The current investment quarter has been marked by financial markets acting like talk of a “return to the 1970s” is yesterday’s story.

This is a reference to the further sell-off in oil and the related commodity complex.

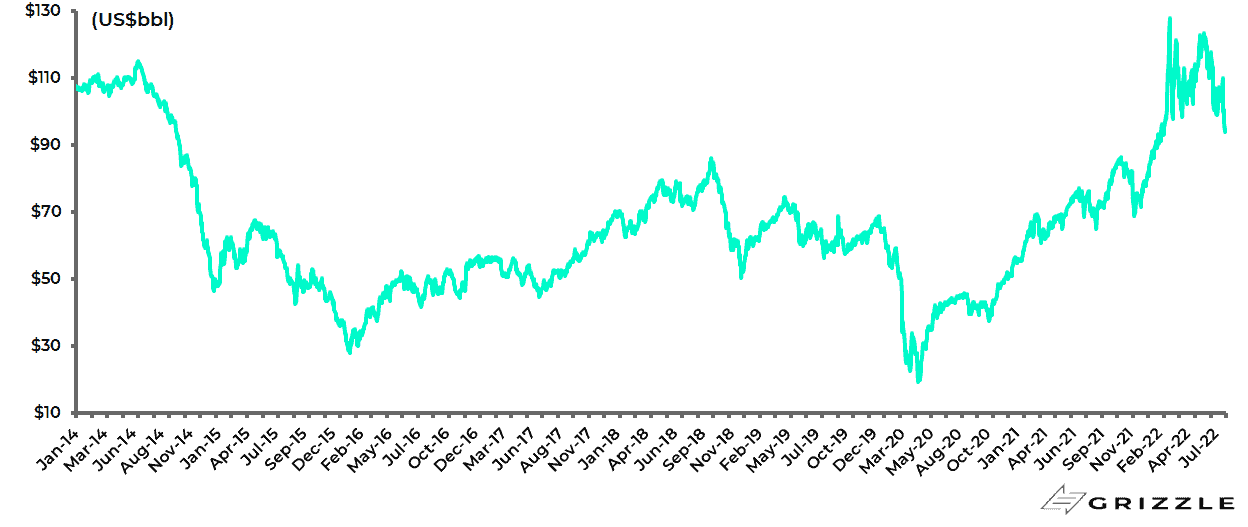

The Brent crude oil price has declined by 19.2% since the start of July to an intraday low of US$92.8/bbl last Friday.

Brent crude oil price

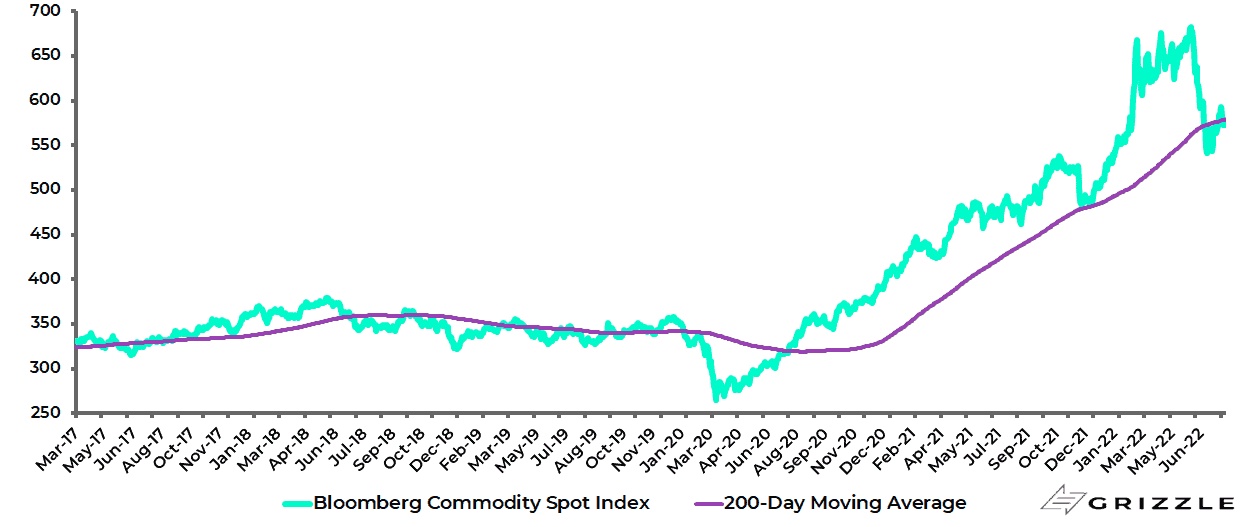

While the Bloomberg Commodity Spot Index, which tracks 23 energy, metal and crop futures contracts, has fallen by 16% from the record high reached in early June.

Bloomberg Commodity Spot Index

The obvious theme remains demand destruction in a slowing global economy.

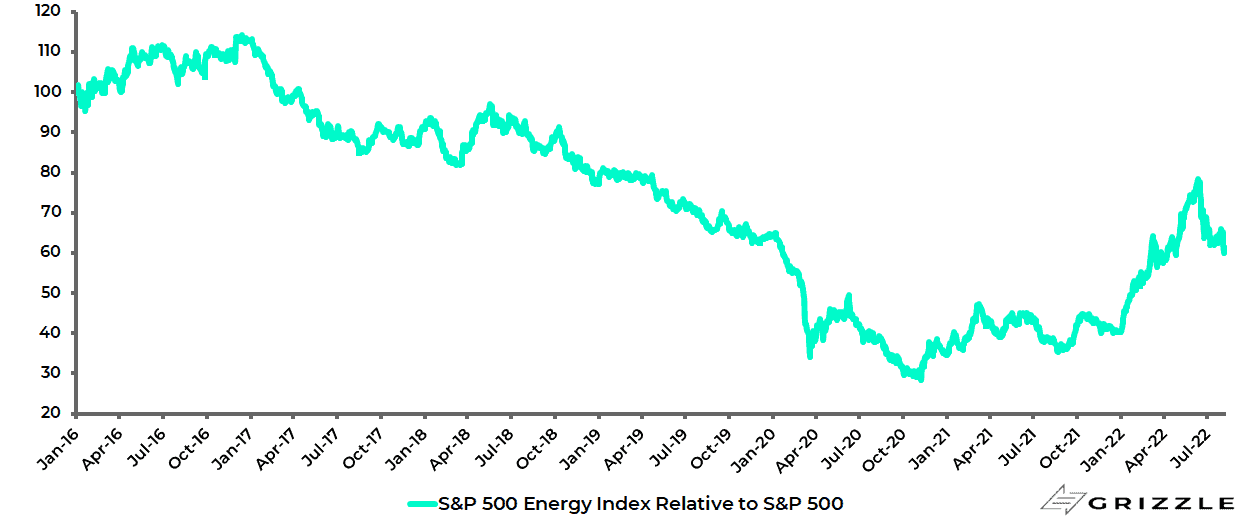

Still, in this writer’s view there is also a technical aspect, in the sense of selling the sector, energy, which had been outperforming until mid-June.

The S&P500 Energy Index outperformed the S&P500 by 176% from a relative low in early November 2020 to mid-June 2022 and has since underperformed by 22%.

S&P500 Energy Index relative to S&P500

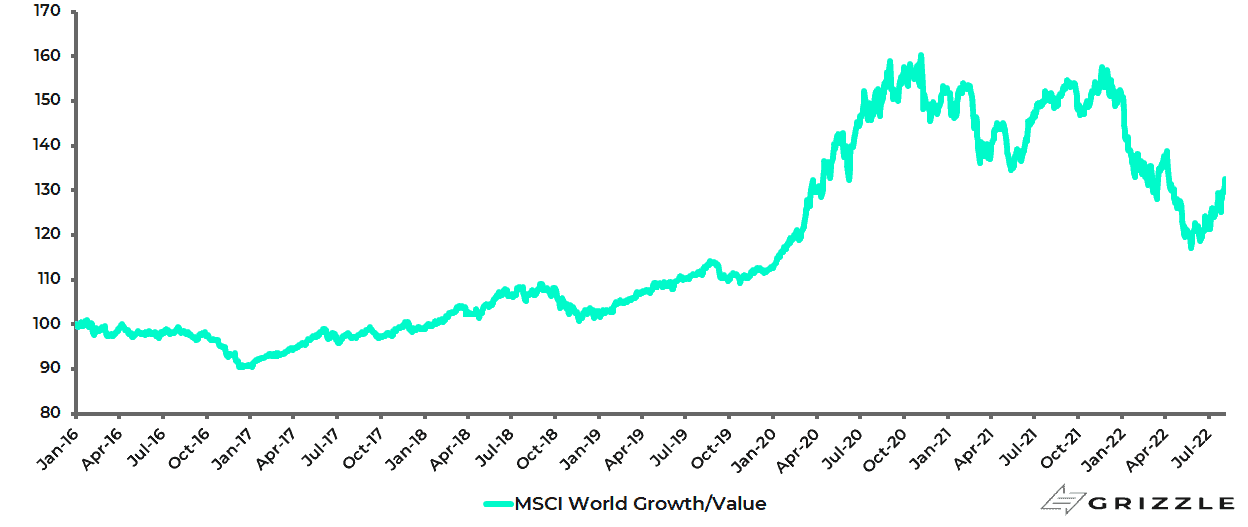

This writer also continues to believe that the return to the 1970s theme of stagflation has legs.

Still, the MSCI World Growth Index has outperformed the MSCI World Value Index by 12.4% since 24 May.

MSCI World Growth Index relative to MSCI World Value Index

A Relaxation of COVID Zero Policies in China Aren’t Enough for Property Investors

Another reason oil has sold off is depressed demand in the Chinese economy due to the continuing Covid suppression policy.

Still, there have been some hints of a relaxation of the policy.

Two examples will be cited here.

Since mid-July it is now required to have a negative result of a nucleic acid test within 72 hours before entering public venues in Beijing such as cinemas.

This should be viewed as a positive in the re-opening dynamic.

Cinema attendance is certainly rising.

China’s box office revenues rose from Rmb716m in May to Rmb1.92bn in June and Rmb3.5bn in July, according to ticketing platform Maoyan.

Second, China’s soccer league, the Chinese Super League, resumed home and away games from 5 August for the second phase of the 2022 season.

The first phase kicked off on 3 June and concluded on 12 July, after having been rescheduled several times due to the pandemic.

Still, the key sector for the mainland economy, namely residential property, remains impacted by Covid suppression and the related growing impact on middle-class consumer confidence with Chinese property buyers not responding to the growing easing efforts by the authorities.

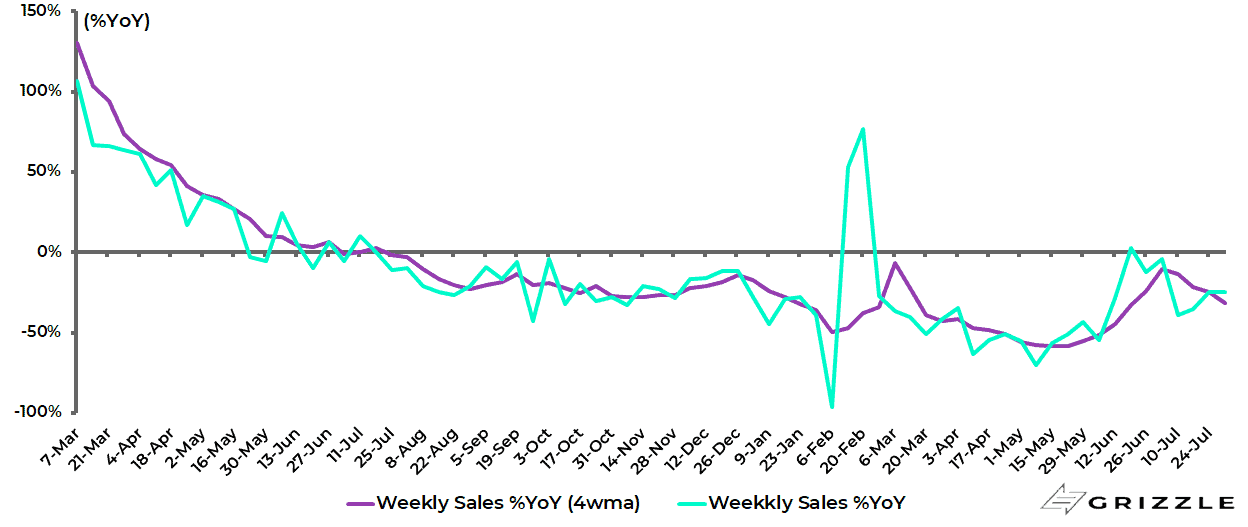

Weekly residential floor space sales in 25 key mainland cities declined by 31% YoY in the four weeks ended 31 July.

China residential floor space weekly sales in 25 key cities %YoY

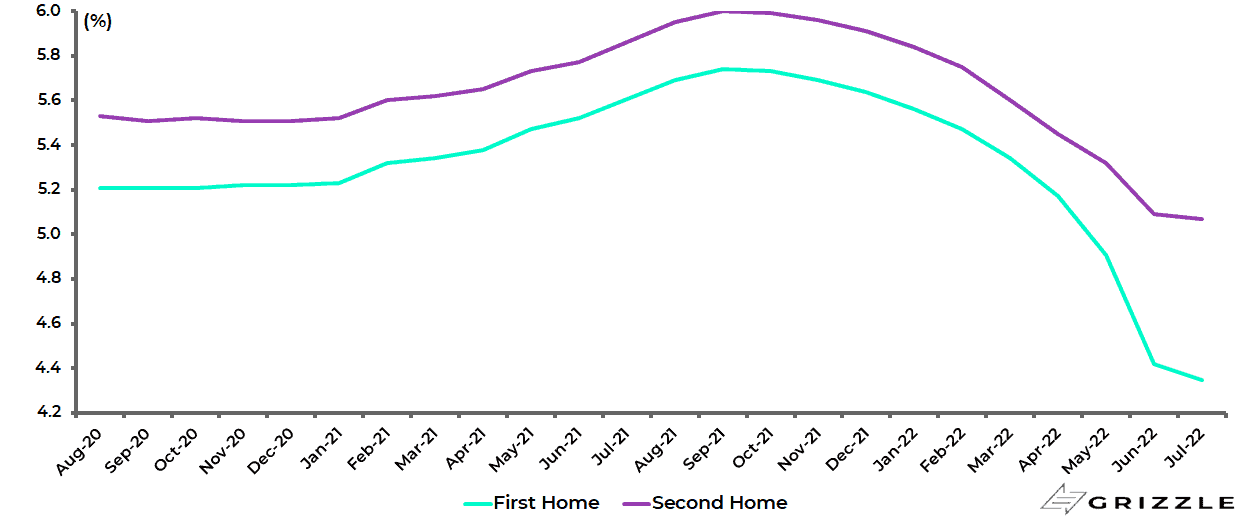

This is despite the fact that the PBOC cut the five-year loan prime rate (LPR), which is a benchmark rate for home mortgages, by 15bp to 4.45% in mid-May and also lowered the minimum first-home mortgage rate to 20bp below the five-year LPR or 4.25%.

As a result, the average effective first-home mortgage rate has declined by 82bp in the past three months to 4.35% in July and is down 139bp from the recent high reached last September, according to a survey of 103 major cities by Beike Research Institute.

China average effective first-home and second-home mortgage rates

There has also been a growing mortgage strike by borrowers who are concerned that the properties they have bought as pre-sales will not be completed because of a cashflow squeeze facing private sector property developers.

Such home buyers, acting in seeming unison via social media, have gone on mortgage strike since mid-July because construction work has halted on their unfinished property projects.

Homebuyers reportedly said that they will stop mortgage payments until developers and commercial banks take action to resume construction.

More than 300 projects in over 90 cities have now reportedly been affected by such mortgage boycotts.

In this respect, private developers, short of cash, have been halting construction of projects even if they have already been sold.

About 90% of property sales in China are of uncompleted units.

The above represents collateral damage from Covid suppression in terms of the unintended consequences of the policy.

Hong Kong Unlikely to Be Swallowed by China Anytime Soon

Meanwhile, it was a positive signal that President Xi Jinping visited Hong Kong at the beginning of July for the 25th anniversary of the handover from British colonial rule on 1 July and the inauguration of John Lee as the new Chief Executive.

Xi’s message was that Hong Kong should focus on business.

This is in the context of recent statements from mainland officials with responsibility for Hong Kong to the effect that “One country Two systems” can be extended for another 50 years after the 50-year expiry in 2047, statements which have not really been reported in the Western media.

Thus, Shen Chunyao, chairman of the Legislative Affairs Commission of National People’s Congress Standing Committee, said on 27 May at a legal forum on the Basic Law that the concept of the 50-year lifespan was only a “symbolic description” and that there would not be changes to the principle after 2047 (see South China Morning Post article: “Beijing offers reassurances Hong Kong’s ‘one country, two systems’ principle will not change after 2047”, 27 May 2022).

Xia Baolong, director of the State Council’s Hong Kong and Macau Affairs Office, also stated in March that Hong Kong’s “high degree of autonomy” could last for 50 years after legally expiring in 2047 despite the national security law passed in June 2020 (see The Standard article: “City’s autonomy could last beyond 2047”, 9 March 2022).

With Xi Still Committed to COVID Zero, No End to the Policy is in Sight

Returning to the mainland, if there is some evidence that China has relaxed Covid suppression without formally admitting it on the account of the collateral damage done to the economy, the problem with this assumption is that Xi has remained publicly committed to the policy.

And he has a track record of meaning what he says.

Meanwhile, the current status of Covid cases is as follows.

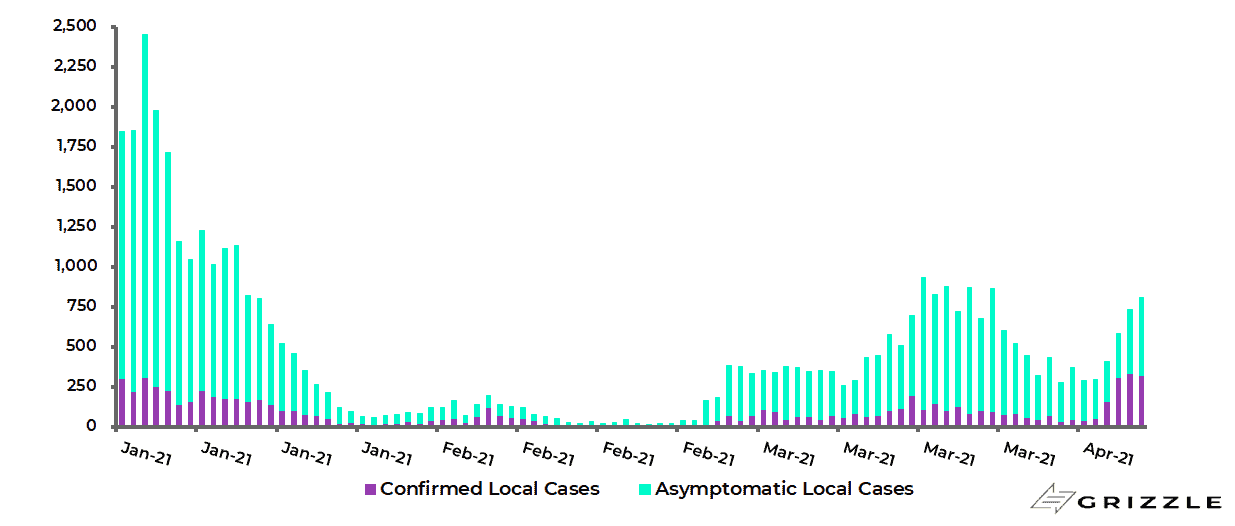

China’s daily new local Covid case count has risen from a low of 14 in late June to 807 on 7 August, though it remains well below the peak of 29,317 reached in mid-April.

A total of 67% of Chinese aged over 60 have now had the required three doses of vaccines as of 22 July, which is what is required to make them effective.

China Daily New Local Covid Cases

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.