Amidst the current volatility in markets, it needs to be remembered that stimulating economic activity is directly at odds with the steps required to slow the economy to defeat the Coronavirus.

This is why the most important number investors need to monitor remains not the details of the multiple easing policies being announced over the past few days. Rather it is the rate of new infections.

This writer was recently asked what was the best signal to buy risk assets.

With the downside target of 2,346 on the S&P500 having been reached, which was the late 2018 low, sharp countertrend rallies can happen at any time as has been the case this week.

But these are probably rallies to sell so long as the infection rates in the Western world, led by Europe, appear for now to be following more closely the trajectory rates seen in Wuhan rather than other Asian jurisdictions which have so far more successfully combatted the virus, most notably China (outside the province of Hubei), Korea or Taiwan.

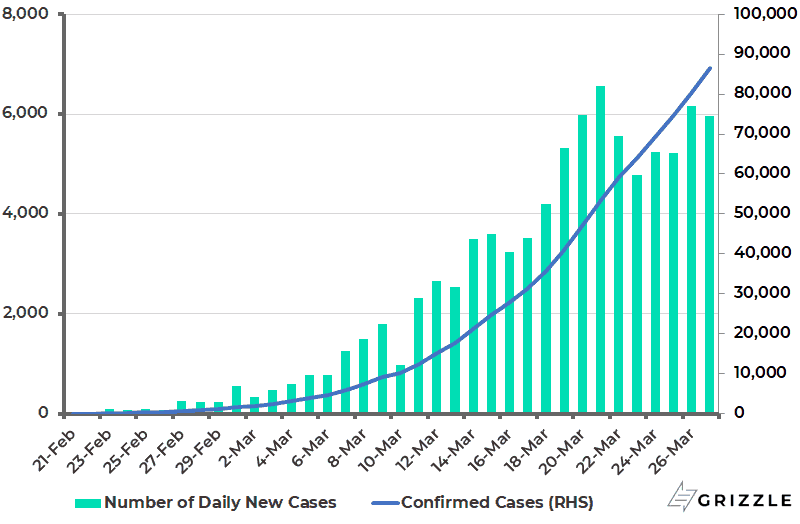

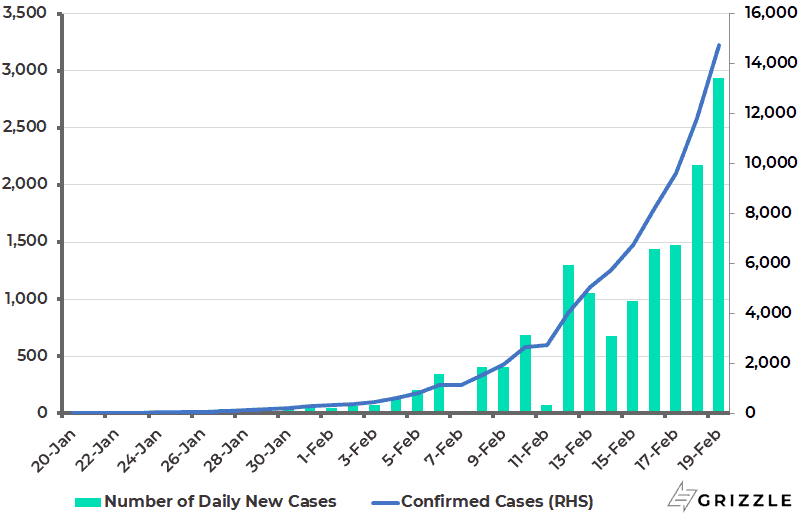

Italy Number of Coronavirus Cases

For this reason, the key area to watch for buying risk assets is any sign of the rate of infections peaking in Western Europe.

This should happen first in Italy, though it has not happened yet with the number of cases still rising by 5,959 or 7% on Friday.

But Italy has been the Western world’s equivalent of Wuhan, namely a public health disaster.

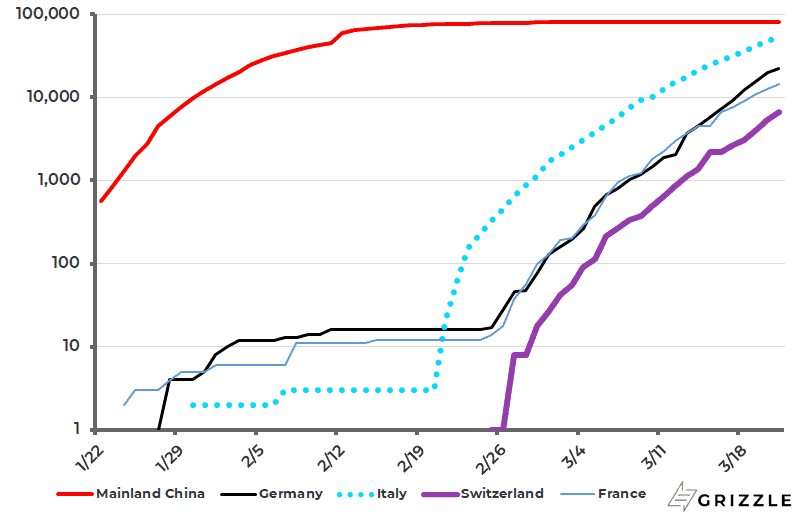

Hopefully, other Western European countries, by adopting lockdown measures earlier in the cycle of infection than Italy, will secure a peaking of infection rates sooner. This is why it makes sense to track closely the numbers in three countries, namely France, Germany and Switzerland, all of whom have implemented major lockdowns in activity for the past two weeks and more.

The chart below shows where they are in the cycle relative to the infection curve in China (see following chart).

Per Capita Coronavirus Cases in France, Germany, Switzerland, Italy and China (log scale)

The reason these countries are important to monitor is that they will provide evidence of whether the spread of this virus can be curbed in a Western democracy rather than being left to run its natural course.

This is important because these countries cannot employ the same draconian methods used by China nor do they have the same culture of social discipline of East Asian societies as seen in, say, South Korea.

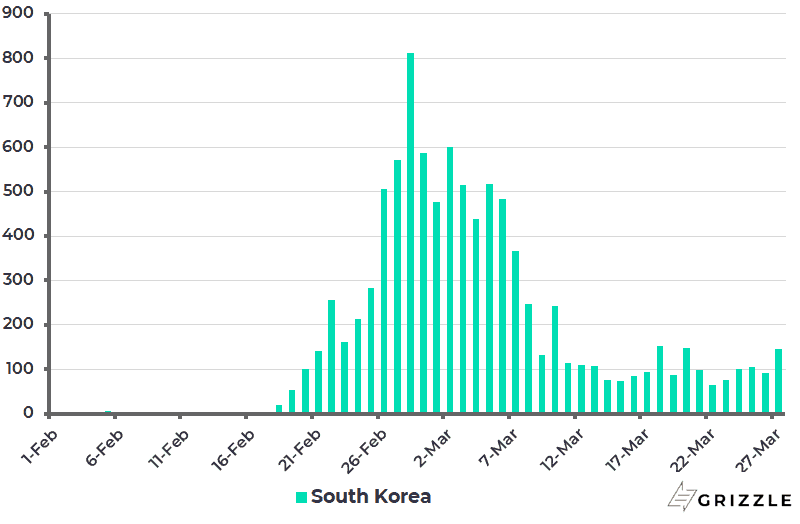

In South Korea, encouragingly, the number of infections continues to come down without a total lockdown of the economy.

The number of daily new cases in Korea has declined from a peak of 813 cases on 28 February to an average of 99 cases over the past two weeks.

Korea Daily New Coronavirus Cases

What about Britain? This country is late in the cycle because, contrary to the WHO advice of “test, test, test”, it initially relied on a policy of building so-called “crowd immunity” through the population at large while seeking to quarantine those over 70.

In theory, this policy could have turned out to be brilliantly successful but it flies in the face of the natural human desire to know if a person is infected.

This is why there has been a total U-turn in the past two weeks as there was media questioning of the maverick strategy, in terms of a laissez-faire approach to rising infections.

The British Government has now implemented the same lockdown measures being implemented in the rest of Europe, albeit with a significant time lag.

This simply means that the rate of infections will take longer to peak out.

UK Number of Coronavirus Cases

The same risk obviously applies in America, which is behind Western Europe in the infection cycle.

Still a similar trajectory of infections in America as in Italy would imply the following.

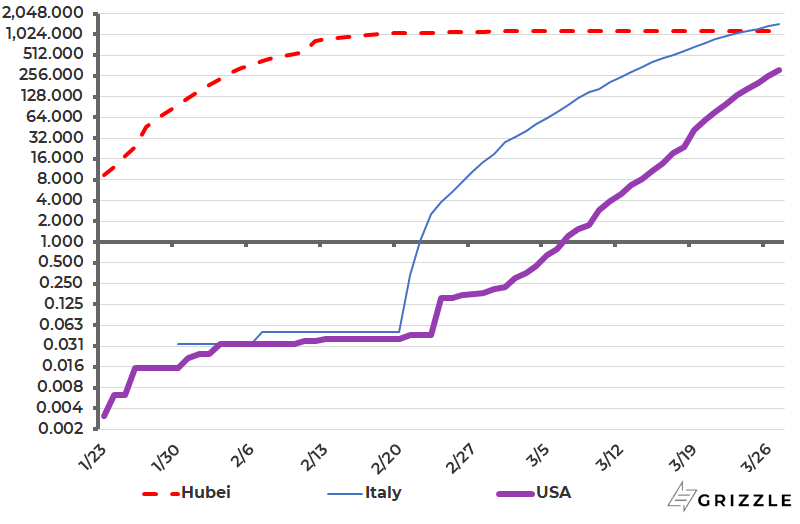

The number of confirmed cases in the US is now around 102,000 or 309 cases per 1m population, compared with 1,429 cases per 1m population in Italy (see chart below).

An increase in the ratio to 1,429 cases per 1m population in America, as in Italy, would imply a total of 470,000 confirmed cases.

Hopefully, it will be nothing like this bad but investors should understand that this is the potential risk.

And clearly, while America is not following the maverick British approach, the public policy response in Washington has been diluted, to put it politely, by the political divide, as well as by the federal structure with cities and states doing different things.

The above means that the risk is that it becomes the equivalent of the British strategy by default.

Coronavirus Cases per 1m Population in US, Italy and Hubei (log scale)

All of the above means that the peaking of infection rates in the above mentioned Western European countries may not mark the bottom of market sentiment.

But it should mark the beginning of the end.

For this reason, this writer is still hoping, as doubtless is the Donald, that the Coronavirus cycle will be a four-month affair, more akin to a tidal wave, than the trigger of a long-lasting depression.

Economies can certainly recover quickly from national disasters.

Still the initial deflationary implosion triggered by the lockdown in economic activity has already served to be the catalyst for a more formal merging of monetary and fiscal policy, as reflected in the Federal Reserve announcing last week that it will start monetizing fiscal facilities directly.

This means the direction of travel is now towards Modern Monetary Theory or “helicopter money” even though it is not being formally called that. This is because the Fed is now financing the government directly and on a large scale. The likelihood is that, once such policies are introduced, it will be hard to pull them back even after the virus has disappeared from the headlines.

The financial market implications of this will be discussed next week.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.