one key issue going forward is whether growth will be supported by rising participation rates of aging workers, where Japan has been the lead indicator. For if economic growth is driven by people and productivity, it is obviously a problem if the growth rate of the population is declining. But, even if it were not, the technological threat to the mass manufacturing model already posed a major risk to the long-term emerging market stories even if there was not also the current political attack on globalization, in terms of trade wars, tariff hikes and the like. For if the mass manufacturing model is on borrowed time, as is probably the case, then the need to upgrade the skills of the labour force becomes imperative.

Has Globalization Peaked?

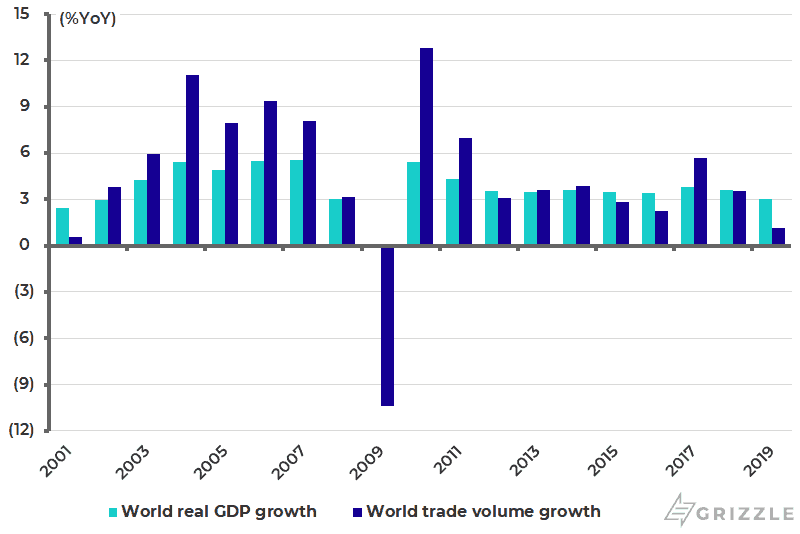

But to revert back to the present, the point is that the challenge facing developing countries was already formidable even if there were not the much-discussed threat to globalization driven by the agenda of the Trump administration. For now I remain agnostic on whether globalization has peaked, or merely gone on hold. What is clear, for now, is that the growth of trade has declined relative to the growth rate of world GDP since the global financial crisis.

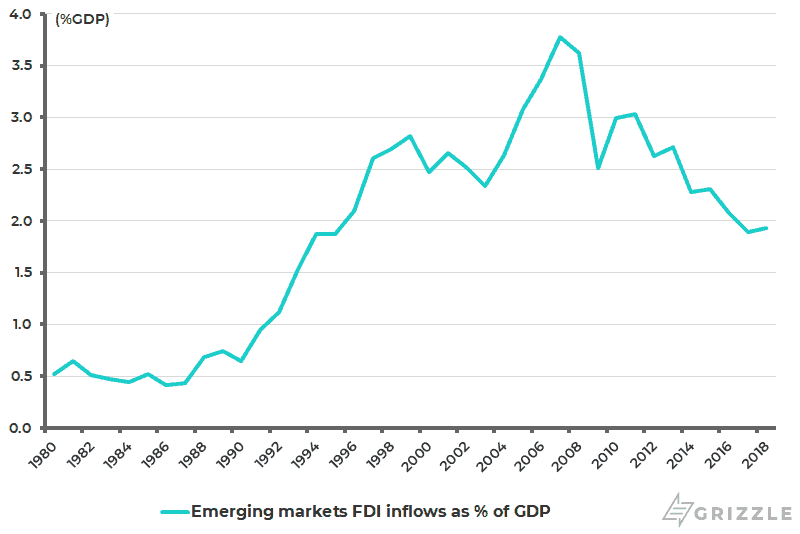

World trade volume growth slowed from 12.8% in 2010 to 3.6% in 2018 and a forecast 1.1% in 2019, according to the IMF. By contrast, world real GDP growth slowed from 5.4% in 2010 to 3.6% in 2018 and a forecast 3.0% this year (see following chart). The same trend can be seen in the declining trend in foreign direct investment (FDI) into developing countries. Thus, FDI inflows into developing countries have declined from a peak of 3.8% of GDP in 2007 to 1.9% of GDP in 2018 (see following chart).

World Real GDP Growth and Trade Volume Growth

Developing Countries’ FDI Inflows as % of GDP

Is It Still Worth Investing in Emerging Markets?

If all of the above seems rather negative, it does not mean that emerging markets are not worth paying attention to. Indeed, for the macro inclined, there will always be lots of money to be made and lost trading the sometimes extreme cycles. Argentina and Pakistan have been recent examples of this phenomenon. But what is being increasingly questioned is the assumption of the ongoing rise of a middle class in these countries. Indeed that middle-income trap looks much more challenging today than was the case ten years ago.

All is not lost for the emerging asset class. First, the major part of that asset class is China and China’s leadership is clearly razor-focused on avoiding the middle-income trap. In this respect, the demographics have only further increased the focus of the PRC leadership on the need to upgrade technological skills and boost productivity. This can be seen in the now downplayed (for political reasons) but still critically important “Made in China 2025” agenda.

As for China’s developing country neighbours, the plan is to offer a helping hand via the hoped for mutually beneficial One Belt One Road mechanism. While China’s critics view this as reverse colonialism, developing countries will need all the help they can get if the bear case for emerging markets having gone ex-growth is correct. Infrastructure will be a major growth story in Asia and other emerging markets for many years, and that is asset heavy not asset light.

As for China achieving its macro goals, and thereby avoiding the middle-income trap, I will continue to give Beijing the benefit of the doubt given its leadership’s intense focus and track record of achievement. The issue is whether this is done in a globalized world or whether China and America evolve into two separate spheres of influence, as highlighted by the 5G issue. I remain agnostic on this for now though both outcomes are clearly possible.

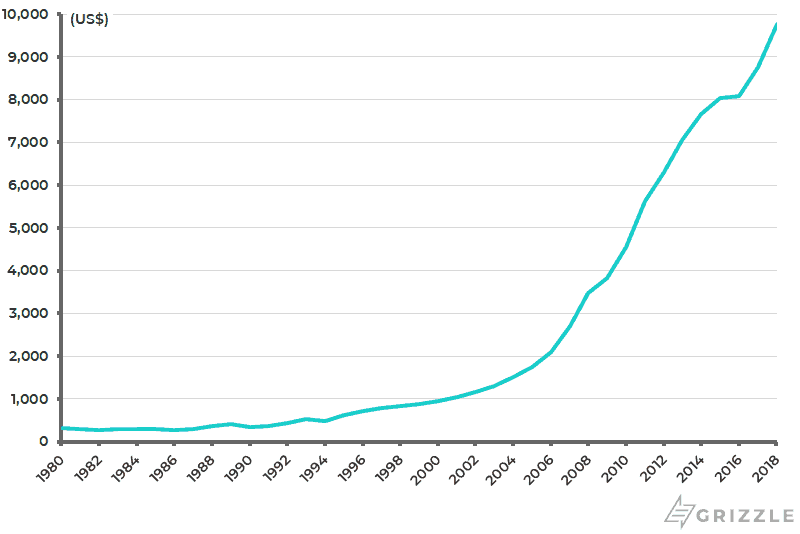

Meanwhile, the central challenge facing China is perhaps less economic than political. That is whether it can maintain the current command-economy model, and the authoritarian political system it requires, in the context of rising GDP per capita. China’s GDP per capita is currently US$9,800 (see following chart). What can be safely said for now is that Beijing has done a much better job pulling off this balancing act than most would have predicted ten years ago.

China Nominal GDP per Capita in U.S. Dollar Terms

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.