Concerns continue to percolate about the Chinese property market with the Federal Reserve recently warning about it.

The Fed said in its latest semi-annual Financial Stability Report published on 8 November that stresses in China’s real estate sector could strain the Chinese financial system, with “possible spillovers to the United States.”

On the same point, this writer’s attention was recently drawn to a bearish Economist article published at the start of last month on China housing (see The Economist article: “China jitters (1): The property complex – How a housing downturn could wreck China’s growth model”, 2 October 2021).

Certainly, there is no doubt that the stellar days of the China housing market may have peaked.

Demographics alone make this point self-evident and this writer makes no apology for repeating the point made here before (see To Survive China’s Market Crackdown: Pick Your Sectors Wisely, 24 August 2021), namely that the biggest mistake made by the PRC in the otherwise incredibly successful reform era was not to end the One Child Policy many years earlier.

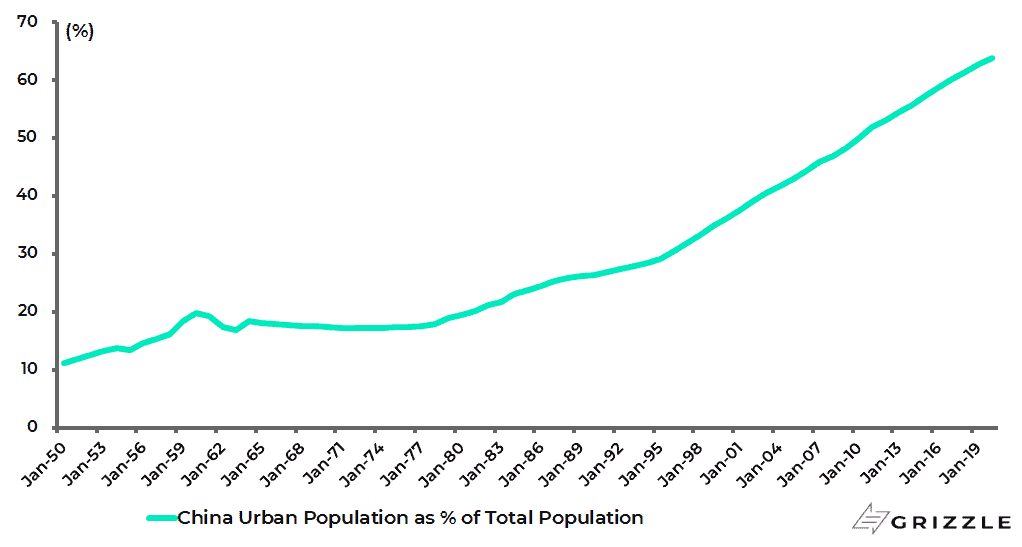

Still, having said that, China’s urbanisation is far from complete and this also drives housing.

The urban population now accounts for 63.9% of the total population in China, up from 49.9% in 2010, according to the 2020 Census.

China Urban Population as % of Total Population

Meanwhile, a potential peaking out of housing as a driver of economic growth is a very different outcome from a housing downturn wrecking China’s growth model.

The central government is deliberately seeking to wean the economy off its dependence on property, just as its proposed rollout of a property tax seeks to reduce the dependence of local governments on land sales for tax revenues.

This is sensible public policy though, in the case of the property tax, it is a long overdue one.

On this topic, the Standing Committee of the National People’s Congress announced last month the expansion of the property tax reform into certain pilot cities over a five-year period.

The introduction of a property tax will, therefore, be a gradual transition, not an abrupt one.

Meanwhile returning to the China housing bust theme, the same old bearish stories have been played out again of late as regards China property in terms of empty cities, unaffordable housing and the like.

The problem with such generalisations is that there have always been two entirely different China housing markets.

There is no doubt that housing is extremely expensive in the biggest cities, most particularly when compared with reported incomes.

Still, all the empirical evidence is that there is huge pent-up demand for residential property in these cities whenever property tightening measures are relaxed.

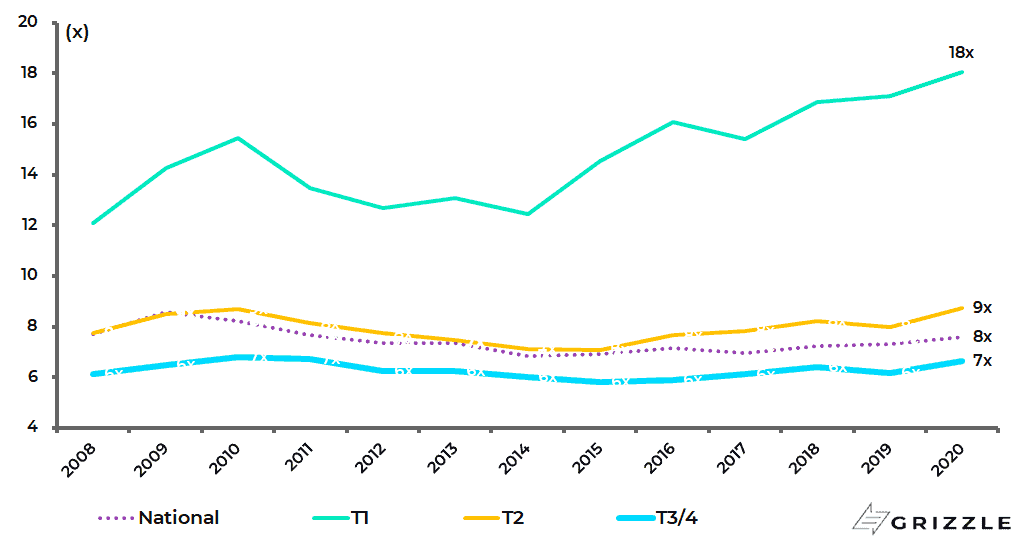

Still, property looks much less expensive relative to incomes when calculated in terms of national averages.

Assuming an average household size of three persons and a unit size of 100sqm, the national average residential property price to annual household disposable income ratio is running at 7.6x, compared with 18x for the Tier One cities (see following chart).

China Housing Affordability (house price to urban household disposable income)

Note: Assuming an average household size of 3 persons and unit size of 100sqm. Source: National Bureau of Statistics, CEIC Data

This reflects the reality that in many smaller Tier 3 and 4 cities the problem is less unaffordable property than

excess supply. And this is where the stories of empty cities come from though, that said, it has to be said that China’s command economy ‘build it and they will come’ model has worked remarkably well so far

Meanwhile, it should also be emphasized that, from a macroeconomic perspective, China’s four Tier One cities, namely Beijing, Shanghai, Guangzhou and Shenzhen, still account for only 3% of the property market as a whole in terms of floor space sold, and 10% in value terms.

In this respect, it is misleading to generalise about the condition of China’s property market from the state of play in these four major cities.

It has usually been the case, for example, that speculative froth has always seemed to be greatest in Shenzhen if only perhaps because it is next to property obsessed Hong Kong.

And Evergrande, the highly leveraged property developer which has triggered stories about China’s “Lehman moment”, is, yes, based in Shenzhen.

The view here remains that Beijing can manage the fallout primarily because the central government should be prepared for the liquidity crisis since it has induced it by its “three red lines” policy discussed here previously (see To Survive China’s Market Crackdown: Pick Your Sectors Wisely, 24 August 2021).

Meanwhile, as regards talk of bubbles, the majority of Chinese cities nationwide still enforce a 30% minimum down payment for first-home purchases while a 30-40% down payment is required for first-home purchases in tier-one cities.

The other more general point is that an ongoing crackdown on property, or at least a perception that a lid is going to be put on residential property prices going forward, is not necessarily negative for Chinese stocks.

This is because equities become more attractive as an alternative asset class.

This simple, but important, point is often forgotten by foreign investors.

China’s Path to Decarbonization Will Not be Straight Line Anymore

Meanwhile, the past few weeks have seen a return of traditional Chinese pragmatism in terms of policy towards its recently stressed energy sector.

The result will be a much more flexible approach to reaching long term decarbonisation goals in terms of a near-term retreat from enforcing power reduction targets.

Utilities have also seen some long-overdue relief in terms of the ability to raise tariffs.

Thus, the National Development and Reform Commission (NDRC) announced on 12 October that it would allow the market trading price of coal-fired electricity to fluctuate 20% above or below the benchmark tariff, up from the previous 10% increase and 15% decrease range.

While all industrial and commercial users will have to pay market prices for electricity, with the industry-specific prices abolished.

That means power producers can charge higher rates for energy-intensive sectors such as metals, chemicals and building materials.

The NDRC also said recently that it will “make full use of all necessary means” to intervene in coal prices to promote “the return of coal prices to a reasonable range” and to ensure the “security and stable supply of energy” during the winter heating season.

Thus, it has ordered coal mines to maintain “normal production” even during holidays and major events, issued approvals for new mines and ordered major coal production bases in North and Northwest China to lower prices by Rmb100/metric ton.

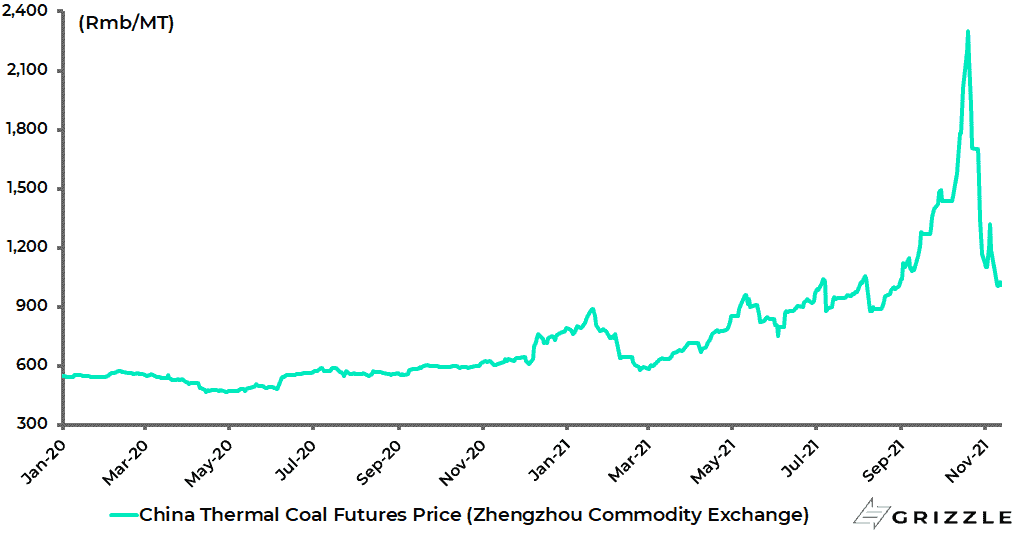

As a result of such measures, China’s thermal coal futures price have declined by 57% since 19 October, though it is still up 27% year-to-date.

China Thermal Coal Futures Price

Source: Bloomberg

It remains the case that coal still accounted for 57% of China’s energy consumption in 2020.

China is also still building coal-fired power plants and remains, as of now, a coal-based economy, as the fallout out from the recent spike in coal prices makes abundantly clear.

Thus, provincial governments approved the construction of 24 new coal-fired power plants in 1H21 with a combined capacity of 5.2 gigawatts.

Coal currently accounts for 49% of China’s 2,200 gigawatts installed capacity.

This present reality raises the issue of how serious President Xi Jinping is when he surprised the world in September 2020 by declaring the carbon neutrality goal by 2060.

The first point to make about this commitment is that Xi has a track record of doing what he says he is going to do, which is a lesson now being learned by foreign holders of Evergrande dollar bonds since the “three red lines” policy was first announced in August 2020.

Still, when it comes to decarbonisation matters, Xi is unlikely still to be President of China in 2060 since by then he will be 107 years old.

In this respect, the practical point to note is that China’s near-term decarbonisation targets are much more modest and so more achievable.

The goal of the 14th Five-Year Plan announced in March is to increase dependence on non-fossil fuels to 20% of total fuel demand by 2025, and to 25% by 2030 based on the target Xi announced last December.

This compares with 15.8% in 2020.

Still the practical reality, as of today, is that China’s industrial sector remains almost entirely fossil fuel driven.

That said, China also sees practical positive commercial consequences from the world’s increasing commitment to decarbonisation.

This is the catalyst to growth provided by the growing adoption of renewable energy.

Here the most practical example of commercial success is China’s global dominance in the market for solar panels.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.