There has been a bit of a pullback in the cyclical trade with US energy stocks down 11.8% from their recent peak and US bank stocks down 3.5% (8.5% at the recent low on 25 March).

This is probably little more than a pause to refresh after the big price gains recorded.

The S&P500 Energy Index rose by 99% from the recent low reached in late October to a recent peak on 11 March and was up an even more impressive 136% from the March 2020 low.

While the US bank index has risen by 106% from the March 2020 low.

So this pullback should prove an opportunity to add to cyclical exposure.

S&P500 Energy Index and S&P500 Banks Index

Meanwhile, the focus will grow in coming weeks on the scale of the Biden administration’s pending infrastructure stimulus which could now be as big as US$2.25tn.

There will also be a growing focus on the tactics employed to get this package through Congress, as well as how much will be paid for by increased taxation.

While some tax increases seem inevitable, particularly an increase in corporate tax, it is also worth noting that there have also been reports that Biden’s “advisers” have also argued that investments that boost the economy’s long-term growth potential “may be worth financing through more deficits”.

Remember that advocates of Modern Monetary Theory, who are well represented in the progressive wing of the Democratic Party, explicitly embrace monetization and are certainly not bothered about rising fiscal deficits.

So the American macro story, as well as the policy context, remains fully supportive of the cyclical trade as does the impressive vaccine roll out in the US where 41% Americans have now had at least one vaccine.

What about the rest of the world?

Rest of the World Lagging in the Vaccine Rollout

The past quarter saw a lack of progress in continental Europe, in terms of the slowness of the vaccine rollout which can definitely put back recovery there by a quarter.

Vaccines in the Eurozone were running way behind Britain, for example.

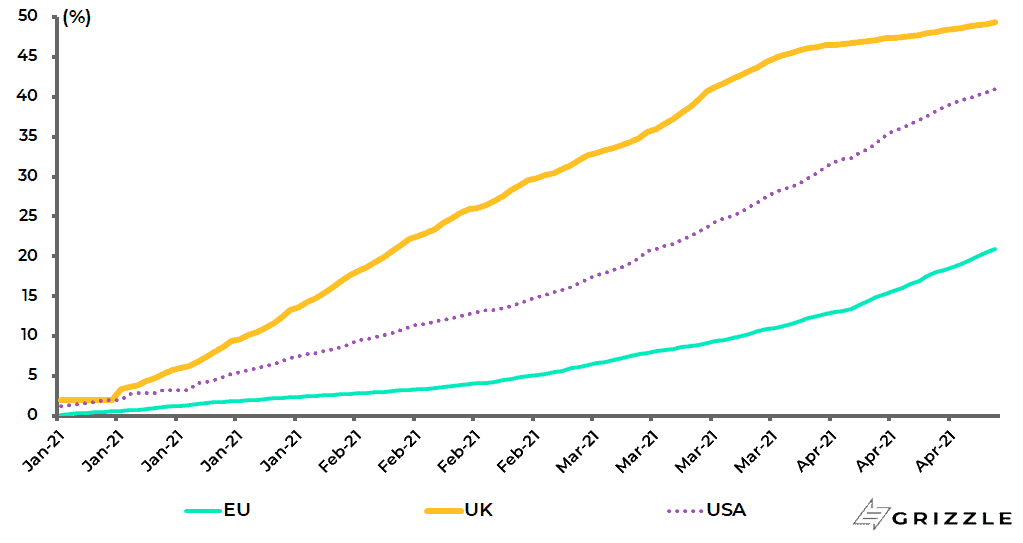

Thus, the share of people who had received at least one dose of the Covid vaccine at the end of last quarter was 46% in the UK, compared with only 12% in the EU.

Share of people in UK, EU and US Received at Least One Dose of Covid Vaccine

This has exposed the problem of the Eurozone as a political entity in the sense that undertaking a vaccine rollout is more akin to fighting a war and the EU has clearly never shown much aptitude for the latter activity.

Still after being severely embarrassed the evidence now is that the Eurozone has got its act together and should reach its target of vaccinating 70% of the population by the end of the summer.

The share of the population who have received at least one dose of vaccine in the EU has already risen from 12% at the end of March to 21%.

The EU authorities now expect 360m doses will have been delivered in the region by the end of June, up from 170m doses in the first quarter.

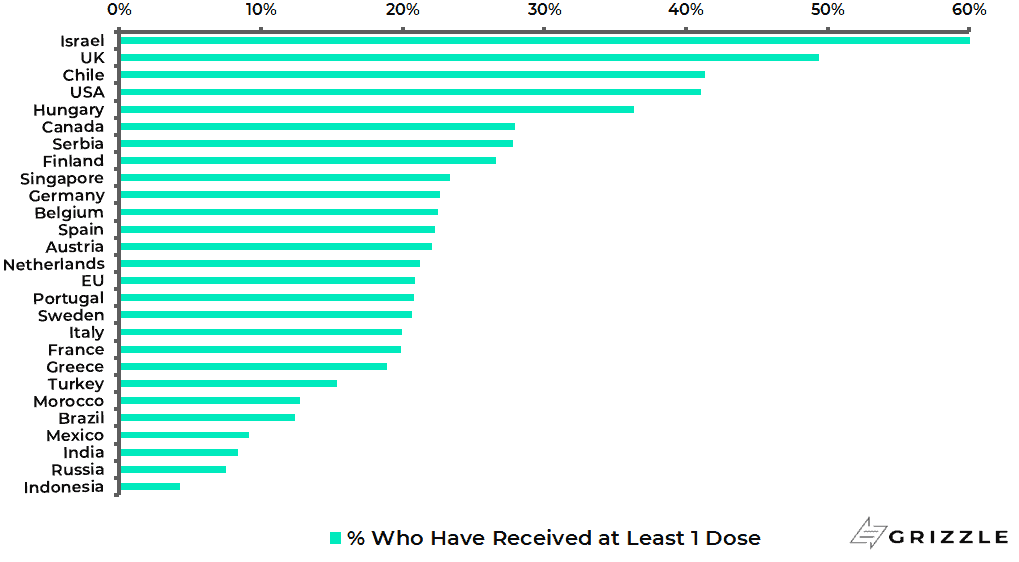

This leaves the emerging markets as the major laggard.

Share of people who received at least one dose of Covid vaccine (23 April 2021)

Source: Our World in Data

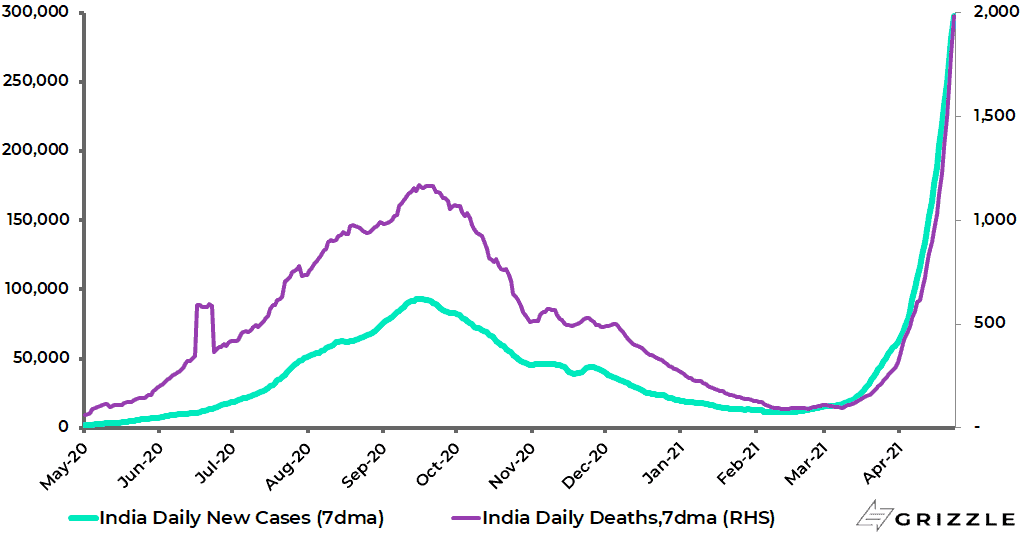

Indeed this is the reason why Covid cases have been rising globally again with India, Turkey and Brazil the main drivers.

The 7-day average daily new Covid case count globally has risen by 456,982 from a low of 358,583 on 20 February to a new high of 815,565, with India, Turkey and Brazil accounting for 76% or 345,884 of the increase.

World 7-day Average Daily new Covid Cases

India COVID Spike in Focus

The rate of ascent of cases in India, in particular, makes it self-evident that new variants are a driver.

And this raises the critical issue of whether the vaccines are effective against the new variant.

This remains unclear.

So far 117m Indians, or 8.5% of the population, have been vaccinated.

India 7-day Average Daily New Covid Cases and Deaths

Meanwhile, the vaccine rollout remains critical given that it has become increasingly evident that Covid is a chronic condition and new variants will likely keep on coming, which is why the world needs to get used to living with Covid and why a new booster vaccine will probably be needed every year.

The problem for developing countries with tropical climates is that these vaccines require sub-zero temperatures and therefore are not really practical for large-scale distribution assuming they can even be afforded.

Still, the positive point for India is that it is a fast-emerging manufacturing centre for Covid vaccines.

In the best case, 2021 vaccine quantities for India could cover 78% of the population with Sputnik V, Johnson & Johnson and Novavax vaccines likely to become available during the current or next quarter.

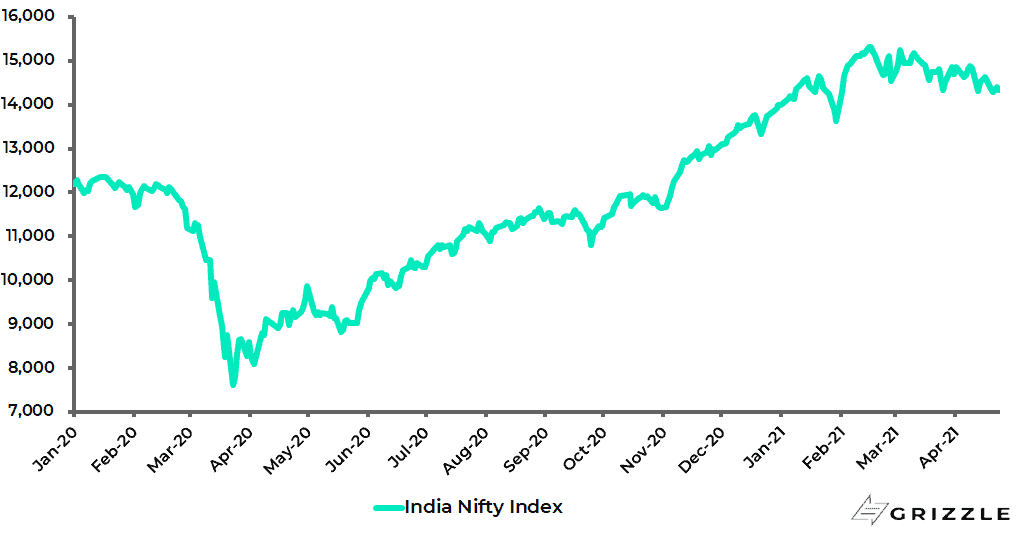

Meanwhile, the Indian stock market is only 7% off its recent high reached in mid-February despite the disastrous newsflow on Covid.

India Nifty Index

The main reason for this resilience is that the Modi government seems determined to avoid a national lockdown similar to what happened last year.

This lockdown is now viewed in hindsight in terms of the collateral damage on the economy where such a large part of the population is dependent on daily wages.

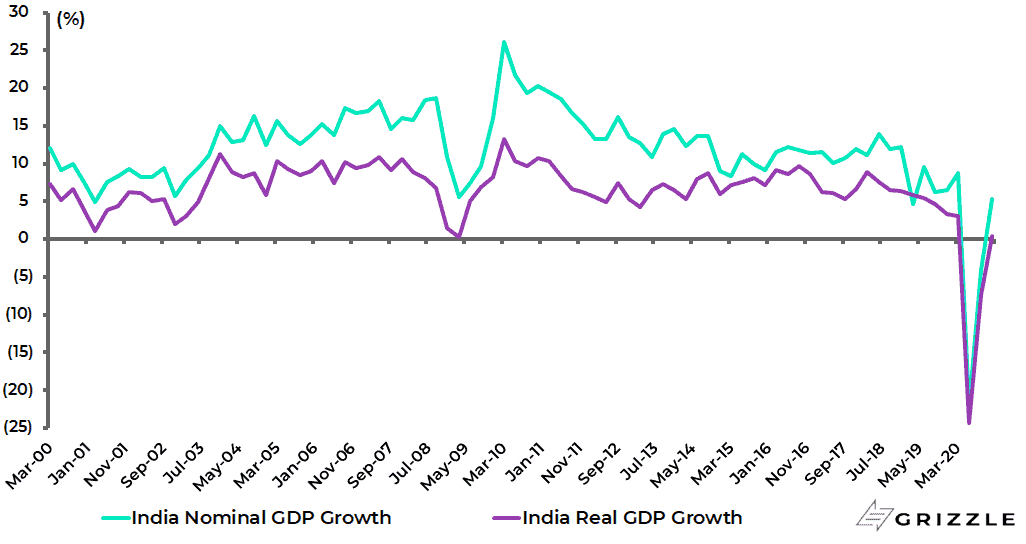

Indian real GDP contracted by 24.4% YoY in the second quarter of 2020.

India Nominal GDP growth and Real GDP Growth

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.