September 2020 is shaping up to be the biggest month for tech IPO’s, initial public offerings, in the last decade.

Coming to the markets next is Sumo Logic, the latest software as a service (SaaS) company seeking to keep the growth streak alive with money from not only private investors but the public as well.

In this comprehensive guide, you’ll learn about the products, the company, and most importantly what the stock is worth.

Everything you need to make an informed investment decision on the first day of trading and beyond.

What Does Sumo Logic Do?

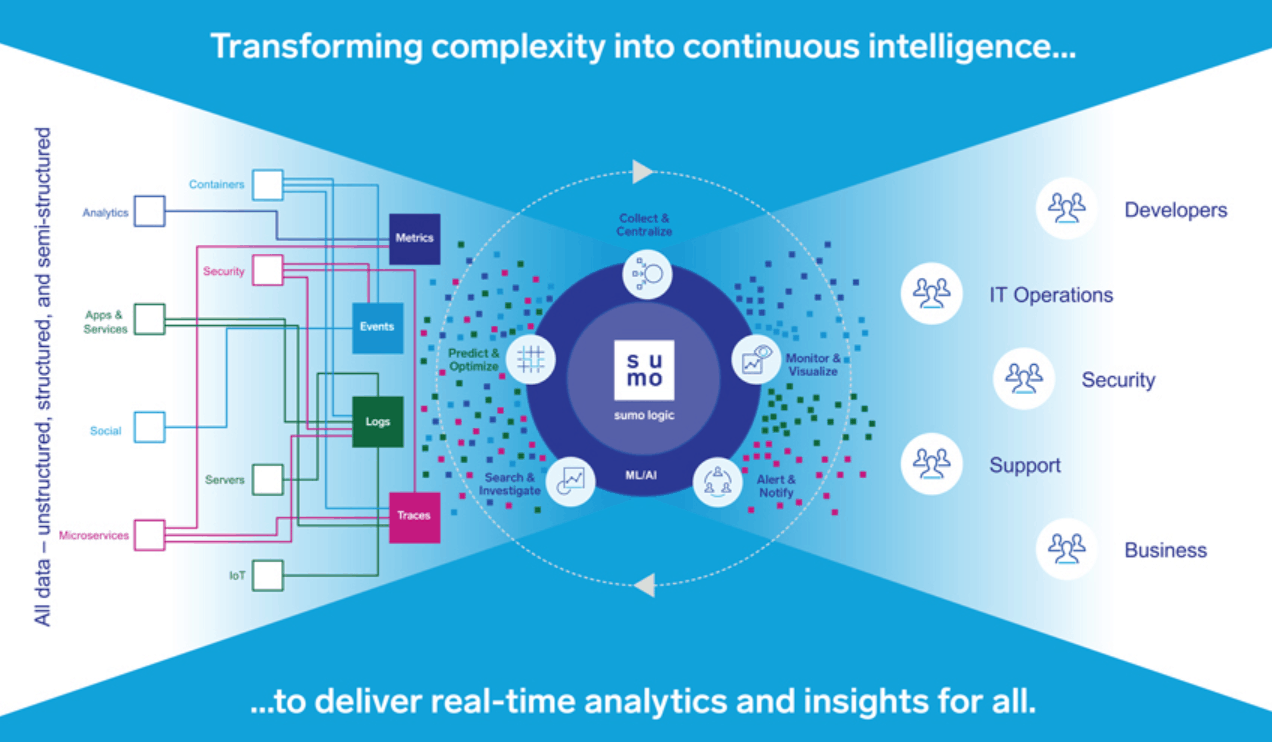

Sumo Logic is a cloud software analytics company that pioneered “Continued Intelligence”; enabling organizations to automate the collection and analysis of application, infrastructure, security and IoT (internet of things) data to provide actionable real time insights.

The company analyzes data utilizing proprietary machine learning technology to identify and predict anomalies in real-time, allowing users to get continuous insights.

Sumo Logic’s mission statement is that the company “empowers organizations to close the intelligence gap”

The company states intelligence gaps are a result of multiple disparate systems and departmental silos; the traditional analytical reporting systems add more noise rather than providing actionable insights.

Sumo Logic’s Continuous Intelligence Platform helps their customers:

- Monitor and troubleshoot their applications and their cloud and on-premise infrastructure;

- Manage audit and compliance requirements;

- Rapidly detect and resolve modern security threats; and

- Extract critical key performance indicators, or KPIs, from various types of machine data to gain visibility into customer behavior, engagement, and actions

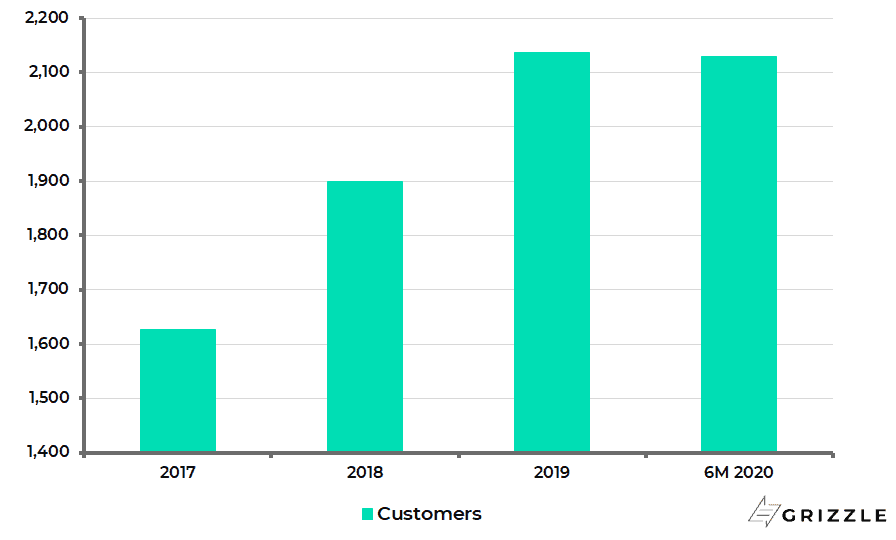

As of July 30, 2020 the company had 2,130 customers, which included Netflix, Salesforce.com, Twilo and PagerDuty.

The customer count has grown 30% since January 2018 (1,626), but has declined slightly in the last six months due to the Coronavirus pandemic.

How Does Growth Stack up?

From simply a size point of view, Sumologic is on the small side for a software company at only $170 million of revenue in the last 12 months.

The median for the cloud software group is $463 million.

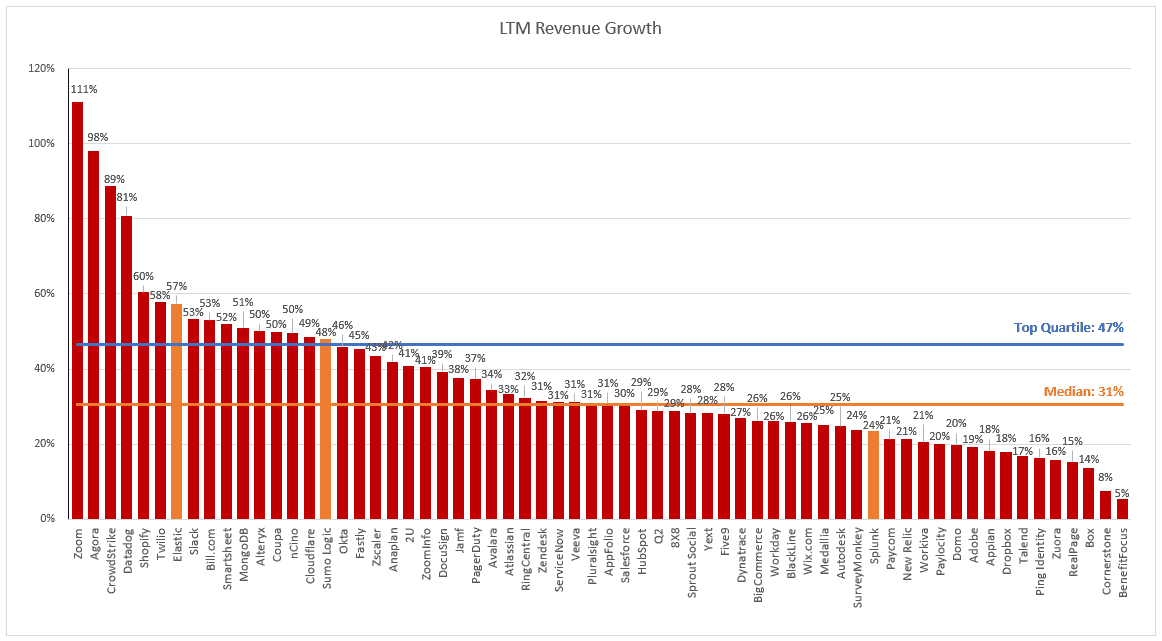

However since its founding in 2010, Sumo Logic has maintained a solid rate of growth and in the last 12 months grew revenue 48% over the prior year though has been slowing noticeably since the pandemic hit in March.

48% growth is solid and puts the company in the top 25% for software companies.

The two other yellow bars are Elastic and Splunk, two company’s offering similar services for reference.

Revenue Growth vs Peers

However, growth has slowed significantly in the last six months due to the Coronavirus, rising only 38% year over year.

The company even included an entire section in the IPO document listing all the ways the pandemic has negatively impacted customer growth and retention.

Its clear SumoLogic is not a pandemic proof stock like some other names we follow such as Shopify and Zoom.

Chief technology officers across the globe are scrutinizing every dollar spent right now and that has translated into some lost business and price cuts for Sumo Logic.

Growth will likely recover but SUMO’s vulnerability to economic swings should earn it a discounted multiple against software stocks that have largely been immune to COVID-19 spending cuts so far.

Customers

Where are the Profits and Does it Matter?

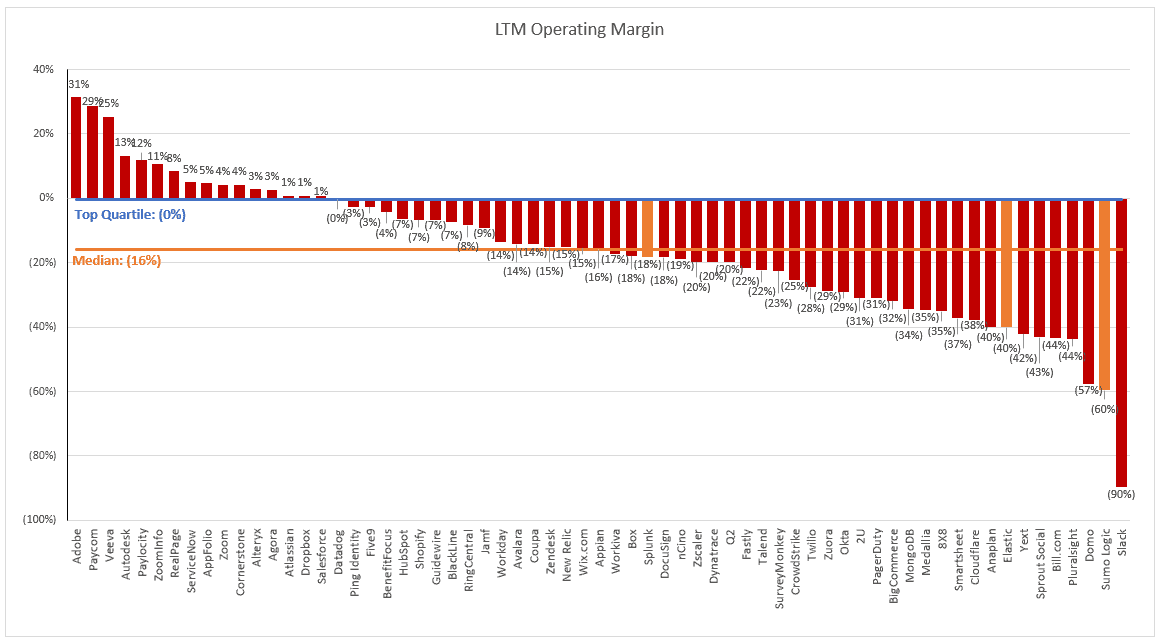

If you are at all familiar with high growth tech stocks, you won’t be surprised that Sumo Logic is far from showing investors any profits.

Yet even among money-losing hyper-growth software stocks, SUMO’s losses stand out.

The operating loss of 80% is second-worst in the entire group, only behind Slack which is quickly losing fans as losses continue even as the company grows.

Operating Margin (Last 12 Months)

Yes SUMO is small and growing quickly which usually means big losses, but the farther away profits are, the less certainty investors have that they will arrive someday.

Yet another factor that convinces us this stock deserves a discount.

The Big Reveal: What is the Stock Worth

Before we talk about what SUMO is worth investors need to understand these are not normal times in the stock market.

Multi-decade-low interest rates and massive stimulus from the government (checks in the mail) are sending stocks to levels not seen since the tech bubble of 2000.

In the short term (1-2 years) there is one price for SUMO which reflects the current market exuberance.

However, over the long term (3-10 years) there is another price which reflects the value of the cash this company will generate for you.

We are going to help you understand both.

Short Term Stock Price (Trading)

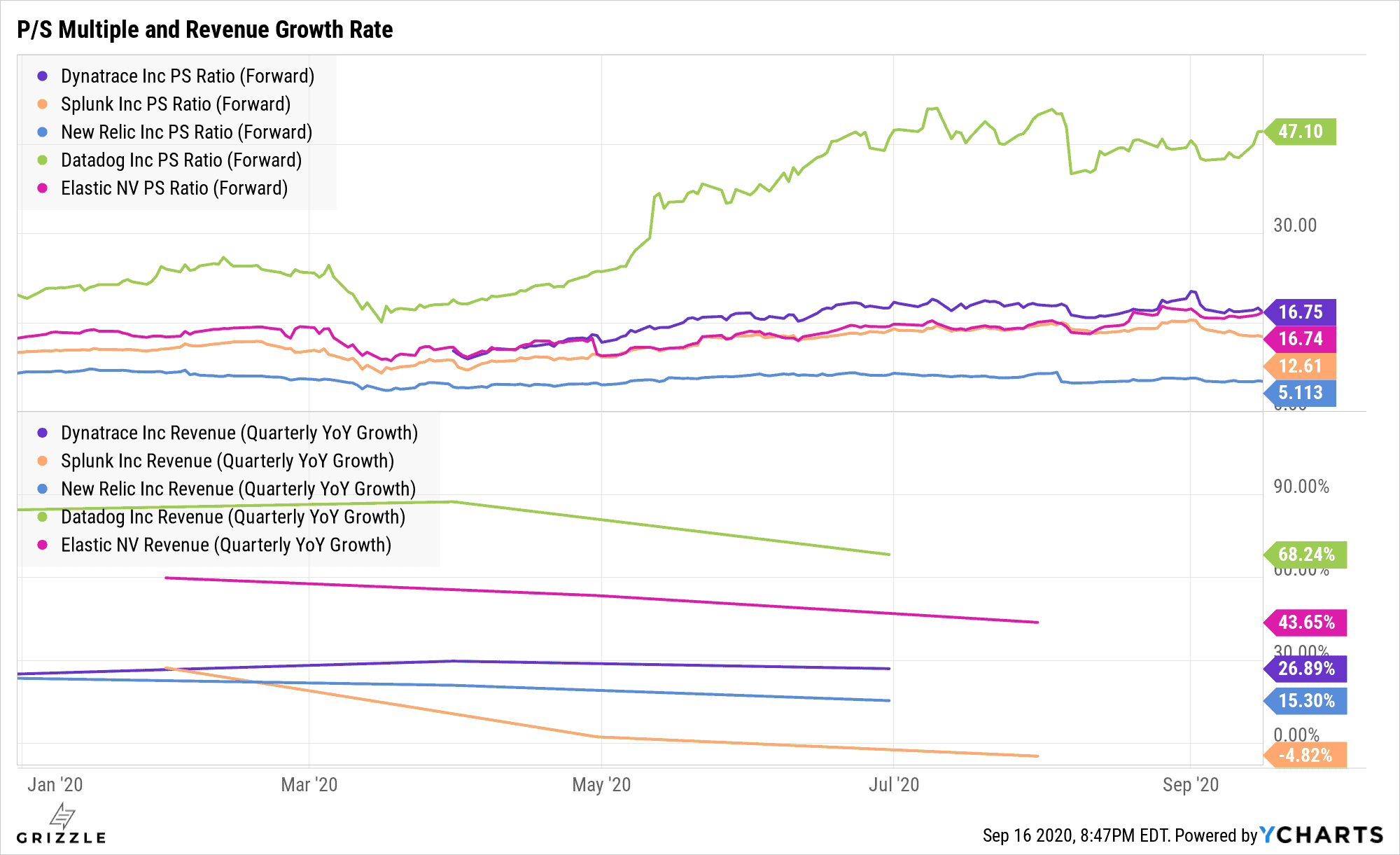

In the short term, SUMO will trade at a multiple of revenue in-line to other competitors offering similar products.

In the chart below competitors trade for between 5x and 47x revenue, a wide range.

Let’s narrow it down.

Multiples and Growth of the Peer Group

SUMO’s growth rate was in the top 25%, but has fallen over the last six months to only average.

The company also loses lots of money, more than almost any other public tech stock.

But in the current growth-obsessed market, investors are willing to overlook any weakness in profits or margins as long as the revenue growth is there.

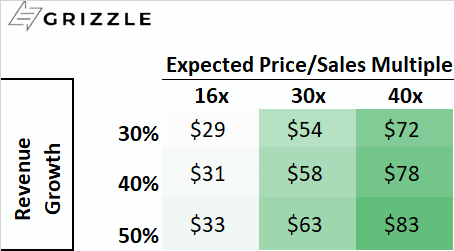

When you also throw in the recent IPO’s of Jfrog and Snowflake which set a new valuation record on September 16th we think its clear investors are in a giving mood which means SUMO will IPO at a high multiple of sales.

This would be a 145% increase from the latest IPO price of $22/sh.

Expected Day 1 Price Range

At such a high multiple SUMO will have to bring growth back up in line with last year at least (~50%) to avoid the multiple falling to 16x ($31/sh), in-line with competitors Elastic and Dynatrace.

On the flip side, if SUMO can reignite growth above 50% as the pandemic wanes, the multiple could increase closer to Datadog at 45x which would be a stock price of $85/sh.

All these prices look attractive, but remember, markets need to stay hot for investors to continue paying 20x,30x or even 100x multiples of revenue.

If economic factors turn consumers more cautious, multiples could easily fall 25%-50%, pulling high-flying stocks like SUMO back to reality.

With software stocks where they are today, we think buying SUMO below $40/sh could make you money in this market.

Any price above that we would sit on the sidelines for now.

The Long Term Price (Investing)

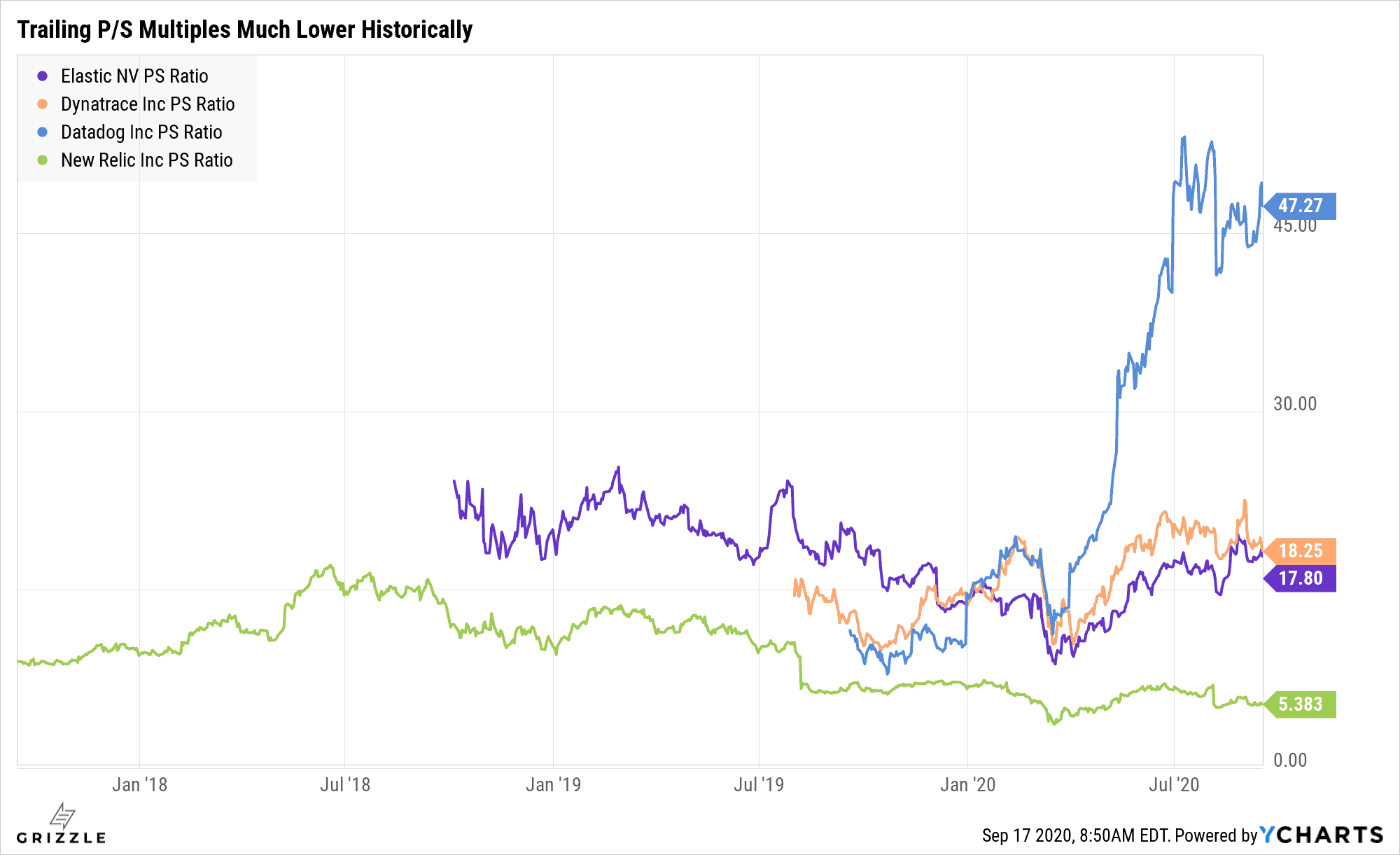

Over the long term, multiples will come back down as investors focus on cashflow once again.

In a more realistic market, SUMO is going to trade based on how growth and profits stack up next to close competitors.

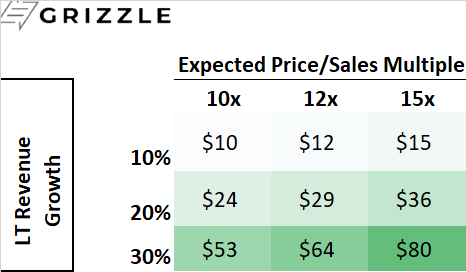

Competitor Elastic is larger, growing faster and generating better margins at 16x revenue, so in a perfect world SUMO would trade at a discount.

A 15x revenue multiple, or 50% less than our expected IPO multiple means the company would need to double revenue just to keep the stock flat.

If SUMO trades for $50 or above on day 1 and you buy it, you could potentially make no money on your investment for 10 years even if the company becomes what anyone would classify as a success.

As companies mature, the multiple investors are willing to pay falls which will put pressure on stocks like Datadog and potentially SUMO that trade at multiples way above what is typical in a normal market.

Multiples Lower in a Normal Market (Pre-2020)

This is why we can’t stress enough you should only be trading SUMO if you buy it for more than the IPO price of $20.

Longer-term investors who like the company’s chances of success should wait for pullback to $30/sh or below.

Long Term Price for SUMO

Sumo Logic is playing in a huge, fast growing market, so there is room for every player to grow.

The growth of data volumes generated by the internet is estimated to be over 50% a year for at least the next 5 years.

However as the market matures, a problem for another day, Sumo Logic may see growth slow faster than peers like Splunk who are bigger, growing faster and have a more entrenched product.

But in the here and now, Sumo Logic is shaping up to be another high flying software stock to add to the growth pile.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.