Inflationary pressures have continued to show up in the official data even as the bond market has managed to rally of late.

The latest US inflation data released on Thursday shows that US headline CPI inflation rose from 4.2% YoY in April to 5.0% YoY in May, the highest level since August 2008, while core CPI inflation rose from 3.0% YoY to 3.8% YoY, the highest level since June 1992.

US CPI inflation

Yet the 10-year Treasury bond yield declined by 6bp on the day of the release to 1.43%, the lowest level since early March, and is now 1.45%.

US 10-year Treasury Bond Yield

The bond rally, in the face of the strongest core inflation data in 29 years, may be somewhat bizarre.

But it is good news for the Federal Reserve in that it signals, for now at least, that markets have calmed down about inflation concerns on the view that the higher inflation primarily reflects a base effect which peaked in May.

The base effect will start to diminish from July in the case of the core CPI, as the MoM increase peaked last year at 0.5% MoM in July 2020 and slowed to 0.3% in August and 0.0% in December.

Meanwhile, if low bond yields reduced the near term pressure on the Fed, the irony is that higher Treasury bond yields could be viewed as a symptom of success, in terms of reflecting economic recovery while also providing an incentive for banks to lend since banks are in the business of borrowing short and lending long.

Still many modern central bankers remain wary of higher bond yields.

For otherwise why is the Bank of Japan still engaging in yield curve control and why does the ECB seem to be practicing closet yield curve control in terms of targeting nominal bond yields in its asset purchases?

The advocacy of yield curve control, and indeed the practice of it, reflects an obsession with managing monetary policy through interest rates as opposed to managing the quantity of money as happened during the Volcker era in the late 1970s/early 1980s.

This, from a classic monetarist standpoint, means dealing with the symptoms (i.e. interest rates) not the cause (money supply growth).

If monetarism reigned supreme when former British Prime Minister Margaret Thatcher and her comrade in arms former American president Ronald Reagan were around, it subsequently lost a lot of its credibility when financial deregulation led to a questioning of monetarism’s traditional tenets in terms of the difficulty of defining ‘money’.

And certainly, it proved more important to be looking at credit, and the various components of credit, than ‘money’ in the lead up to the 2008 global financial crisis.

This writer is certainly not a hardcore monetarist and is influenced more by the Austrian economists’ obsession with credit.

Still, the reaction against ‘money’ has gone way too far as reflected in the almost total ignoring of money supply data by economists in the US when it is published in contrast with the obsessive focus on the same data back in the late 1970s and early 1980s.

It remains the case that there is a long-term relationship between broad money supply growth and nominal GDP growth even if there can be a considerable lag.

For example, US M2 growth accelerated from 6% YoY in 3Q08 to 9.7% YoY in 1Q09, before slowing to 1.9% YoY in 2Q10, while nominal GDP declined by 3.1% YoY to a then bottom in 2Q09 and was up 4.6% YoY in 3Q10.

US Nominal GDP and M2 Trend

This is one reason why, after the base effect-triggered surge in inflation, the base case here remains for a further pickup in inflation over the next year and more in a post-pandemic era simply because of the expansion of broad money supply since last March which has already taken place, though clearly velocity remains a key variable.

Meanwhile, as regards the base effect, it is also worth noting that the Fed’s favourite inflation indicator, the core PCE inflation, rose from 1.9% YoY in March to 3.1% YoY in April, the highest level since July 1992.

Even assuming 0.0% MoM growth in May, core PCE inflation will remain high at 2.9% YoY.

US Core PCE Inflation

The laggard impact of monetary growth could lead to a pickup in US core CPI inflation to, say, the 4% YoY level later in the year which would certainly create a lot of inflation noise in markets in a post-pandemic world.

But the key issue remains how the Fed responds to such an outcome.

If it reverts to orthodox policies and resumes tightening in a response to a significant overshoot in its inflation forecast, which would definitely be the case in a 4% outcome, then the deflationary trend can resume, most particularly if the credit multiplier continues to fail to get traction.

But in a world where price controls are introduced in the US Treasury bond market, as would be the case with the implementation of some form of yield curve control, then the likelihood of regime change grows dramatically.

Consumers are Flush, Will they Spend or Work?

Meanwhile, one aspect of the likely ongoing inflation scare remains pent up demand in America.

It is worth stressing again the extent to which American households have been net financial beneficiaries of the pandemic.

US households have now lost US$366bn in personal income in the 14 months since the arrival of COVID and related lockdowns and received US$1.9tn more in transfer payments than the pre-COVID levels.

This is measured by comparing personal income/transfers over the 14 months to April 2021 with the pre-Covid level in February 2020.

US Personal Income and Savings

| US$bn, saar | Feb-20 (Pre-Covid) |

Apr-21 | Mar20-Apr21 (Average) |

Mar20-Apr21 Chg vs Feb-20 |

| Personal income (excl. transfers) | 17,373 | 17,943 | 17,060 | (366) |

| Personal current transfer receipts | 3,211 | 4,799 | 4,840 | 1,900 |

| Disposable personal income | 16,831 | 18,845 | 18,210 | 1,608 |

| Personal outlays | 15,442 | 16,030 | 14,823 | (722) |

| Personal saving | 1,389 | 2,814 | 3,386 | 2,330 |

| Personal saving/disposable income (%) | 8.3 | 14.9 | 18.6 | 10.3 |

Note: Personal income includes compensation of employees, proprietors’ income, rental income, interest and dividend incomes. Source: Bureau of Economic Analysis

One issue raised by this transfer payment windfall is whether there will be an incentive to return to work.

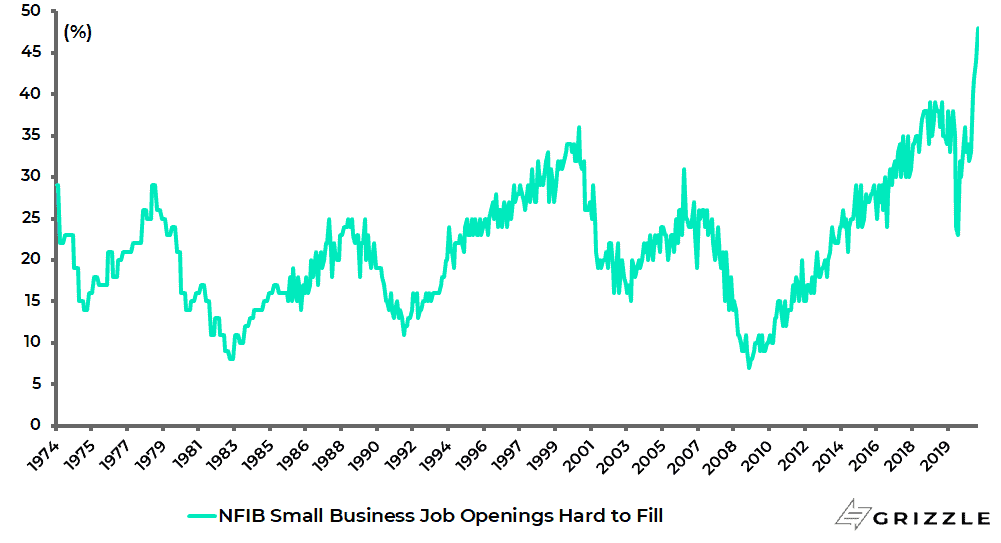

This continues to be reflected in the difficulty reported by small businesses in America finding labour.

Thus, the National Federation of Independent Business survey released in early June found that a record 48% of small business owners reported they could not fill job openings, and this data series goes back to 1974.

US NFIB Small Business survey: Job openings hard to fill

Remember that the unemployed are getting an extra Covid-related US$300/week from the federal government in addition to an average US$320 benefit provided by the states, though it should be noted that the extra Fed top-up is due to expire on 6 September.

It is also the case that 25 Republican-governed states have already announced that they will stop the supplementary federal unemployment benefits as early as 12 June precisely because they understand the obvious point that incentives matter.

In macroeconomic terms, these states account for 43% of the workforce or 38% of the economy.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.