The Federal Reserve announced at its 2-3 November meeting the commencement of tapering as expected.

It will begin from mid-November reducing its monthly pace of net asset purchases by US$10bn for Treasury securities and US$5bn for agency mortgage-backed securities, compared with the previous pace of US$80bn and US$40bn respectively.

That means the Fed will still increase its holdings of Treasuries and agency MBS by at least US$70bn and US$35bn respectively per month beginning mid-November and by at least US$60bn and US$30bn per month beginning mid-December.

The key point for investors to remember is that the Fed balance sheet is still expanding, not contracting, though the central bank’s asset purchases are scheduled to end by June 2022.

With the Fed still finding it hard to escape unorthodox monetary policy despite the evidence of rising inflation, the crypto asset class continues to generate more attention.

Indeed it is almost becoming mainstream.

After Bitcoin’s astonishingly rapid recovery from the Beijing clampdown on Bitcoin mining in the mainland in June, when the price of the digital store of value collapsed by 30% in seven days in a deluge of margin call-triggered selling, the potential is for a further melt up in coming months in a move which is also likely to continue to see growing speculative focus on Ethereum.

This is due to move in the first half of 2022 from “proof of work”, which requires mining, to “proof of stake”.

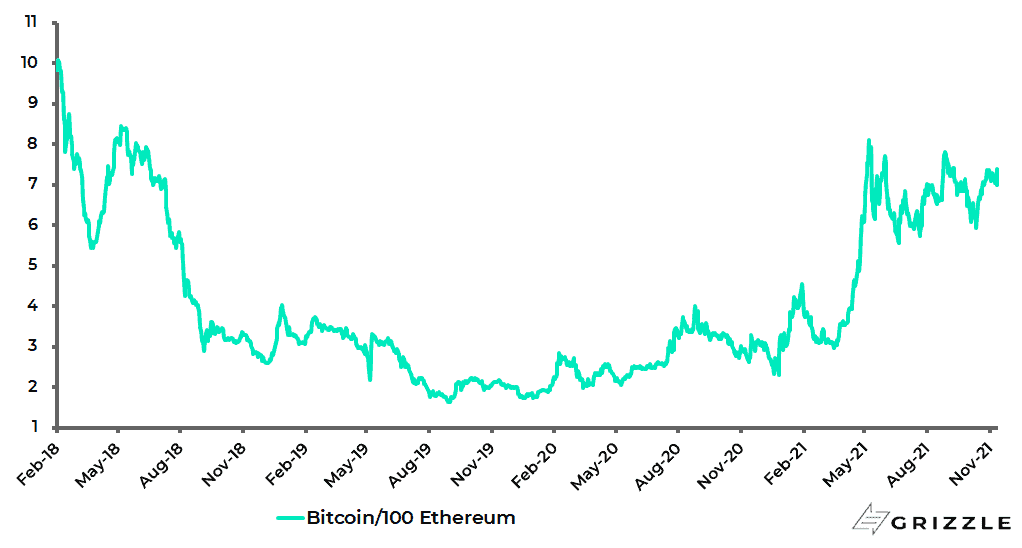

The reason for the growing focus on Ethereum, and its price has outperformed Bitcoin by 187% year-to-date, is that this protocol is at the center of the action in the fast expanding decentralised finance (DeFi) space.

Bitcoin / 100 Ethereum

This writer has discussed this before (see Own decentralised assets, digital and physical – Bitcoin and gold, 10 June 2020) but it really is important in the sense that DeFi is where it is possible today to see how crypto has begun to eat conventional finance.

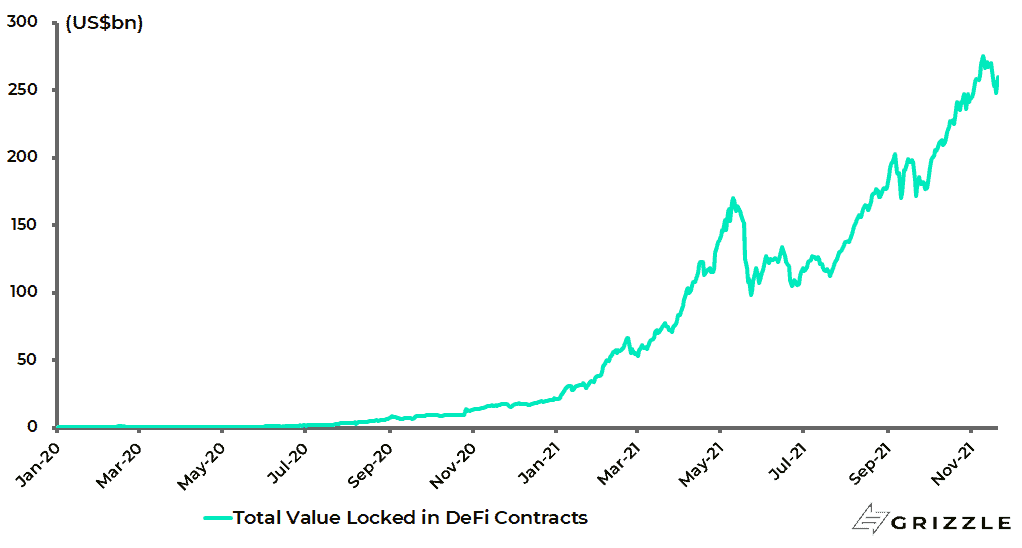

There are currently about US$100bn of deposits lodged on such “smart contracts”.

By way of definition, a smart contract encodes a transaction between two parties so there can be no dispute.

It is now possible to hear confident predictions that this figure would reach US$1tn in the next 12 months. US$1tn begins to be real money.

Total bank deposits in the UK are, for example, US$4.6tn.

Meanwhile, a recent IMF report on crypto, published in early October, also estimated DeFi contracts totaling US$110bn as of September, up from US$15bn at the end of 2020 (see IMF report: Global Financial Stability Report: Covid-19, Crypto and Climate: Navigating Challenging Transitions, 6 October 2021).

But in an indication of the surging growth, the total value locked in DeFi contracts has now reached US$260bn, according to DeFi data tracker DeFi Llama.

Total value locked in DeFi contracts

This concept of how crypto has begun to eat conventional finance is why all banks should be focused on the technology to see how to try and profit from it rather than to wait and be disrupted by it.

A decision to go the smart contract route would, for example, lead to huge savings in back office and compliance costs for traditional commercial banks.

That said, it is always a challenge for legacy companies to deal with disruption, the precise challenge facing carmakers today.

Microsoft’s success transforming itself from a software monopoly to a cloud-driven enterprise is, by and large, the exception that proves the rule.

Bitcoin could Trigger the End of the Dollar’s Reserve Status

If blockchain technology has the long-term potential to eat conventional finance, by eliminating the need for intermediaries, it also has the potential to trigger the end of the current dollar paper standard in a more benign manner than might otherwise have been the case.

Clearly, the US dollar paper standard has been living on borrowed time ever since former US President Richard Nixon removed the last formal link of the dollar with gold 50 years ago resulting in a complete lack of underlying discipline.

It is increasingly obvious that central bankers in the developed world are now in a trap of their own making, in the sense that they have not been able to escape from unconventional policy in the 13 years since former Fed chairman Ben Bernanke first adopted quantitative easing in late 2008.

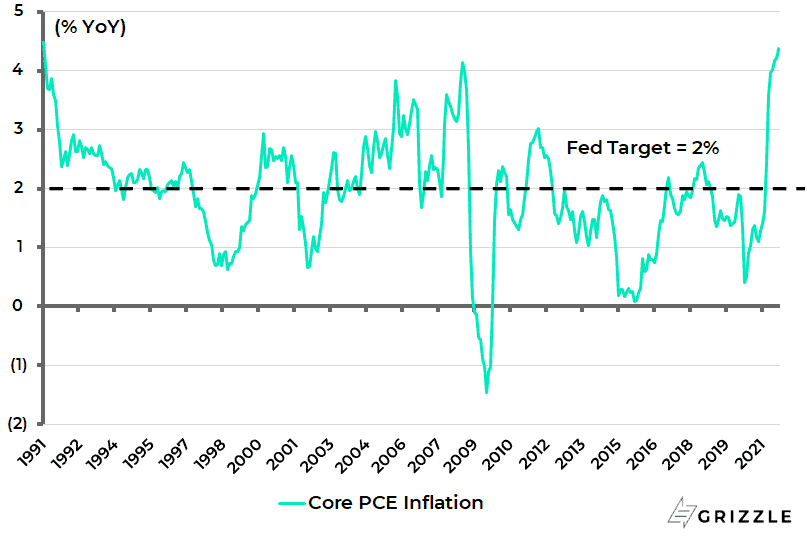

This trap will become completely obvious to everyone if inflation really proves to be more than transitory, and the last release of the Fed’s favourite inflation indicator, the PCE deflator, has also kept the inflation story building.

US PCE inflation rose from 4.2% YoY in August to 4.4% YoY in September, the highest level since January 1991.

US PCE inflation

This raises the prospect of a day of reckoning when the G7 central bankers finally lose all credibility.

This certainly remains one possible outcome.

But there is another possibility.

This is that savings simply migrate to the crypto world where far more attractive yields are currently on offer.

True, there are possibilities for all kinds of fraud and malfeasance in the evolving DeFi and non-fungible token (NFT) worlds but that does not stop the direction of travel, though the mass adoption is going to be by millennials not baby boomers.

This is because, instinctively, the former are going to be much more comfortable with smart contracts.

All this is why it is important for regulators to get their head around crypto since it does not fit easily into existing definitions of what constitutes a “security” and the like.

On this point, there was an interesting article in the New York Times recently on how the Silicon Valley venture capital firm Andreessen Horowitz was seeking to influence the regulation of crypto (see New York Times article: “Big Hires, Big Money and a D.C. Blitz: A Bold Plan to Dominate Crypto”, 29 October 2021).

The spin of the article was that the firm, a smart seed investor in Coinbase in late 2013 and many other crypto start-ups, wants not only to own the space but set the rules for it also.

If that is the spin to be expected from a cynical journalist, the reality is that the regulators needs all the help they can get from those smart enough to understand the scale of the potential disruption at hand.

Just how prescient Andreessen Horowitz has been can be seen by reading an op-ed on Bitcoin written by cofounder Marc Andreessen in early 2014 and referenced in the same article (see New York Times article: “DealBook: Why Bitcoin Matters”, 21 January 2014).

Andreessen wrote the following in his 2014 article which still makes sense today: “Bitcoin is a classic network effect, a positive feedback loop.

The more people who use Bitcoin, the more valuable Bitcoin is for everyone who uses it, and the higher the incentive for the next user to start using the technology.

Bitcoin shares this network effect property with the telephone system, the web, and popular Internet services like eBay and Facebook.”

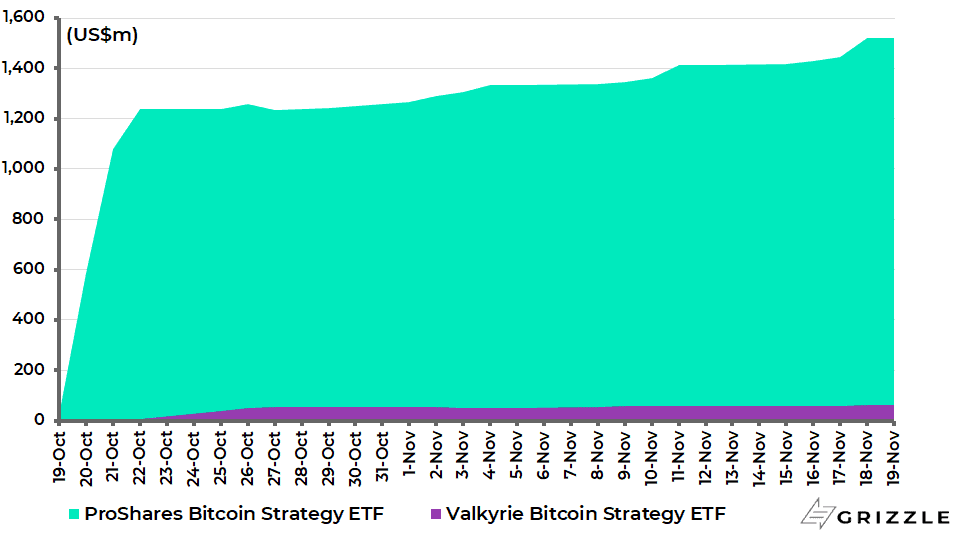

Cumulative flows into US Bitcoin Futures ETFs

Bitcoin is Finally Available to the Masses

Meanwhile, it is now increasingly easy for anyone to get exposure to Bitcoin, most particularly with the launch of the first two Bitcoin futures ETFs in America on 19 October and 22 October respectively which have now attracted a combined US$1.58bn in inflows (see previous chart).

While this represents progress it would have been much better to have a spot ETF which holds Bitcoin in cold storage, which is the case with Bitcoin physical ETFs listed in Canada and Germany.

Still at least in America retail investors can now buy a Bitcoin ETF.

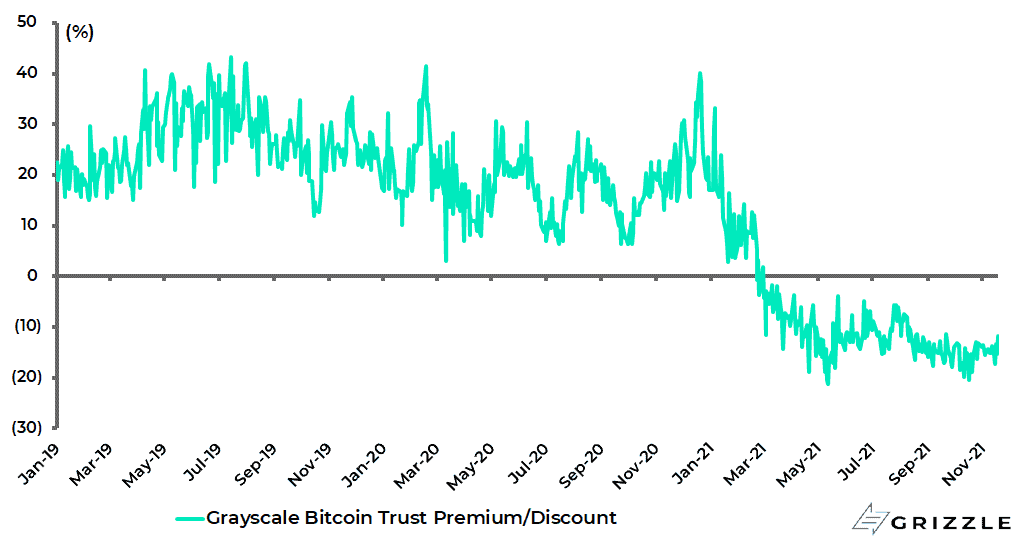

Meanwhile it is interesting to note that the Grayscale Bitcoin Trust, essentially a US-listed closed-end fund, now trades at a 12% discount having been at a 40% premium as recently as last December.

Grayscale Bitcoin Trust fund premium

Still this vehicle has served an important role in providing American investors with an ability to own Bitcoin since its public launch in May 2015 when Bitcoin was priced at US$240.

Grayscale was launched in 2013 as a private fund for accredited investors and got Financial Industry Regulatory Authority (FINRA) approval in May 2015 to publicly trade in the US.

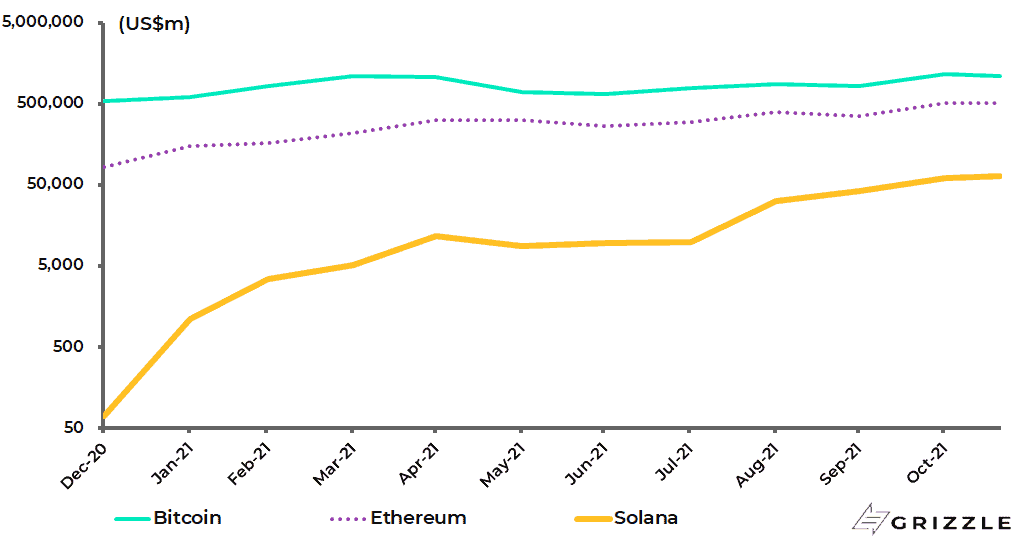

Grayscale also has vehicles offering exposure to Ethereum and Solana which is probably the next most interesting protocol in terms of the potential for mass adoption.

The market capitalisation of Solana is now US$65bn relative to Ethereum’s US$507bn.

But Solana was only worth US$70m at the start of this year. Bitcoin’s is now US$1.1tn.

Bitcoin, Ethereum and Solana market capitalisation (log scale)

Only 2% of Bitcoin Wallets Own 95% of the Coins

Meanwhile, it remains the case that only very few people in the world own a meaningful position in Bitcoin.

Thus, only 2.1% of the Bitcoin addresses hold one or more Bitcoins though they own almost 95% of the total

18.9m of Bitcoins, according to BitInfoCharts.com.

Bitcoin distribution

| Balance, BTC | Addresses | % Addresses | Cumulative % | Coins (BTC) | US$bn | % Coins | Cumulative % |

| [100,000 – 1,000,000) | 3 | 0.00% | 0.00% | 568,530 | 33.2 | 3.01% | 3.01% |

| [10,000 – 100,000) | 83 | 0.00% | 0.00% | 2,071,863 | 121.0 | 10.98% | 13.99% |

| [1,000 – 10,000) | 2,084 | 0.01% | 0.01% | 5,283,972 | 308.6 | 27.99% | 41.98% |

| [100 – 1,000) | 13,951 | 0.04% | 0.04% | 3,979,817 | 232.5 | 21.08% | 63.07% |

| [10 – 100) | 131,686 | 0.34% | 0.38% | 4,289,653 | 250.6 | 22.73% | 85.79% |

| [1 – 10) | 660,527 | 1.69% | 2.07% | 1,685,151 | 98.4 | 8.93% | 94.72% |

| [0.1 – 1) | 2,450,623 | 6.28% | 8.35% | 761,939 | 44.5 | 4.04% | 98.76% |

| [0.01 – 0.1) | 5,967,031 | 15.29% | 23.64% | 193,252 | 11.3 | 1.02% | 99.78% |

| [0.001 – 0.01) | 9,725,927 | 24.92% | 48.56% | 37,129 | 2.2 | 0.20% | 99.98% |

| (0 – 0.001) | 20,074,095 | 51.44% | 100.00% | 4,135 | 0.2 | 0.02% | 100.00% |

Source: BitInfoCharts.com

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.