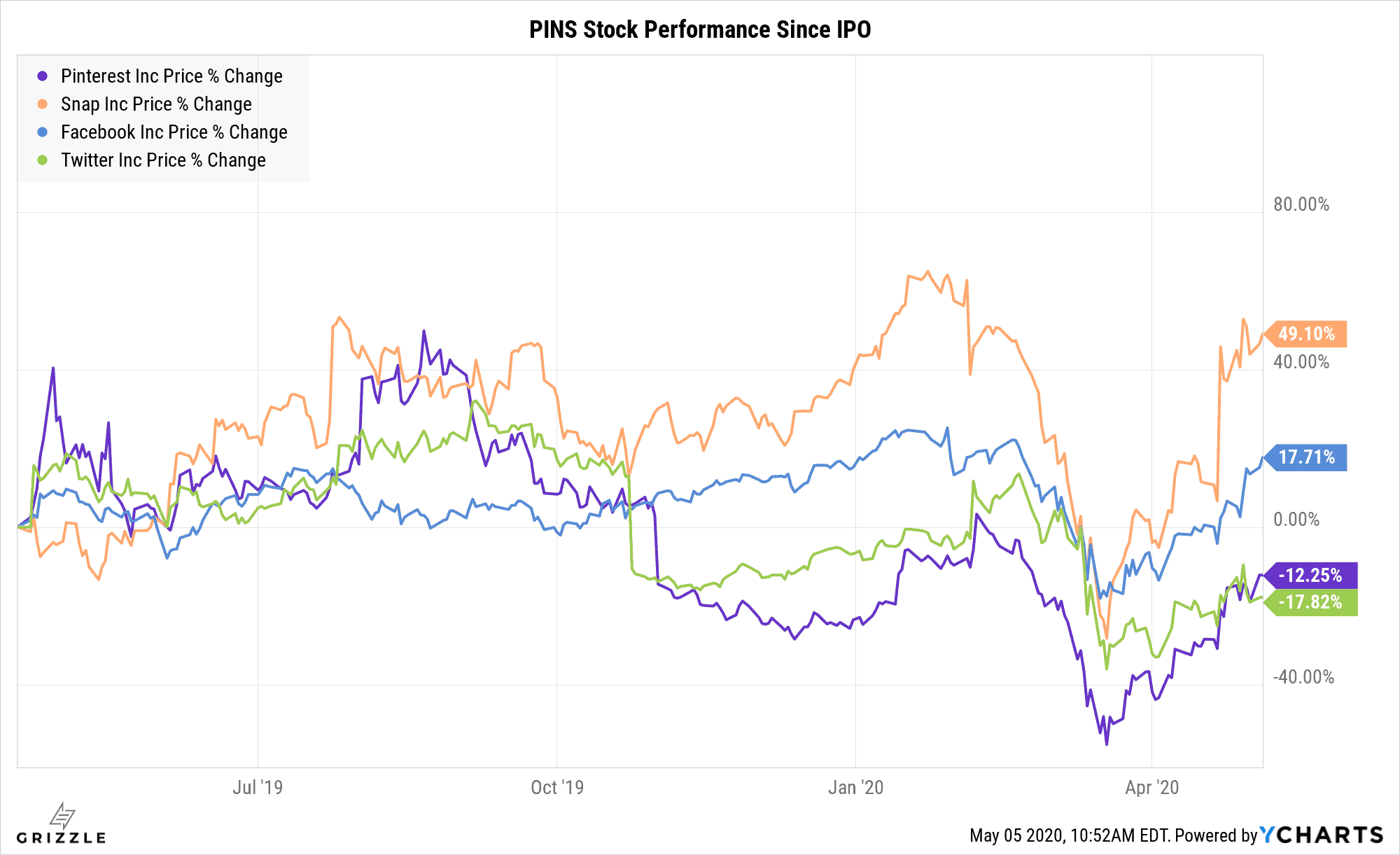

Social media and shopping platform Pinterest (NYSE:PINS) announced earnings that met expectations but were tinged with a more negative outlook on margins in the coming quarters.

The stock is down 11% in after-hours trading as the market digests what is shaping up to be a tough year for this previously high-flying tech stock.

Management already pulled guidance for the year on April 7th, yet the stock is only 10% below where it traded before the Pandemic began.

Revenue came in at $272 million, generally in-line with consensus of $271 million and management’s revised guidance of $271 million.

Revenue growth of 35% was down meaningfully from last quarter’s growth of 46%.

Adjusted earnings per share missed estimates, coming in at a loss of -$0.10 compared to the consensus estimate of a -$0.09 loss.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Pinterest is still priced like it will become the second most profitable social media property behind Facebook. With no indications yet that revenue per user will ever surpass Twitter and consumer spending on the decline, we won’t be buying this stock unless we can get it for $16/sh or below. [/su_panel]

Pinterest’s multiple is now higher than it was before the Coronavirus pandemic began as revenue estimates for this year are down 17% while the stock price is only down 4%.

[su_panel]Pinterest is more expensive than it was in February even though consumer spending is currently falling off a cliff.[/su_panel]Not to mention Pinterest makes 35% less per user than Snap and 60% less than Twitter.

The Pinterest platform is built for monetization so the cashflow will come, but the stock is still pricing in that Pinterest becomes the most profitable social media platform behind Facebook.

We have absolutely no data indicating this will be the case, making this a risky bet at this time.

| Company | 2020 P/S | Revenue Growth Rate | (Avg Rev Per User) |

| Snap | 12x | 32% | $1.36 |

| 9.7x | 46% | $0.87 | |

| 7.8x | 19% | $8.44 | |

| 6.8x | 13% | $2.03 |

Ever since the IPO, we could never justify a stock price higher than $16/sh, even if we assume Pinterest becomes more profitable than all of its competitors, except for Facebook.

ARPU Needed to Justify Only $16/sh

Our handy visual guide below will help you make buy and sell decisions if you choose to invest in Pinterest over the long term.

Grizzle Guide to Buying or Selling Pinterest Stock

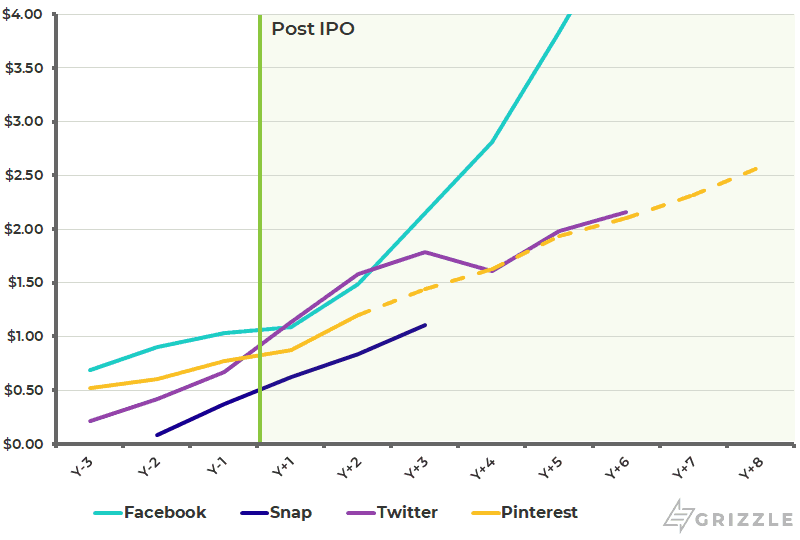

PINS has Been the Second Worst Performing Social Stock Since its IPO

Pinterest has struggled to regain highs set from its IPO in 2019.

For the stock to move through the mid-20’s we think Pinterest will have to surpass the U.S. profitability of Twitter, which it is still 50% below.

Pinterest already generates more revenue per user than SNAP, making Twitter the next bogey for management to go after.

The length and severity of the Coronavirus pandemic will determine if Pinterest can break through $25/sh this year or if its headed back to the mid-teens.

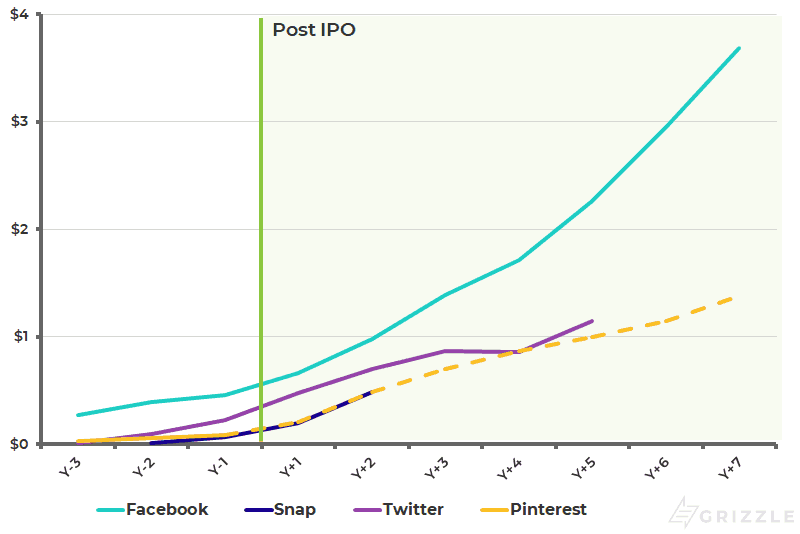

EBITDA Will Have to Wait for Later

Pinterest is accelerating the revenue it generates from each user but is still lagging the profitability of Twitter, Snap, and Facebook when they were at the same stage of growth.

The market is pricing in a nice acceleration in per user revenue and if Pinterest doesn’t at least meet Twitter’s numbers, the stock has further downside to it.

It is still early days for management and they are only a year into figuring out how to fully monetize their platform internationally which is where the real growth will come from.

Watch international revenue per user closely as it could foreshadow the acceleration in revenue the company needs to get the stock moving higher.

With the Coronavirus raging and consumer confidence on the decline, the hoped for profits in 2020 will have to wait until 2021.

Yet another reason to be cautious on this stock.

PINS International Profit Per User Still Has a Long Way to Go

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.