There is no doubt that Wall Street has in the relief rally underway since late June been in an awful hurry to price in the peaking out of inflation and the end of Fed tightening.

Fed tightening expectations peaked in mid-June at 4% in early 2023 while the money markets are now discounting 25-50bp of easing next year after the federal funds rate peaks at an assumed 3.5-3.75% in March 2023, or 125bp above the current level following the 75bp hike in late July to 2.25-2.5%.

Meanwhile, as regards the current state of the American economy, it is hard to make a conclusive case as yet that it has entered a significant downturn.

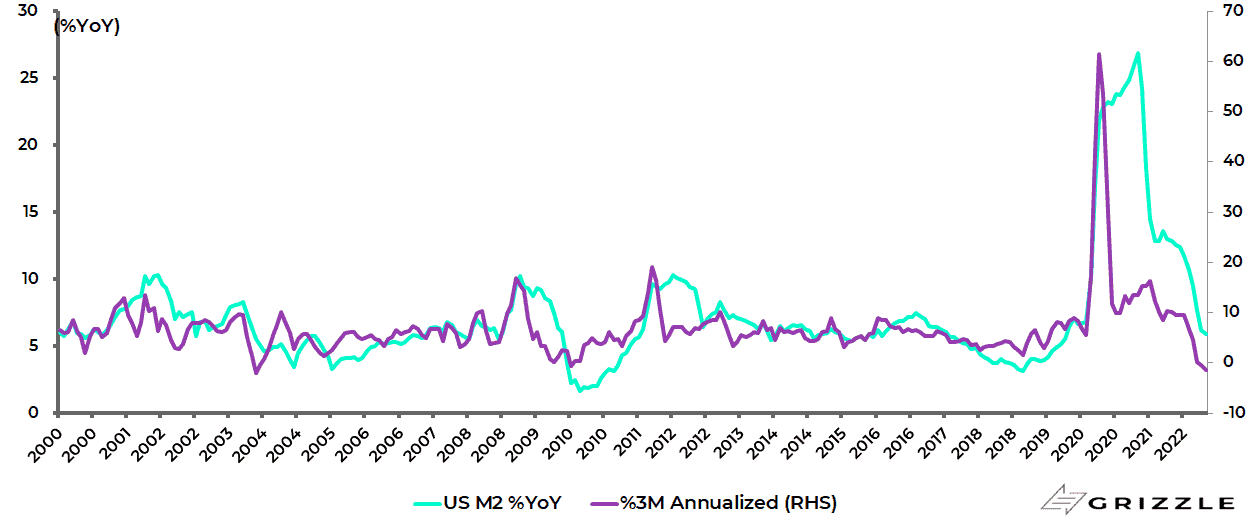

Still, the more broad money supply growth collapses, and the latest M2 data shows a further decline, the more it highlights the likelihood of growing economic weakness in the American economy next year given the natural lags.

US M2 rose by only an annualised 0.6% in the six months to July while, on a year-on-year basis, M2 growth slowed further from 5.9% YoY in June to 5.3% YoY in July.

US M2 growth

The problem for financial markets right now is that the lack of convincing evidence that the economy is turning down, in the context of a still ostensibly tight labour market, makes it hard for the Fed to justify a significant change of language as yet.

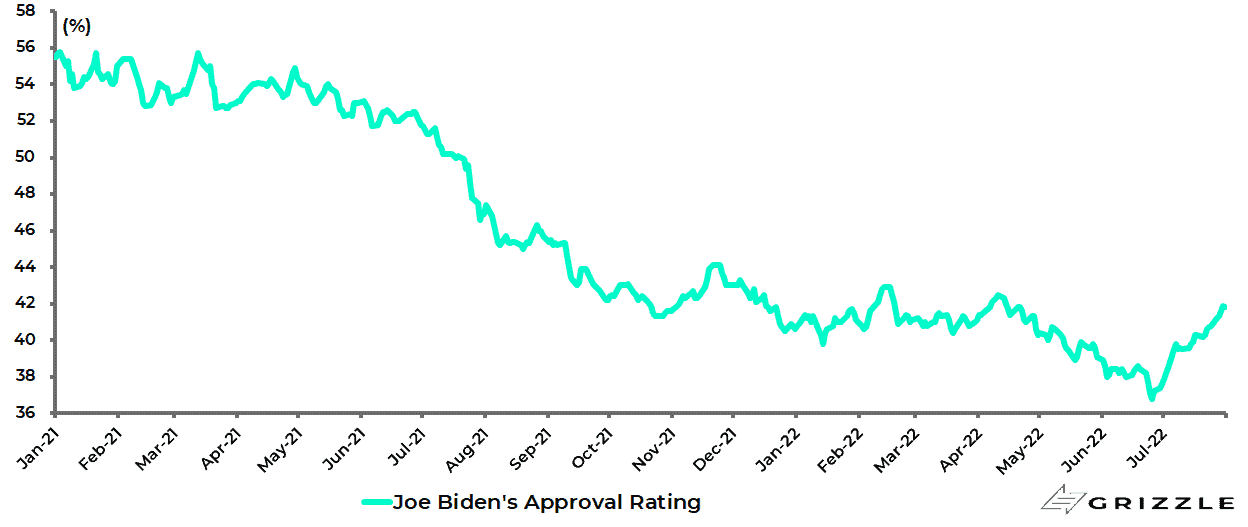

Meanwhile, the political focus remains on the inflation issue with prices remaining the number one issue for the American electorate, while Joe Biden’s popularity rating has remained at low levels, though there has of late been a bounce off the bottom.

The latest Fox News poll conducted on 6-9 August showed that 71% of respondents disapprove of the way Biden is handling inflation.

Biden’s average approval rating has declined from 42.5% in early May to a low of 36.8% in late July and is now 41.8%.

President Joe Biden’s approval rating

Fed Can Keep Pushing While the Bond Market is Healthy

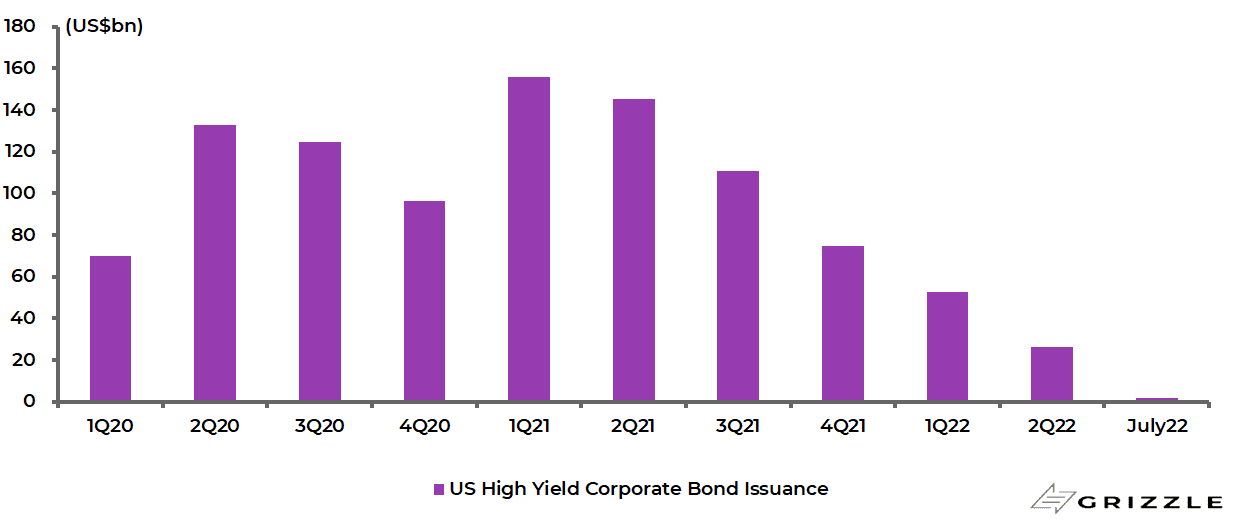

Meanwhile, with stocks behaving better of late, there is also less reason in the near term for the Fed to back off while credit markets have, not yet at least, gone completely on strike.

Thus, while junk bond issuance has declined dramatically, it has not yet stopped altogether.

US high-yield corporate bond issuance has fallen from a peak of US$156bn in 1Q21 to US$26bn in 2Q22.

US high-yield corporate bond issuance

Falling Inflation Expectations Could Give the Fed Cover to Pivot

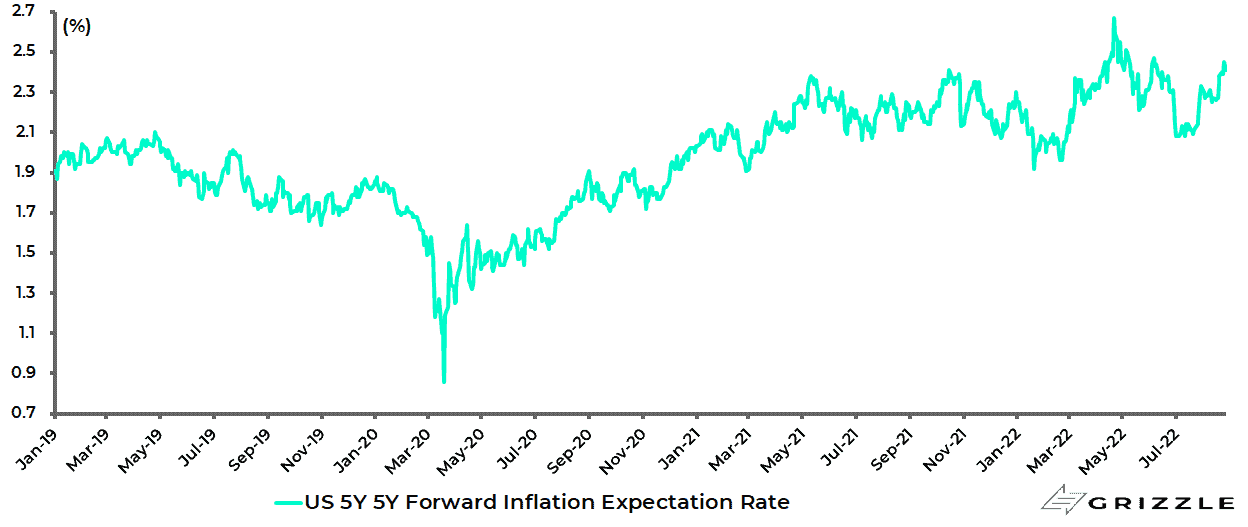

In view of the above, how could the Fed justify a change in language to a more doveish posture, assuming it wanted to, in the absence of a clear deterioration in the labor market.

The 5-year forward inflation expectation declined from a peak of 2.67% in late April to a low of 2.08% on 11 July though, unfortunately for those looking for such a doveish pivot, it has since risen back to 2.41%.

US five-year five-year forward inflation expectation rate

Source: Federal Reserve Bank of St. Louis

The argument would be that because there is now more evidence that long-term inflation expectations have been re-anchored as a result of the much more hawkish Fed, with 75bp of tightening in each of the last two meetings, there is now more room for the Fed to ease up.

This writer is not expecting such a move in the immediate future but it is probably coming at some point.

It is certainly a reason to continue to keep an eye on inflation expectation measures.

This writer has highlighted on several occasions in the past that the importance attributed by modern-day central bankers to market-driven inflation expectations is academic gobbledygook and, to be fair to the Fed, its own research department published a paper arguing exactly this point last September (See Fed staff working paper: “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)”, 23 September 2021).

Still, that does not mean that market-driven expectations are irrelevant for markets.

They are clearly very important as the Fed thinks they are important and thus can drive the Fed’s policy reaction function.

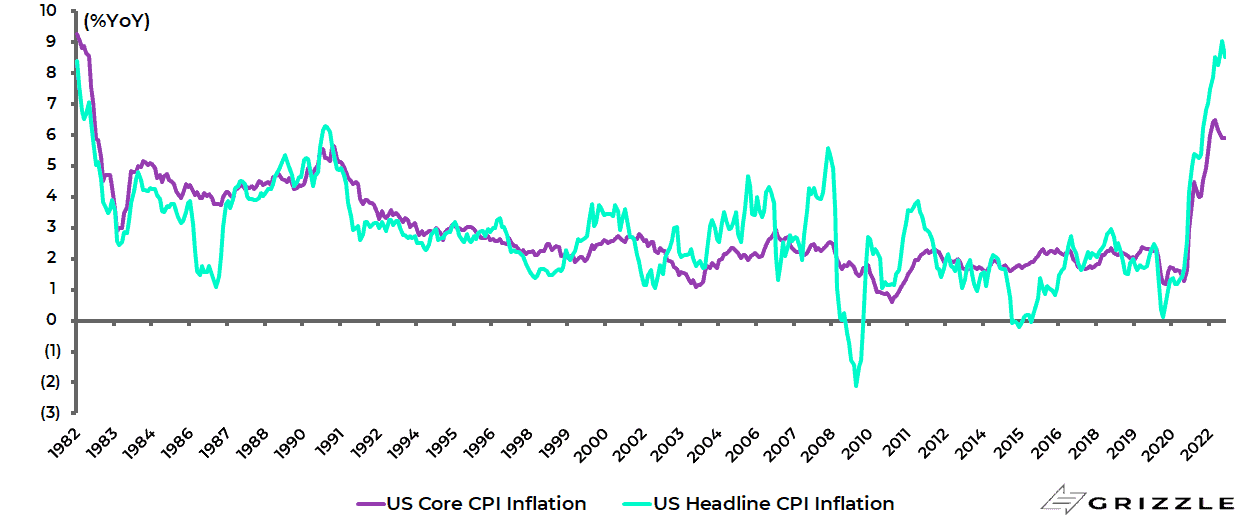

In this respect, what those in the markets betting on the “inflation has peaked” narrative would love to see is the Fed in future placing more and more verbal emphasis on falling inflation expectations, assuming optimistically that trend resumes, and less and less on “backward looking” inflation data even though the last CPI report on 10 August of 8.5% YoY was still a huge 6.5 percentage points above the Fed’s 2% target.

US CPI inflation

Meanwhile, the key medium-term issue remains whether the Fed will stay the course until inflation is below 2% or whether it backs off long before that.

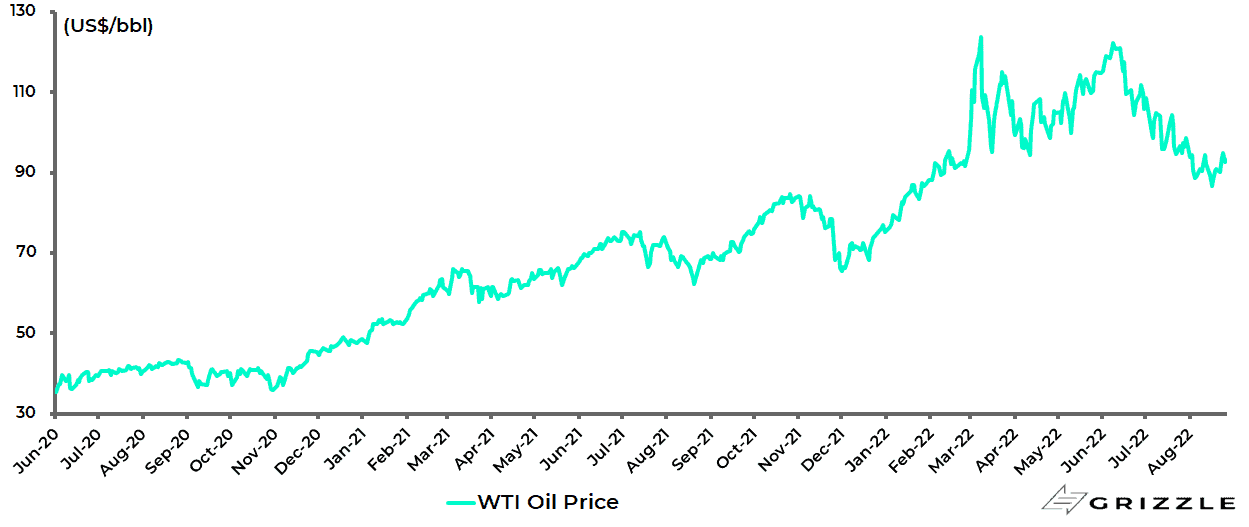

US headline inflation may have peaked for now, helped by the 25% decline in the crude oil price since mid-June.

WTI crude oil price

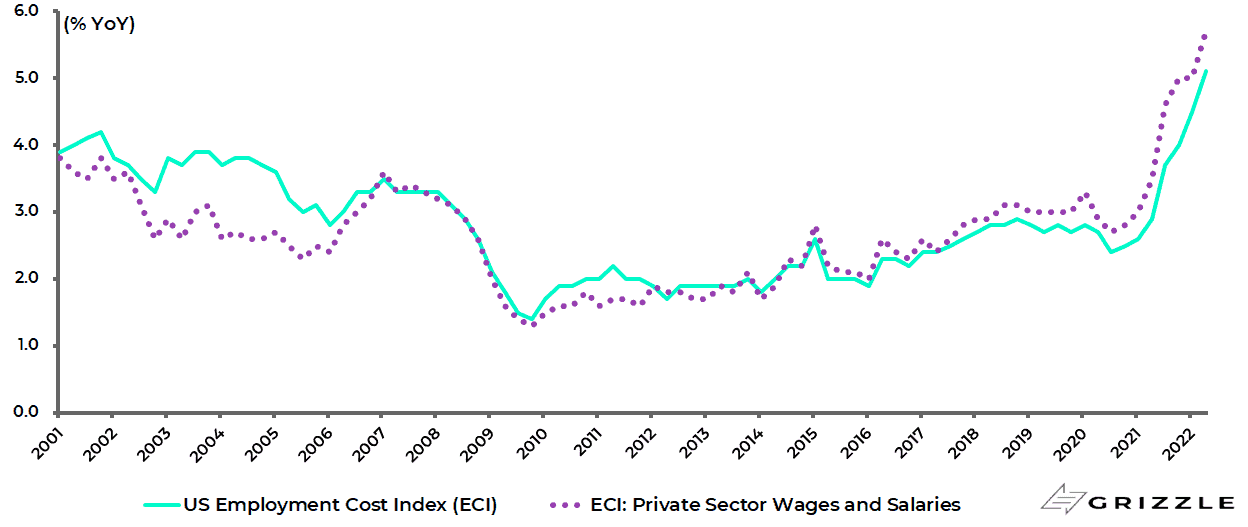

But that does not mean that it is falling in a straight line to 2%, most particularly with no evidence of a reduction in wage pressures with the employment cost index rising by 5.1% YoY last quarter.

US employment cost index

Core PCE inflation at 4.6% YoY in July was also still 2.6 percentage points above the Fed’s target while a rebound in oil prices would create concerns about a rebound in headline inflation.

And the Fed, in view of its policy errors of the past two and more years in terms of failing to anticipate the surge in inflation, no longer has the luxury of only focusing on core inflation.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.