This writer has continued to take a positive view on energy stocks.

That said, energy and other cyclical commodity-related sectors are clearly vulnerable as concerns about slowing economies mount, and the resulting concerns about demand destruction rise.

This can be seen in the market action in recent weeks.

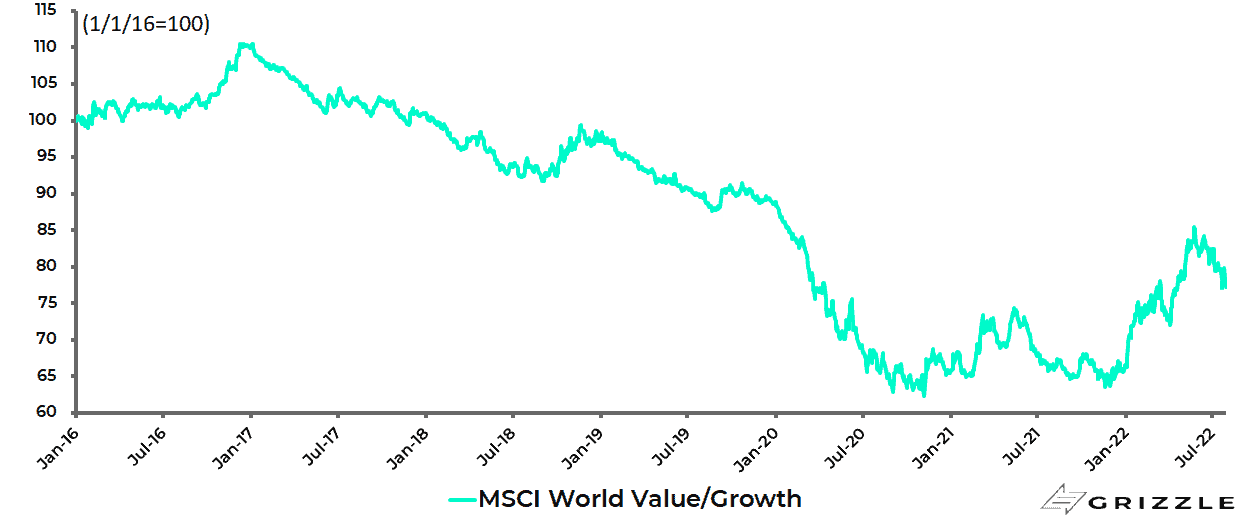

The MSCI World Value Index has underperformed the MSCI World Growth Index by 9.6% since late May.

MSCI World Value Index relative to Growth Index

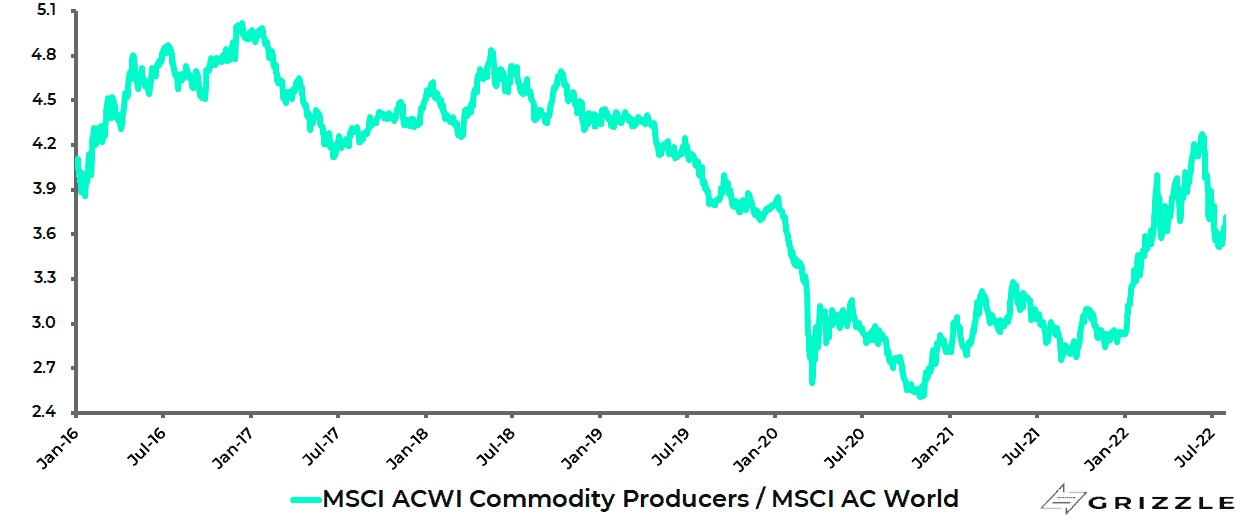

While the MSCI ACWI Commodity Producers Index has underperformed the MSCI AC World Index by 13% since mid-June.

MSCI ACWI Commodity Producers / MSCI AC World

Still, this writer would make a distinction between oil and copper as the latter has historically been much more cyclical and does not have the same positive gearing to rising geopolitical concerns.

True, copper also has the added positive of gearing to the EV story, though even EV demand can fall victim to slowing economies.

Staying on the subject of energy, it was interesting to read ExxonMobil’s Chief Executive Officer, Darren Woods, quoted recently saying that he expected the oil price to continue to rise “until it spurs renewed investment in output”, citing the famous adage that “the cure to high prices is high prices” (see Financial Times article: “ExxonMobil chief predicts continuing surge in oil markets”, 28 June 2022).

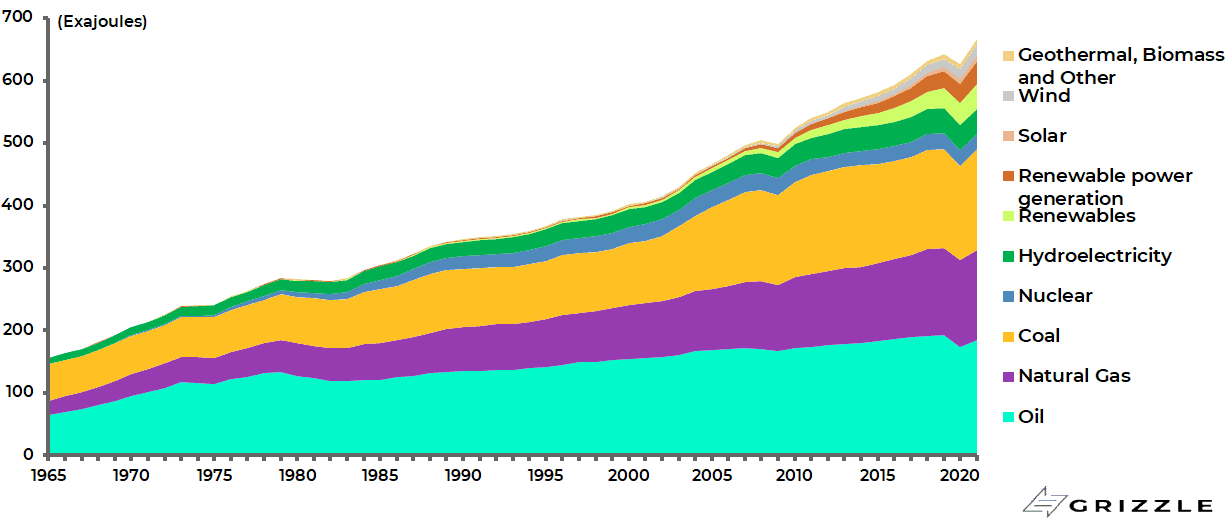

This makes complete sense, and highlights again the absurdity of last year’s climactic frenzy to curb fossil fuel production while failing to focus on the issue of continuing robust demand for fossil fuels, a demand again confirmed in the latest BP Statistical Review of World Energy report published on 28 June.

The BP energy book shows that global primary energy demand increased by 5.8% last year, surpassing the 2019 level by 1.3%.

While fossil fuels still accounted for 82% of total primary energy consumption in 2021, though down from 85% five years ago.

World primary energy consumption by type

It is also good to see some oil and gas executives start to take a more assertive stance and stop apologising for what they are doing, which has been the self-defeating stance of many of their number in the recent past, most particularly those based in Europe.

Hey Oil Demand, Did you Forget About China?

The other point, as regards current cyclical concerns on the demand destruction theme, is that investors should remember that there is always the potential for demand in China to recover.

In this respect, there is no sign as yet of an end to the Covid suppression policy but the shortening of quarantine for those entering China from 14-21 days to seven days in late June did come as a complete surprise and must reflect a concession to the lobbying of multinationals based in China.

Or at least such is the assumption.

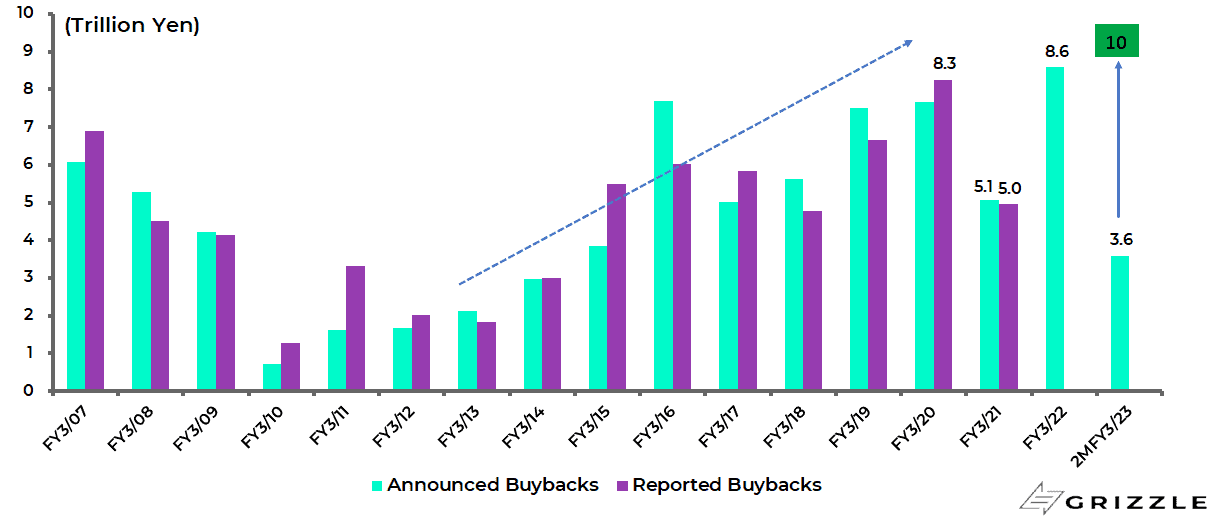

Don’t Ignore the Japanese Share Buyback Boom

Staying in Asia, it is also worth highlighting the continuing share buyback boom in Japan.

Corporates announced Y3tn of buybacks in May, the biggest monthly total ever, and are more or less on track to reach more than Y10tn this fiscal year following the record Y8.6tn last fiscal year.

Annual buybacks in Japan have now more than quadrupled since the launching of Abenomics back in late 2012, rising from Y1.8tn in FY3/13 to Y8.6tn in FY3/22.

Topix reported and announced share buybacks

The rising buybacks are the result of cheap valuations and cash-rich balance sheets as companies seek to bolster shareholder returns.

This is one reason why this writer remains favourably disposed towards Japanese equities with the major problem remaining that Japanese institutions, as opposed to Japanese corporates, do not want to buy their own stock market.

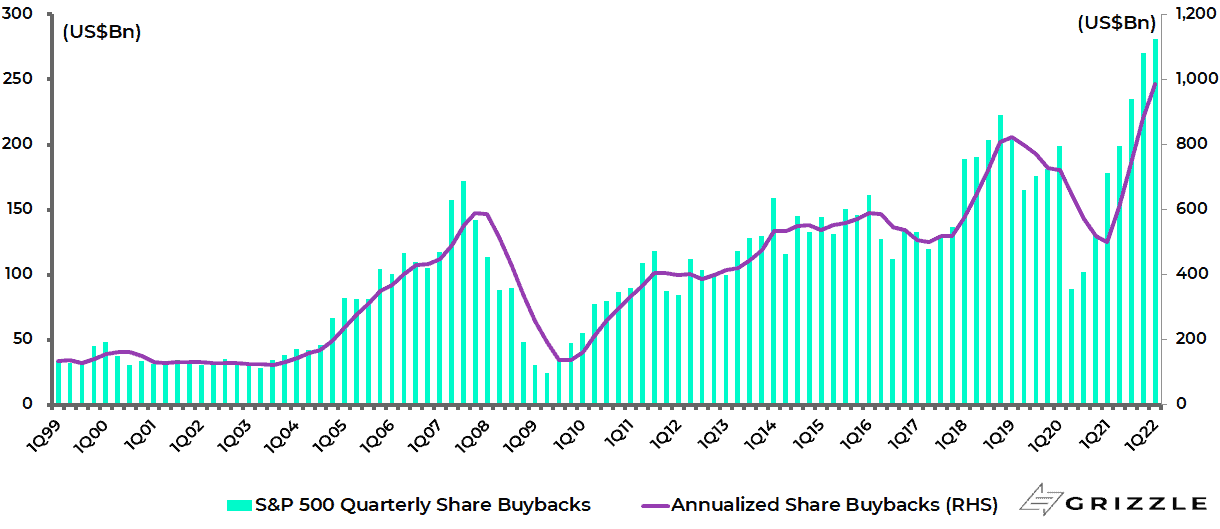

Meanwhile, it is worth contrasting again the dynamic behind the Japan share buybacks and what has happened in America over the past many years.

Japanese companies are increasingly using excess cash on their balance sheets to buy back shares because they are undervalued, as activists have long wanted them to do.

By contrast, in America share buybacks have tended to be pro-cyclical.

The more share prices rise, the more buybacks rise and the more corporates have borrowed money to finance those buybacks, thereby boosting return on equity, a measure by which many executives are compensated.

But when stock markets go down history suggests that share buybacks collapse even though the decline in share prices should make share buybacks more fundamentally attractive.

This is at least what happened after the 2007-2008 stock market collapse during the global financial crisis.

Will it happen again?

S&P500 quarterly share buybacks

This time around the financial engineering-driven strategy of borrowing money to buy back shares to boost RoE also threatens to be undermined by the higher interest rates which could become more permanent if the US is moving into an era of structurally higher inflation.

Loosening of Yield Curve Control in Japan Would be Bullish for Stocks

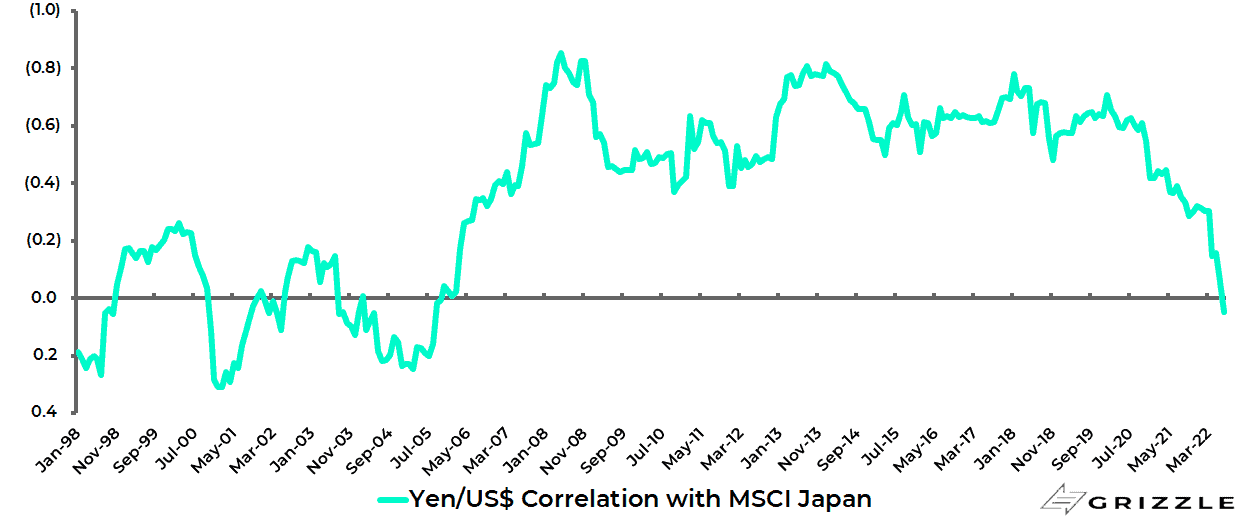

Returning to Japan, there has been a breakdown of late in the traditional correlation whereby a weakening yen has been a positive for Japanese equities.

During the 2012-15 yen devaluation cycle, the MSCI Japan had a 0.8 negative correlation with the yen. But the correlation has since collapsed during the past five years to a positive 0.05.

Yen correlation with MSCI Japan (2-year rolling correlation of monthly returns)

So the recent weakness of the yen, driven by Bank of Japan Governor Haruhiko Kuroda’s continuing defense of yield curve control, has not proved positive for Japanese stocks in recent months.

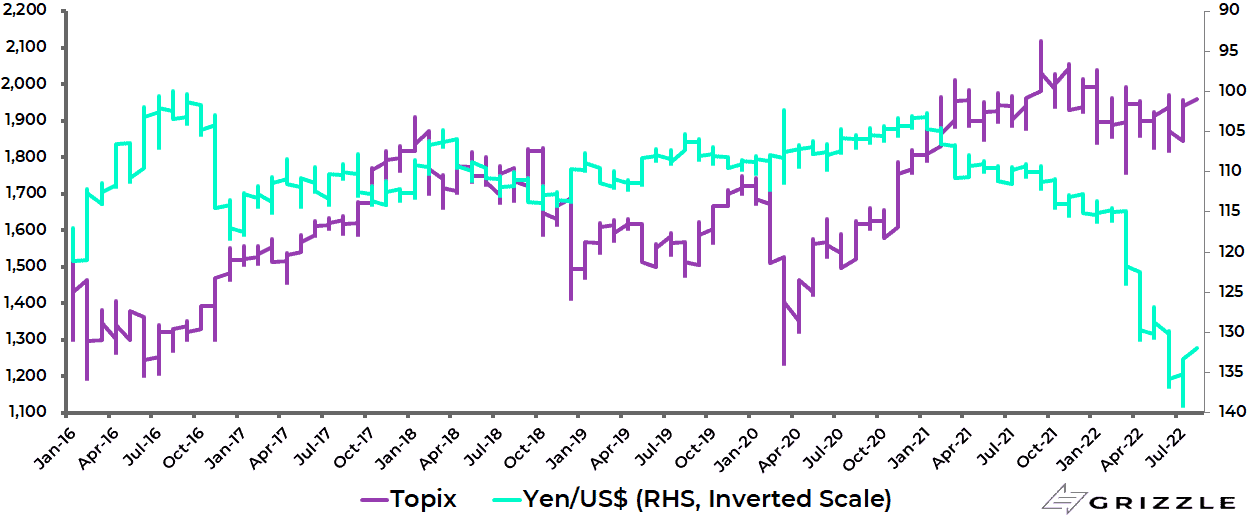

The Topix has declined by 1.6% year to date and is down 7.5% since mid-September 2021, while the yen has depreciated by 12.8% against the US dollar so far in 2022 and is down 17.3% since mid-September 2021.

Topix and Yen/US$ (inverted scale)

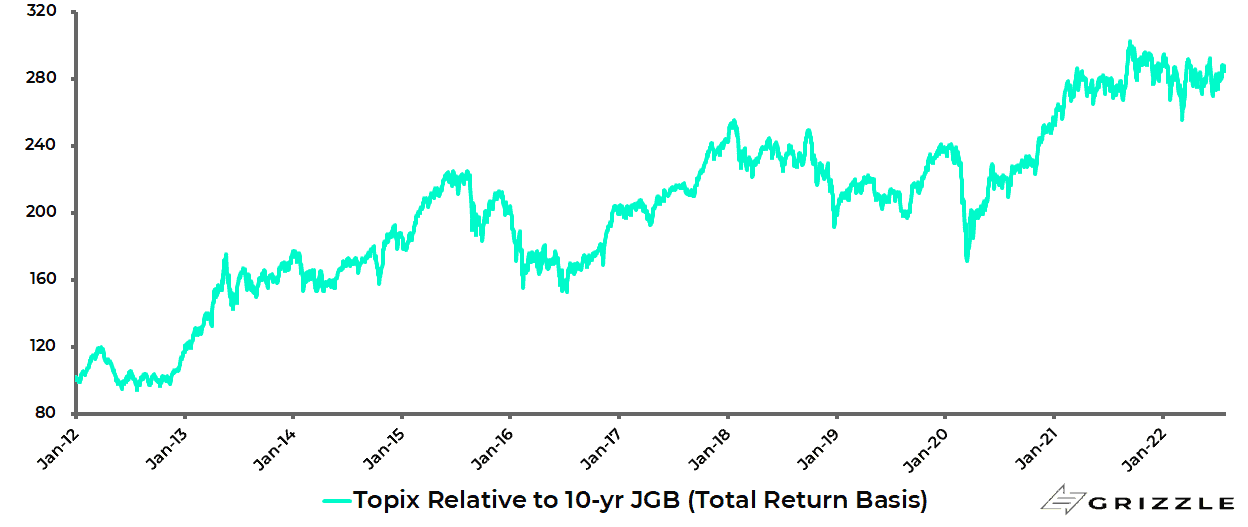

The irony is that if Kuroda adjusted the policy or, better still, abandoned it, the outcome could give a positive signal to Japan’s institutional investors that the deflationary trend had bottomed out, while also relieving banks of the drag from negative rates.

That could just be the sort of signal needed to persuade Japanese institutions finally to start to reallocate out of JGBs into Japanese equities.

As noted here on numerous occasions previously, this is something they already should have done as the Topix has now outperformed the 10-year JGB by 194% since November 2012 shortly before the launch of Abenomics, and this is measuring the performance of a JGB whose price is being artificially supported by the central bank.

Topix relative to 10-year JGB (total return basis)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.