As good a stock market investment story in Asia as any is India.

The Indian economy is almost back to normal and the recovery has also taken place in the marked absence of a huge fiscal stimulus in terms of an increase in transfer payments and the like.

Instead, the government’s more practical focus was on providing free food to 800m people for eight months rather than putting money into people’s pocket.

Meanwhile, the trigger for the cyclical recovery has simply been ending the lockdown which was at its most intense in May 2020.

Importantly, there are also growing hopes that India, with a median population age of only 28.4, has already seen the worst in terms of the pandemic.

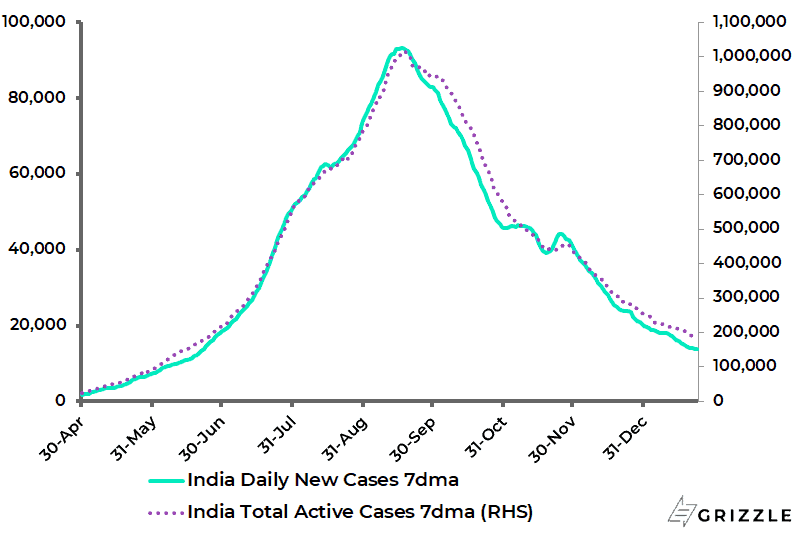

The 7-day average daily Covid case count has declined by 85% from the peak of 93,199 reached in mid-September to 13,793.

While the total number of active cases peaked at 1.02m in mid-September and has since declined by 82% to 184,408.

India Covid-19 7-day average daily New Cases and Total Active Cases

No Panic Stimulus in India

It is also the case that vaccines have begun to be rolled out since 16 January.

The plan is to inoculate 300m or one-fifth of the population by August.

So far 1.58m have already been vaccinated.

India manufactures the Oxford/AstraZeneca vaccine locally.

The result is that, like China, India has eschewed panic stimulus this past year in stark contrast to America and the rest of the G7 world.

Indeed the current Indian government seems to have learnt the lesson from China that the way to boost long-term growth and productivity fiscally is by investing public sector funds in infrastructure, not in transfer payments.

The Reserve Bank of India has also, for now at least, continued to avoid direct monetisation.

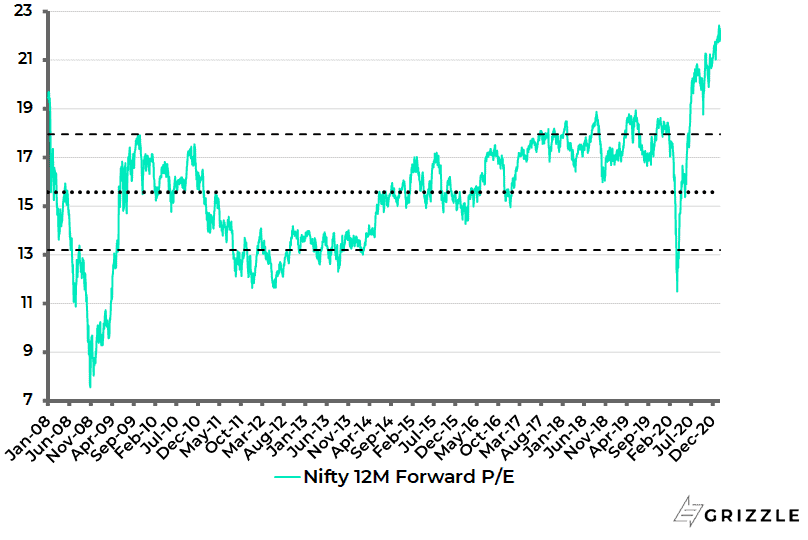

To be sure, the Indian stock market is not cheap with the market trading at 21.8x 12-month forward consensus earnings.

But the positive point is that the multiple should have a tendency to decline going forward as estimates are for 30%+ earnings growth for the fiscal year 2022 ending 31 March 2022.

Nifty 12m forward PE

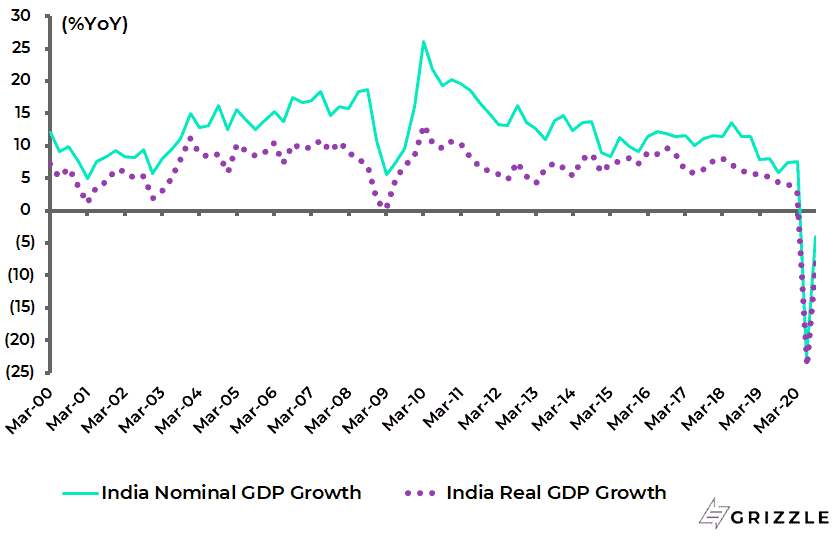

Such are the positive arithmetical consequences of year-on-year base effects given that real GDP growth collapsed by a stunning 23.9% YoY in the second quarter of last calendar year in the context of the aggressive lockdown.

India Nominal and Real GDP Growth

Real Estate Market Recovery will drive the Economy

Meanwhile, in one important area of the economy, there is already clear evidence of cyclical recovery.

That is the residential property market.

Such a recovery is not before time.

Sales volumes in the Indian housing market peaked out back in 2013 and were still one third below their peak in 2019 before Covid hit.

The results of the listed property developers last quarter showed clear evidence of recovery, as did the trend in property registrations.

Industry-wide residential unit sales are expected by property consultants to rise to 85-90% of pre-Covid levels this year, while Mumbai property registrations were up 94% YoY last quarter.

The scale and duration of the downturn is why the new housing cycle is expected to last several years.

This will create an important ongoing private-sector driver of investment in an economy which in recent years has been primarily reliant on government investment.

A sustained Indian residential property cycle is certainly what the Indian economy needs, as well as the Asia equity asset class, most particularly as China’s Xi Jinping has declared that houses are for living in not speculation.

The other reason the Indian housing cycle can run for an extended period is that prices are very cheap while historically low mortgage rates make borrowing affordable. Property prices have risen at an average annual rate of only 1-2% since 2013, well below inflation running at around 5% and per capita income growth at around 8%.

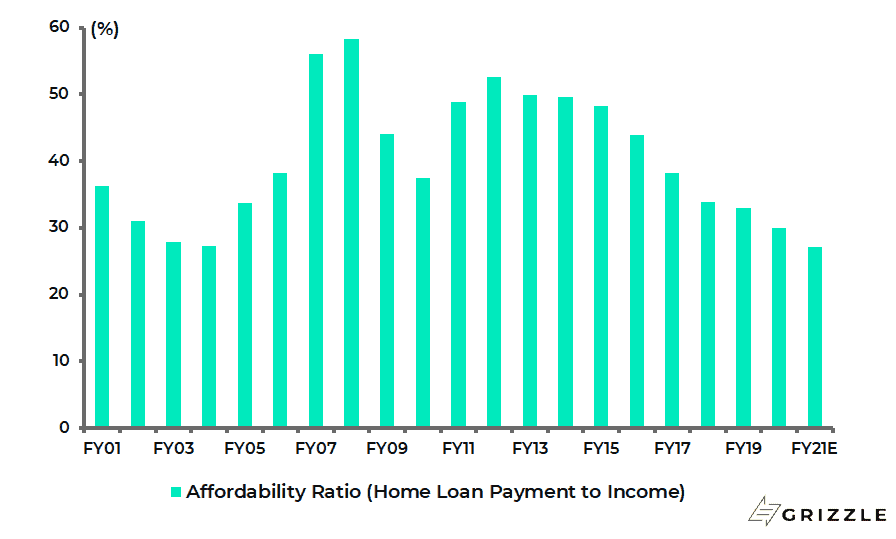

As a result, property is more affordable than ever before.

The housing affordability ratio, measured as home loan payment to income ratio, has declined from 53% in FY12 to an estimated 27% in FY21 ending 31 March, the lowest level since at least FY01.

India Housing Affordability Ratio

Real Estate Reform has Left Developer Stocks in a Much Better Place

Meanwhile, the fundamentals of the market on the ground are much healthier as a result of the Real Estate (Regulation and Development) Act implemented in 2016 which undermined the business models of the then many over-leveraged developers.

This stipulated, among other things, that developers need to put 70% of revenues from presales into escrow until a project is completed.

Such a reform was necessary since many developments in the past were never completed with buyers losing the money they had paid up-front.

The result, combined with other shocks such as demonetization in 2016, the introduction of GST in 2017 and now Covid, has meant a brutal consolidation.

Indeed this writer, in many years of following property markets, has never seen a consolidation like it which is why the surviving major quoted developers should be viewed as long-term holds.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.