The “phase one” trade deal between the U.S. and China, which was finally signed on Wednesday in Washington amid much Trumpian razzmatazz, has as expected proved positive for stocks. This is because it includes some element of a tariff rollback as well as the anticipated agreement on currency-related issues, in terms of a mutual agreement not to engage in competitive devaluations.

It is also the case that the U.S. has stated that all remaining tariffs will be removed if a “phase two” deal is agreed in the future. There are still tariffs of 7.5-25% being imposed on US$370 billion worth of Chinese exports.

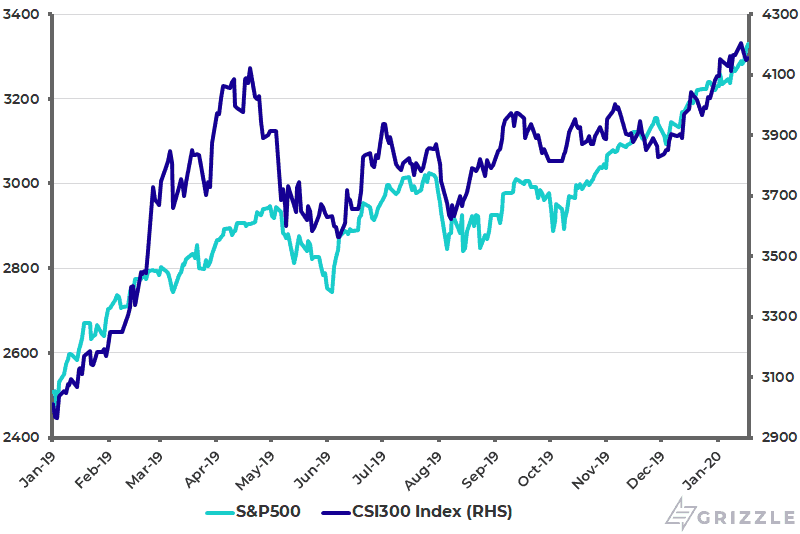

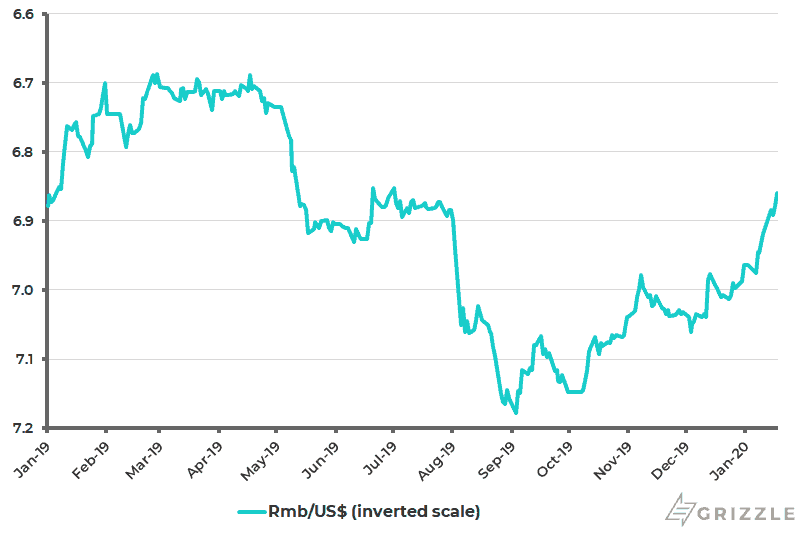

The last point allows markets to keep hoping for more good news. Meanwhile the S&P 500 is up by 5.1% and China’s CSI300 by 6.8% since the terms of the deal were first announced on Dec. 13 (see following chart). The renminbi has also appreciated by 2.2% against the U.S. dollar since then (see following chart).

S&P500 and CSI300 Index

Renminbi/US$ (inverted scale)

A Win for Trump

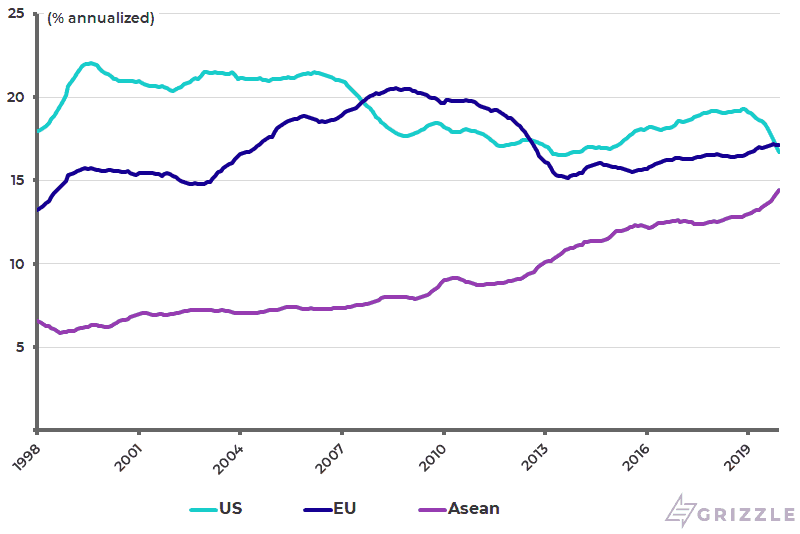

With the impeachment noise about to escalate again, it is clear that Donald Trump needed a “win” just as much, if not more so, than the Chinese. It is certainly the case that the importance of the U.S. export market to China is nothing like it used to be. America’s share of annualized China exports has declined from 19.3% in 2018 to 16.7% in 2019 (see following chart).

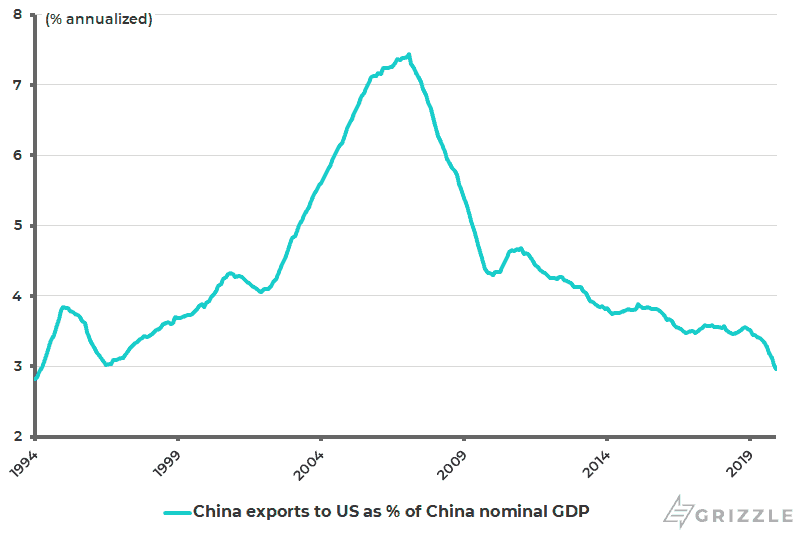

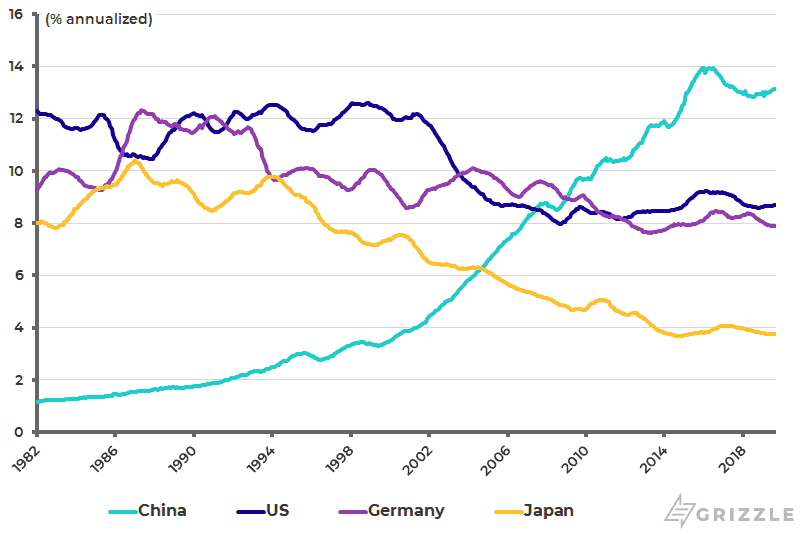

While Chinese annualized exports to the U.S. as a percentage of China nominal GDP have declined from 7.4% in February 2007 to 3.0% in December 2019, the lowest level since 1994 (see following chart). Yet despite this decline, China’s share of world exports has barely declined. China’s share of world exports rose to a peak of 13.9% in 2015 and was still 13.1% in the 12 months to September 2019, compared with 8.7% for the U.S. and 7.9% for Germany (see following chart).

Share of China Exports by Region

China Annualized Exports to U.S. as % of China Nominal GDP

China’s Share of World Exports Compared With U.S., Japan and Germany

China the Enemy

If such is the case, what will concern Beijing more than the trade issue is the growing trend in Washington in the past two years to treat China as an enemy, as typified by the speeches of Trump’s immediate subordinates like Vice President Mike Pence and Secretary of State Mike Pompeo.

Still, as written here on numerous occasions before, Trump is not one of those national security zealots. Indeed the Chinese leadership will be grateful that Trump has not used the recent demonstrations in Hong Kong as leverage in the trade negotiations. In this respect, Beijing will hope that the “phase one” agreement will give Trump a “win” domestically which could in turn lead him to put pressure on the likes of Pence and Pompeo to ratchet down their anti-China rhetoric.

That would leave the Democrats as the main driver of anti-Beijing sentiment and clearly the Democrats have become much more anti-China since Hillary Clinton ran as the pro-free trade pro-Beijing candidate in the last presidential election. In this respect, it is as if the “liberal” side of American politics has suddenly woken up and discovered that China is not a democracy, all of which is why Beijing would probably prefer Trump being re-elected for all his seeming chaotic unpredictability. The same calculation doubtless applies to Russian President Vladimir Putin and North Korean leader Kim Jong-un.

North Korea Wants Attention

Speaking of Kim, North Korea was back in the news late last year with reports of a “very important test” on a North Korean missile launch site in December. Recent events concerning Iran have distracted attention of late. But expectations among experts had been for Pyongyang to manufacture a crisis before the end of 2019 if America did not offer some concessions on sanctions. In this respect, the North Korean leader had stated in a speech in April that North Korea would resume its nuclear activity unless America offered some concessions by the end of last year. The North Korean offer seems to have been some form of partial surrender of the nuclear program in return for the end of sanctions.

In the event, the North Korean regime has, for now at least, not yet made such a move. Still the renewed aggressive demeanor from the North is no surprise since America has not, in public at least, departed from its formal stance that no concession is possible on sanctions until North Korea shuts down all its nuclear program. With the significant and surprising (to Washington) progress made by North Korea in developing its nuclear and intercontinental ballistic missile (ICBM) capability in recent years, such a concession was never realistic. In fact it would be suicidal from the standpoint of Kim. This is why it would have been disappointing to Kim that no concession has been offered by the U.S. despite the renewed hopes generated by the Donald’s historic walk into Korea’s DMZ at the end of June 2019.

Meanwhile it is surely the case that Trump, who is street smart if no intellectual, must understand that Kim would never agree to give up the nuclear program in its entirety. But for now my base case is that some kind of deal on North Korea would be agreed in the first term of Trump’s presidency, is looking wrong. This again raises the risk that, if the ever-mercurial Trump realizes a deal is no longer possible, he may refocus on military options in line with his renewed rhetorical references to “rocket man”.

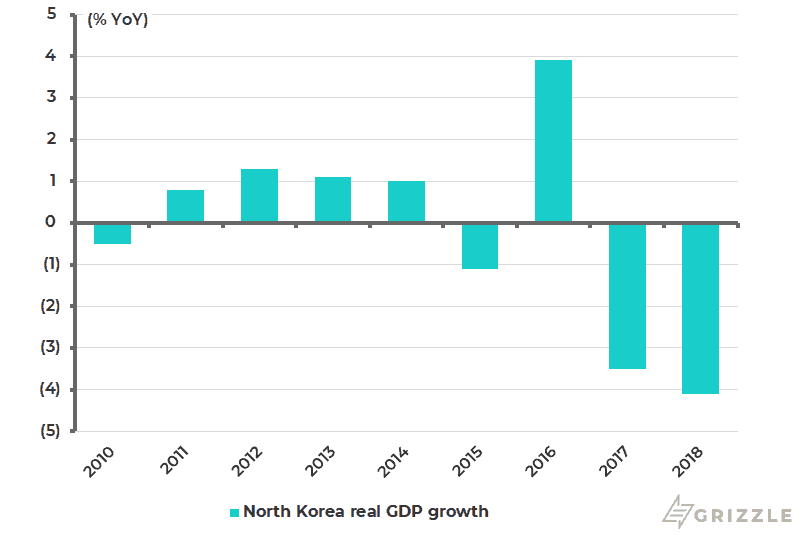

Meanwhile, Kim is anxious to provoke America’s attention again not only because he wants his country’s nuclear status to be acknowledged but also because the U.S. sectoral sanctions introduced in March 2016 have caused economic growth to stall badly after the relative boom seen in the first four years of his rule which began in December 2011, as he gave greater freedom for the market economy to operate bottom up.

North Korea Real GDP Growth Estimated by Bank of Korea

What Will Kim Do Next?

How might Kim now manufacture a crisis in the hope of attracting Trump’s and the world’s attention? One sure way would be to launch a real ICBM. This could be done in one of either of two ways. One option would be to shoot it straight up into space which means it would fall back to near where it is launched. Another more risky way would be to aim for a target in the Pacific which would be very provocative for both Japan and America. This is because the missile would fly over Japan and be heading in America’s direction.

Another option would be another nuclear test. Remember that the last one was in September 2017. This, however, would have the drawback of annoying China which has in the past signalled its clear displeasure with North Korea’s nuclear tests. There were six nuclear tests in the period between 2006-2017. Indeed this would risk reviving the united front against North Korea which was briefly the case, in terms of the US-China relationship, between August 2017 and early 2018. By contrast, China does not appear to have an issue with the North’s ICBM program. There is not the same risk of Chernobyl-style contamination spreading into neighbouring China as in the case of a nuclear test gone wrong.

The other potential option open to the North would be a more mundane conventional military attack on a South Korean target, similar to the attack on the South Korean vessel in 2010 which killed 46 people. The risk of such a move is that it would alienate public opinion in the South whereas right now South Korean President Moon Jae-in remains ultra-doveish on the North Korea issue.

One Fact Remains

But amid such theorizing, the one definite fact is that a plenary meeting at the end of last year of North Korea’s ruling party Central Committee resulted in a formal withdrawal of the North’s self-imposed moratorium on nuclear activity. This moratorium was announced in April 2018 when Kim was hoping that a real deal could be negotiated with the unconventional American President.

If such a re-escalation happens, it is still the base case that Trump is more likely to end up doing a deal with Kim on the nuclear issue rather than attacking militarily. This is because the track record suggests that the transactional focused Trump is not comfortable with military escalation.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.